Agree and support your reasoning. Very attractive at these levels and it would definitely bounce back. Reasonable valuation vs peers, almost 30% discount on EV/EBIDA, in fact this company should be trading at par if not premium vs peers.

3 Likes

These are uncertain times. In my view, it is bit early to take any call. should wait until dust settles and then take position.

1 Like

There’s a gap-up from the range 1091-1132.

Technically the stock may fall till this range before consolidating.

I’ve another question, why is market discounting it so much? There’s the revenue from the island which doesn’t come under Indian jurisdiction (correct me if I’m wrong). Is the market thinking that the island business is also not going to be good? Or perhaps there will be margin pressure…

Very hard to understand.

Disclaimer: Bought in the last 30 days. Not a buy or sell recommendation.

My guess is the growth rate is just 6% this quarter compared to mid teen growth reported by all peers. Market maybe valuing it accordingly.

2 Likes

What do you mean by these levels, pls elaborate

historically hospitals have traded at 1-3 cr per bed . all of hospital stock’s valuation have shot up. at cmp definitely not mouth watering price. Will be very happy if i can get NH at valuation of 2019.

4 Likes

Well… have you reflected how the sector has changed since then? Healthcare in overall got a push because of COVID. Unorganised to organised shift has been seen even in healthcare. Incidence of respiratory diseases and cardio diseases have increased and India in general is ageing incrementally.

So obviously, hospitals will not trade at 2019 valuations when their TAM itself has increased?

6 Likes

Also, there was no proof of concept for Cayman Island hospital. It was sucking money from the system. Especially debt levels.

There was a gap-up in the chart, the stock jumped above the resistance level and started trading above it. Generally, it’s observed that these gaps may get filled aka the stock price comes back and fills the range (not always). That’s why I mentioned that the stock may fall down to this level. Also, previously as well it acted as the resistance, so now may become the first strong support.

Note: I may be wrong. Someone please correct me in case, will help me improve my understanding.

5 Likes

i said valuation and not value. anyways .was just suggesting what would be ‘very attractive valuation’

1 Like

Reallly amazed to know the infirmation u gave Dr…its not morally good to charge so much … now Hon ble Apex court asked Govt to Fix rates and all hospital stocks coming down.

2 Likes

I don’t understand this whole issue here!

Why doesn’t government spend in public hospitals? Are they just there to get all the tax money and not provide any infra… what about schools - private schools charge a bomb due to lack of public schools, then why not regulate school fees? Simply put, government should spend more money in social spending, until then they can’t regulate prices, it should be market driven or DD/SS driven.

Secondly, why does India have maximum share from gulf in medical tourism. It’s due to quality of our medical science, infra at competitive price. I don’t think overall hospital charges are higher in India vs other countries and therefore we attract highest international medical tourism.

Coming specific to NH, no doubt they are the most affordable in providing heart surgeries in this country. No agent commission, pure focus on affordable cost model to provide most needed critical heart procedures.

Now, SC wants to even get this basic right from our people, rather than slapping Government for lack of social infra. What’s really going on?

17 Likes

Yeah we all got your point. But P/E is still in the same range. What are you referring to as valuation here?

2 Likes

Keeping an eye on situation very closely. I am wondering what will happen after 6 weeks, when supreme court will again asked the government ? Imo there will be negativity till 15 of April. Looking charts I, think it can take support near 1000 or 1050.

Disclaimer: Not holding , just studying will take position if it falls near to 1000.

1 Like

I think by Mid March, election dates will be announced and election code will come into place and it will be in status quo till new government is formed in May 2024.

Even after new government is formed it will take its own time as Health is state subject and central government will have to form consensus by discussing with all states.

In My opinion Q4,Q1 results won’t be impacted for sure.

3 Likes

Why look at historical per bed metric to determine valuation? It’s like trying to determine hero motor’s valuation by looking at historical average price of their bikes.

Average revenue per bed has been trending up for all hospitals which could be due to just inflation, operating leverage or product mix change or all of them. EBITDA for leading hospitals including NH has also been steadily increasing with only exception of Apollo. So there is no reason to believe why earning per bed of hospitals will remain at historical levels.

