Nvidia mentions Netweb as only elite OEM partner for AI system

I saw the video however I wonder why only Netweb was mentioned. Its strange cos Dell India and Supermicro India also manufacture servers on which Nvidia GPUs are be hosted and have a lot wider adoption. Something extremely fishy here on how netweb is being propped up. Although they claim they have enterprise customers I don’t see any enterprise customers mentioned on their website. With enterprise customers they may be implying the likes of ONGC and PSU banks.

HP, VVDN, and Lenovo will start server manufacturing in India like netweb under PLI 2.0.

Others may manufacture servers with Nvidia GPU but may be not AI system chips. Like NVIDIA Grace Hopper Superchip. These are newest in line and are definitely going to be next big thing.

Netweb mentioned the adoption for these chips are low as of now and Netweb are already ready for that.

Typically, the server makers (like Dell/Lenovo/Hp etc…) work very closely with CPU makers like Intel/AMD on these server release every time there is a newer version of the CPU under work. Typical server launch cycle can be anywhere like 1-2 year. During this period, the CPU and server building company work very closely with each other. Server maker has access to the reference design of CPU and motherboard from the CPU player. One can easily appreciate the importance of confidentiality clauses when this happens.

Till now, nVIDIA was a major GPU player and both Intel/AMD server designs supported their GPUs. In fact, there isn’t much to do in a server to support GPU. It’s a plug and play kind of design to support most GPUs. At max the work needed from the server team is on GPUs thermal management (cooling the GPU by ramping the fan etc) side. That also is not always true as many GPUs are now coming with their own thermal management.

Now, this is where things get complicated, with nVIDIA showing ambition of it’s own CPU based on ARM architecture launched in 2023 Source : NVIDIA Introduces Grace CPU Superchip | NVIDIA Newsroom

This is a direct attack on the bread and butter of Intel/AMD server business.

It’s understandable NVIDIA need partners who can make servers for their CPUs. From what i understand and can see on plain google search usual server makers like Lenovo/Dell/Hp are not supporting the nVIDIA Grace CPUs as of today.

This is where Netweb has entered into picture by becoming partner for manufacturing of servers based on the Grace and GraceHopper CPUs.

Trying to bust some myths as per my understanding:

Server design and manufacturing is a very complex process -

Not that great deal IMHO. Server design process starts at CPU makers (Intel/AMD). They share a reference architecture of the server with server manufacturers (Hp/Dell/Lenovo…). What the server manufacturer does is make different design of servers with diff. configs like 1U/2U/blade/multiple processor support/etc etc. One can liken the server mfg’s process to a laptop manufacturer who uses same Intel processor and gives multiple options in laptop with diff. capabilities like storage/display/etc etc…

The design capabilities required for a server maker are not R&D level, it’s more a implementation level with active guidance from CPU manufacturer at each step.

Once design is ready. Most server makers outsource the actual manufacturing to the OEMS like Foxconn/Gigabyte/Wistron etc etc…OEMs manufacture the server motherboards/boxes etc. Parts like Harddisk/GPU/RAM/wires, as we all know have diff. reputed manufacturers and all this is assembled by OEM and they put the sticker of vendor like (HP/Dell).

Server makers capability lies in customer management/sales/support/ etc…

How did they develop all the Super Computers listed in their deck…

At a very simplistic level, a super computer is not one huge complicated computer (if you are thinking of it like that). It’s just thousands (or tens of thousands) of servers networked with each other where a software layers has the capability of pooling these compute resource to tackle a problem needing such high compute power. Huge numbers of server networked with each other , mostly in a single premise. Does it sound that intimidating anymore ?

Hope this part is answered. Others are manufacturing servers which supports nVIDIA GPUs. Just like Netweb also does with their Intel x86 based servers support nVIDIA GPUs. Netweb is not going to manufacture NVIDIA Grace (Hopper) Superchip CPUs. They will likely manufacture the server to support those CPUs. But we have to keep in mind, as on today the market share of NVIDIA CPU in server market is close to ZERO. It’s a good thing or bad thing, time will tell. CPU/GPU manufacturing is still in the capability of exclusive club with the likes of TSMC/Samsung. No Indian company has come anywhere close to such capabilities as of today. We may, in future!!

Yotta, is the data-centre in the company from Hiranandani with landbank.

