About the Company

NCL, incorporated in 1979 and based at Hyderabad, manufactures different varieties of cement, cement particle boards and Ready-mix concrete under the brand name “Nagarjuna”. The cement plant was established in the year 1984 with the capacity of 1800 tpd Line-I. Line-II was installed and commissioned in April 2010 with the capacity of 3000 tpd. Line-III was installed and commissioned in March 2018 with the capacity of 3000 tpd. Present Clinker capacity as on 31.03.2020 is 7800 TPD (2.6 MTPA) and Cement manufacturing capacity is 6120 TPD (2.0 MTPA). Company also has environmental clearance for 10.25 MW WHR Power Plant, the project is under execution with total capex of Rs. 87 cr. Company has captive Limestone mines which are at a distance of 2 km and 6 km from the plant. Company’s manufacturing process is explained in very detailed form on Page 16 of Environment Audit Report FY 2019-20.

Company has five divisions Cement, Boards, Ready Mix Concrete, Doors and Energy. Majority of company’s sale (86% in FY21) and EBIT (97% in FY21) comes from Cement division. The Readymade Doors division commenced its commercial operations in December 2019. For Door division NCL Industries has collaborated with AGT, a global manufacturer with advanced technology in wood industry, based in Turkey.

Valuations & Key Points

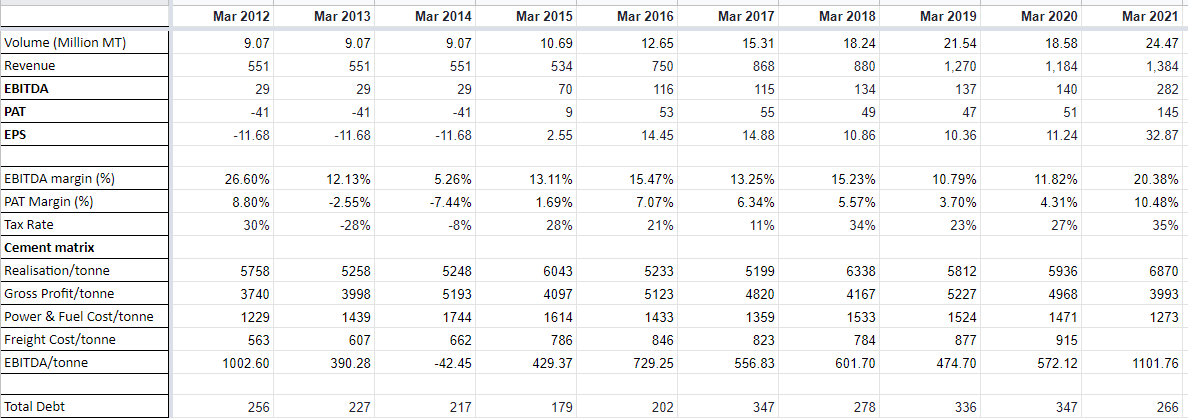

With a debt of Rs. 266 cr and cash equivalents of Rs. 71 cr as on 31.03.2021 company has EV of Rs. 1410 cr. Company has EBITDA of Rs. 282 cr in FY21. Company is available at EV/EBITDA of 5 times. Other small and mid sized cement players like Birla Corp, Heidelberg

and Shree Digvijay are all available at more than 10 times based on FY21 results.

The consortium of NCL Industries and NCL Buildtek Ltd has recently received Letter of Acceptance (LoA) from Andhra Pradesh govt for Door Frames. Total order value is Rs. 1863 cr. NCL Industries has 50% share in the consortium. Company did sale of Rs. 5 cr in Q1FY22 from Door division. Incremental sales from this division in next few years could be meaningful.

Setting up new additional grinding unit that is a greenfield project in Vizag with capacity of 6.6 lakh tons. And recently, taken up one more grinding facility at the parent plant. They have a total capacity of 2.7 million tonnes per annum, and with the expansion, this will go up to 3.6 million tonnes per annum in the next two years. With increase in cash flows in recent years, management is also getting aggressive. They did capex of Rs. 350 in FY18, they setup a Door division in FY20 and now have planned a Rs. 300 cr capex for next 2 years.