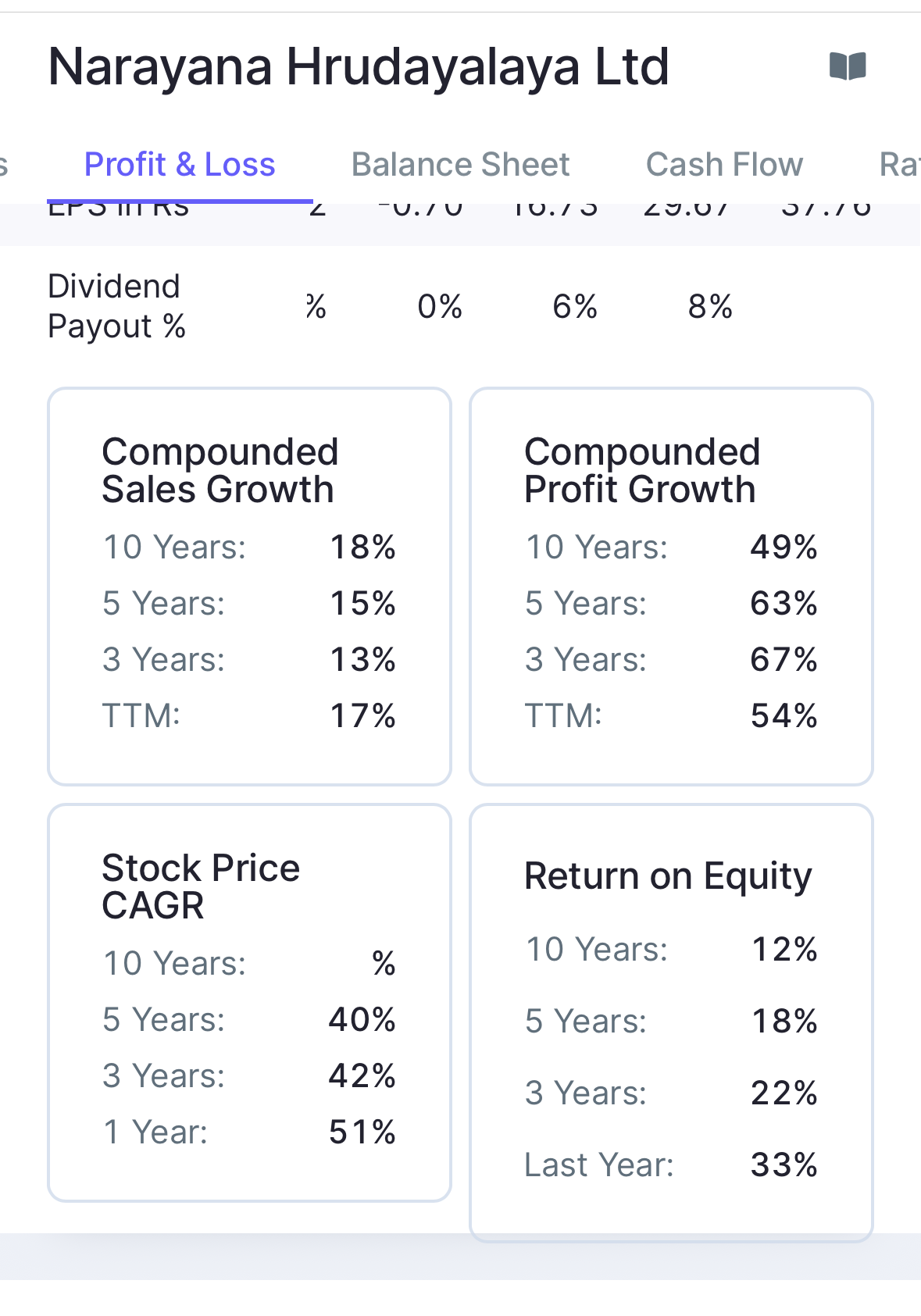

Coming to NH, it trades at some 30 p/e against a sector average of 70 with leading hospitals such as Apolo, Medanta, Max all trading at 70 p/e. Interestingly NH stock prices have trailed earning growth which means stock is heavily derated (guess something to do with Cayman overhang).

10 Likes

Looks like Marcelleus made an entry.

6 Likes

Everything true… Only, EV/EBITDA multiple is generally used as a metric for hospitals instead of PE as it shows a better picture in this case. EV/EBITDA multiple of NH is also the lowest among peers though.

5 Likes