The fire incident was known for long. As their large electrolyte plant is coming online soon, it’s obvious that costs will run up. They will need workers, researchers and good management that can execute and this will obviously lag revenues and profits. The higher insurance premium will stay for a few years but that was obvious as well.

They have had higher finance costs due to debt to run their operations that got affected by the fire, which will resolve on getting the insurance money.

Literally no reason to panic after the latest results if you were comfortable before hand. Revenues are up despite the headwinds on to of a strong Sep last year so its not just a base effect. I think market is thinking very narrowly here

Absolutely agree with you. I actually concluded the article with the same reasoning in the Bull Case and Investment Outlook sections. With this post, I wanted to objectively list the reasons behind the current fall, but I agree that the market is missing the bigger picture. Neogen offers great upside here if someone have the patience to hold for the medium-to-long term, especially at the current market cap.

Disclaimer: Invested and biased.

Thank you, @naveendahiya for this useful write-up! Particularly the chronology of events is of great help in coming up to speed on the stock. Sharing my thoughts below:

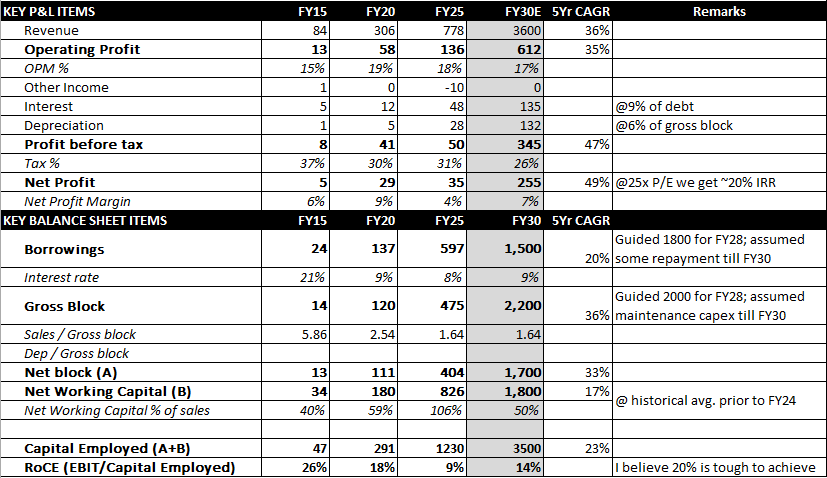

PAT margin assumption is aggressive

- I feel that the 9% PAT margin assumption might be tough to achieve, given that the company may have 225-250cr of depreciation + interest cost.

- The company has indicated a peak gross block and debt of 2000cr and 1800cr on full utilization.

- 9% might be possible if (1) the balance sheet is debt-free, (2) gross block turnover is >2.5x or (3) EBITDA margins are >19%

Exit multiple may be lower than anticipated

- I have my doubts if the market would give 30x/20x exit PE / EV multiple to Neogen given that (1) it will be a 20%/15% ROCE/ROE generating business and (2) will inherently volatile.

- While there is some edge in (1) access to technology and (2) scale among non-Chinese capacities, the industry has behaved more commodity-like in the past.

- For a more moderate multiple of 25x P/E and lower net margins of 7%, the IRR does not appear as attractive (but still decent!)

- I personally, would prefer either (1) a deeper valuation discount or (2) major positive development to warrant capital allocation. But to each his/her own.

A point on execution

-

While I agree that several factors have been beyond management’s control, but frequent delays in achieving guidance is still a matter of concern.

-

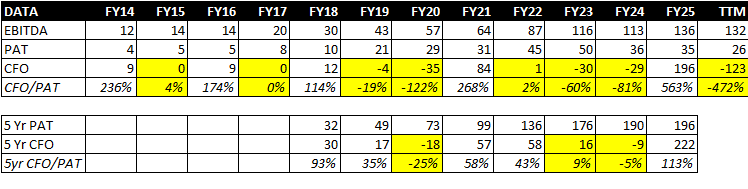

Very importantly, as @vnktshb has also mentioned, the hit on working capital has been more drastic than anticipated every time there is a shock in the business. In 1HFY26 too, the CFO of -246cr was an unpleasant surprise; even when adjusted for 180cr of one-time inventory hit due to the fire.

