NBV was established as a ferroalloy plant in India in 1972. Since then, the company has expanded in power (734 MW), agriculture (25000 hectares) and healthcare across Southeast Asia and Africa. Currently, the ferroalloy plant has a capacity of 200000 tons per annum. As of FY23, this is the summary of the assets held by the company.

Ferroalloys

2 facilities. Telangana has a capacity of 125000 tons / annum. Odisha has a capacity of 75000 tons / annum. Till, December 23, the Odisha plant was converting FeCr for the Tata’s at a fixed cost. Now, Nava is producing SiMn from that plant after converting it the furnaces.

Energy

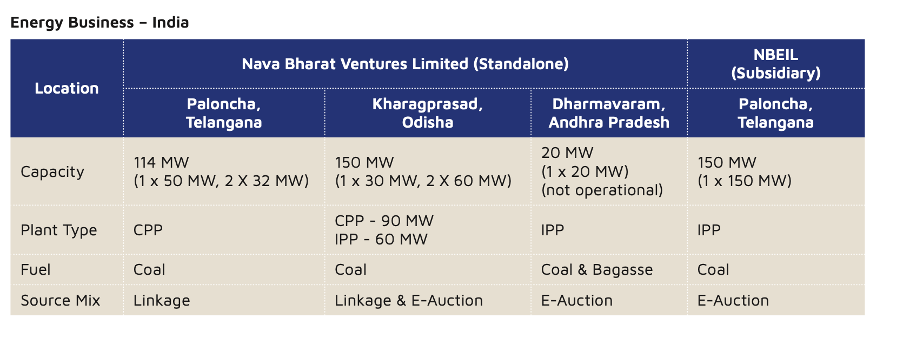

The following table is a concise description of the power assets in India.

CPP – captive power plant. IPP – independent power plant

Nava uses its own power plants to produce ferro alloys. It is dependent on the auction coal in India. Also, the company is not using the 20MW unit in AP due to low efficiency.

Nava has a 300 MW plant in Zambia which is 10% of the power capacity of Zambia. The subsidiary, MCL is 65% owned by Nava and 35% owned by the Government of Zambia. This power plant is supported by a 190-million-ton coal mine in Zambia. Out of the 300 MW, about 32.5 is auxiliary consumption, 180 MW is the long term PPA by ZESCO (electricity board of Zambia) at .11$ per unit (super high rates) and the rest 80 MW can be sold to other African nations or to Zambia on spot prices at .14$ (according to the con-call). The power plant is running at superb capacity –

Mines

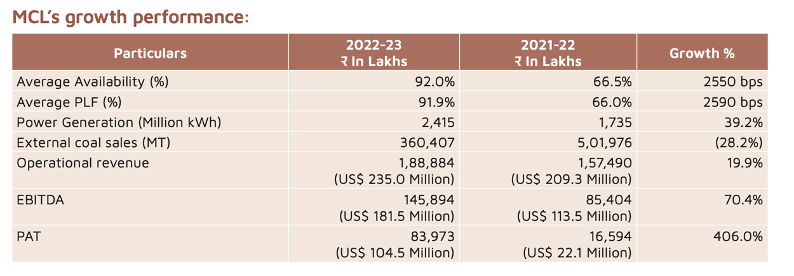

The company owns coal mines in Zambia. To produce electricity at 91.9% PLF (2415 million units), Nava required 1.491 million tons of coal + it sold 0.36 million as merchant sales. Currently, it is increasing the pits and therefore the production by 45k to 60k tons/month.

Exploratory work of ferro manganese ore mines in Africa – Nava has started exploring for FeMn mines in Cote d’Ivoire over an area of 64 sq.km. This adds well with the synergy of the group and securing raw material for the future. Deadline – end of FY24.

