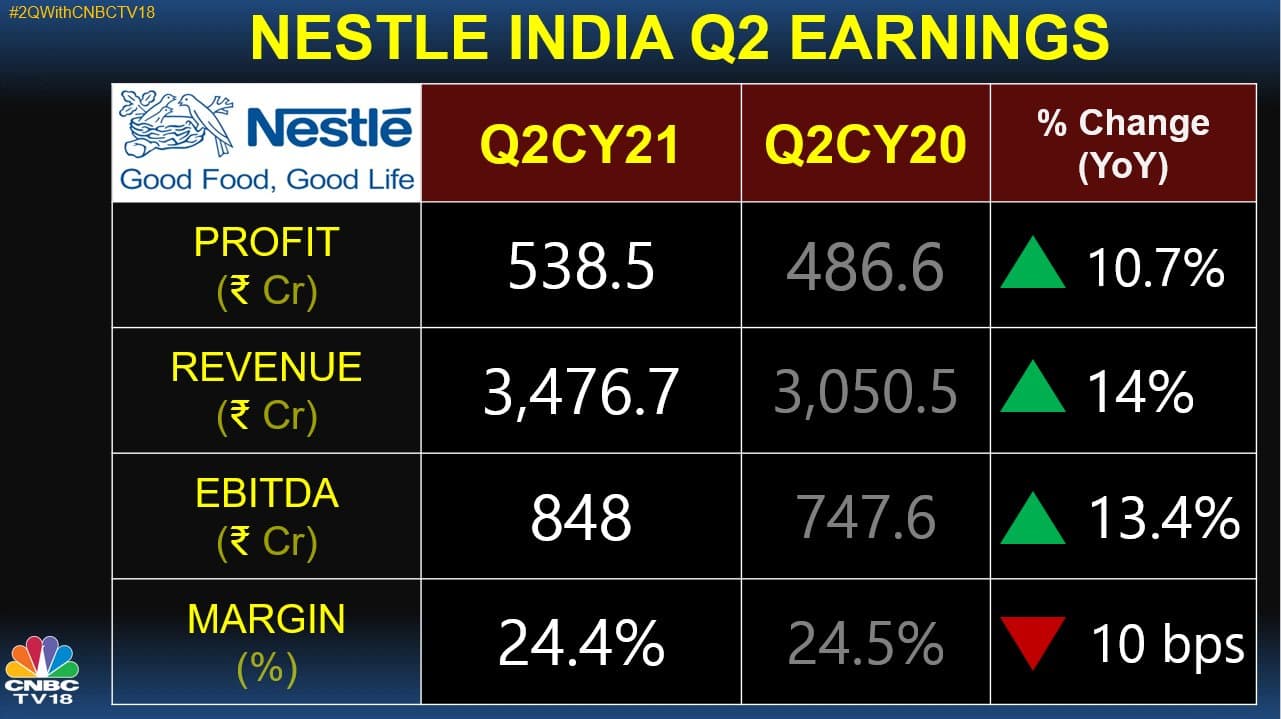

Quarterly Result - June’21:

3 Likes

Nestle India Net Sales

Over last 10 years, revenue of the company grew at a CAGR of 9.35%. On the other hand, PAT grew at a CAGR of 11.64%. Due to strong market holding in most of its products, Nestle secures pricing power. Moreover, cost efficiency drives good margin growth. PAT margin grew from 11% for CY17 to 14.3% for CY19.The average price of products sold did not see much increase since FY16. The management’s focus is on volume based growth

3 Likes

Record date of 27th October 2021 for second interim dividend for the year 2021, if any; and date of payment of second interim dividend for the year 2021, if any, on and from 16th November 2021