-

Ultimately, the inability to meet stated guidelines and maintain positive CFO, at the very least, points to the complicated nature of Neogen’s operations and the industry. Hence, a lower exit multiple would be prudent to work for long term investors.

Some number-crunching from my end:

Disclosure

- Not invested. Only tracking the stock.

- Not a recommendation. Only sharing my thoughts to improve our collective understanding.

7 Likes

@HBORA1012

Thanks for the reply and sharing your analysis. You are right to point out that my assumption of a PAT margin of 9% is on the aggressive side (7% seems more realistic for FY30). However, one thing I have noticed in my personal investing journey, where I have earned decent returns, is the “rate of change” in key variables (revenue growth, EBITDA growth, net profit growth, expansion in return ratios). That’s why I think a P/E and EV/EBITDA of 30x and 20x are very reasonable, even with your assumptions.

Again, thanks for sharing your analysis; it does help in improving our collective understanding. As they say, investing is a game of probability and I think Neogen offers a high probability of at least a decent return (even with your conservative estimation, we are looking at ~20% IRR) and a good probability of asymmetrical returns from current levels, especially if revenue and EBITDA margins come in at the upper end of guidance.

3 Likes

I agree to most of the points discussed recently.

another factor that may impede Neogen’s battery chemicals march would be serious meltdown of Ola!

Ola giga factory is one on whom neogen is banking big for initial head start

3 Likes

Very well summarized for all of us.

Wanted your view on a scenario where, India in-order to continue getting access to rare earth magnets if China forces our govt to open our doors to electrolyte salts, then could Neogen still be competitive with Chinese players? Due to the JV with Morita, would Indian Battery makers be willing to buy from Neogen at say 10-15% premium instead of Chinese substitues.

In a somewhat similar scenario, Valiant Organics were the first to commision PAP (again crucial import substitute) but now facing headwinds with excess supply from Chinese players.

Wanted your 2 cents on this..

Very pragmatic analysis! Thank you for sharing.

1 Like

Thanks for the reply!

I cannot comment on the hypothesis that India might open its market to electrolytes in exchange for access to rare earth magnets - that is a complex geopolitical subject and I am no expert.

Also, I do not track Valiant Organics, so I cannot comment on that specific comparison.

However, regarding Neogen, the management discussed cost competitiveness in detail during the Q2FY26 concall. Here is why they believe customers will stick with them:

- Indian Cell Producers:

