Thank you for listing out the high points outlined in the concall. However, I also find some interesting takes from the chairperson’s outlook on various things such as:-

When asked about exploring CDMO segment then he firmly emphasized the expertise of the company is related to complex generics and they are more inclined to be the best in that segment only.

Furthermore , he justified the acquisitions in Africa rather than India for having the expensive valuations in the latter.

He did not give the false hopes of having the great years ahead with multiple filings to be approved with surety.

So, yes it is really difficult to be in the spot as an investor to see the things unfolding beyond FY’27 but there could be a major takeaways from the journey as investor as well.

The CDSCO SEC meeting on endocrinology and metabolism took place on 9th december and the minutes revealed no mention of Natco Pharma Phase III clinical trials.. instead Sun Pharma,Zydus and Alkem got the recommendation for semaglutide manufacturing.. natco management inefficiency was revealed once more as they received consent to conduct phase 3 trials a good 1 and a half to 3 months prior to those who got approval, yet they could not submit their trial report to the committee before the others.. the only saving grace is that there was one more meeting on the 17th december scheduled and one hopes that the Natco management has put up their case in front of the committee.. better late than never I guess, I was a bit disappointed especially as they have an F2F in US for the same and have been tomtomming the semaglutide domestic opportunity to rev up its stagnant domestic formulations performance for years now..

That being said there are some interesting insights to glean from their consolidated H1 numbers when compared to the previous ones:

the current liability provisioning as at 30th sep 2025 is higher by 353 crores compared to 31st March 2025. I suspect that this means that they have booked some expense in advance, most likely in R&D so that the higher profit period of 6 months abosrbs this and they manage to show profits in the remaining two quarters of H2, probably learning from the disastrous Q3 results of last year which lead to a lower circuit!

And correspondingly in the other expenses we see an absolute increase of 297 crores in other expenses and 75 crores in employee benefits.. these 2 abnormal jumps have been addressed by the management in their note accompanying the quarterly financials but it is also true that if one adds back the increase in employee expense and other expense increase that must have found its way to provisions the resulting reduction in profit margins and absolute profits would be much narrower H1 to H1 comparision..

These were a couple of nerdy accounting points that I asked the promoter in the concall afterwards but he ofcourse brushed the point aside with his usual swagger..

Here is hoping that the last minutes to be made public shortly by the CDSCO SEC on endcrinology and metabloism brings some much needed cheer before the end of the calendar year for all of us holding Natco Pharma through this rut.

Merry Christmas and a Happy New Year 2026.. my wish is ofcourse that Natco plays a leading role in making India a less obese nation in the coming year :)

Finally!! The SEC of CDSCO on Endcrinology and Metabolism in its meeting dated 6th January 2026 has recommended Natco Pharma’s application to manufacture and marketing of prefilled multidose pens of generic semaglutide for type 2 diabetes mellitus

