Stock has already corrected approx. 60% from the high after the demerger. Is it the expected price because of holding company discount or we can expect some up move?

The value of the major investments in Britannia via BBTC stake ( 9.43%) comes closer to 5000 crores approx Plus 0.9% stake in bombay dying worth 28 crores.

So holdco discount here is 89% which is too cheap.

| As on 10th Oct 2023 | |||||

|---|---|---|---|---|---|

| Value of Investments | |||||

| Market Value of Investments | No of shares held consol | Issued sh. Cap | % holding | Mkt cap( in cr) | Intrinsic value |

| BBTC ( REF.Page 170 of AR - 2022) | 6585117 | 6,97,71,900 | 9.438064608 | 8611 | 5042.361521 |

| Bombay dyeing | 1895900 | 20,37,56,125 | 0.930475096 | 3093 | 28.77959472 |

| 5071.141116 | |||||

| Current Mkt cap of NATIONAL Peroxide holding co( in CR) | 542 | ||||

| Discount to Intrinsic Value of Holdings % | 0.893120702 | ||||

| Intrinsic Value of BBTC | % terms | Mkt cap | Value( in crores) | ||

| Britannia Stake | 50.54% | 109000 | 55088.6 | ||

| Bombay dyieng stake | 40% | 3093 | 1237.2 | ||

| 56325.8 | |||||

| Net Debt | -2900 | ||||

| 53425.8 |

| Hold co discount comparison of Wadia Group | Mkt Cap (in cr) | Approx Intrinsic Value of equity Investments ( in cr) | % Discount |

|---|---|---|---|

| BBTC | 8611 | 53425 | 0.838820777 |

| National Peroxide ex demerger | 542 | 5071 | 0.893117728 |

| ** | Equivalent Discount to BBTC | ||

| ** | Est. mkt cap in crores | 817.3398409 | |

5 Likes

I think this much discount may remian for few reasons.

Being a small cap & no dividend.One example being Kalyani Invest.

My primitve guess is if they start declaring dividends, this discount may get narrowed.

Personal opinion.

dr.vikas

@ Vikasbargale Agree with your point but i think two wrongs dont make right ![]()

Looking at the current chain of events, looks like wadia group are on the verge of restructuring . They are trying to restructure less complex things ,my hunch is major restructrung is on the cards and these are all precursor to the same .

1.NPL demerger

2.Bombay dyeing land bank monetization

My hunch is next course of action would be merge all holding companies .

Anybody with 2 years time frame will have good risk reward ratio.

Disclosure : Invested very small amount for tracking purpose.

5 Likes

I agree with your valuation metric but if we want to evaluate the chemical company which is going get listed in the market maybe in few days is this the process example.

sale for the current year is 380cr and the market cap to sales ratio is 3.2 median which means the valuation of the listing company will be at 1216cr.I know the other metric are also will be taken in account. I don’t know i am write or wrong plz correct me regarding this.

1 Like

Does anyone has any idea when the demerged share will be listed? It has been 2 months since the record data, and yet no communication of the listing date.

Hi Gaurav, the market value of Investments - both shares and land is approx. 1050-1100crs and at 50%-60% valuation, seems like National Peroxide market price is at fair levels. Hope NPL Chemicals listing happens soon so that we will get to know if there has been unlocking of valuation in line with mgmt intentions. Thanks

@ parash :you may check the valuation again is way higher, calculation is already mentioned in my previous post.

Hi Gautam, BBTC mkt cap is 10k cr. Nat per holding is approx. 9.5% which equates to -900crs. Requesting you to kindly check. Thanks

@Gaurav2000k Gaurav* Sorry. Auto corrected.

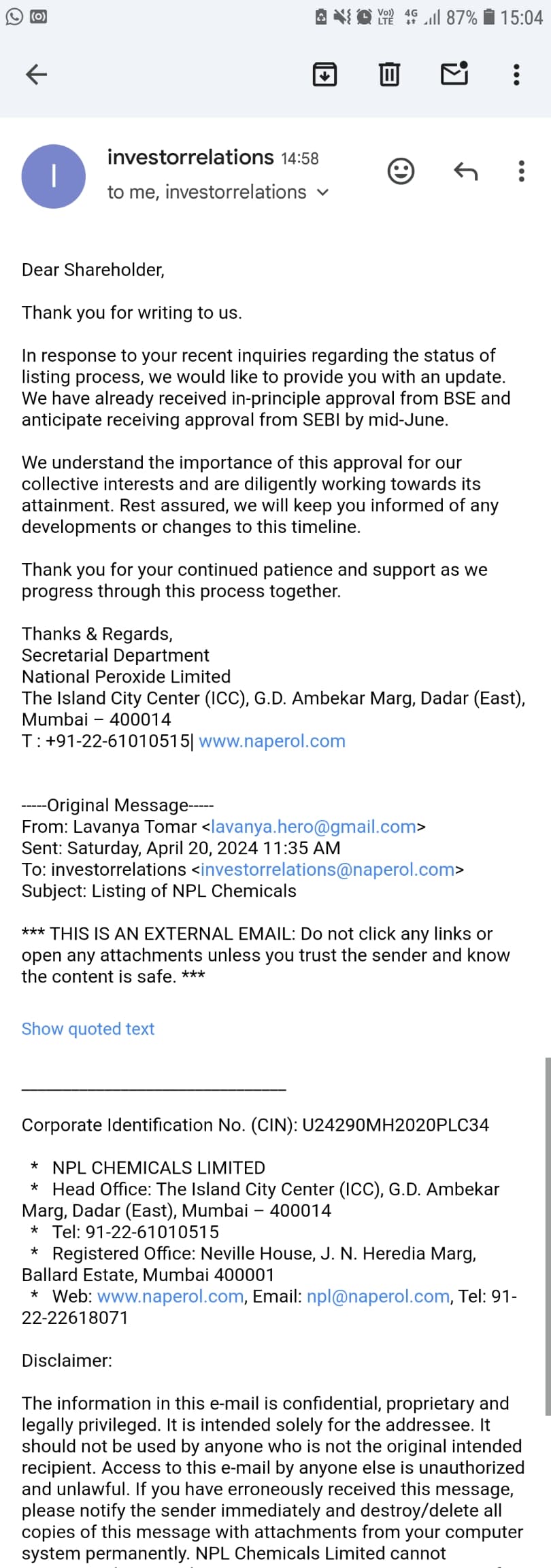

Any updated on listing of NPL Chemicals?

Demerger happened two and half months back, still no info…

Have anybody wrote to management and go reply ?

1 Like

Mailed CS 14 Times

Still no reply

Worst corporate Governence imo

listing of demerged business will take time . redtape takes almost 4 months .

Name Change - From National Peroxide to Naperol Investments

Hope this helps.

dr.vikas

1 Like

I see the stock on my NSDL statement that comes in my mail.

![]()

Is there any update with regard to listing of shares??

is this anyone knows when npl chemicals willl be listed

Hi Lavanya

Did they update on the situation?

Notice Number Listing from 4th July

2 Likes