Measure are being taken by the management to improve the efficiency which will further improve the EBITDA per tonne of the company. The new 10.25 MW WHR recovery plant will save power cost by Rs. 30 cr p.a. Replacing Ball Mills with Vertical Roll Mills to have better energy efficiencies.

Key Risks

Cyclicality in the cement industry and CDR history of the company: Demand and supply dynamics determine the fortunes of the company mostly in this industry. Company faced a difficult period from FY2013 to FY2015. Company faced double whammy and reported losses in FY13 and FY14 due to decrease in cement prices and increase in power cost in Andhra region. Excerpt from AR2013 “Cement units in the State were badly affected by a combination of factors such as creation of excess capacity coupled with a fall in demand, recession in the infrastructure sector and slow-down of construction activity, frequent power-cuts, steep rise in the cost of key inputs like power and coal, coupled with fall in the market prices.” Company went into CDR in 2014 and completely emerged out of it only in 2017.

SEBI, by order dated 30.03.2020, imposed penalty of Rs. 7 lakh on promoters of the Company for violation of Insider Trading norms during the period 15.12.2011 to 09.10.2014.

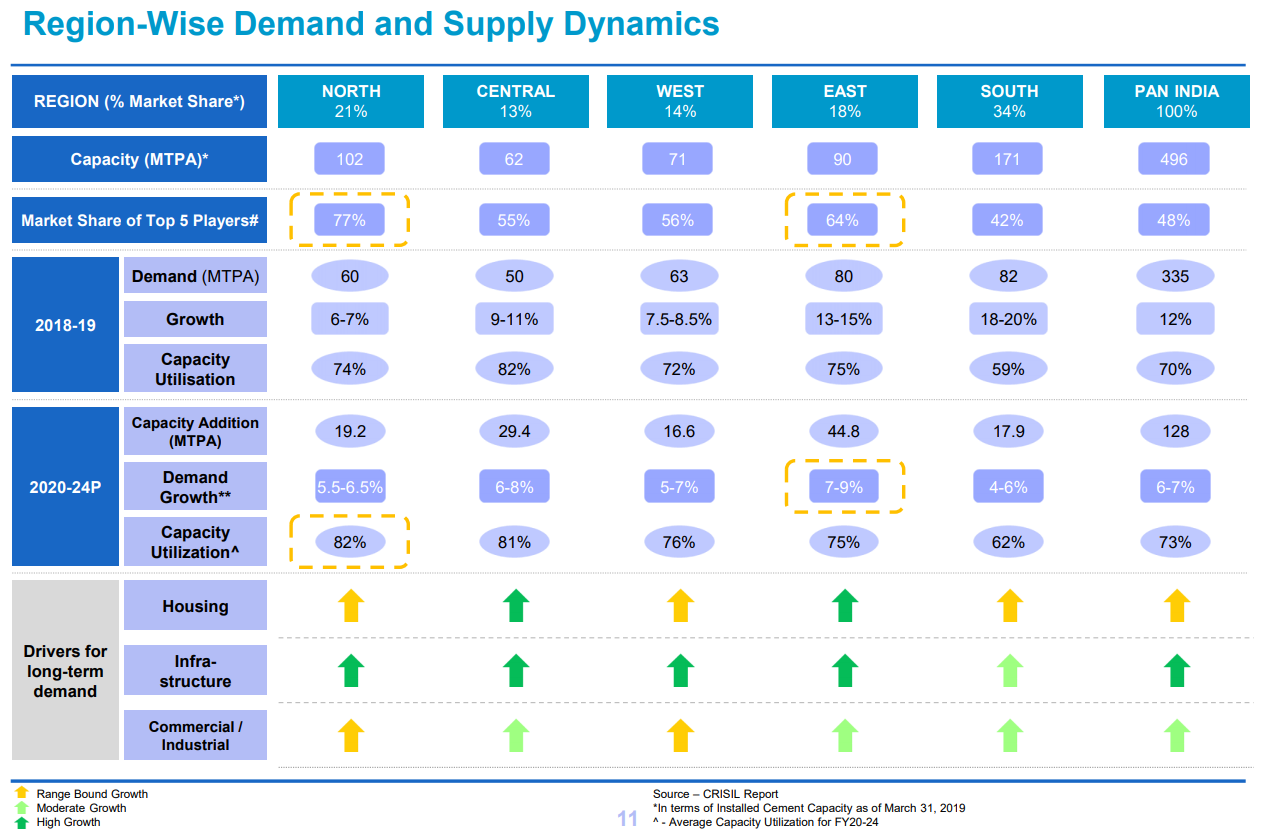

High competition in Southern Region: South region has 34% capacity market share with installed capacity of 171 mtpa out of 496 mtpa pan India as on 31.03.2019. Also the capacity utilisation is on lower end at 62% in South against 73% pan India basis.

