I think estimating the impact of the COVID situation on revenues and profitability would be too difficult since non-critical patients will not be too enthused to visit hospitals for 3-6 months until COVID subsides. I would prefer to wait and see for 2 quarters before initiating a position in this stock. Also feel that the market in general is underestimating the impact of COVID and there could be a serious correction in stock prices post Q4 results and Q1 results in 2021.

HDFC Security initiates coverage

3 Likes

NH Q1-22 Highlights:

Revenue Rs 8,598 mn for Q1 FY22 vs Rs 3,935 mn in Q1’21- Up 118.5%

EBITDA* Rs 1,404 mn, margin of 16.3% vs loss of Rs 863 mn in Q1 FY21

PAT* Rs 762 mn, margin of 8.9% vs loss of Rs 1,198 mn in Q1 FY 21

India operations were hit by Wave 2, outpatient footfalls reduced to 330 K from 460 K in Q4’21, hopefully this will bounce back this quarter.

Doctors cost as % of revenues declined sharply from 71 % to 44 %, need to understand how this was achieved, and longer term consequences. Were doctors fees reduced, will they come back to earlier levels, or is this reduction sustainable ? Or will doctors leave for other hospitals ?

Caymans continues to do well, with revenue doubling to $23 Mn from 11 Mn Q1 last year, and $18 Mn in Q4 and both inpatients and outpatients doubling, ARPU remained constant. Their expansion plans here are on track. Need to see what Aster does with the planned Caymans expansion.

Technology adoption for remote consultations is still not great, despite piloting this way back in 2015-16 timeframe as a Cisco CSR project. Apollo has made much better progress on remote consultations, possibly also because they do more non-invasive general medicine. But I would like to see NH step up their efforts on this side. They have made more progress on tech initiatives to streamline hospital operations and workflows, but not much on the patient facing side.

[Investor PPT]

I think This is an “Intelligent fanatic” owner operator driven high quality business in a segment with high demand. Key concern is regulatory meddling. The Investor call is on 9th, and AGM on 27th Aug.

Disc: Invested since last 4 years, holding and adding at reasonable valuations.

Watching Aster, but not yet invested.

5 Likes

I attended the Investor call, highlights I captured:

1 Manpower costs are currently 44-45 %, this is on the higher side we expect it to go down, maybe closer to 40 %, though 35 % may be too aggressive.

2 Telemedicine- back end is done, most work was for streamlining the hospital workflows. In the next year, will see a lot more focus on the front end and generating more revenues from Digital channel. Focus first on India, but could leverage the same for Caribbean as well. Already a lot more patient interest is coming from Central India.

3 Renovation of older hospitals- Some of the older units need revamping of interiors, plan to do this in the coming few quarters. Also may reduce the amount of space used by the Open General wards to create more private rooms, consultation rooms for OPD etc. This will increase maintenance capex slightly. May use the new Govt scheme for raising money for this via debt.

4 Cayman- Local patients are still visiting NH despite easing of travel restrictions, this was attributed to patients being happy with the care provided. Swank clinics with upmarket feel and Apple PC’s etc. are being added in Caymans. Also took up a management contract for an existing hospital in St Lucia. Plans to have NH doctors travel in nearby islands to increase the reach as well.

6 Likes

Strong Numbers with Ebitda Margins sustaining as guided by the management in the previous concall.

Some positives:-

-

Exited O&M contract in Bangladesh which was leading to operating losses (4 crore).

-

EBITDAR margins in Bangalore crossing 30%, which is inline with what other mature hospitals like Kims do in Secunderabad (32%+)

-

Best part:- Ever since NH announced its additional greenfield in Cayman Islands. Aster has shelved the plan for the time being as it will lead to overcapacity if Aster also sets up. NH is adding oncology blocks in Caymans.

-

Delhi NCR hospital is not making EBITDAR losses anymore. This should scale up in the coming years as ARPOB is the highest in Delhi NCR and its close to the airport.