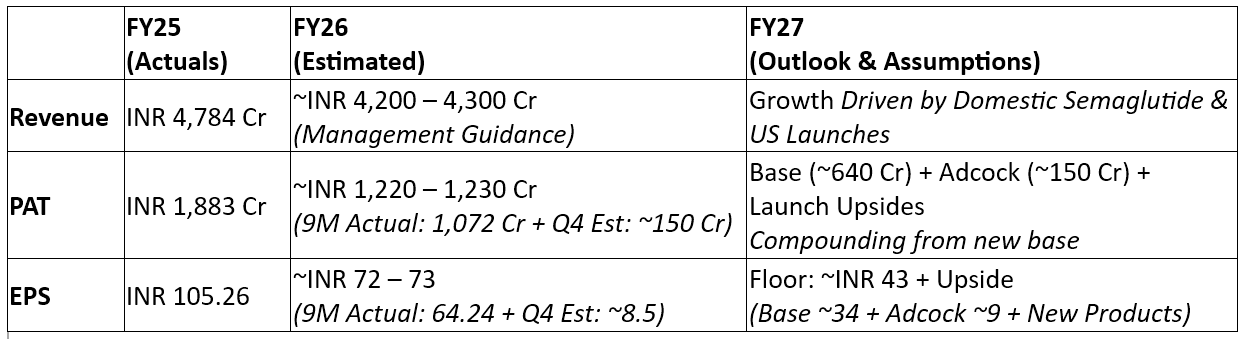

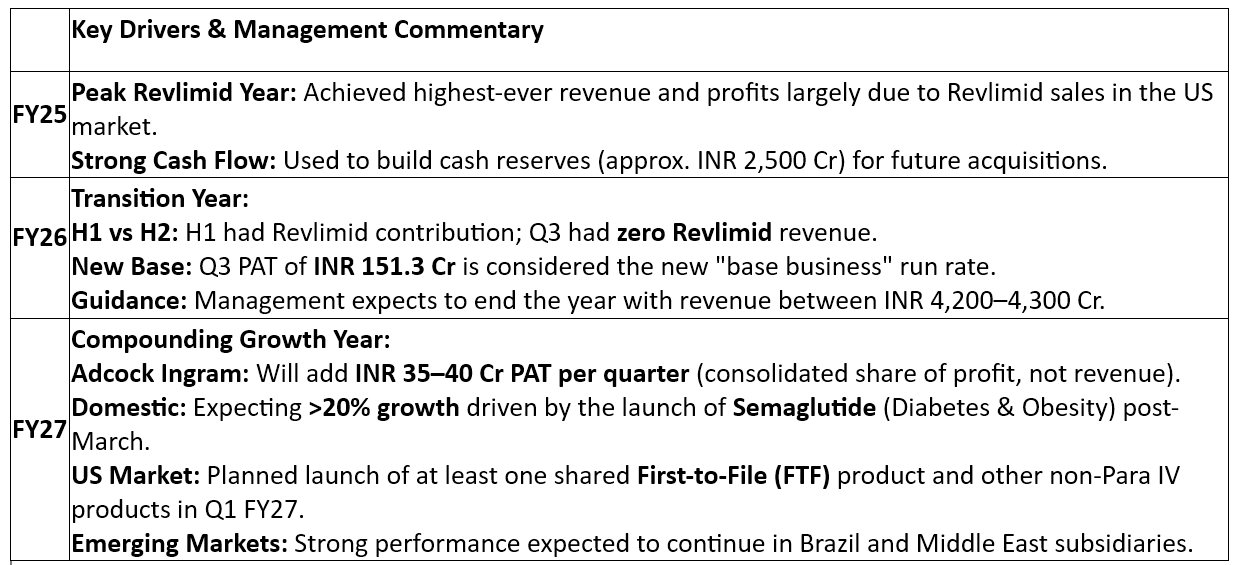

From next quarter onwards 35 crs will get added to PAT from Adcock Ingram acquisition

Management expects the domestic business to grow by more than 20%, primarily driven by the launch of Semaglutide

Emerging market profits, combined with Adcock Ingram, will drive the company’s growth moving forward. Specifically, Brazil has strong approvals and launches expected in the next 12 months.

Management is actively engaging in “trying to do another very large transaction” and is actively pursuing two to three target, expected to close in CY 2026

