Just wanted to understand the 1yr forward P/E of the company which is currently at 18x.

The average one year forward P/E of the Indian pharma cos. including the ones which are currently facing a lot of troubles from US businesses. have been around 26x. Natco, with clear focus on complex generics, steady pipeline of blockbusters, sound management team, and most importantly with the ability to recognize industry changes ahead of competition and accordingly reshuffle business plans is trading at a low valuation compare to peers. Definite buying opportunity according to me. If someone is cautious whether it can sustain growth post 2020 / long term, then that is true for the entire pharma sector. No company can assure you a very very strong growth for 10 years or even 5 years with so much competition. I think what is important is to back management ability to identify opportunities and act faster than competition and also execution. From what I know of Natco, it has proven itself in these fronts. Still it is a company in a sector, which requires monitoring of the industry landscape, new drugs, competition, etc. and not something on which you relax for years.

Expert opinions on current valuation is most welcome.

Excellent read. RA has done some good home work here. Thanks for sharing @james_kerala.

One disconnect though on the table on page 6 titled ‘Key brands and filings to look for FY 19&20’: This table is listing Revlimed as 4.41B USD opportunity. LENALIDOMIDE (Revlimed) is one of the top 10 drugs globally. My understanding is that this has a clocking of 8.0B+ USD currently, slated to increase to 12B by 2022 “IF” Celgen is able to ward off competition. Some legal tangle on interpretation of one specific clause of patent is currently going on between Dr. Reddy and Celgen. (there was a hearing date of March as well, no update though).

Natco has a limited quantity conditional launch settlement with Celgen starting 2022, timeline can move earlier if competition join the fray. Key point to notice is that this is non-exclusive i.e. Celgen can find a similar amicable way with Dr. Reddy’s as well (read somewhere that as a possibility).

Natco Pharma is developing a plant at Beshankovichy. Beshankovichy is a part of Vitebsk Oblast. Vitebsk Oblast is the site of a Belarusian Free Economic Zone.

The benefits offered by the Free Economic Zone are certainly alluring.

They are as follows:

Tax free profits on all goods and services for five years. Post 5 years there’ll be a 50% concession.

50% discount on VAT on import substitution goods manufactured within a FEZ

No real estate taxes for owned or leased property in the Free Economic Zone.

Exemption from payments to National Agriculture Support Fund

No tax on vehicle acquisition.

No customs duty on raw materials and equipment imported from outside Belarus

Assurance of consistency in legislation governing the Free Economic Zone for 7 years.

I’m not certain that the Natco Pharma plant is at the aforementioned Free Economic Zone.

But, there’s a healthy chance it’s located at the zone thanks to the extensive benefits offered.

And, even if it’s not a part of the Free Economic Zone the company will receive a volley of incentives.

The reason being that Beshankovichy has a population much less than 50000 people.

In order to boost enterprise and generate entrepreneurship in smaller towns the Belarusian government has exempted businesses operating in such towns from paying taxes for 5 years.

Also, no transport tax and real estate tax will have to be paid.

Great data on the government benefits. Another possibility would be to get access to the CIS markets.

A bit dated reference-

accesshttp://m.eng.belta.by/economics/view/india-ready-to-invest-in-pharmaceutical-industry-of-belarus-89324-2016

Hep C market is probably declining due to high cure rates. Gilead’s revenue from Hep C has peaked and now declining. Same will probably hold true for Natco.

Indiainfoline has got the dates wrong. Off-patent in 2026/27 and not 2017…

The other error is Natco if the present conditions prevail they could launch lenalidomide in 2022 but if more competitors arrive they can bring forward the launch date

Revenue increased 7.8% YoY for FY18 and net profit increased 43%. The management had given a guidance of 700 Cr Net profit for FY18 and they have achieved 695 Cr profit !

Results are excellent.

The press release mentioned about good sales of their generic products including Glatiramer, Lanthanum, Liposomal Doxorubicin etc.

now what remains to be seen in concall tomorrow is the individual contribution to the revenue from Glatiramer (which roughly will reproduce quarter on quarter) and from Tamiflu (which is one time).

Management had given a guidance of 700 crore and they indeed have achieved that, hopefully market will like that.

Lot will also depend on further launches of new products and rate of increase in market share of Copaxone.

Disclosure: invested.

Our top 4 products in USA are Tamiflu, Copaxone, Liposomal Doxorubicin and Lanthanum Carbonate.

Copaxone is doing good in USA, shift to 40 mg was beneficial. Greater benefits from Copaxone will be seen in later quarters.

Imatinib will be launched in FY 2019 but won’t make any money on it. Too much competition is there for it. If we launch it in first wave then might make some money but if we launch it with everybody else we won’t make any money on it.

Revlimid will provide good annuity type income from March 2022.

Decline in Hepatitis C sales in domestic market has been stabilised. Currently we are doing Rs. 70 cr sales per quarter which is reasonable and will stabilise at these levels.