-

These margins are at a time when interntational patients haven’t fully comeback to pre covid level .

Levers for ARPOB and Margin improvement:-

-Payor mix changing.

-More complex surgeries being undertaken.

-Oncology blocks being added.

-New hospitals, turning EBITDAR Margin positive.

-International patients coming back to the usual.

Disc: invested and transactions in last 30 days. Not sebi registered.

31 Likes

-ARPOB in Cayman has been maintained and Revenue has grown 24%. Margin has come down because margins are dependent on types of procedures we undertake. Sometimes they have higher end procedures, types of procedure end up deciding procedures. Margins were affected due to this.

-Sustainability of Margins in Caymans:- coming up with an oncology facility. Some amount of investments they will make in the near time for creating infra and hiring consultants. Current margin will soften for next few quarters, until full facility comes up and scale up happens.

-They haven’t opted for 25% tax rate, as there are some brought forward losses. Once we cross it, we will opt for 25% tax rate.

-In the middle of pandemic, they have taken a call not to create a pricing differential between domestic and international patients. Once international patients do come back, will lead to higher yielding patients. Won’t change the numbers materially in a short period of time.

-EBITDA was 10.2 million in Cayman. ALOS has been high due the nature of cases that came in.

-There was a one off in Q2 ebitda(refund of deposits from unit in Whitefield). Excluding that, inspite of a seasonal quarter. They Have improved Ebitda QoQ.

-Delhi Cluster:- Impacted by Seasonality.

-Construction period at Cayman in two periods:- First oncology block (1 year), and 1 year after that surgery room, cap labs etc. Temporary margin % dilution. Topline will increase due to this once utilization increases.

-As international increases, it will lead to increase in overall average ARPOB.

-Long term growth trajectory: on Capex plans

1.Long term outlook is positive.

2.Capex in Cayman. Opportunities in exploring adjacent countries on a small scale.

3.In India, opportunity will be greenfield in the same city, brownfield and Acquisition.

4.Most obvious:- Brownfield at little cost, after this greenfield in the same city like Bangalore or Kolkata, Inorganic are few and far in between. Will only do inorganic when valuation is favourable. Inorganic has to add something different to our unit. We will be trimming some low yield beds and add higher yielding beds.

5.Opportunities in Caribbean Islands:- eg govt hospital O&M of St Lucia. A lot of challenges in Bangladesh, wasn’t really working out. Decided not to renew our contract.

6.Setting up oncology centres in Ahmedabad and Jaipur. Adding bed capacity in Howrah (bengal). Ahmebdad, have bought some nearby units in Kolkata and small pieces of land for Radiation oncology. Opportunity to get a landlord, to build an OPD plaza next door to main health city in Bangalore, on rental basis. Dharamshila, in discussions with the partner to add few beds in bone marrow and ICU. In Gurugram, if permission is given.Can add two more floors here. In Mysore, will be adding 30 beds. In Shimoga (Karnataka). Will be adding radiation oncology.

7.In nearly every hospital, will do some efficiency improvement, oncology and minor capacity additions.

-53% Occupancy in India and 52% in Cayman islands on the revenue generating beds.

-Cardiac has increased in speciality profile:- Typically yes the margins are higher. Higher profitability in this particular mortality.

-Average revenue per patient has decreased due to covid impact. In Q1 we had a lot of covid patients.

-Dharamshila they have started generating positive Ebitda. In Gurgaon, due to seasonality Ebitda decline. In 6-9 months, they will turn around Gurgaon into a positive Ebitda market. Next year, they expect full and proper break even. It is still relatively new, anything less than 10 years is relatively new.

-Sequential decline in ARPOBs because of general seasonality impact.

-If they don’t even invest in infrastructure, just through efficiencies we can manage volumes for next 2-3 years.

Disc: Invested. Not SEBI registered.