Other businesses

Agriculture – KSL – Nava has procured 25,000 hectares of land in Zambia. It wants to plant avocados and sugarcane. This land is surrounded by 2 rivers, so there is ample water for the cultivation. The company also has the capability to make ethanol from sugarcane juice for blending with fuel. Initially, the company wants to plant avocados and then plant sugarcane. Expected expenditure is 40 million $ in the next 4 years to grow avocados in 1100 hectares.

Healthcare – TIASH – This company is 65% owned by Nava and 35% owned by its current CEO in stock options. It has clinics which focus on iron deficiency in Malaysia & Singapore.

The other businesses are a very small part of the business and are at a very nascent stage. For the report, I have ignored the details in this section in the thesis.

Corporate Structure

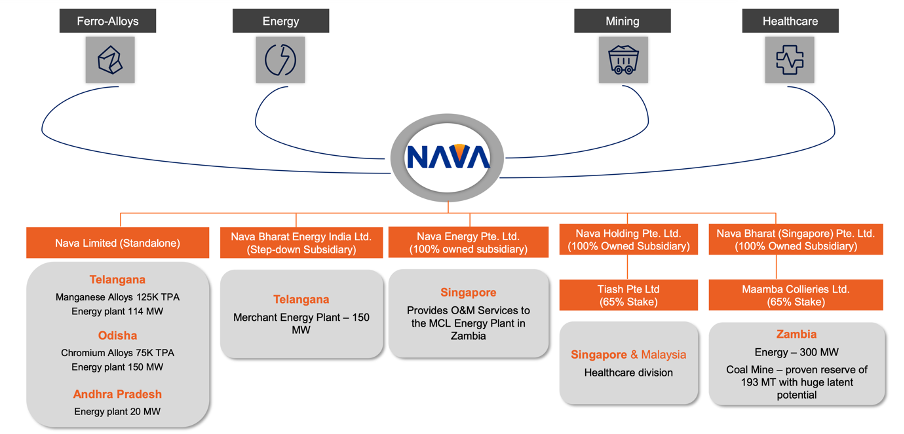

The company has a complex structure. There are a lot of subsidiaries and subsidiaries of subsidiaries. For the purpose of this thesis, we are exploring the structure with regards to MCL (African subsidiary which has the power plant and the coal mine in Zambia) and the Singapore subsidiary of Nava – Nava Bharat Singapore (Singapore). The mother company, Nava Limited (NL) is the Indian company which controls most of the subsidiaries. The strategy of the company thus far was that NL would give out loans to Singapore to invest in other wholly owned subsidiaries of Singapore. NL gave a loan of 738 cr to Singapore which was then invested as equity in MCL through the Singapore subsidiary. In exchange of the investment, Singapore received 65% of the shares of MCL.

Numbers

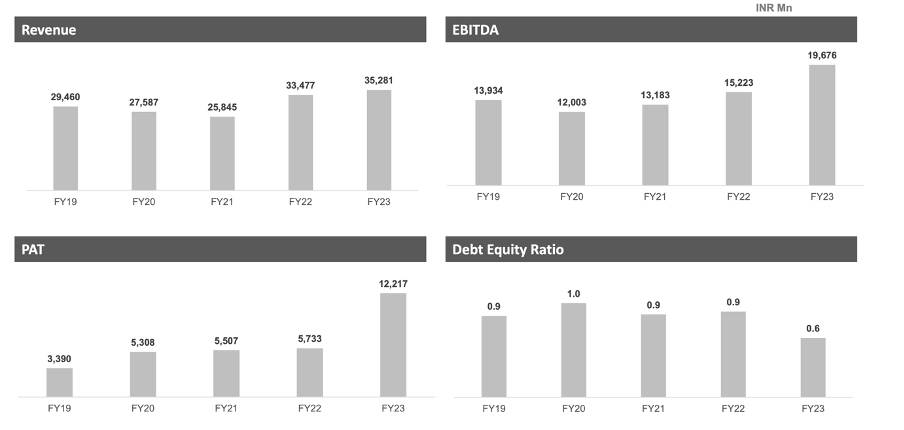

From the figure, revenue increased marginally from 3347 cr to 3528 cr from FY22 to FY23, a very nominal change but the PAT from operations increased from 573 cr to 1221 cr. The PAT including other exceptional income increased from 679 cr to 1518 cr during the same period. This is a huge jump. There are mainly 2 attributes to this –

-

- Increased efficiency in the power plant – MCL’s PLF increased from 66% to 92%.

