What’s stealing the show at India’s gaming major, Nazara? Hint: it’s not gaming

Nazara Technologies is inside a plotline reminiscent of the latter stages of a gripping role-playing game. Every move is critical, with consequences echoing through each level. And retreat isn’t an option.

The gaming company—India’s only publicly listed one—has reached a critical point where it has to respond to a pressing question to move forward: gaming or esports?

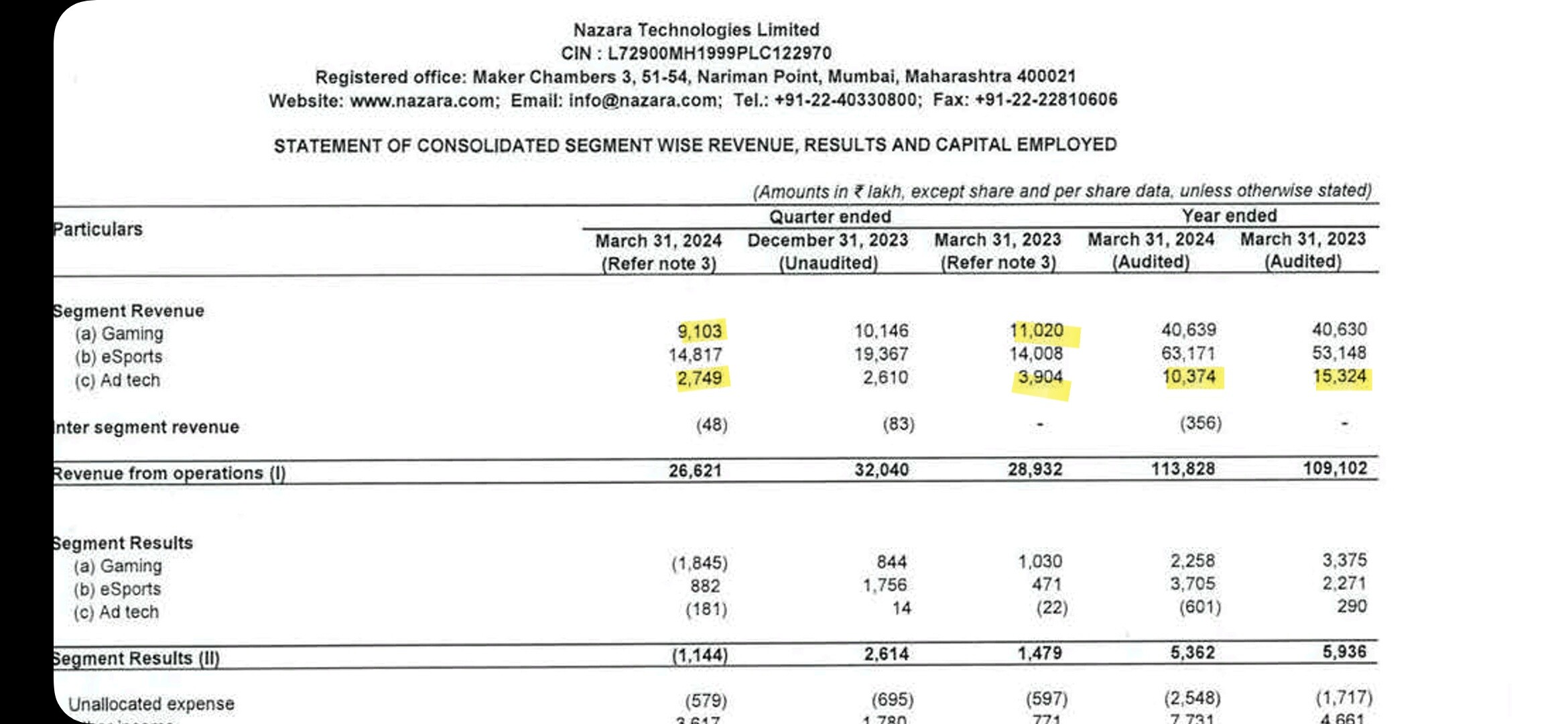

Nazara, with a Rs 5,000-crore (US$611 million) market cap, has made several moves over the years. And all of it has culminated in this: in the year ended March 2023, the growth of its esports vertical, for the first time, outpaced what it calls its “core gaming business”.

In fact, even during the first nine months of the last fiscal, esports accounted for over half of the company’s Rs 914 crore (US$109 million) revenue, as per official filings. Gaming managed to pull in just over a third.