27 Likes

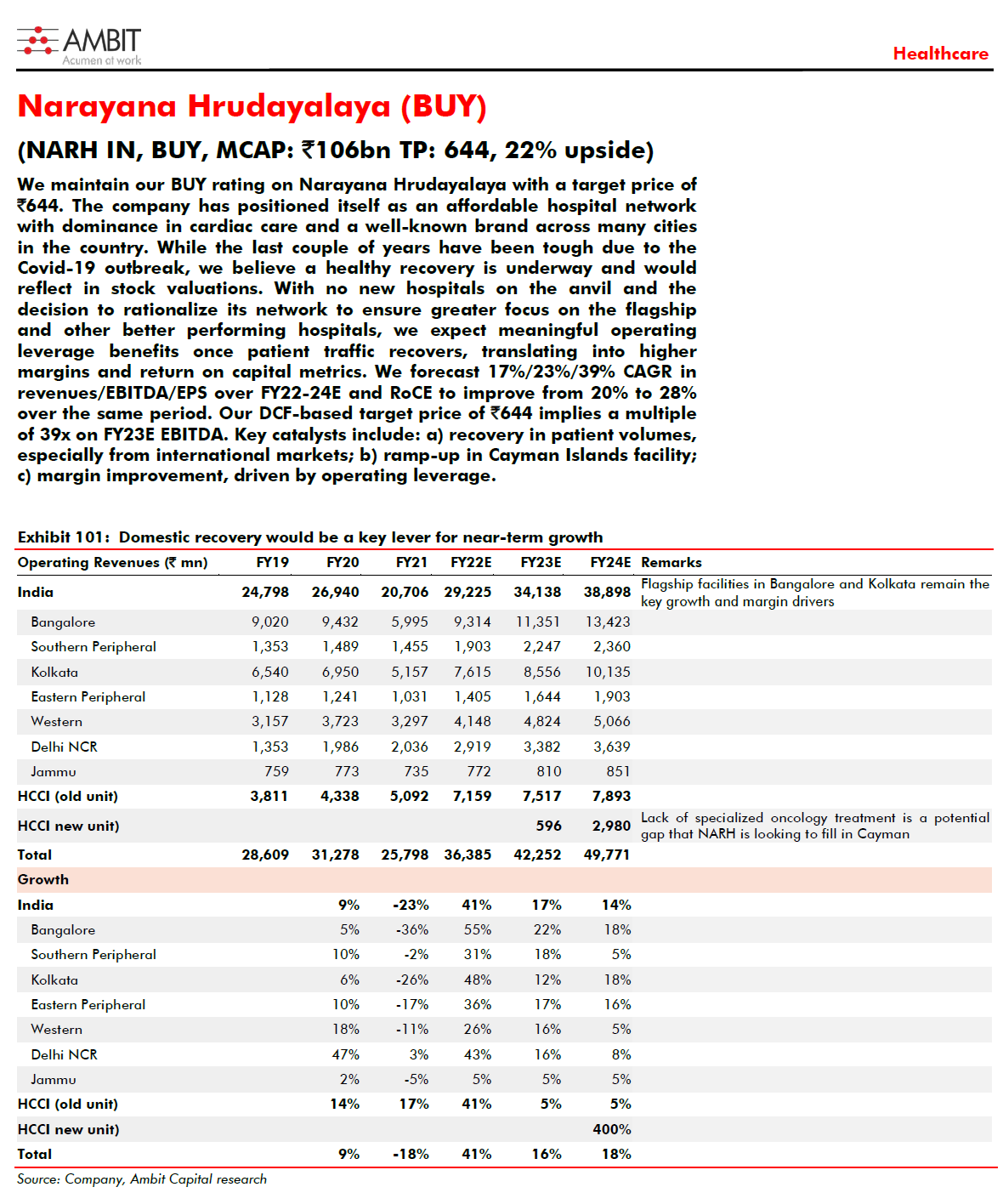

Hospital sector review and initiating coverage report on NH by Prabhudas Lilladher

9 Likes

NH Q4 Results

Decent results, given the Covid wave in early part of the quarter. Flat revenues and and lower margins QoQ, driven by increased tax outflow.