Ordinary Portland Cement

Portland Pozzolona Cement

Special Cement- 53-S

Unit 1: Simhapuri, Telangana

Unit 2: Kondapalli, Andhra Pradesh

Capacity : 2.70 Million Tons

Dealers: 1800

Markets: Andhra Pradesh, Telangana, Tamil Nadu, Karnataka, Pondicherry

READY MIX CONCRETE

Unit 1, 4 & 5: Visakhapatnam, Andhra Pradesh

Unit 2, 3, 6 & 7: Hyderabad, Telangana

Capacity: 60Cu.Mtrs / Hour each

Markets: Hyderabad & Visakhapatnam

CEMENT BONDED PARTICLE BOARD

Plain, Laminated, Designer Boards & Planks

Unit 1 & 3 : Simhapuri, Telangana

Unit 2 : Paonta Sahib, Himachal Pradesh

Capacity: 90,000 tons

Distributors: 350+

DURADOOR UNIT Malkapur (V)

Near Hyderabad

Capacity: 1,000 Doors Per Day

HYDRO POWER PROJECTS

Unit 1: Pothireddypadu, Andhra Pradesh

Unit 2: Hospet, Karnakata

Installed capacity: 15.75 MW

Things to work on.

Door Division: Company has capacity of 1000 doors per day and with each door priced at around Rs. 18000, they have a sales potential of Rs. 600-700 cr p.a. They also received LoA from Andhra Pradesh government recently of total order of Rs. 1860 cr in which NCL has 50% shares. What is the sales potential and time frame of this order?

What could be the reasons for low valuations in such good markets? Other cement companies in same region are also priced better than NCL. Company is quite old and management also has clean past.

Our plans are now focussed on modernisation of the existing cement plant, improving operational efficiencies and energy conservation

Nagarjuna Cement is one of the chosen brands for Polavaram, the national irrigation project is expected to supply water and stabilize over 75 lakh acres. The dam is being built across the Godavari River in Andhra Pradesh. The project is a multipurpose major terminal reservoir project for the development of irrigation, hydropower, and drinking water facilities. Nagarjuna Cement is the single largest supplier of cement for this prestigious project.

Recently launched Nagarjuna RMC in key urban centres like Hyderabad and Visakhapatnam, and has plans to spread to other locations.

Cement Boards:

To meet the increasing demand and cater to the North India market, the company had set up its second Boards plant with 30,000 tpa capacity in Paonta Sahib, Himachal Pradesh.

Recently added one more plant of 30,000 tpa near the existing plant at Mattapalli in Telangana. Trail runs are in progress

The present total capacity of all the three plants together stands at 90,000 tpa.

The expansion of lamination line unit at Malkapur near Hyderabad and Sandwich Panel Board unit at Paontasahib in Himachal Pradesh are under implementation.

NCLdoor is manufactured at India’s largest door manufacturing facility, which is spread over 2 lakh square feet.

NCL Energy was created to meet the ever-increasing demand for clean power and to this end, two mini Hydel Projects have been set up. The first project was completed at the head regulator of the Srisailam Right Main Canal, which produces 7.5 MW of power, while the second hydel project was constructed on the Right Bank High-Level Canal of Tungabhadra dam and generates 8.25 MW. There are plans on the anvil to set up many projects in the near future and an aggressive expansion strategy is being rolled out.

During the year under review, your company acquired 100% of the share capital of Tern Distilleries Private Limited (TDPL) from United Spirits Ltd, (USL) Bangalore. The acquisition was mainly to utilize the land of TDPL near Visakhapatnam for establishment of a new grinding unit. The existing distillery unit of TDPL has been closed for over two years, and action has been initiated to dispose of the existing plant and machinery.