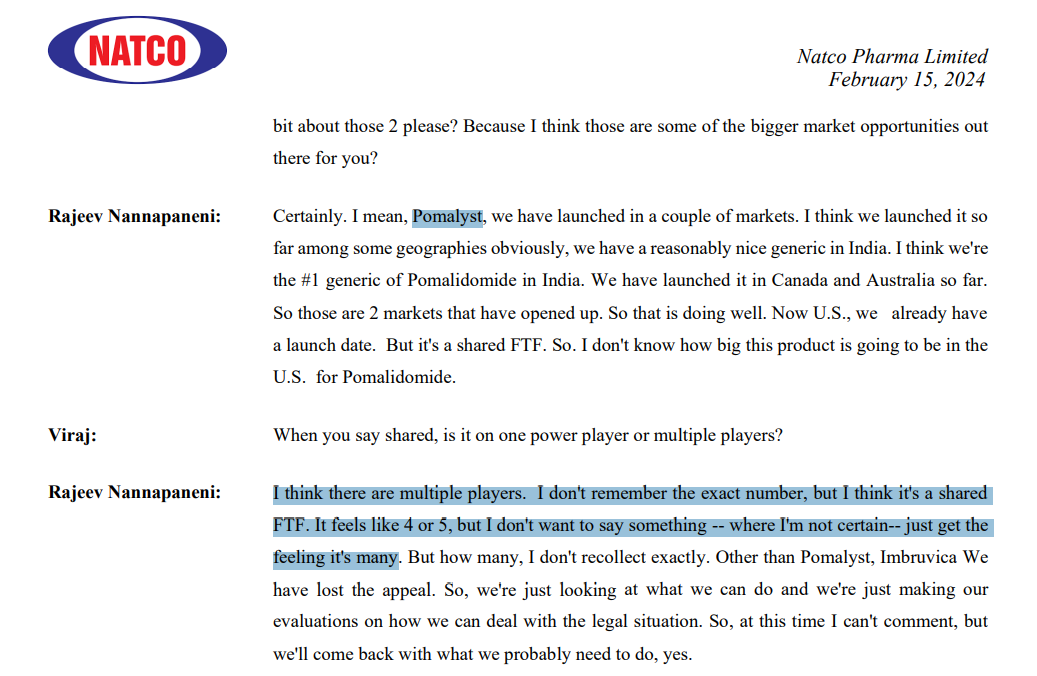

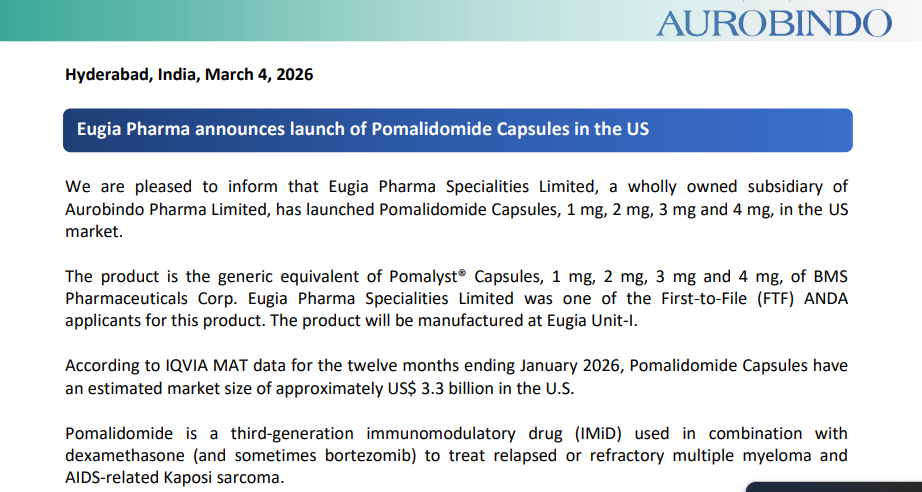

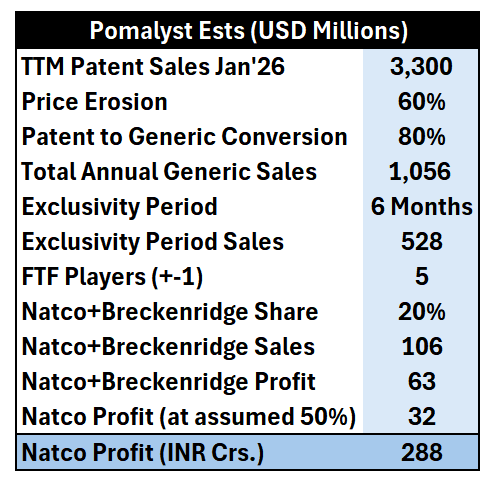

‘‘Pomalidomide Capsules, 1mg, 2mg, 3mg and 4mg, had estimated sales of USD 3.2 billion in the U.S. for 12 months ending Sep’25 as per industry sales data. NATCO believes based on information made available by the U.S. Food and Drug Administration (FDA) that it has 180 days of shared exclusivity.’’ - As per Statement by Natco Pharma.

Seems a good opportunity for the next 2 Qs. Also, Semaglutide domestic launch expected in 3rd week of March.

Natco launching 180 day exclusive drug pomalyst sales value 3.2 billion dollars, I think this is the surprise natco has given and hence it’s up 20 percent in last one month when overall market is falling.

Lets see which ways it goes, but its going to contribute good in FY27 it seems and I feel they will grow the revenue and not decline. Let see Q4 concall for more clarity.