- YoY growth for Q4: Revenue + 12.9 %, EBITDA +23%, PAT +1.3%

- Cayman continues to do well with 31 % growth in Q4 and 33 % for the full FY22.

- FY22 : EBITDA margin of 18.6%, and PAT margin of 9.2 %.

- Q4 EBITDA margin of 19.6%, and PAT margin of 7.3 %

- Net Debt/Equity is 0.16 % which is comfortable.

Inv call is on Monday. Would be interesting to see the results by Aster on Tuesday and Apollo on Wed.

Disc: Invested and holding.

9 Likes

Interesting acquisition announced by NH. This acquired entity will add 100 beds in Bangaluru. It provides ability to offer Orthopedics and Trauma care. Overall cost of acquisition is Rs 200 crore. The entity being acquired clocked revenue of close to 50 crore last year. So the purchase comes has a 4x price to sales multiple.

4 Likes

Opinion by Prabhudas Lilladher

NARH signed a Business Transfer Agreement (BTA) with Shiva and Shiva Orthopaedic hospital (Sparsh Hosur Road unit) located in Narayana Health City Campus, Bangalore where NARH already has two flagship hospitals operational: NH Cardiac sciences (offers only cardiac related services) and Mazumdar Shaw Medical center (multi-specialty hospital offering other than cardiac, orthopaedic, and trauma services). The company agreed to pay Rs2bn upfront and subscribe for Rs. 800mn Optionally Convertible Debentures (OCDs) to be redeemed after 4 years. NARH would have the right to convert OCDs into equity shares of the company (Shiva) in case of default. There is no intent from NARH to acquire other units of Shiva and the acquisition will be completed before CY Dec-22.

.

Sparsh unit possesses 100 beds operational since a decade that has generated Rs490mn and Rs180mn revenues in FY22 and FY23 (4 months) along with healthy profitability. Flagship units of NARH in Health City generates +25-30% OPM. Assuming similar profitability levels, acquisition works out to be 16-17x EV/EBITDA and Rs 28mn/bed in FY22. Prima facie acquisition is expensive (typically cost/bed including land in metros is Rs14-15mn/bed), however it allows NARH to offer entire spectrum of healthcare services in Health city. Assuming Rs800mn money flow back to NARH after 4 years, acquisition works out to be at 12-13x EV/EBIDTA and Rs20mn/bed.

7 Likes

NH Q2 Results

Good results, margin improvement with more cardiac surgeries happening.

- Consolidated operating revenues of INR 11,416 mn up 21.4% YoY and 10.5% QoQ

- Consolidated EBITDA of INR 2,749 mn - EBITDA margin improves to 24.1% (19.4 in Q1) PAT margin 14.8% (10.7 in Q1)

- Net Debt/ Equity is 0.14 now, up slightly from 0.05 last quarter

Regional Breakup

- Revenue Growth - ( India 19 % YoY, 7 %QoQ , Cayman 47 % YoY, 30 % QoQ)

- West (Mum, Amd) continue to struggle badly, no revenue growth and lower -1.7 % EBITDA margin (- 0.6 % Q1)

- Flagship Bangalore region does very well on revenue and margin growth

- Other regions are ok, even North is now slowly getting profitable.

- International patients up to 8 % from 6 % of revenue in Q1

Inv Ppt: https://www.narayanahealth.org/sites/default/files/download/nh_investor_relations/Investor-Presentation-Q2-FY-2023.pdf

Aster Declares results tomorrow, would be interesting to see how they fare in comparison.

NH Investor call is on friday2.30, will try and dial in if possible.

Disc: Invested and holding

8 Likes

Q2-FY23 con call key highlights

- Incurred Capex of 550cr in H2.Planning to incur 1000 cr CAPEX in FY24 as well

- Published 192 research papers this year and published over 1640 scientific papers over the last two decades.