And despite its gaming arm wilting in a post-pandemic slump—troubled by mounting customer acquisition costs (CAC) and economic headwinds—Nazara plans to double down on this segment.

In March, it announced that it would

allocate

US$100 million for mergers and acquisitions. It then set a

target

of ramping up the division’s revenue to Rs 1,000 crore (US$120 million) by this fiscal’s end.

“For us, the core gaming playbook is going to be the focus in FY25,” Nitish Mittersain, the company’s co-founder, joint managing director and chief executive (CEO), told The Ken in an interview.

In a nascent market like India, Nazara’s had

multiple pivots

—from selling mobile games in partnership with telecom companies to an incubator-style model focused on acquiring and scaling gaming companies.

Its two esports units—Nodwin and Sportskeeda—have grown their revenues by over 23X and 9X since their respective acquisitions in 2018 and 2019. But this segment is a tough nut thanks to narrowing margins.

So, the company can’t rely solely on this segment for growth.

That’s why Nazara is focusing on expanding its roster of gaming properties, noted Mittersain. But given gaming’s sluggish growth, Mittersain has to pull off a great balancing act—especially since the 44-year-old is back at the helm after seven years.

Making a comeback

Mittersain is no stranger to navigating troubled waters.

In his earlier stint, he steered the company through the turbulence of the

dot-com bubble

. Now, the task in front of him is to navigate his company through an uncertain time for the gaming industry.

Now, over the past few months, he has led Nazara’s Rs 750 crore (US$90 million)

funding round

, bringing in high-profile investors like Nikhil Kamath (co-founder of discount broker Zerodha*) and two of India’s biggest asset management companies, SBI Mutual Fund and ICICI Prudential Mutual Fund.

He will need all that cash to drive his gaming company through a familiar yet challenging terrain, far from the excitement surrounding its US$80 million initial public offering (IPO) in 2021.

But what renders gaming indispensable to Nazara?

Unlike esports, the gaming vertical is built on its own intellectual properties (IPs)—from arcade mobile to educational to real-money games. Since it owns the IPs, it can expand them into more lucrative areas like Youtube content or merchandising. Much like the billion-dollar grossing film The Super Mario Bros. Movie, released in the US based on gaming giant Nintendo’s Mario franchise.

But Nazara’s gaming properties have hit a wall in terms of growth.

Kiddopia, a gamified e-learning app and flagship in Nazara’s portfolio, generated Rs 220.6 crore (US$26 million) in revenue for the year ended March 2023, marking only an 8% growth from the year before. Also, its EBITDA declined by almost a third to Rs 35.7 crore (US$4.2 million), and its subscriber base dwindled in four of the five preceding quarters.

In reality, all of Nazara’s gaming properties have struggled to grow, according to an equity research analyst monitoring the company. They and several others quoted in the story declined to be named due to their company’s media policy

The analyst pointed to the free-to-play mobile game World Cricket Championship, one of its pre-IPO acquisitions whose revenue growth has stagnated in the past 2–3 years.

It’s a testament to how difficult it has been to monetise Indian gamers thanks to “wanting everything for free”, said a former executive of Nazara.

That‘s likely why Nazara looked to diversify its gaming business across geographies with its later acquisitions. Both Kiddopia and the educational game Animal Jam earn 80% or more of their revenue from the US, according to Nazara’s filings and investor presentations. But they, too, haven’t been immune to the macroeconomic headwinds

Then there’s the

data-privacy crackdown

by Big Tech, such as Apple and Google, that adds a pricey twist in the CAC game, said the former Nazara executive.

Perhaps that’s why Nazara is eyeing a bigger stake in real-money gaming (RMG).

RMG turnaround

By largely avoiding RMG, Nazara lost out over the past years.

“We were very conservative in our approach. In a way, it was a missed opportunity,” he told The Ken. “The reality is that the only thing in gaming that has really been monetised in a big way in India is RMG.”

Mittersain previously stated that Nazara’s Indian investments from its US$100 million M&A fund will solely fortify its RMG portfolio, currently anchored by the Classic Rummy app. He said that Nazara is setting sights on RMG firms with revenue of “at least a few hundred crores [tens of millions of US dollars]”.

Meanwhile, problems in the sector have piled up, and it is teetering on

life support

amid heavy taxes on online gaming. For instance, Classic Rummy’s EBITDA plummeted to Rs 80 lakh (US$96,000) in the nine months ended December, a significant drop from Rs 8.5 crore (US$1 million) the previous year before the

new GST policy

took effect.

