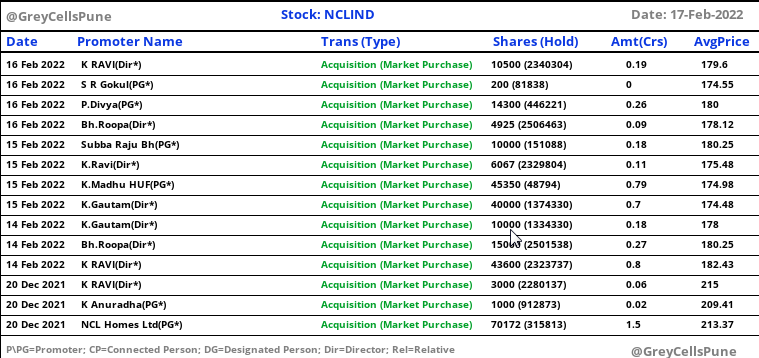

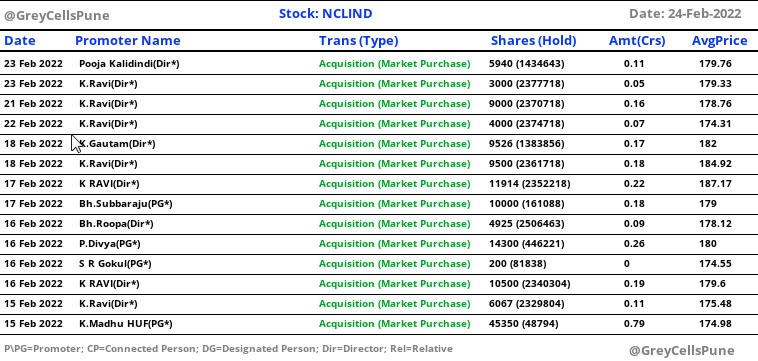

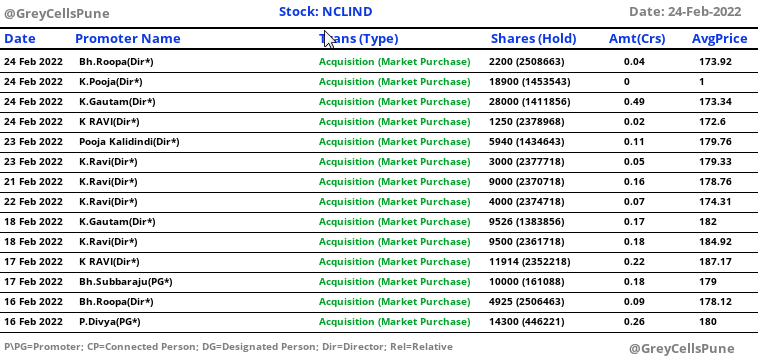

I don’t see any governance issues on the face of it. Very small cap cement + allied business with sub-1000 Cr (631 Cr as on date) M-Cap will not attract any institutional investor / MF interest to drive prices up. Q1 & Q2 FY21 results have been good, in fact exceptional. If they can sustain these results over the next few quarters there is bound to be some interest going forward. Promoter families / groups have been buying shares aggressively from the open market in the last 6 months. Promoter holding up by 1.4% between Q1 to Q2 in FY21.

1 Like

The expansion for this company in cement is very limited because they are able to sell only in Andhra and Telangana. Freight and competition is heavy if they cross their border. Second is, other building products are not contributing much and they are slowly expanding in boards and doors. But the are very conservative mgt and they will grow slowly.

Coming to current years, the cement price increased due to rural demand and cement companies increased the price. Imo this will not sustain for long time.

Mgt is good in my opinion. This will be a up and down company and will scale up if structurally grow their other building products but already competition is high with companies like everest, hil, visaka

The

2 Likes

You have any reference article for this, can you please share

NCL inds call takeaways : Rs.350 price currently. 90% Utilisation in Q2 sustainable, not one off. Q3 should maintain Rs.1300 ebitda/ton. Volumes very confident of 2.2 mn for the year (not being able to meet demand). Pricing in Q4 need to see if Telengana govt can maintain spending, Telengana govt needs to raise liquidity/funding.

