@nav_1996 What if your view on diversified vs concentrated? What do you think is the ideal number of stocks in the portfolio?

Around 15 is what is comfortable with me. Helps me diversify across industries/biz houses etc Beyond 20 standard deviation(measure of risk) does not change much

3 Likes

Just an opinion, over which discussions are most welcome.

Stocks with low RoE, RoCE, Sales or absence of an increment in EPS over last 3 years, are at most risk. If there is a general correction, then such stocks will be affected the most, and double the effect of it’s a small or a midcap.

Having Gold ETF would be better than having any such stock in hand.

Time to be careful.

Hello @nav_1996

Do you still hold Repco & ITC?

Repco’s yearly results were OK but the stock is near to 52 Wk level. What is your take on this scrip

I see you have a clarity of purpose and expectations from market, which is really good. Some points which came to my mind, I maybe wrong…

- Being conservative investor, allocation to financials is very large, almost 35% out of which more than 20% to single group, although best so far.

- In those financials, no direct life insurance company, the business of which seem to match those of long term conservative investors i feel

- Pharma I never could or can understand. I missed the bull and then the bear in pharma so cannot comment in who winners can be. In short it seems to me one of the tougher sectors than it looks like, something like hospitals also…where I lost money.

- In FMCG I see you hold agro tech. I also have been holding it for years now with no returns. The company shows no growth, no significant new products. I think problem is that their US products are ahead of time in India or not suitable for Indian markets while Indian r&d and India specific launches strength is low. Let me know your thoughts on this.

Thanks

Pointwise reply

- Financials have grown quicker so they have ended up as high % of portfolio. My picks are also high quality finacials. So I am not trimming but have stopped putting fresh money into financals. So it will restore balance in few years.

- Don’t understand insurance. Find them costly compared to global/chinese companies. I am exposed through Kotak and HDFC.

- Pharma is mixed bag - Could not sell at top. Glenmark is back to 400+ from 1200. My price was 300 ages ago. Same story with Lupin

Just have Biocon/Lupin/Glen

Just have Biocon/Lupin/Glen - Agree about Agrotech. Trimmed Agortech to very small position and moved to ITC

Just have Biocon/Lupin/Glen

Just have Biocon/Lupin/Glen

1 Like

No, sold Repco a few years back. It was a wrong pick though I made some money.

Have added more to ITC.

1 Like

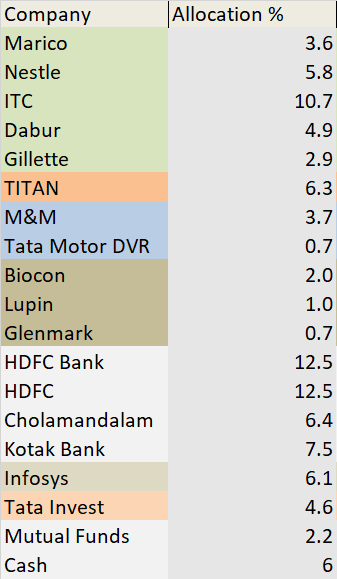

Would you give an overall update on you current PF in terms of percentage allocation. I could see that last update was about 2 years ago. How the PF performed in last 18 months.

Below is my current portfolio.

Company Allocation %

No drastic changes. Exited Agrotech(poor growth/portfolio overalp with Marico), reduced Biocon(uncertainity) and TaMo(JLR story got derailed). Added to few positions when valuations became attractive.

3 Likes

I don’t really track that. I watch out for under performers and try to analyze that. For others I revisit and see if story has changed.

I have further tried to move towards “Not loosing is best aggressive strategy”

2 Likes

Hi

Good picks.

Could you post the latest PF & how has been the experience in topsy turvy market over last few months?

| Company | % |

|---|---|

| Marico | 6.9 |

| Nestle | 13.4 |

| ITC | 9.0 |

| Dabur | 9.7 |

| Zydus Wellness | 6.5 |

| Gillette | 4.2 |

| TITAN | 10.1 |

| M&M | 6.3 |

| Biocon | 5.1 |

| Lupin | 2.4 |

| Glenmark | 1.6 |

| HDFC | 18.6 |

| Cholamandalam | 5.7 |

Got rid of banks both Kotak and HDFC, definitely not at top. A couple of reasons. Becoming too big in mcap term in relation to economy. Issues with rising credit costs. Company specific issues. HDFC Bank - Already have exposure thru HDFC and CEO transition. Kotak - Slower growth, subsidiaries not scaling up to top 3, RBI may not allow promoter to continue as CEO, without him it is expensive stock.

TataMotors - Not a rosy picture now.

Tata Invest - Got good exit point and it was more of a proxy to MF.

Infosys: Mature and slow growth. Will use this to invest in US tech oriented funds.

Added Zydus wellness by exiting Agrotech and trimming ITC. It has wellness products which can have real long runway.

4 Likes

Thats a solid portfolio! Looks like carefully built over last decade?

We share few names in common. I see from Jan to May - Your allocation to Nestle, Dabur and Marico has gone up among existing holdings. More so on Dabur and Nestle…is that result of price action or new addition in fall?

Among P&G firms, any reason to chose Gillete as compared to P&G HH?

Regarding Zydus Wellness - Ealier their major product were sugarfree and nutrilitie. There were some health concerns about chemical sweteners. Some experts say they are actually more harmful as compared to sugar over long term. Also, they purchased complan at a significant cost that would have added debt…what are your thoughts on this and also on the promoters quality? Thanks

% Has gone up as I sold banks and these stocks have not got down in price. No additions.

