Thanks @harsh.beria93 for initiating the topic on NALCO. I have been tracking NALCO and Aluminium prices for last few months and would add to the above as follows:

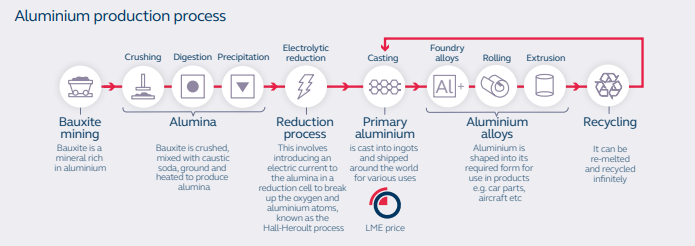

ALUMINIUM BASICS

Following process summarizes aluminium production process (Source: LME)

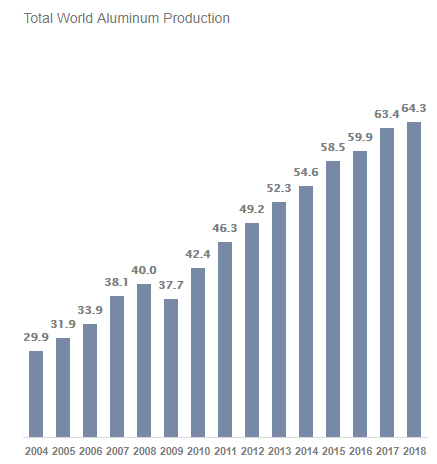

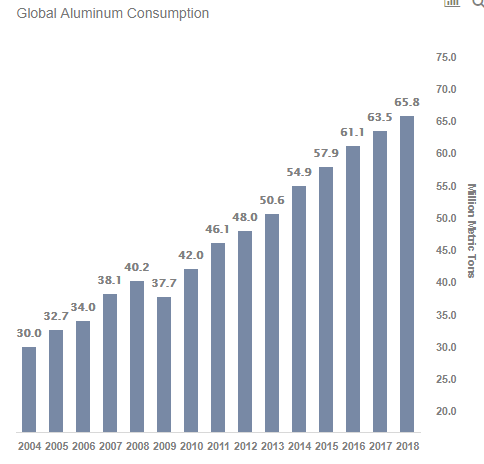

Annual Production and Consumption of Aluminium

(Source - Featured Analyses | Trefis)

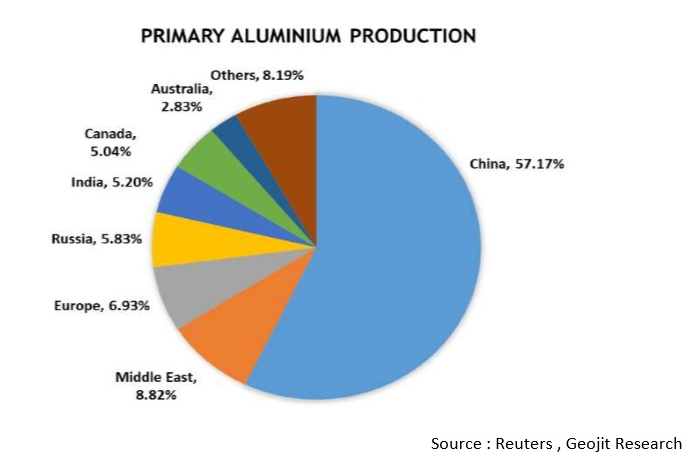

Country wise Aluminium production as per Geojit (2018)

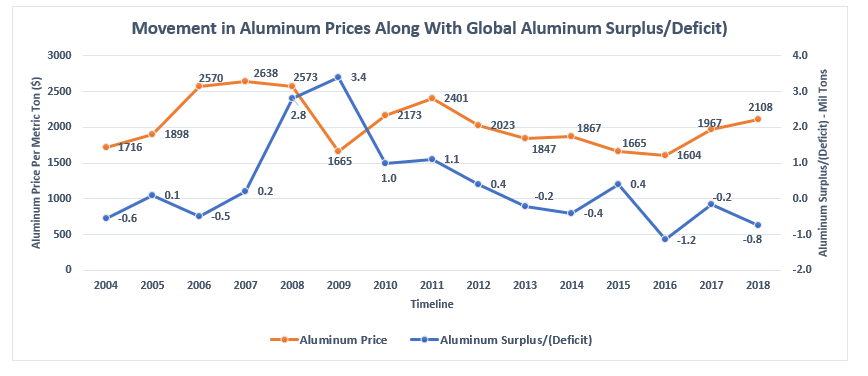

Aluminium prices globally are determined with reference to prevailing market price in the most actively traded commodity exchage i.e. LME. Due to differential costs of transportation and tariff structures between countries, most of the realized prices are at a premium to the LME prices.