- Significant CAPEX in Banglore and Kolkata

- Mumbai hospital may break even in 6 to 9 months

- Seasonally, Q3 is a weak quarter due to Diwali and Christmas. Expect the robust performance to continue otherwise.

- A mature centre’s growth can come from

-Efficiency work

-Reducing the length of stay

-Changing payor profile (e.g. Govt. insurance or cash)

-Focusing on high-end surgeries - However, this can add low single-digit growth to mature centres. It won’t contribute meaningfully to growth. Capacity expansion is needed for meaningful growth [Hospitals are a capital-intensive business. Once a hospital reaches the mature stage, it does not contribute meaningfully to growth. The company can tweak various parameters, but it won’t contribute to growth. The company needs a new capacity addition to show growth.]

- International patients - 7.5%, much lower than pre covid levels.

- Improvements in gross margin due to cost structure. However, currency movements make costs very volatile as NH imports medical equipment. In addition, additional input material costs

are also volatile. As a result, it cannot provide a strong forecast on gross margin. - Received long pending dues from govt. Difficult to predict when they will be paid.

- Setting up Oncology facilities in many of the existing facilities

- There is a lot of demand for nurses and doctors in the US,UK, and Canada. It is very difficult to hold on to senior resources due to this.

- Gurugram- Most competitive market in the country.

- Ahmedabad- A site location is not so great a part of the city. Had challenges hiring full-time consultants as part-time consultants were taking a portion of patient pay.

Bangalore new acquisitions (Sparsh):

- Orthopaedic speciality.

- 300cr on Sparsh

- Adjacent to the existing facility.

- 100 beds + 110 beds can be added at a later stages

- Decongest existing facilities, as existing Ortho facilities can be transferred to the new hospital.

- 49 cr revenue last year (impacted due to Covid)

- This year could go around 55 cr. 20% margin.

Capex

- Two years - 2000cr

- Cayman - 800cr

- Fy23 CAPEX

- approx $30 million

- Greenfield assets take 24 months to build and six months to commissioning

- approx $30 million

Cayman Island

- Been here for 8/10 years

- EBITA of $12.7 million (approx 102 cr, which is 40% of Q2 EBITA)

- CAPEX (planned $100 million

- 300 cr already spent on acquisitions

- Cost escalation from $16 million to $40 million

- $30 million pending for H2

-$60 million will be in FY24

- It is for the single cancer-focused hospital with a radio theory block.

- Hospital commissioning is a two-step process.

- The first step is radiotherapy. It will be commissioned in Q4-Fy23 and will start treating patients immediately.

- The second phase will start 12 months after the first phase - Due to the new CAPEX, the margin will be affected for a few years. However, in the medium to long term, it intended to protect 40-45 margin on a larger base

- $40 million of cash. If they decide to bring it to India, it will incur taxes. Intend to use that cash for further CAPEX, there

- Other than Cayman- not looking for asset-heavy investment other than Cayman in nearby region. - - Recently concluded contract with St Lucia for management of the asset.

11 Likes

if medanta is spending 350 crore to add 1000 bed capacity in Noida ( read in news article) ,how many additional bed NH would add with 2k crore investment in next one year ? does it mean NH would have 9k to 10k bed by end of FY24 ?

1 Like

-

Cash and cash equivalent 560 cr, debt 780 cr. Net debt 210 cr

-

Net debt: equity 0.11. Sufficient room to fund expansion through borrowing and internal accruals

-

YTD capital outlay 680cr, in Q4 we will spend 320 cr

-

Soft launch of Athma SaaS designed for small healthcare facilities such as diagnostic labs, nursing homes and standalone hospitals

This segment offers an underserved segment of the market scattered across tier 2/3 cities. -

1000 customers for subscription service in Banglore

-

EBITDA for new centres -7.3%. Mumbai Hospital has almost broken even.