-

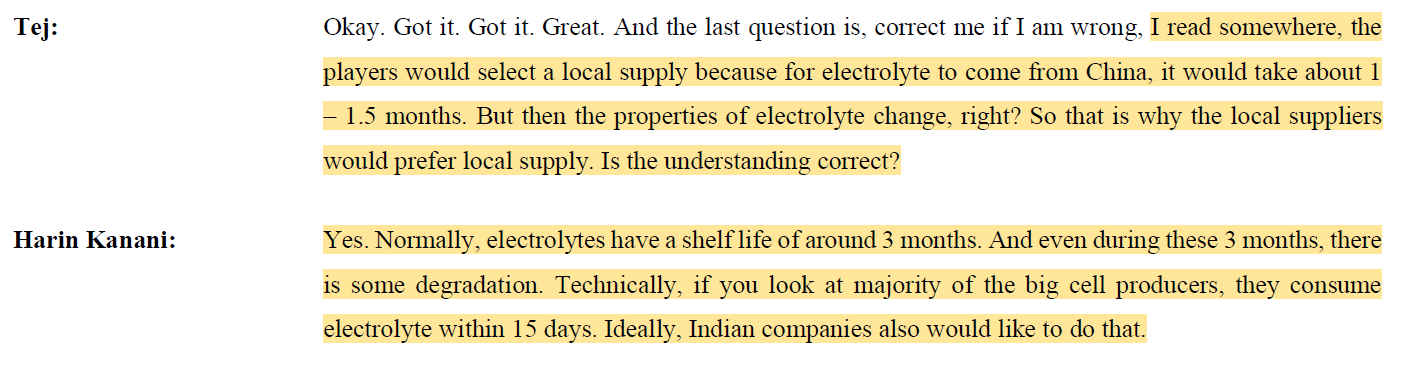

Shelf Life and Consumer Preference: Electrolytes have a shelf life of only around 3 months. Importing from China takes 1-1.5 months, which leads to degradation. Technically, major cell producers prefer to consume electrolyte within 15 days of manufacturing to ensure quality. This physical constraint makes local supply critical.

-

PLI Norms: To qualify for incentives under the PLI scheme, Indian cell manufacturers are mandated to use at least 60% indigenous material, making local sourcing a necessity rather than a choice.

- International Customers:

