Current scope of health insurance is just hospital stay, over time scope may expand to cover all expenses, like US based HMOs. Also a large population finds the current cost of insurance prohibitive, hence they might also be the target market. disc: have a tracking position

3 Likes

6 Likes

Very Interesting!!

Taking a complete different route, expectations of breaking even within 5 years. Pretty impressive.

Let’s see how things pan out. If they’re able to scale it, I believe we’ll see major shift in Insurance industry. But things are very far from today.

Disc: Recently exited, not SEBI registered.

4 Likes

Anyone with the list of hospital & number of beds planned between FY24-28?

1 Like

The target audience for NH insurance foray will not be urban upper middle class people, it will be lower middle class people who are currently not part of any insurance or only dependent on govt schemes. I understand that there is income cap for one to be eligible for Aditi policy. They won’t offer it to anyone who is above the defined income limit. Plus it covers only general ward treatments, if anyone is opting for semi private or private ward then pro rata difference will be borne by patient. It is kind go a private sector Ayushman Scheme. This won’t compete with other private insurers.

9 Likes

I think their valuation now reasonable .like 6 yr back when apollo hospital was stuck for 2 yr.their earning will be good in fy26. So seen …

1 Like

2 Likes

Q1 FY25 Concall Highlights

-

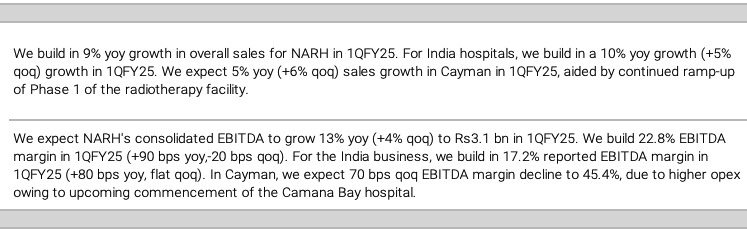

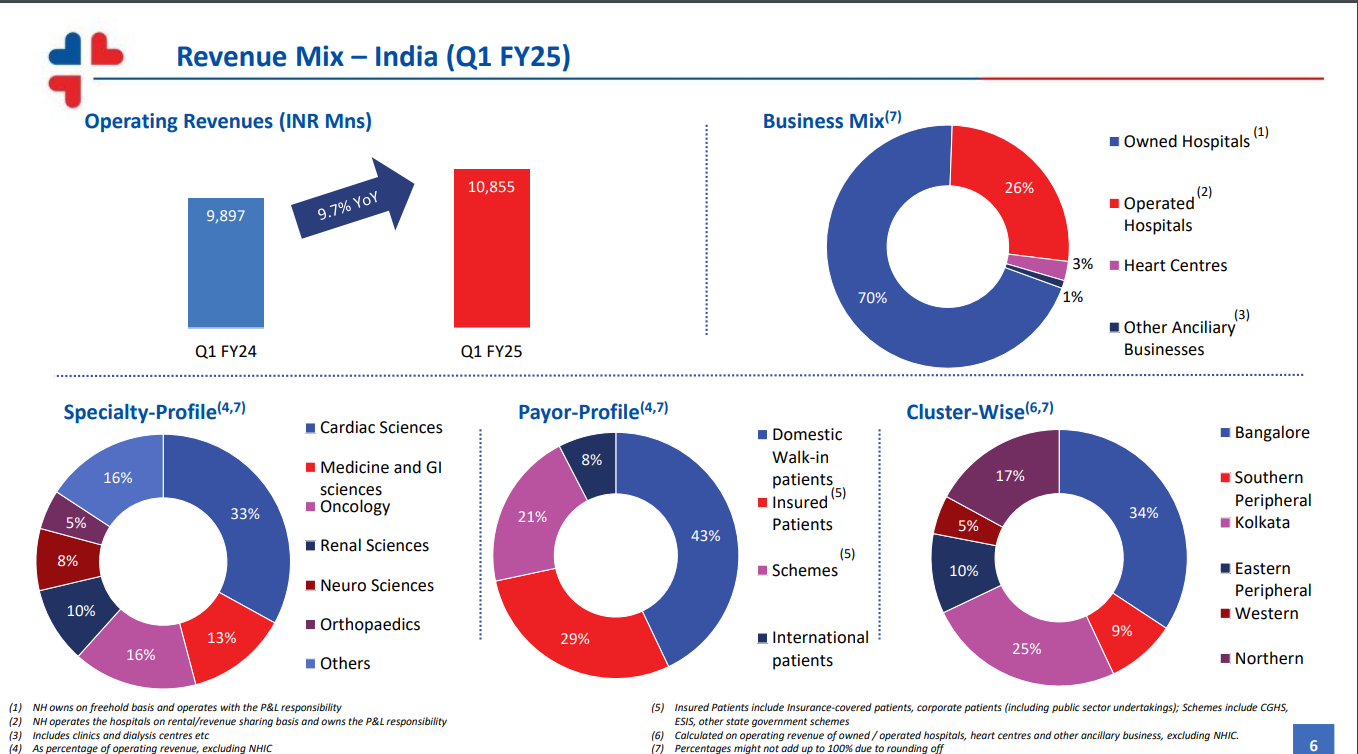

Consolidated operating revenues of INR 13,410 mn in Q1 FY25, an increase of 8.7% YoY and 4.8% QoQ.

-

Consolidated EBITDA of INR 3,274 mn in Q1 FY25 at margin of 24.4%, and consolidated PAT of INR 2,015 mn for Q1 FY25 at a margin of 15.0%.

-

Consolidated Total Borrowings less Cash & Bank Balance and Investments of INR 1,549 mn as on 30th June 2024**, i.e. net debt to equity ratio of 0.05** (Out of which, debt worth US$ 75.0 mn is foreign currency denominated).

-

Revenue from NHIC and NHIL stood at INR 80 mn and EBITDA stood at -INR 120.8 mn for Q1 FY25.

-

Kolkata Greenfield capex- The estimated capex would be INR 1000 cr and in the first phase, 350 beds will be built

-

Bangalore greenfield capex- Estimated capex to be INR 500 cr, bed capacity yet to be finalized

-

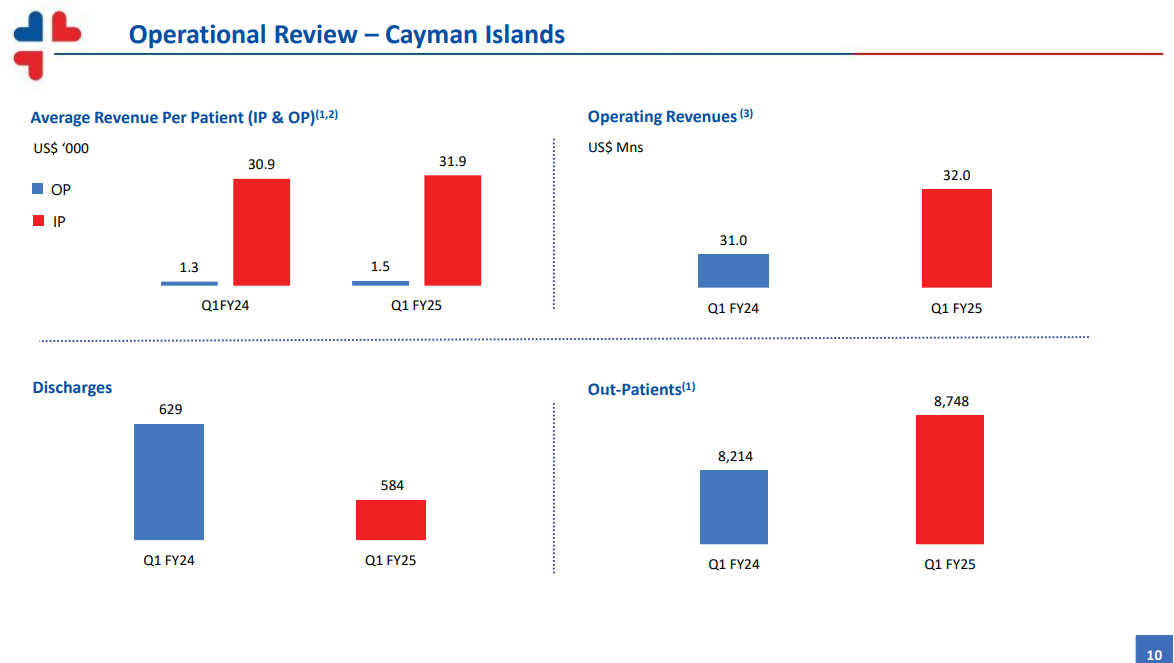

Cayman facility- NH will see margin dilution for some time due to the upcoming Cayman facility capex due to high fixed costs. The new facility will fill the gaps on NH’s existing offerings in Cayman. The existing Cayman facility is also seeing a saturation point, so the management feels it as a good time to go for a new facility

-

The insurance facility is currently limited to Narayana hospitals across India. In future, the management sees that the insurance facility will not be provided all the major hospitals like we see in normal insurances today and will operate in a narrow network.

