Why shouldn’t we buy other cement companies like Sagar or Mangalam Cement as they look to be cheaper than NCl with more capacities and higher realizations ?

I haven’t looked into the businesses you have mentioned. Thus I cannot comment on them.

One positive that I liked about NCL though was, increase in promoter holding at current levels. If promoters show confidence about the business and things look set for near future, it’s good enough for me to take a position.

NCL has been a high conviction bet for me from RS. 70 levels. A couple of things that are worth noting are

it does not sell to govt/contractors but sells on cash and carry/low credit period in retail

NCL’s plants are amongst the closest to amaravathi the new capital city near vijayawada

for a near 25 % increase in sales in FY15, receivables have inched up only about 2%.

cash flows are very good - Rs. 55 Cr. of OCF - led by improvement in all effficiency parameters - increase in current liabilities, decrease in inventories,OPM. If the company can maintain these going forward, this can be a 2-3 x on the back of both PE re-rating and rapid EPS expansion.

I just read the report of Nirmal bang. I agree with all of your points but then how their relizations are lesser than other cement companies I have mentioned? Nirmal bang report contains all the numbers. The only thing I see here is that their recovery haas started earlier than the other 2. Views invited sir!

@ramakanth:

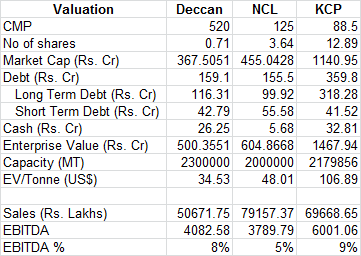

One another correction - For EV calculation, we must use Net debt and not Gross debt. In the above calculation you have used gross debt to compute EV.

NCL’s Net Debt is somewhere around ~ 144cr.

But yes, at CMP new investors do not have the same level of valuation comfort compared to those who had entered at 80-90 levels.

Additional Info - Management envisions this # to go down to 96 cr by the end of this FY.

FY15 EBIT for board business was 30% of overall EBIT. Revenue was 15%+ of total revenue for FY15. This business has been growing at more than 20% with margins of 17% odd.

I had also read in ET that this business can be valued at 150-175 Crs.

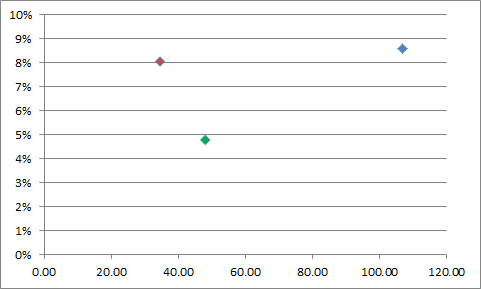

Even if we value this business at 150 Crs and deduct the same from current mkt cap of 467 Crs. then the residual business is still available at 317 Crs. or EV of 455 Crs. (If I don’t allocate any debt towards board business) or EV/EBITDA (FY16-arrived at by extrapolating FY16Q1 nos. This might be naive and too layman but I think safe assumption as capacity utilisation will go up and prices may hold) of 4.6-4.8 times or EV/Tonne of 38-40 US$ odd, which I think is still not expensive, considering that the cement business has good earnings visibility and better times ahead.

If we go by company MD’s guidance of 75% capacity utilization for FY16, we may observe an EPS around rs. 22-25 for the year (probably more). In such a scenario, NCL is trading at forward p/e of less than 6 for FY16 which is just 2 quarters away.

I believe there is a good amount of valuation comfort at these levels.

As discussed in Deccan Cements thread. Cement companies are normally valued on EV per tonne basis and not on PE basis because of earnings fluctuations. Enterprise Value per Tonne suggests roughly how much it would take for someone to set up a given cement capacity. Normally it takes around 130-140$ per tonne to establish a new plant and therefore is used as a comparable number.

Ncl for me is a not a long term investment case (I have already mentioned this before). The basis of taking a position in NCL is visibility of improved earnings over the next few quarters as well as improving fundamentals.

It is for the same reason the stock is being rerated by the market. I believe the trend may continue in the foreseeable future. Hence, the basis of earnings rather than EV/tonne or EV/ebtda.

Sure Nikhil. Appreciate your view. For me too it is an opportunistic bet. Its just that say for e.g. if NCL would have been trading at EV/tonne of say 100-120$ and EV/Ebitda of say may be 8-9 then despite good earnings visibility there might not be much scope of appreciation and less valuation comfort.

But I do get your point and either ways there is some money to be made here

Another announcement was made on 28th Oct for further release of pledged shares.

Quarterly results to be declared on 13th November.

Expecting Sales and Profits to be somewhat affected due to 22 days maintenance during the quarter (by how much is yet to be seen as company hasn’t been operating at Optimum capacity)