Gillette has virtual monopoly in razors, I don’t see any competition in shops. P&G HH main revenue driver is sanitary napkins, though has strong brand moat, it is not monopoly.

Zydus wellness buyout was not super expensive but at right price. Complan was a minor brand. Two other leaderships brand which came along were Nycil(nice fit in skin care portfolio) and Glucon-D (nice fit in health portfolio). Both are market leaders. SugarFree may have minor side affects but millions die from sugar and no one has died from SugarFree ![]() As it gets more researched and accepted this can be huge with more than 90% market share. Hoping for the best. Don’t want a repeat of AgroTech Foods. Promoter’s quality seems to be ok (Zydus Cadila promoters). Held by PPFAS.

As it gets more researched and accepted this can be huge with more than 90% market share. Hoping for the best. Don’t want a repeat of AgroTech Foods. Promoter’s quality seems to be ok (Zydus Cadila promoters). Held by PPFAS.

3 Likes

Pls check more details on harmful effects of ingredients of all sugar free products - here I am not referring to Zydus’ sugar free brand but anything which has artificial sweetners. There is no free lunch in this world and same applies to sugar free as well.

In US there are plenty, and they keep confusing consumers with new ingredients and new products by new companies which call them “natural” etc etc. However, many consumers have realized that for otherwise healthy individual, these cause more harm than sugar…and for those with diabetes - most of them find leaving sugar better than these artificial sweetners because of the taste and also their other harmful effects.

Btw no one eats too much sugar to cause diabetes…it happens because of multiple factors…anyways that is a seperate discussion…

1 Like

Updated PF

| Company/Fund | % |

|---|---|

| Marico | 5.8 |

| Nestle | 7.2 |

| ITC | 7.7 |

| Dabur | 6.2 |

| United Spirits | 4.6 |

| TITAN | 9.6 |

| M&M | 5.6 |

| Biocon | 2.8 |

| Lupin | 1.5 |

| Glenmark | 1.3 |

| Sanofi | 2.7 |

| DSP Pharma Fund | 0.7 |

| HDFC | 17.6 |

| Cholamandalam | 10.4 |

| L&T | 6.3 |

| Edelweissh US Tech Fund | 2.0 |

| OFSS | 8.1 |

| Bharti Airtel | 4.4 |

5 Likes

Nice portfolio! A solid 8% new entry in OFSS during the crash it seems.

L&T , M&M, United Spirits rightly placed to capture growth when capex, discretionary consumption grows

I dont track Cholamandalam but since you own significant 10%, I will research about it.

Would be nice if you can share more about this company as well

What is your thought process on Bharti Airtel? I once thought to enter as they are as capable of developing the digital platform like how Jio has built. Would be nice to know your investment rationale and vision for Bharti Airtel

Also, do keep writing. We seldom come across seniors who are into market since as long as you and who also have the patience and vision in them to keep holding a 35X!!

Also, nice to see a FMCG heavy portfolio.

Many argue that FMCG investing is slow growth and high valuations but they miss on few important aspects like -

- India is still a developing economy and FMCG consumption of even the most basic & organized, decent quality goods is abysmal

- Not to mention the capability of premium, niche FMCG products

- Plus, we have certain small home grown FMCG firms which are comparatively very small in size but very big in aspiration & talent

- Lastly, India has many industries which are highly valued and many top quality companies in every industry is highly valued, so why everyone is mostly concerned about FMCG alone - Probably because it is most boring, most simple & most straightforward investment and we as investors tend to complicate things more often than not!

Best Wishes

2 Likes

OFSS: This was to compensate for my big mistake of exiting Infosys. No I got in after recovery around 3000. It services companies had run up fast but this was still available at pre-Covid prices.

L&T: I have initiated a thread on this. Please check that.

M&M: I like their exposure to cyclical economy but still differentiated and diverse product range. They keep investing in new biz. This can be good(chase new opportunities) as well as bad(poor capital returns as some will not succeed).

Chola: It is number one in CV financing. Run by a competent and ethical management. This has runup 10x so forms a large chunk. Will trim it slowly over few years.

Bharti Airtel: This is digital infra bet. We have always though infra as physical infra only.India data cost is 1/100th of US. Can not remain like this forever. But not sure when that trigger will come. Probably when economy stabilizes, operators will be comfortable raising prices. Huge operating leverage. Any increase in revenue flows to bottomline. This is also a play on African growth, IoT and 5G. Berkshire Hathway bought Verizon recently.  So I am in good company

So I am in good company

3 Likes

Time to update PF this Diwali

| Holding | % |

|---|---|

| HDFC | 20.0 |

| Cholamandalam | 12.0 |

| TITAN | 12.0 |

| M&M | 9.0 |

| Nestle | 7.0 |

| L&T | 6.5 |

| OFSS | 6 |

| United Spirits | 6.0 |

| Dabur | 5.0 |

| Marico | 5.0 |

| ITC | 3.0 |

| GSPL | 2.5 |

| Biocon | 1.5 |

| Wheels India, FDC, Lupin, Glenmak, Indus Towers, LIC, Just Dial | <1 |

Core PF has not changed at all.

- Lost patience and trimmed ITC at cheap valuation. Pathetic decision. Lessons learnt.

- Have sold MFs after losses. It was small part and doing well. More of a consolidation process

- Added to HDFC in correction.

- Sold Airtel as it is very capex heavy biz. Digital hype has not played out well.

- Have made small opportunistic bets based on valuations. Have not quite worked out.

- Added GSPL as gas sector bet. Has been a disaster due to rising gas prices.

2 Likes