Your Directors are pleased to report that your company in consortium with NCL Buildtek Ltd has bagged an order worth Rs.1863 Crores for supply of Pre-painted (GI) Steel Window Frame with Glazed Shutters and GI Powder Coated Door Frames to the Andhra Pradesh State Housing Corporation Ltd (APSHC) as part of its implementation of the “Navaratnalu-Pedalandariki Illu Scheme” of the Government of Andhra Pradesh. Your company has a 50% share in the consortium. The order has a tough time-line of 12 months for execution. Successful completion of the order has the potential to significantly contribute to the profitability during the current financial year.

The large order we bagged from the Government of Andhra Pradesh for the mass housing scheme is an opportunity, a challenge and also a testament to our capabilities

The 8.00 MW Waste Heat Recovery Captive Power project set up at a total cost of around Rs.100 Crores at Mattapalli in Suryapet has become operational from March, 2021. The generation of power from this project will reduce the cost of power which will be reflected from the current financial year 2021-22

Cement Division: The expansion of Line 1 upgradation works at Mattapalli (V) in Suryapet district in Telangana State is under progress.

Financials

A major part of the growth was accounted for by the Cement Division, which registered a gross Turnover of Rs.1681.39 Crores which was higher by 52% in comparison with the previous year. Higher capacity utilization and better price realization, coupled with operational efficiencies contributed to this improved performance.

The Boards Division improved its Turnover by around 5% at Rs.131.81 Crores during the year under review (Previous Year Rs.125.92 Crores).

The generation of hydel power during the year was slightly improved by 0.71% at 37.06 million units compared to 36.80 million units in the previous year.

The Ready Mix Concrete division improved its Turnover by 21% at 101.39 Crores compared to Rs.83.84 Crores in the previous year.

The Readymade Doors division registered a Turnover of Rs, 11.72 Crores compared to Rs.1.51 Crores in the previous year an increase of 675% during the year under review.

Rs. 56 cr Trade receivables in Non Current Assets.

HI harshit,

I was curious if your are still tracking this stock. What is your take on this stock and the cement industry. What is your take on the margins for current financial year as well. Also please share how do you see the overall growth of demand in cement industry. If you are still holding this stock are you adding in current fall. I feel this stock is undervalued as of now but will need to dig deeper on the growth side of this company and the industry as well. Please share you view on this company.

It’s undoubtedly undervalued, the humongous buying of promoter proves this, also it’s in a down cycle now which gives margin of safety, capacity wise it may not be comparable, but Door segment & particle wood board segment goes well , also it has a good traction from Andhra Govt capex order,

NCL BuildTek , in which NCL ind. holds 68% stake itself is valued at 330-350cr in the unlisted market. This company makes Doors, Particle boards, Putty, Coatings, uPVC windows etc, (home improvement biz). This translates to a valuation of 225-230cr for NCL.

Deal valuations in cement sector happening at 85-125USD/t Enterprise value - Orient - Adani (116$), India cement 120$, Penna 89$, Kesoram 84$, Sanghi 100$. In comparison, NCL EV/t stands at just 42$ (860m cap+220debt = 1080/3MT), so its a lucrative takeover candidate !

Power assets - 15mw hydro + 8mw Solar + 7mw waste heat recovery = 25MW portfolio, valued between 150 - 200cr. Captive power meets 25% of their reqt.

Recently acquired Vishwambar cement for 322acre limestone reserves @16cr , which it would use as captive mines. Also investing 150cr (90cr term loan funded) for 6.6 lakhs cement capacity expansion in Vizag. Currently NCL is operating at 90-95% capacity, with operating margins 10-11%, so the efficiency of the comapny looks decent.

cement sector as such is not doing good, but deep under valuations, which can be repriced in case of a takeover or IPO of its unlisted subsidiary can unlock value for shareholders.

What happened to the 1863cr door orders?? As far as i could track, they hardly supplied 70-75cr doors in AP Housing project, so what happens to the rest of order?

i dont expect any fantastic growth in NCL, its an event based rationale for value unlocking. Can test investor patience though.

Also, any insights into promoters & corporate governance and any other not so visible aspects of NCL would be highly appreciated !