-

- Reduction of ‘Allowance for credit loss’ from 322 cr from FY22 to FY23. This allowance was taken in FY22 because the management was not sure regarding the payment of the electricity supplied to ZESCO.

This is an income boosting transaction. If, adjusted for the ‘Allowance for credit losses’, the PBT from operations of the consolidated business in FY 22 would be 1220 cr which is just 46 cr lesser than FY23. Only thing changed was that the company now was receiving payments from ZESCO. Here are the following reasons why profitability in FY23 was not great –

-

- FY22 was an exceptional year for ferroalloys business and the prices were very high. In FY23, the prices of ferro alloys were rock bottom.

-

- The PLF of stand-alone power plant dropped from 64.3% to 61%. This was due to coal shortages. The company had to wheel the power from the board to produce ferroalloys. This led to shutdown of a 20MW turbine also.

-

- The PLF of Indian subsidiary power plant dropped by 18%. 2 reasons for that – a major overhaul and delays from Telangana utilities to provide open access permission to sell electricity in the grid. The company has challenged this in the High Court and there may be some delays in getting the appropriate permissions.

-

- Taxations – The company paid over 323 cr in taxes on FY22. In FY23, it paid only 44 cr. The company took benefit of 86 cr of deferred taxes.

-

- The Odisha plant had a capacity of 75000 tons of manufacturing FeCr. The furnaces were converted after the mutual decision of Tata and Nava to end the contract prematurely. The furnaces were producing SiMn in FY23 after that.

Standalone profit reduced from 381 cr to 322 cr. MCL made up for profit lost in FY23.

The profit is the same, but the cash flow of the company has substantially improved. In FY22, the cash flow from operations was 608 cr but this year it is 1223 cr. This is mainly because of the reduction of account receivables. The working capital outflow last year was 813 cr but this year it is 283 cr. This is a substantial improvement. The company has paid 37 cr of long-term debt last year. This year it is 832 cr.

Thesis

MCL was suffering because ZESCO was not paying for the power as per the power purchase agreement. By FY23, Zambian Government has settled 1488 cr (120 million $ + 60 million $ write-off).

Payment structure of the remaining 413 million $

| Month / Year | Dec 23 | Dec 24 |

|---|---|---|

| Amount | 234 million $ | 180 million $ |

The loan outstanding of MCL is 285 million $ (2475 cr) as of FY23 which is to be paid in 11 half yearly installments. As of June 2023, the outstanding loan balance was 206 million $ and the outstanding payment from ZESCO was 397 million $. Now, there is no loan overdue on the company’s end.

The interest on these loans is anywhere between 5-7.5% + LIBOR (about 12%).

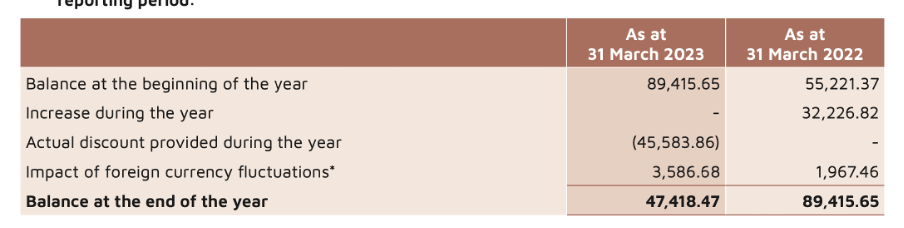

There is hardly any material change in the current and non-current account receivables number between FY22 and FY23. This was mainly because of reduction of ‘Expected credit loss on financial assets’. As seen by the cash flow statements, there was no increase of receivables in the Zambian entity in FY23. All the increase of receivables in FY23 were due to standalone entity. In FY22, 850 cr was the increase in receivables due to MCL.