Yet, leaning on this model is still a safe play.

“RMG, as a market, still works in India,” remarked Adi Vemuru, former chief technology officer at Openplay Technologies, the Nazara-owned company that operates Classic Rummy. But the companies need to optimise their unit economics, which means scaling up the user base. “If you consolidate with others, the bleed can be controlled.

Clearly, Nazara shares the same perspective.

But as gaming faces a crunch, what about the vertical that has remained consistently strong?

Riding the wave

The strength of Nodwin—which saw an 84% surge in topline in the year ended March 2023, closely followed by Sportskeeda with a 55% growth spurt—lies in their reliance on third-party properties. This mitigates dependence on any single product’s success

“[In the gaming business,] developing, publishing, marketing, user acquisition is a massive struggle,” explained the former Nazara executive. “[In esports,] you don’t have to break your head about the product itself. You’re just creating a vehicle for the product.”

Sportskeeda, for instance, has remained resilient against the

slowdown

in digital-ad spending despite its revenue model being driven by advertising, according to Anirudh Kumar, chief strategy officer at Absolute Sports, the parent company of Sportskeeda.

“[This is because] sports is an evergreen category,” he said, elaborating that regular flagship events such as the annual Super Bowl in American football or the 2022 FIFA World Cup

continue to grab eyeballs.

Meanwhile, Nodwin—a market leader—contributes over a third of Nazara’s revenues. But the margins are a challenge. The EBITDA margin took a dive from 7.4% in the year ended March 2022 to 1.8% the following year and dipped into negative territory in the next nine months.

This can be partially attributed to a failed acquisition.

In March 2022, Nodwin bought a 35% stake in Wings, a gaming-accessories brand specialising in headphones and speakers. But, as the above-quoted analyst pointed out, this is a capital-intensive venture requiring consistent investments, and the products are sold at significant discounts, which eats into margins.

Mittersain admitted the deal didn’t pan out as expected, stating, “We realised that’s not a business we really want to be in. We have deconsolidated [sic] that business from February.” This means Nodwin will cease further investments in Wings

Will that be enough, though?

Waiting to click

Esports companies like Nodwin are in a “very operations-heavy business. It’s a volume game,” said a senior e-sports executive at global gaming conglomerate Tencent, which has partnered with Nodwin for several events.

Organising an esports tournament involves submitting proposals to game publishers like Garena or Krafton, who evaluate them based on costs and event experience. So, it’s difficult to charge a premium beyond the high cost of venue arrangements, broadcast equipment, technical infrastructure, and more.

The Tencent executive stressed that building strong partnerships and bringing operations in-house can slash costs and boost margins. Yet, replicating this scale at Nodwin’s level could prove daunting.

Meanwhile, selling broadcast rights for esports tournaments to media houses and streaming platforms represents another avenue for growth, the analyst noted. “Media-rights revenue offers margins without additional investment.”

But Nodwin hasn’t been able to pull that off

Its media revenue for the nine months ended December totalled Rs 50 crore (US$6 million)—a 36% year-on-year dip. The figures in the year before were also nearly flat.

Mittersain doesn’t refute this, either. “[Nodwin] will really become profitable the day media rights take off. But the reality is, it’s not happened yet. We’ve seen early signs of it happening,” he said, recognising that such a development is still some time away.

A major factor in this delay is the geopolitical tensions between India and China. In recent years, the Indian government has cracked down on apps with ties to its neighbour, including temporary bans on popular esports titles like BGMI and Free Fire.

While they were

unbanned in 2023, the future remains uncertain: sponsors are

wary of splurging until the storm blows over

In the face of unique challenges in esports and gaming, can Nazara maintain a balance between growth and profit margins?

One can’t ignore Nazara’s profitability, positive cash flow and two-decade survival that set it apart from the newer, disruption-driven tech startups.

Mittersain’s focus now is on the core business—“How do we improve the metrics? How do we make it cash flow-positive, self-reliant?.”

Despite the muted demand for online gaming, India’s gaming market is still estimated to grow to US$7.5 billion by the year ended March 2028 at a compound annual growth rate of 20%, according to gaming-venture fund Lumikai’s State of India Gaming Report from October 2023.

In the quest for that treasure, Nazara will be powering up with its US$100 million war chest over the next two years. With its stock down by nearly 19% since the IPO, this could just be the respawn point it needs