Bison board panels will recover very well in H2 as main markets are Mumbai & Delhi

Waste heat recovery 25 rs cr savings from fy 22. 80-90 cr capex done in 1st half.

3 Likes

Seeing the promoter buying in the market, gives one more confidence. Disc: invested, wondering if to add with promoters, 3-4x PE is too mouthwatering

1 Like

Great show from NCL so far.

Prices are up 15 to 20 pc yoy in south and volumes are up 50 pc for NCL. Also some prominent investors have bought in the December quarter

Monthly business update. Volumes are up 40% . Operating at 100% capacity and RMC / Door sales have also ramped up significantly. Surprising why the market has not re-rated the stock . Management has been very transparent and are announcing dividend 3 times a year! Expected EPS for this year should be closer to Rs 45 and hoping dividend is ramped up beyond Rs.5 . Brownfield Capex also announced for increasing cement capacity to 3.6 MT from 2.7 currently.

Cement prices in June quarter have increased the most in South. So the EBITDA margins of NCL should definitely be a little better

Stock has corrected mainly due to increase in Coal prices and also reduced demand because of shortage of river sand. I feel it is a good time to enter because

- With real estate and infra pickup post monsoon, the company will definitely announce a price increase soon . This will offset the increase in coal prices which has impacted all players. River sand is a temporary issue which surfaces every year

- They are slowly shaping their company into a building products company - with addition of bison boards, doors, RMC and now modular containers which could be used for making toilets in a big way. See the announcement below :

https://www.bseindia.com/xml-data/corpfiling/AttachHis/3bcdb101-2b02-444a-8115-cb0299ec194e.pdf

2 Likes

Current quarter results are not that bad even though fuel costs have gone up Rs.40-50 crores over last quarter

I have been observing it recently, as commodities prices will be sky rocketing along with Gas & Fuel in the coming few quarters which will hit the margin hard for sure shot, the stock can be drag to 60 moving avg, also coming Q2 will see margin drop due to monsoon , so the promoters are buying before it bottomed out , any news of project they have in hand or demand surge or they are buying with the dividend they have got, bit confused , any thought on that

3 Likes

They also created pledge somedays back , how to interpret , since buying is huge , pledge document was not visible clearly i think it was a small pledge but not confirm about quantity