-

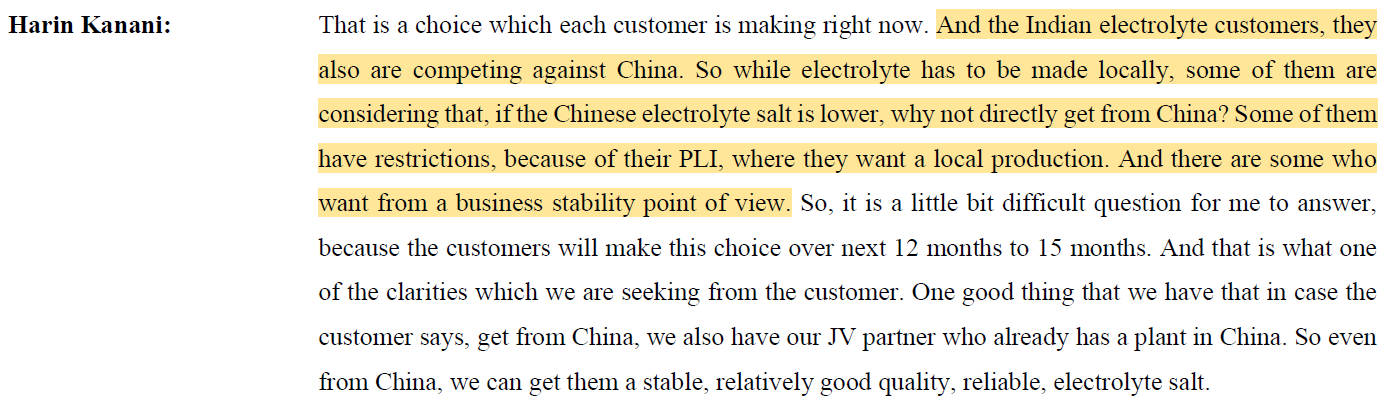

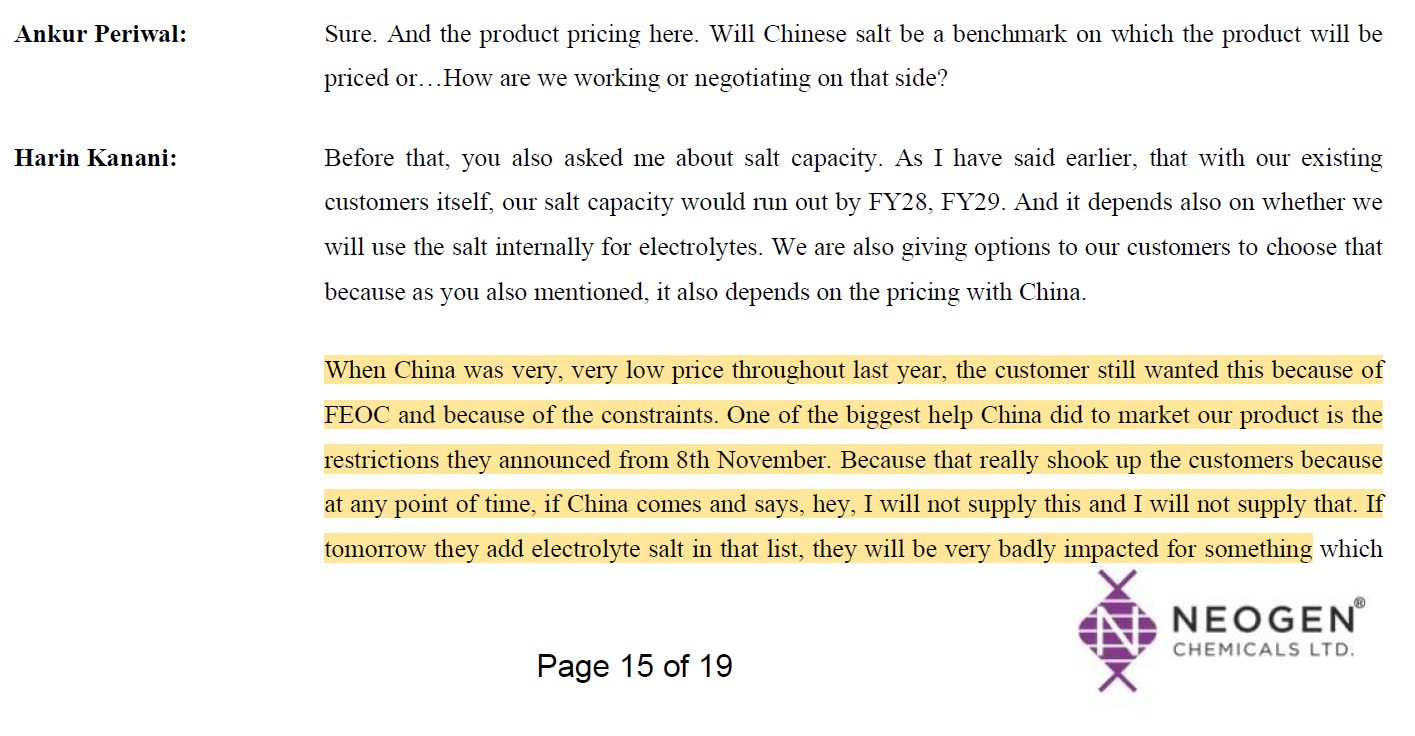

Supply Security and Non-FEOC status: Management emphasized that recent Chinese export restrictions (specifically the Nov 8th changes) have shook up the market, shifting customer priority from chasing the lowest price to ensuring reliability. Within this critical “non-FEOC” market (essential for tax credits), Neogen claims to be the most cost-competitive global supplier outside of China.

-

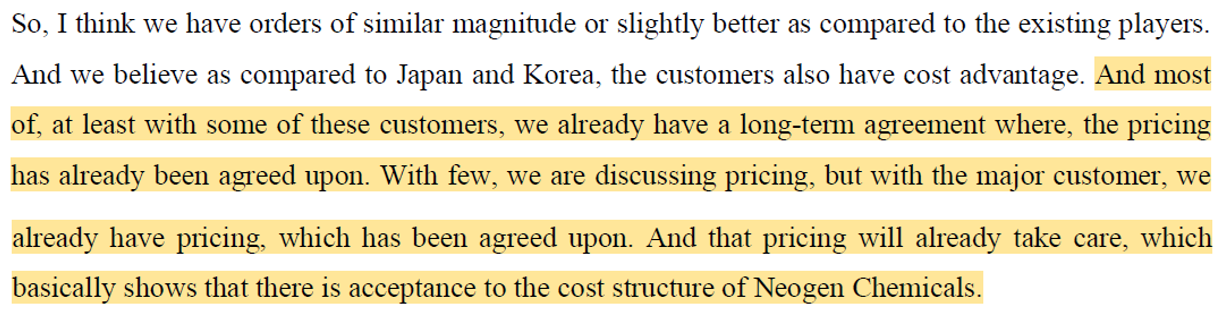

Pricing Locked-in: For electrolyte salts, the company has already signed long-term contracts with major customers where pricing has been agreed upon, signaling acceptance of their cost structure.