Approved Ready to Eat /Cook Production link Scheme

2 Likes

2 Likes

1 Like

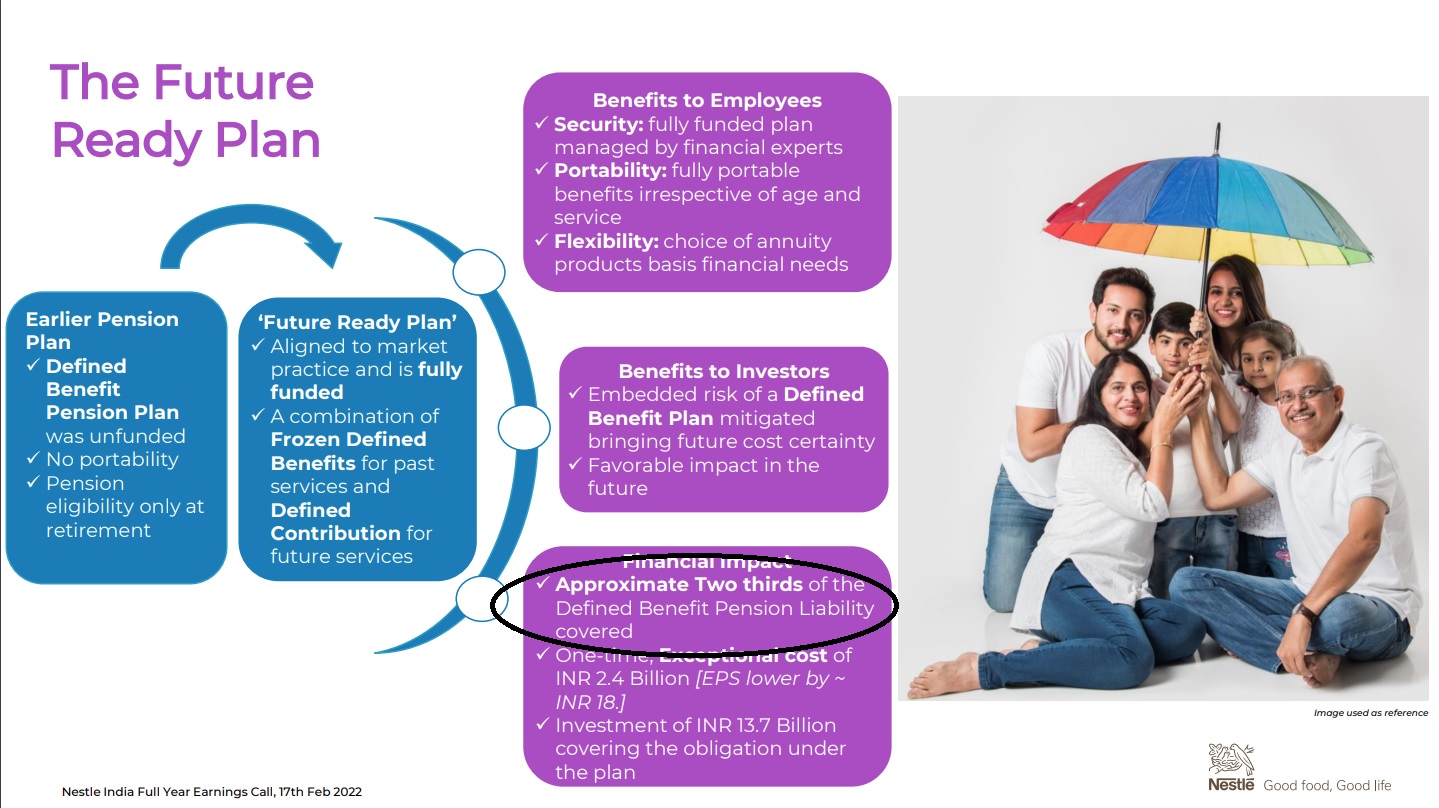

Hi I have just started tracking NESTLE and wanted to understand regarding the one-off due to the change in pension plan. Every quarter and even last year the company is have exception item with regards to RE-MEASUREMENT OF RETIRAL DEFINED BENEFIT PLANS. Is this related to the Future ready plan or is that one time expense separate from this? Can someone in general please summarize why Nestle keeps this expense as separate and why is it ongoing?

As per company presentation 2/3rd of the liability have been migrated from defined benefit pension plan to “Future Ready Plan”.

Seems company is incrementally covering it’s employee pool to avoid an exceptionally large P&L hit in a given quarter.

But is a very good exercise to protect itself from future liabilities. So long term positive.

It keeps it seperate because the hit in P&L is not due to any external exigencies and does not reflect it’s actual earnings in the quarter and the cost is one time only. Seems reasonable to me.