This will benefit companies like Netweb and supermicro; Netweb does have a high ROCE and partnership with Nvidia but that doesn’t mean Yotta will use them, if they have technology like super micro at lower price which is the reason one would be pick them (I don’t have that insigth). I think it is a good small bet, if you tracking and are able to add specifics then add that then it will be helpful. As a rough working estimate for terminal value; I would expect $20-30 of order flow from India or India based companies from companies’ large players in the AI training and inference chips from Nvidia; and industry is just starting to develop; and 40% of new spend is in HPC compute. Large IT services player capex plans are not yet announced yet expect HCL tech not very meaningful, this can increase the marketsize. At these, valuation it is important to know the scope.

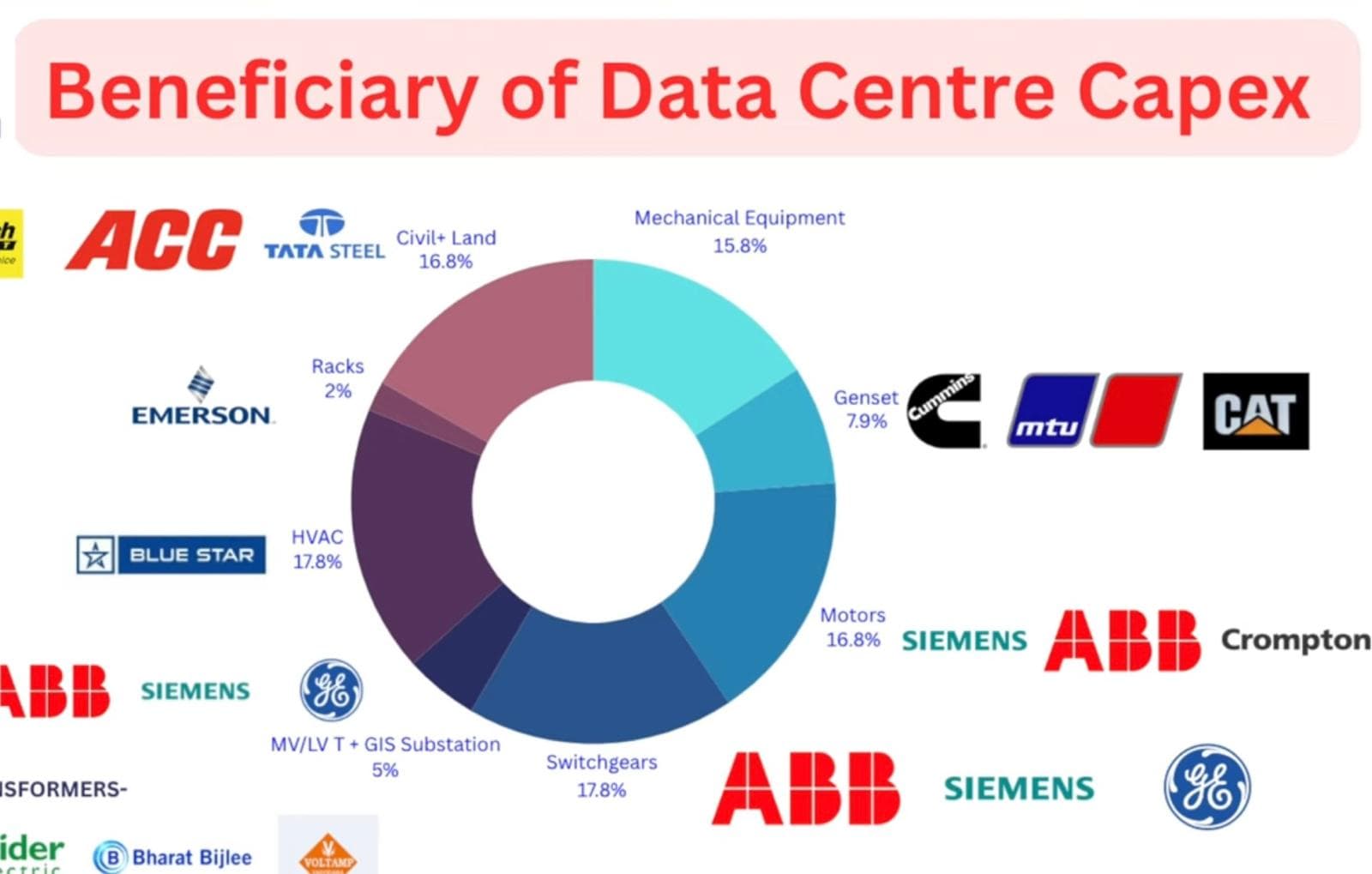

ABB reports data center growth area; in terms of picks and shovels/proxy here some more details below with a ballpark estimate of the 45cr per mega watt; But I don’t know if there is scope higher margin/ROCE or are directly play on this growth area; ABB for example is diversified but they trade at 60 times etc…

