At first let me disclose that I am invested in this stock – it constitutes about 13% of portfolio. I am posting this to share my investment thesis, and also to receive feedback on the same.

Business model

NDTV is in the business of News and Media. They also have lot of online ventures such as NDTV.com, CarandBike.com.

Some of the Highlights

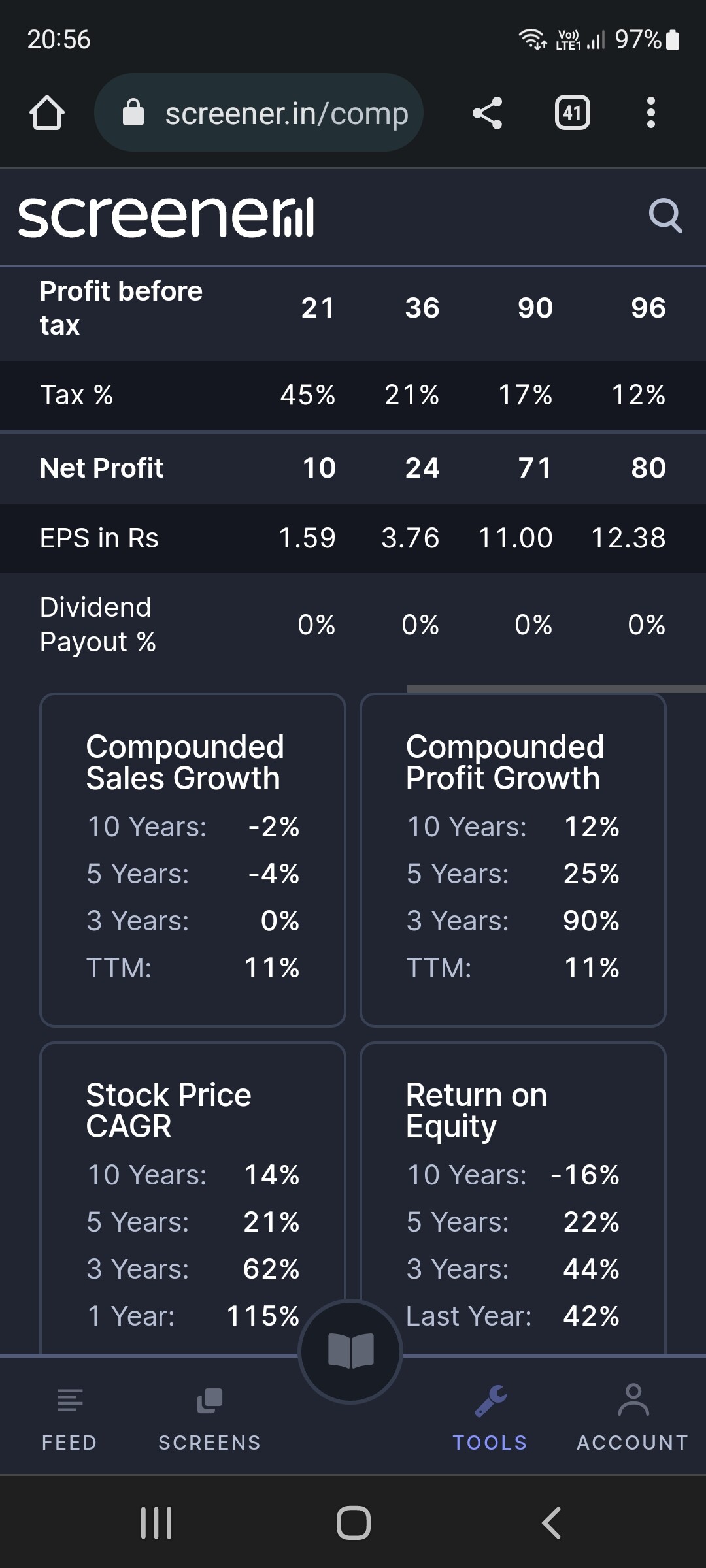

- Company has delivered Profitability in 8 out of 9 quarters in the last 2 years.

- Company’s employee cost is down from 44% in 2017 to 23.55% in Sep 2020. (Ref: Screener.in)

- Company’s Production Expenses are down from 111 Cr to 60.24 (Mar 2016) Cr in Mar 2020, Annually (Ref: https://www.valueresearchonline.com/)

- Company’s General Expenses are down from 123 Cr in 2016 to 81 Cr in 2020 (Ref: https://www.valueresearchonline.com/)

- Company’s Selling and Distribution Expenses are down from 128 Cr to 40 Cr. (Ref: https://www.valueresearchonline.com/)

- Company has consistently got rid of their top Anchors and are focusing on getting their TV business back to profitability.

- Their main focus has been NDTV.com and is consistently profitable for the company. Also they won 300+ cr deal with Taboola.com for Advertisements. Also their other online ventures doing well too.

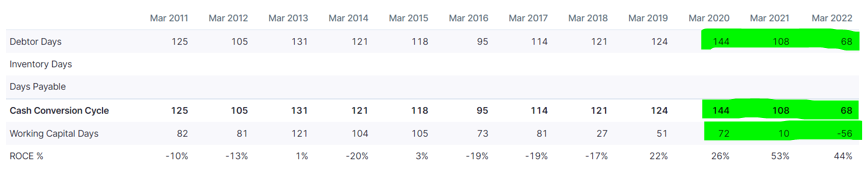

- Their long term liabilities have decreased from 705 Cr in 2009 to 89 Cr in 2020. (Ref: Screener.in)

- Promotoers are very reliable and have consistently maintained 60+% holding in company.

- They closed down their Non Profitable business such as General Entertainment Channel and focusing on their core skills.

Weakness:

- Until now Promoters were not focusing on profitability of the company and I feel they are little emotional when taking some of the business decision. For. eg: Even though hindi news channel is loss making since ages, they are refusing to shut it down.

Threats:

- The biggest threat for NDTV is Goverment, Especially NDTV is very risky stock when it comes to goverment trying to control the media.

Opportunities:

- Get rid of some of the loss making business such as Hindi News Channel or NDTV Profit.

- Focus on Online News.

For More Details:

https://www.screener.in/company/NDTV/consolidated/#top