-

Debtor days- Comparing YoY, we are at similar levels. But comparing QoQ, we have deteriorated by about 8-10 days as in Q4 most of the collections happen. The management expects the debtor days to improve in the next quarter.

-

Company is focusing more on domestic patients and less on international patients. Management is OK if the international patient’s revenue goes down to 0% in next 5 years. As per the mgmt., they never differentiated on the prices for international patients and domestic patients (Superb management quality according to me, I know investors might not like it)

-

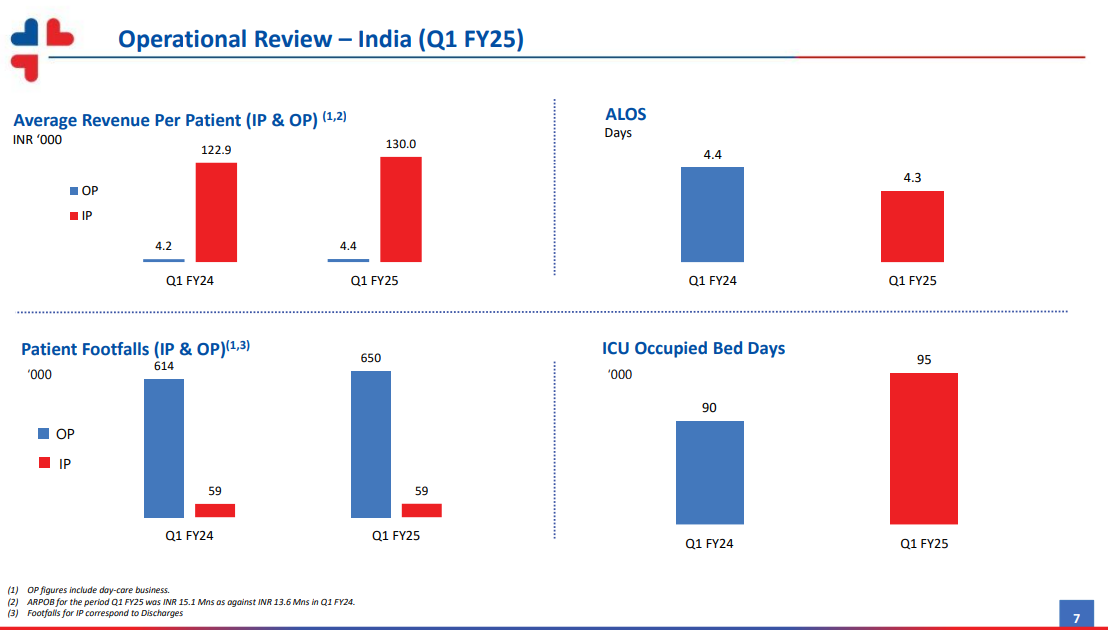

Occupancy levels in Q1 was around 60%

24 Likes

Can anyone help to understand why pe is alltime

Low.anything I miss please

I believe there are multiple factors for this:

The Hospital sector lost its momentum after the News of Supreme court order for standardization of rates…

However, NH is entering into new vertical like Health insurance and its investing heavily into new hospitals. The new hospitals have a gestation period higher, even though there are doing capex now, that will take more than 2-3 years to reflect in profit and loss statements. These are the details as of now. I believe these are some of the reasons for underperformance.

12 Likes

I think the main factor is capex spend on new greenfield hospitals which will take time for utilisation. In the last ~2 years, nost of the expansion was brownfield so it added to bottom-line quickly and the stock went up accordingly. My view is we might see time correction at this levels in the short term.

9 Likes

Lots of green filed capex. Cayman will also be a drag in margins for near term. Market is factoring that ahead in time.

4 Likes

So,is it good time for add

very interesting discussion between father and son duo…explains the philosophy of this business very beautifully

13 Likes

I have tried to summarize key points based on what I have seen in the hospital sector. These are broad points which includes some softer aspect to give insights:

1.First established multispecialty hospital in a city will have significant moat in attracting patients. Main reason being the trust of that particular hospital gained over decades of service and is difficult for the new competitor to replace it. Many patients and relatives keep coming to the particular hospital because someone known to them was treated and recovered in that hospital even if it’s more than a decade back. This happens despite the same specialty being available in some other hospital near to them which was not existent earlier. Even for the same level of service and specialty doctor the existing one is preferred even at slightly higher cost. The feeling that someone known to them recovered in a particular hospital and trust has an ever lasting impact on people and probably the greatest moat.