1 Like

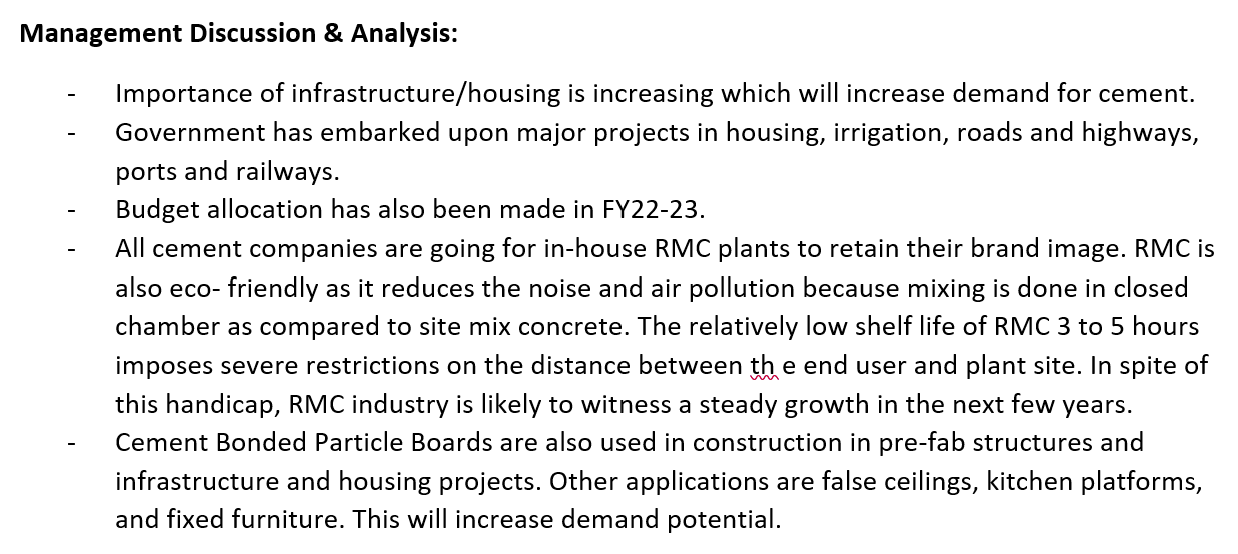

Outlook is strong as there is going to increasing demand for Cement, RMC and Cement Boards for Infrastructure & Construction Segment. The segment is also backed by Huge Budget Allocation in 2022-23.

Outlook for the cement and building materials industry looks promising medium term despite the uncertainty caused by steep increase in coal and other input costs.

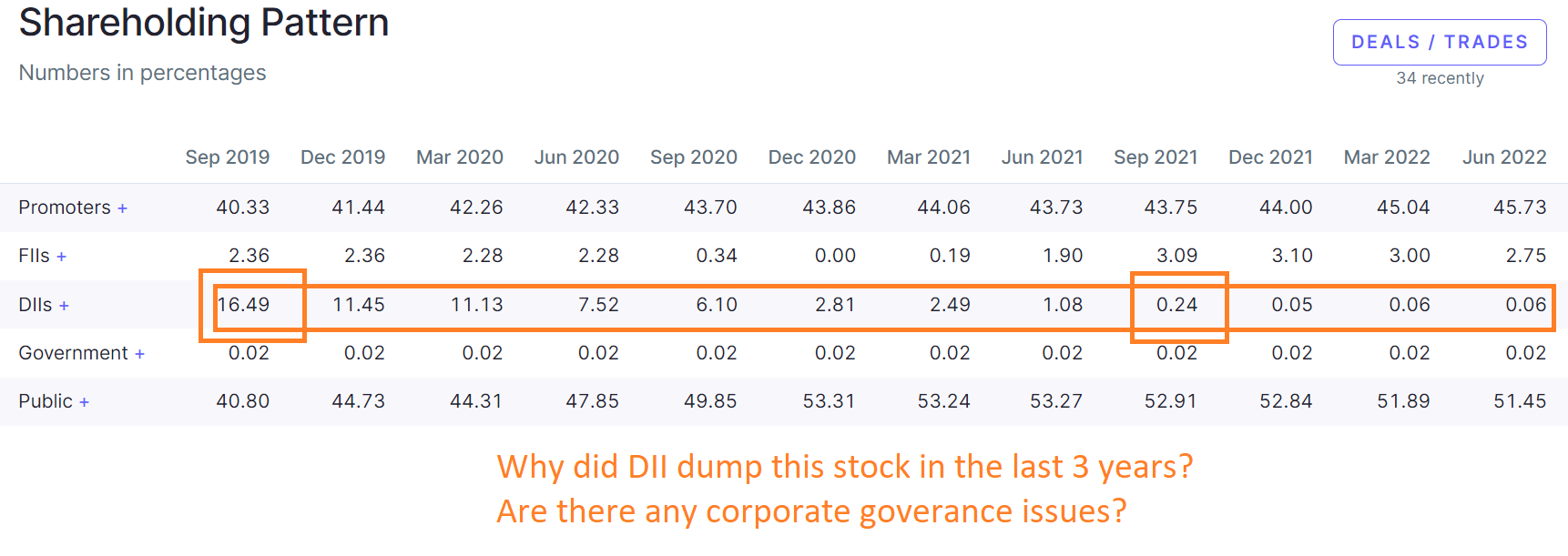

Some close ended funds sold their holding because they completed their tenure.