One of the key determinant in the LME price is the prevailing global demand and supply of the metal.

Global Market Trends upto 2018-19

- Dominance of China

From 2004 onwards, China has increased its share in world aluminium production from 22% in 2004 to 57% in 2018. Most of this increase is attributable to higher demand from China due to increase in infrastructure, consumption of automobiles and government push.

- Low global Inflation

The commodity prices boom during 2004-2008 was partly driven by higher global inflation especially in countries like China.

Since 2008, inflation across key markets has been substantially lower which hasnt increased cost of producing commodities. As a result, prices of many metals have still not crossed their 2008 peaks.

Case in point - Here is the inflation chart of China which has a very similar appearance to the aluminium price chart

- International trade tensions

A lot of producers including in India had alleged that some countries like China were dumping products in their domestic market. Chinese producers having govt incentives like lower tax, were at a price advantage. Post 2018, with the US-China trade war, tariffs as a whole were on the increase which promotes consumption of domestic produced metal. This has also slowed down the aluminium demand of China, the largest consumer.

- Scrap usage

A lot of the western countries have increased recycling of aluminium, further denting demand for fresh metal. To quote an article from aluminiuminsider.com,

"There is a growing tendency by major aluminium processors to use higher amounts of recycled aluminium for making their products. At the same time, there are no reliable and accurate statistics on how much new scrap goes back into the production process over closed-loop schemes, or how much old scrap has replaced orders of primary aluminium.

China will import alloyed aluminium ingots (produced from secondary aluminium) from Europe and elsewhere instead of scrap and may increase exports of semi-finished aluminium products, at higher value and prices than alloyed ingots, while reducing the same (conversion) business in Europe and elsewhere. All things considered, this is the real reason why primary aluminium demand fell so quickly."

(Source - https://aluminiuminsider.com/aluminium-market-oversupplied-demand-growth-flat/)

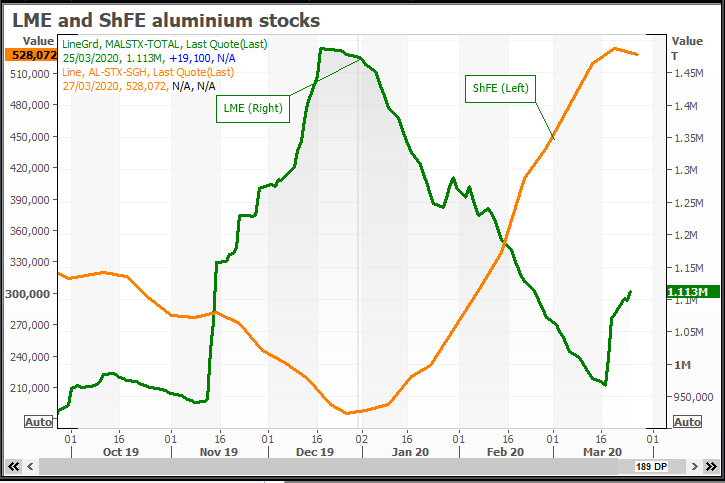

Current Scenario (Covid-19) - Supply side

Preliminary estimates of Aluminium surplus in March 2020 at LME and Shanghai already are at a more than 10 year high.

This data does not include stocks at unapproved warehouses (which are not counted in LME stocks) and stocks stuck at smelters around the world due to logistical problems. A lot of producers cannot completely shut the smelters and would be producing even with marginal cost of production higher than the market price. As a result the final surplus figure after accounting for all the stocks say after 3-6 months would likely be much higher, maybe even higher than levels seen in 2008. The fear is that this surplus would take much longer to clear out as compared to 2008 since growth in global demand is lower than 2008 and also there is increased usage of scrap.

This has caused LME aluminium prices to crash below USD 1500 levels, at which a lot of the global smelters would run cash losses.

In the near term, the most logical way to increase prices is to shut smelters and reduce the supply.

As per various reports, high cost smelters in China have started to slowly shut

Chalco is the world largest producer of Alumina.

https://www.nasdaq.com/articles/chinas-chalco-weighs-output-cuts-as-aluminium-alumina-prices-hit-lowest-since-2016-2020-04

Likely Bottom?

“Wood Mackenzie estimates that prices under 12,000 yuan a year (roughly 1600 USD) means that “nearly 70% of the Chinese producers will be under water, and that’s certainly not sustainable”. Their profitability is also suffering due to sharp increases in the prices of raw alumina, promoted by bauxite mine supply and transport costs.”