Hi,

We are analyzing National Fittings and have it to be doing good on operational, financial and historical growth parameters

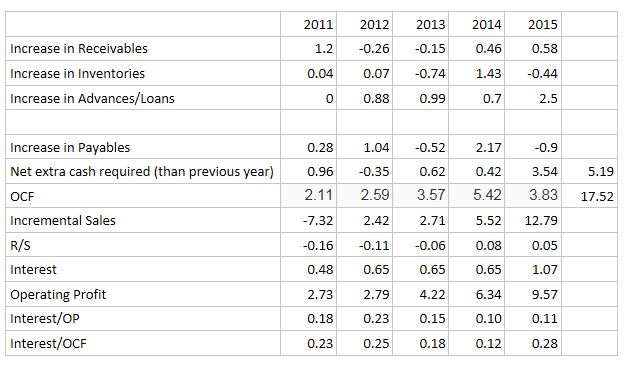

- Operating efficiency:

Here we see that the operating cash flow from last 5 years is able to easily meet the working capital requirements. Hence, the company has been able to manage its sales, receivables and payables from internal cash flows. Also, interest component can be written off from CFO by debt prepayment (almost equal).

- Financial health:

Inetrest/Operating profit and Interest/CFO - company has sufficient debt coverage which gives it room for aggressive sales, aggressive WC management and growth. D/E is 0.12 whereas promoter holding is close to 65%. So, promoters still have option to dilute equity if required without losing control. However, it is not required since CFO is generating enough cash to meet growth.

- Historical growth:

Sales growth rate 10 years - 24%; 5 years - 14%

PAT growth rate 10 years - 46%; 5 years - 21%

PAT growth rate can be more than sales growth rate given that company doesnt have significant interest expenses, no new Capex which would lead to depreciation. Hence, incremental sales will lead to higher operating leverage.

Now, all this looks fine, but before investing, we have the following queries/concerns:

- It has only 1 unit which is split across Dindigul and Kaniyur. Concern is how much incremental sales could be achieved from this unit? Additional setup of units would require close to 7 crore excluding land which if materialized would hit EPS in short to mid term.

- Is the management competent to double sales from here. It looks like it is still a completely family run business with the promoter being 73 years of age. Annual report gives just a new director’s name but not sufficient information on her role and responsibility. (she is marked as being more of an operational person rather than sales person)

- Which are the key competitors with whom National Fittings would have to fight out for growth?

Disclosure: Not invested.

Regards,

Akash & Nikhil