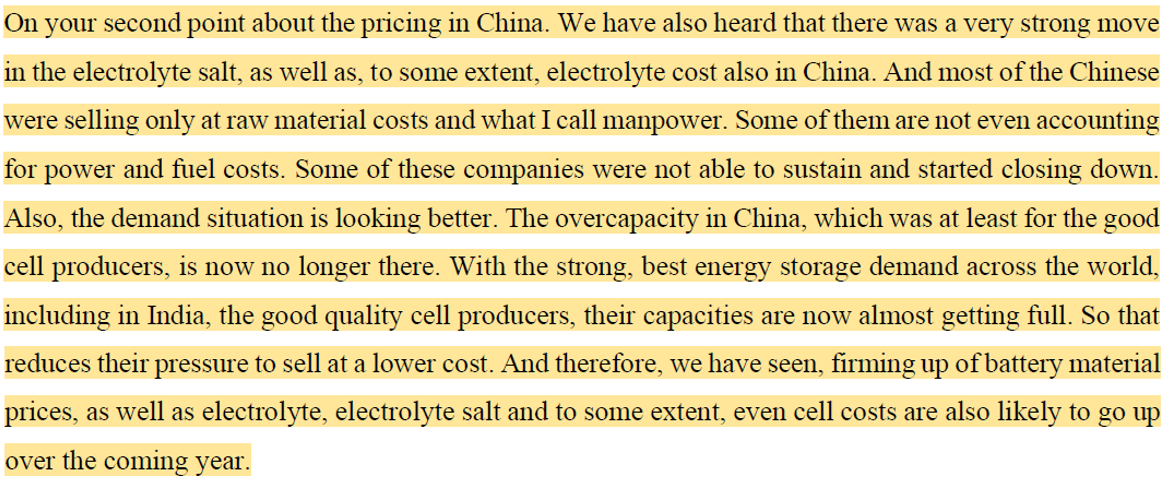

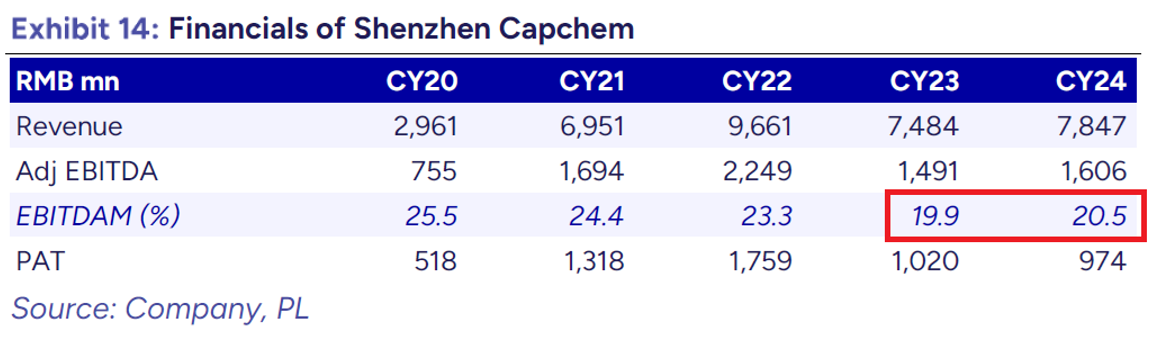

Management indicated that pricing in China is stabilizing/firming up. Previous low prices were unsustainable as suppliers were selling at raw material and labour cost, leading to plant shutdowns. Even in a report by PL Capital, EBITDA margins for one of the largest players in electrolytes (Shenzhen Capchem) increased in 2024.

As investors, we can only track things going forward. If the thesis doesn’t play out positively, one can always reassess and exit.

4 Likes

Thanks for your detailed input. This definitely helps. Much appreciated.