-

Longer the hospital is functioning, the better will be its revenue and margins as they can keep on expanding their capabilities like , oncology, higher radiology services, specific surgical capabilties like organ transplants, robotic surgeries etc. As the hospital expands these superspeciality services, the revenue per patients and margins improve with limited additional investment.

-

Mix of patients in terms of paying: Best is to have a private insurance patients pool as the money is guaranteed on time and there are standard payment terms with the insured. Also standard hospital rates are defined and the patient knows what will be their share in paying. Hospital charges are highest for cash patients but the problem is at least 5% of cash patients do not pay the full amount and the hospital has to let go a reasonable amount for such cases under various circumstances like death/influential calls from local leaders/politicians.

-

Mix of surgical vs medical patients. In general higher the number of surgical mix better the profitability of hospitals. As cost of operation and associated charges like OT charges, radiology imaging before surgery etc… are much higher per bed compared to patients undergoing only medical treatment. If the occupancy of such a hospital improves the operating leverage is significantly higher as fixed cost of operation theater/pre and post op care is better absorbed.

-

Typically hospitals agree for most of the Govt schemes like ECHS,CGHS etc in the beginning as it helps them to cover certain basic costs. It also helps to gain good will among patients over the years as the family members/friends of such scheme patients will start availing the particular hospital services and increasing occupancy. Govt schemes come with their own risk of increasing receivables, significantly less consultation fee/operation fee impacting margins. As occupancy of a particular hospital reaches around 70%, typically hospitals will start to withdraw from Govt schemes. This helps in freeing up sufficient beds for other patients and increases average revenue per patient. The consultation fee and other charges for a private patient is 10-20 times higher compared to Govt schemes. This may lead to some drop in occupancy for particular hospitals in the short term but the ARPOB are much much higher for a pvt patient compared to Govt scheme. It also helps in reducing receivables, reduction in manpower employed in Govt insurance desk, lesser requirement of healthcare workers as overall no of patients comes down but with much better profitability.

-

Hospital with optimum ALOS. In general the maximum billing for any patient happens during the first few days of hospital admission. Initial evaluation including lab tests, radiology investigations and critical therapeutic intervention happens during the first 1-4 days. After that it’s generally the ongoing maintenance therapy of the initial plan and revenue per patient per day drops after 3-4 days. It’s better to look for hospitals with ALOS of 3-4 days. It also indicates how efficient the hospital system is in terms of quick admission, evaluation, treatment and discharge process and dealing with insurance companies for quick discharge. Reducing ALOS less than 3 days in multispecialty hospitals is practically impossible as the number of sicker patients, superspeciality, and complex surgical treatment increases.

-

Presence of long serving doctors who can get more patients to hospitals on their own. Impact of it is more in particular surgeons/gynecologists. Obviously patients do prefer to go under knife with the same surgeon who has done it successfully in the past for them or relatives.

One of the key things to look at is retention of consultants by hospitals. If the same consultant remains to work with the same hospital for a longer time of more than 5/10yrs it brings a lot of repeat patients. The time and efforts required spent in evaluating known patients with readily available past history is lesser than a new case. Probably this is one of the key but ignored question to ask in company concalls. -

Presence of DrNB educational program in hospital.It makes the particular medical fraternity of the hospital to be updated about ongoing changes in the medical field and improve the care of patients. It also gives the hospital administration adequate junior level doctors to work during their training period. Generally if some of the junior doctors are good during their training period will be absorbed into the unit as they complete the degree.

-

International patient mix; Higher mix of international patients bring higher revenue and better profitability. Generally international patients come to India for superspeciality care like Oncosurgery, Organ transplantation etc… The cost of the same is higher by ~25% compared to domestic patients helping in better revenue and margins for hospitals.

Disc: currently not invested in hospital stocks.

38 Likes

Narayan Hrudayalay.pdf (155.2 KB)

Disc: Invested

7 Likes

8 Likes

Impact can now be seen in the numbers, reduction in margins due to hiring for new capex and increased depreciation giving double blow to bottomline.

2 Likes