Disc: One of my core holdings

2 Likes

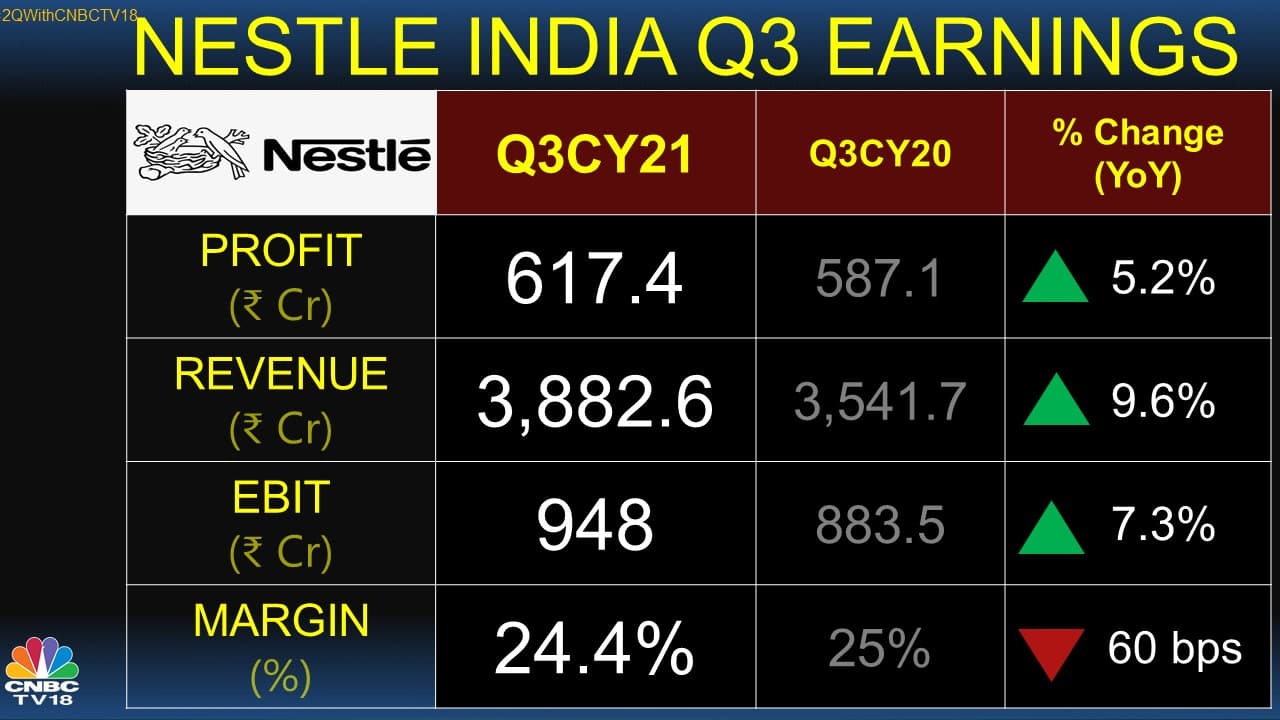

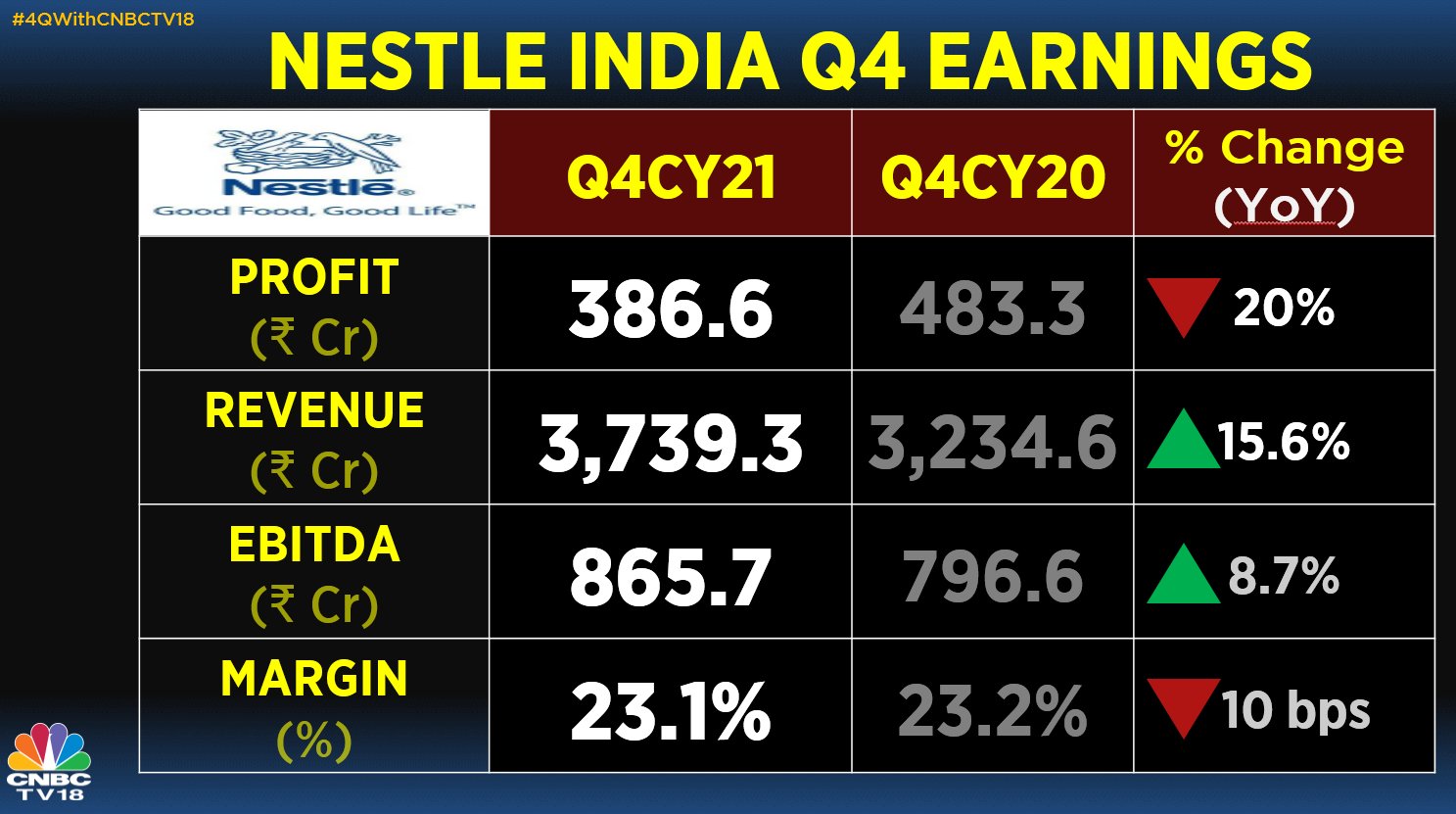

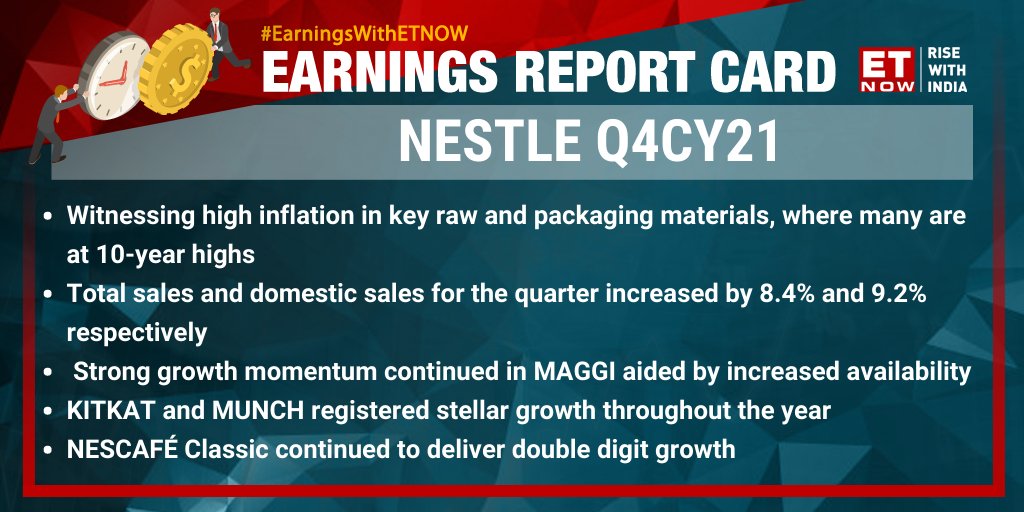

Annual Report 2021

3 Likes

Nestle India has yet to introduce many products available in the US and Europian Markets which has lot of scope in India.Exports of Indian Products like Maggi has huge Potential in Global markets ! They are yet to go aggressive on ready to eat foods . So all in all good rerating awaited !

At PE of 80.8 … Nestle is not of in need of Re rating , but delivering on the promise of earning …

That is sad part for Nestle … inspite of so many core advantages … its long term earning growth < 10% is worse than sub par commodity companies …

It has failed to live up to its potential … Now it has to depend upon parents to give them products to succeed …

Where are innovations like Maggi which happened in 1990s - No earth shattering product development is happening in India … Sad for a company that has market cap of 1.85 lac crore … and great talent

1 Like

Thats why I always wondered why Nestle gets such a high PE valuation despite its poor performance. Why its performance never revert to mean as per its earnings? A question to ponder…

All FMCG companies tend to have relatively high PE ratios vs companies that are into lets say manufacturing or even IT space. I feel these high ratios are partially justified because the valuation of a company is not based solely on the earnings but also the assets. All FMCG firms have brands that they have built up over decades along with strong distribution channels and vendor partnerships. Nestle is spending 750CR per annum on advertising and all of this cements the MOAT. It has taken ITC over 10years to finally turn its FMCG ventures somewhat profitable (even now Yipee! is a far 2nd to Maggi but definitely ITC is on the right track in general). That is just my opinion on the matter, would be very happy to have a healthy discussion on how we should value the intangible assets that these companies possess!

Disc - invested in nestle and ITC.

The logic for higher PE in FMCG is that for high growth they won’t require higher capital ( esp by equity dilution ) …

But when there is no growth for 10 years that so called moat is useless … It is like having factory with low capacity utilisation …

Distribution , brand and people assets have been under-leveraged by Nestle … that means for last 10 years - Nestle management has been plain incompetent

1 Like