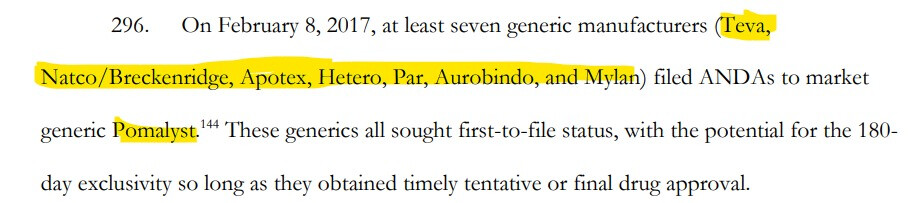

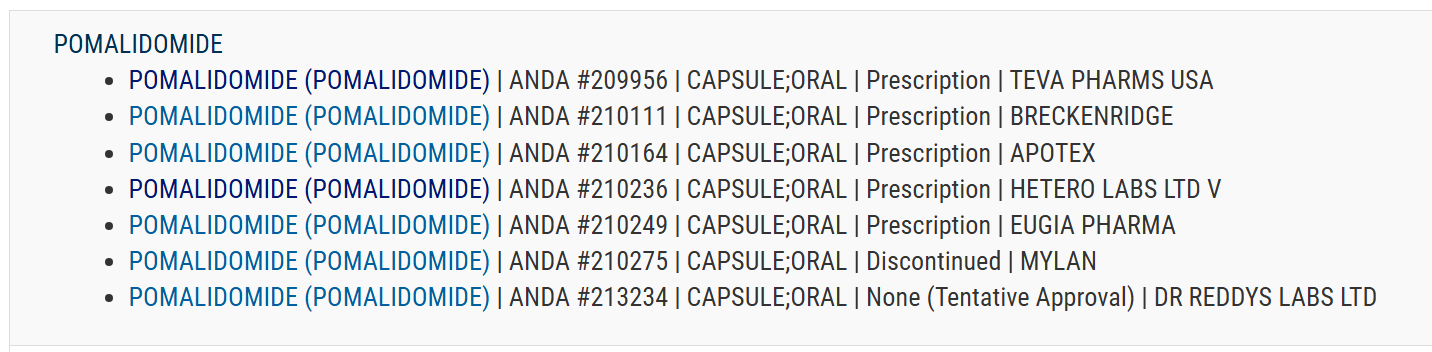

The Pomalyst (Pomalidomide) FTF was filled by multiple players and not just Natco due to which the market exclusivity period (180 Days) will be shared by the 4-5 Players and thus Natco would not be able to capture all the generic sales and also the price erosion could be higher due to undercutting by other players.

These are very rough estimates basis the above data points, however this will only be a one time event and profits won’t be sustainable.

On another tangent, do read the Cigna vs Celgene case (https://business.cch.com/ald/TheCignaGroupvCelgeneCorporationComplaint.pdf) as it refers to the arrangements made between pharma companies for their challenged patented drugs (Revlimid and Pomalyst) which delayed the launch of Pomalyst by 5 years despite the challengers (Natco, Eugia etc.) getting the FDA’s go-ahead.

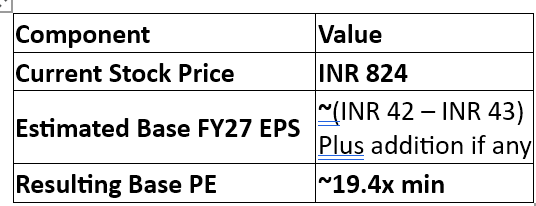

What are we buying at current price ( Market Capital: 15488 Cr ):

- We as retail investors often forget what are we buying at cost per share, as pin pointing the business worth is difficult to an exact number, because what a business is worth is always a moving target, a spectrum or range.

What you buy for ~₹15,488 Cr ( I am assuming you are buying the whole business at current market capital )

(i) A base business that, in its worst printable year, still throws off ₹500 cr+ Net Profit (MEDIAN) and ~₹1,700 cr operating cash, debt-free, ~16% ROE in the trough.

(ii) ~₹2,400 cr net cash (~₹135/share) being redeployed, not hoarded — a 35.75% stake in Adcock Ingram (a ~₹4,800 cr-revenue South African platform, already contributing associate profit and a plausible path to control/consolidation), an eGenesis/CRISPR position as a long-dated biologics hedge, in-house NCEs.

(iii) The next windows: generic semaglutide is already launched in India (multi-dose vials ~₹1,290/month vs ₹10,000+ branded, plus pens and third-party co-marketing — cash now), a US first-to-file shot at a >$30bn franchise around 2030, and Risdiplam (SMA) pending an Indian appellate nod expected shortly. The market pays roughly ZERO for (iii). : )

What is the Engine?

Find an expensive patented blockbuster, attack the patent (Para IV in the US, compulsory licensing/challenges in India), be first-to-file, win ~180 days of exclusivity, harvest, repeat. The visible business is pills; the real asset is forty years of litigation-and-regulatory craft that lets NATCO read a patent cliff before the market prices it. Conversion is the point — Nexavar (the landmark 2012 Indian compulsory licence), Hep-C sofosbuvir, then gRevlimid. Each was dismissed in advance as a long shot; each landed as we can see the stock price volatility in last decade at each product cycle.

The single driver that matters ( according to me ):

Do you underwrite the recurring engine, or only the current cycle? Everything else — semaglutide-US timing, Adcock, the precise FY27 print — is second-order. Believe only the base business and you earn a low-teens IRR off cash return and modest growth and don’t lose money (assumption). If the engine produces one more window in the next four years — and a fifteen-year cadence says it will — the upside is a multiple of that. The asymmetry is being given away precisely because the asset is between hits, which is the only time a business like this is ever cheap.

Key risks ( What can hurt NATCO in next 10 years ):

Patent Thickets { Tough overlapping patents to crack created by big companies to avoid getting their margins eroded by companies like NATCO, TEVA etc }

Biologics { Natco’s entire product line depends on small molecules which are easy to synthesise, future holds gene therapies which is extremely hard to produce, talk to a pharmacist about this : ) }

Overpriced Acquisitions

Note:

This is completely my view, I do not care about where the stock price for next 10 years , I only care about the entry price and business fundamentals if the core structure is intact.

” If my entry price is at top of the product life cycle ( the one heroic drug increasing topline numbers ), why in the world would I get the stock at cheap valuations ?? “

Happy Investing !!! Not investing advice of any kind, do your own research.