Market cap – 5012 cr company as of 27/7/2023.

Cash – 931 cr.

Outstanding balance – (3396-2495)*65% = 585 cr (Zambian Government owns 35% of Zambian subsidiary)

This equates to 1516 cr. You are getting the entire company at a 3500 cr valuation. I have assumed that the entire debt is serviced with the money received. The PAT will increase by 300 cr due to lower interest payments. Therefore, the PAT of the company should be about 1800 cr. The 2 year forward looking P/E is roughly 2.

Safety nets –

-

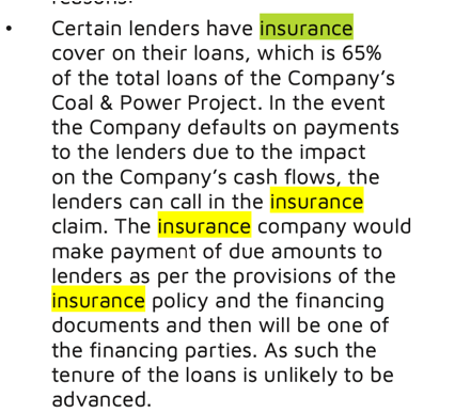

- The company has won the arbitration from the UK court regarding the payments. These loans are secured by the insurance company which required them winning the arbitration. The insurance covers all the outstanding payments to the banks. So, I think that the risk of debt burden is mitigated.

-

- The second thing is that the company is a part of SAPP, and they can supply power to entire southern countries in Africa. It does not have to be dependent on Zambia.

-

- As of FY23, out of 3528 cr of revenue generated, 2280 cr is from power. This can lead to a re-rating of the company as Nava is more of a power company than a ferro alloy manufacturing company.

Risks –

-

- Diversified business – The company is engaging in agriculture and healthcare business which is not a core competency of the company.

-

- Zambian govt may not honor its commitment to Nava and not abide by the payment schedule.

-

- Such a big payout at one time may lead to misallocation of funds.

-

- Another coal mine has opened and giving a lot of competition to the company. This year, the merchant sales were lower than the years before, but the overall coal consumption was high because of higher consumption of coal internally.

Income boosting transaction of 474 cr that the company can use in the future.

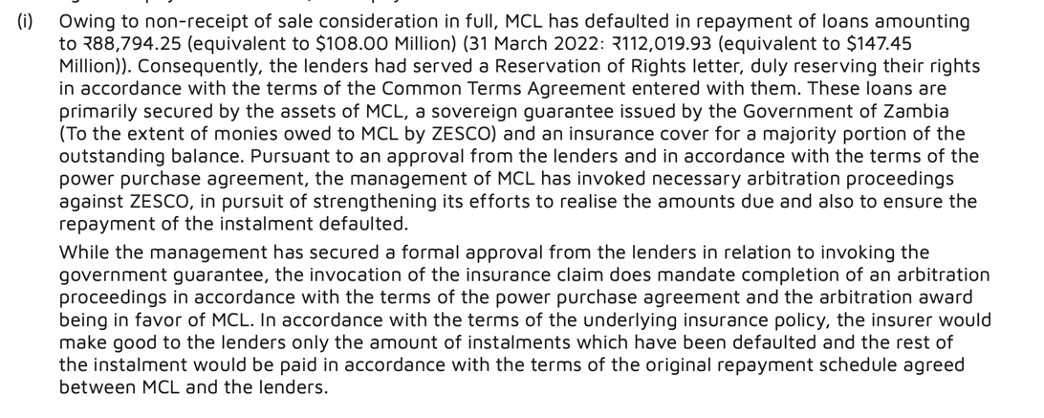

Page 253 of the FY23 annual report

Page 285 of the Annual Report FY23, highlighting the insurance terms of the loan.

Disclosure - Invested