-

Gurugram and Dharamshala are there in term of higher EBITA margin of 17%. Mumbai broke even in January, so it will take around a year to move to a higher margin of 17%

-

Doing 2000 cr Capex in Fy23/24. Once the capex is complete, it will take around two years to break even on the EBITA level. This will be a little faster as not all capex in greenfield

-The larger hospital can be tweaked to improve output. However, smaller hospitals do not have a leeway to improve once they reach maturity. -

ARPOB improvement will not happen through price increases but due to payor mix or handling complex patients or bringing inefficiencies

-

New faculty bought in Banglore has integrated well (Sparsh). Generated 30% EBITDA this quarter

Cayman

- Zero tax location for everyone, and it is not time bound

- Exploring opportunities in surrounding islands near Cayman

- New department for Rediology will be ready to treat payment from April 23 onwards.

-Only radiotherapy centre there - Patients from nearby islands are not yet contributed significantly.

- Average Revenue per person is increasing

- Increase in complexity of patients we treat, and it is likely to increase going forward with new oncology centres

- Doing 2000 cr Capex in Fy23/24. Once the capex is complete, it will take around 2 years to break even on the EBITA level. This will be a little faster as not all capex in greenfield

- New Capex is a separate location

- We offer an increasing number of services from the facility. That is a growth lever as well. For example, bought a high-volume ENT specialist earlier.

9 Likes

Anyone knows how much (hospital) land they own, lease and rent. This is equivalent to debt with rents counted as interest. The problem becomes bigger as they eventually need to buy them at higher costs

2 Likes

Narayen Hrudayalya Q3 concall highlights -

Current capacity -

Northern region - 4 hospitals, 1140 beds

Western region - 2 hospitals, 355 beds

South region - 6 hospitals, 2100 beds

Eastern region - 8 hospitals, 2050 beds

Cayman Islands - 1 hospital, 110 beds

Revenues at 1128 cr vs 960 cr yoy,up 17 pc

EBITDA - 254 cr vs 173 cr yoy,margins at 23 pc

Gross borrowings - 780 cr

Cash and cash equivalents - 560 cr

Enough space to fund massive capex lined up for next 2 yrs through a mix of borrowings, cash on books and internal accruals

Intend to spend Rs 1000 cr each on capex in FY 23,24 respectively. Rs 680 cr already spent in FY 23

Out of this, green field capex for FY 23,24 at Rs 200 cr each. Rest is brownfield andmaint. Capex earmarked for Cayman Islands at Rs 800 cr ( aprox )

03 hospitals ( Mumbai, Gurugram, Dharamshala ) are of recent vintage. These generated a revenue of Rs 110 cr, up 17 pc yoy, EBITDA at 9.3 pc. Gurugram, Dharamshala to reach 15 pc kind of EBITDA in 2-3 Qtrs

Most of Cayman capex towards new Oncology block and a new Hospital

New Onco block at Cayman Island to go live by Q1 FY 24. Expect to ramp up quickly as there is no radio based Onco therapy at Cayman

New capex of Rs 2000 ( over FY 23,24 ) will double the gross block

Gross margins improving continuously from Q1 to Q2 to Q3

Company believes, Q3 gross margins are sustainable

Govt scheme patients are about 20-22 pc of total Mix. Have been making representations to revise Govt rates as current rates were last revised long time back and are currently kind of unviable

Expect gradual increase in ARPOB in India business. Don’t expect big jumps

Cayman Islands continues to be a tax free zone. So, no tax for new facility as well

Had Acquired an Ortho hospital in Bangalore for 200 cr in Oct last Yr. Already generating a EBITDA margin of 30 pc

Expect new Cayman hospital to be commissioned by Mid CY 24

Cayman EBITDA margins currently at 40 pc!!! Don’t expect any margin dilution once radio Onco block kicks off in Apr 23

Disc: holding, biased

16 Likes