Q4 sales bifurcation

Formulation Export: Rs. 492 cr. (rs. 433 cr was profit share and Rs. 59 cr sales)

Formulation Domestic: Rs. 158.5 cr.

API Domestic: Rs. 8.2 cr.

API Export: Rs. 51.50 cr.

Guidance of 8-10% growth in topline and net profit for FY 2019.

Conditions in US generic market is tough, there is no visible sign of a turnaround. One can remain hopeful but we would like to plan keeping reality in mind. Therefore we will focus on ROW market from FY 2020.

For FY 2020 and 2021 focus will be on ROW markets specially India, Brazil and Canada. We expect to file 6-7 FTF in next one year in both Brazil and Canada. Hope to get approvals in Brazil by March 2019 and launch products in FY 2020. Whatever we loose from Tamiflu from 2020 will be made up from India, Brazil and Canada. Will be focusing on Oncology and Multiple Sclerosis in ROW. Brazilian market is based on government tenders.

Excluding Hepatitis C we will grow by 15-16% in domestic market.

Vizag Plant will be completed in next 2-3 months, expect to commercialise it by September 2018.

Will spend Rs. 350-400 cr on CAPEX this year.

There was a one time increase of Rs. 30 cr. in employee cost in Q4. Rs. 20 cr was given as one time bonus to employees and Rs. 10 cr. extra provision was done due to change in Provident Fund rules by government.

Other income in Q4 includes Rs. 16 cr as interest income and Rs. 4 cr. as export benefits. This will be maintained at same levels in next quarter as also we have surplus cash balance.

Tax rate for next two years will be 21%.

We don’t hedge our foreign currency exposure, everything is left open. The day we receive dollar payment we convert it into rupee.

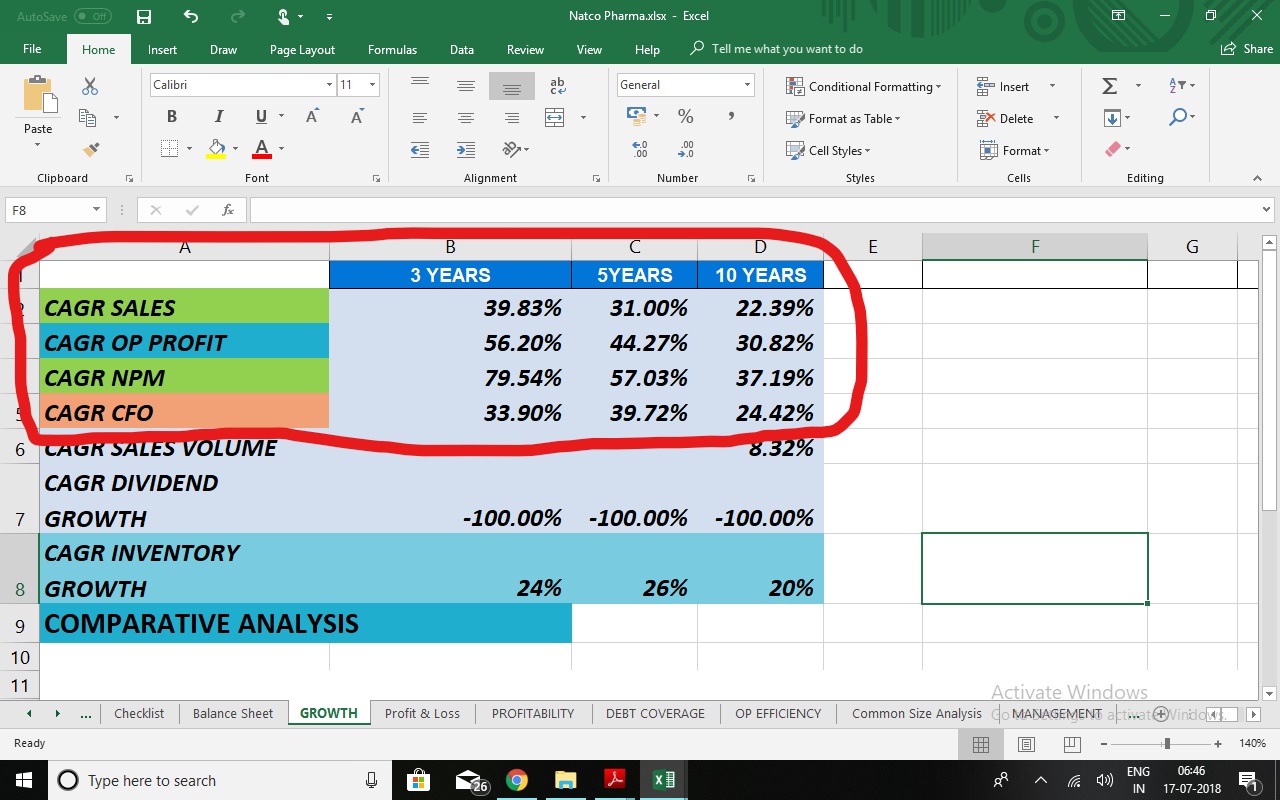

year on year, there has been a higher growth of receivables than sales…it may indicate that the company is increasing its sales by offering a longer payment duration to the distributors.On average, receivables have grown at an avg rate of 36% while sales have grown at an avg rate of 25%…

This particular factor might be a tool for gaining larger share in market by allowing such incentives to distributors but it derides the Company of cash.