Also, in terms of foundry-based model following maybe useful information, in terms of market size estimation for Netweb which further increased by unicorn start-up etc. I guess now I am just assess if there is no real competition. I am long on Nvidia for a long time and hence very picky, I there is no need to take a proxy play and these data from wider research, to manage the position and not invested in Netweb, but interested and tracking if the price is right. Hope this is helpful its not specific to netweb but a necessary precursor ?

NETWEB is not in OSAT (semi-conductor packing) business but if it does get into it; there are larger players getting into that side; If they get into right will be a key growth area with high margin; Worth to keep an eye in-concalls; as it is a good vertical for them

trying to understand their R&D capability as that is key for company.

As per DRHP , their designs are licensed from another entity(Netweb Pte) belongs to one promotor.

Now I realize that doing a multiples analysis is very simplistic, but I want to understand if there is any margin of safety for Netweb at these levels. Please let me know what you think about my points below:

Nvidia has a 60% EBITDA margin (which may drop), with a 262% y-o-y increase in revenue in the quarter ended April 2024. It does not do any manufacturing work, nor does it bother with customized services/setup. It trades at ~33x TTM sales

Netweb, by comparison, has a 14-15% EBITDA margin, which doesn’t have much scope to increase significantly, 115% y-o-y revenue growth in Q4FY24, and does manufacturing, as well as customized services/setup work. It is currently trading at ~17x TTM sales.

Unless revenues more than double in FY25, there is no margin of safety at the current price, in my opinion

Disclosure: Not invested, but recently started tracking the stock

Sector Tailwind, Make in India and very Large Adressable Market. I assume once company grows some more backend manufacturing ( Like SMT they have started doing) they may start. A parallel may be drawn from Sirca Paints Ltd., iniitially they were only dealer of Itly Company and now manufacturing their own items.

Disclosure: Invested

i dont think they will get into OSAT because they are not pure EMS company. They are a product company focused on specific product and also happen to manufacture their products. The promoter has multiple times said on multiple concalls “we are not box builders” to various questions which were pointed in the EMS direction.

Yes customers are mostly government and educational institutions. But in latest presentation FY25Q2, they seem to have added more customers. In concall too they told that they have started their exports also, with customer(s) in Europe and Middle East. But I couldn’t find these customer logos in the presentation. I found one Korean automotive company logo though (HL Mando).

Any idea who these European/ME customer/customers are?

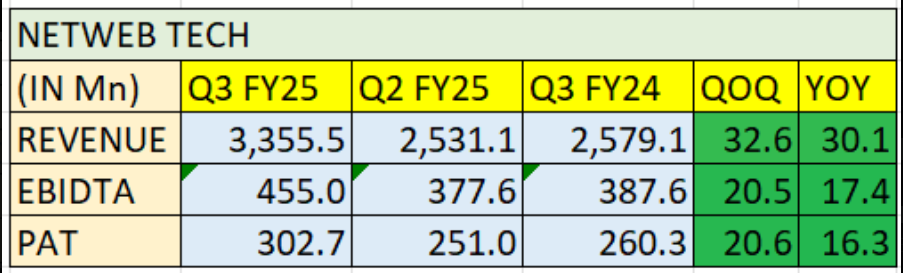

Netweb Technologies achieved 30% revenue growth and PAT growth by 16.6% year on year. The company has met lower end of its 30-35% revenue gudance. There may be some disappointment with lower PAT growth and reduced OPM. (The EBITDA margin for Q3 FY25 was 13.6%. This is lower than the 15% reported in Q2 FY25 and 14.9% in Q3 FY24.) The company’s healthy order book and growth in the AI segment signal a positive trajectory for future performance.Stock trading is steep valuation and to maintain such valuation higher growth and PAT is required.