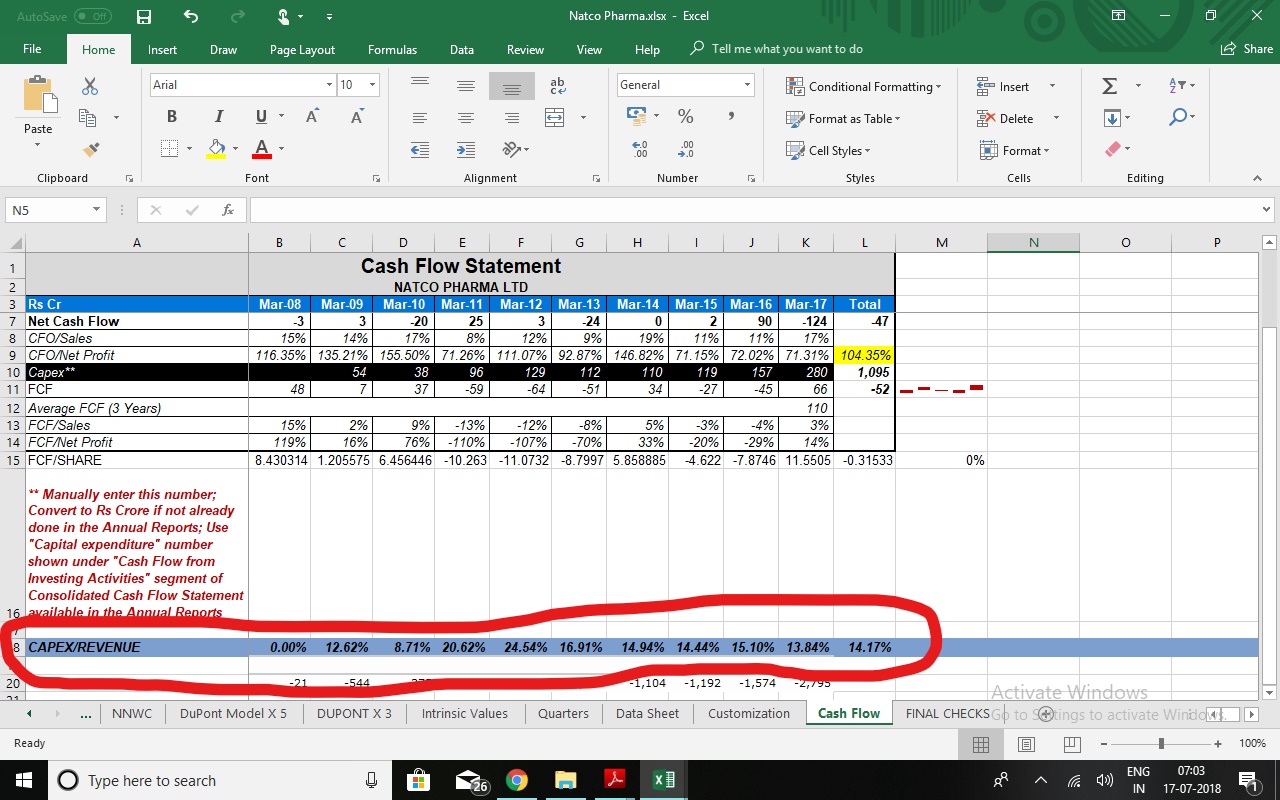

Since natco is involved in production of complex formulations, it incurs a heavy capex

…the heavy capex might be because of expansion …so the net free cash flow since last 10 years has been negative…but the they have generated less than avg cash flows from operations…this thing needs to be understood…the annual reports also seem to be shallow…

While the oncology and hepatitis theme is great, the business model seems to be just avg…this may lead to a below avg valuation as compared to the peers…so Biocon which is also incurring the heavy capex due to R&D and expansion, is generating better cash flows than Natco and avlb at a higher valuation…Natco is using QIPs for generating cash and avoiding the debt route but it also means dilution of equity…as such promoter’s holding is low at 48%…

This information may be helpful while deciding an entry price for Natco…i feel that it should be bought at 1 year forward looking valuation of less than 20…

Ill request seniors for correction in my assumptions…

Also Biocon is quoting at higher valuation in anticipation of the contribution of biosimilars business. This vertical is the expected new growth driver for pharma companies.