THE VALUEPICKER PORTFOLIO

Most of the portfolios coming on the forum are companies that get recommended very very frequently. Where is any value picking in them? And most of all, I believe if one thinks that these 250/300 companies is the whole Indian share market universe, there is no need to talk about value picking. All these are there in all MF portfolios under some scheme or other. Just look at the ones which have the maximum no. of these and buy them and go to sleep.

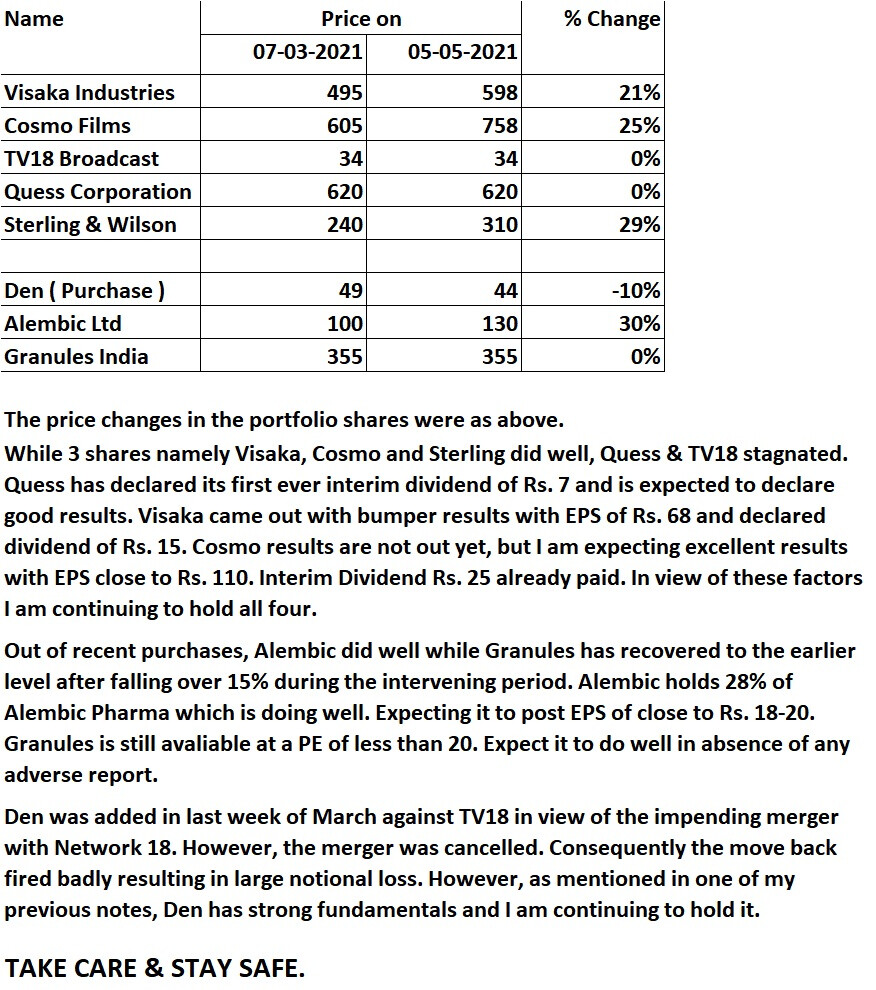

Further, I am in the market not only for making money but also for some excitement. And there is nothing more exciting than making a real VALUE PICK that justifies the name of this forum. Hence, most of the shares I own are shares which are completely out of sync with most of the other portfolios disclosed on this forum. Other than Sterling Wilson, and Cosmo Films, I own the other 3 for a long time(4-7 years), but added good quantities post March crash. One common thread is that despite not being talked about frequently, they all are among top 3 in their field.

1. Visaka Industries : CMP Rs. 495

- No. 2 in Asbestos roofing sheets, No. 2 in Cement Board Panels. Unique Yarn Producer, Original ATUM solar panels ( product patented for 20 years).

- Strong financials with high growth expectations in coming years.

- Investor friendly. High dividend yield. Dividend Rs. 15 last year.

- 50% interim CFY.

- Low pledge. Low borrowings. Low PE ( below 8 ) on FY21e EPS – 65+…

- High promoter holdings – now 52%+. Have increased their holding by over 10% in last 9 months.

- Old established co.

- Highly innovative. Vnext cement board panel and Atum solar panels are the examples.

- Had couple of lukewarm years but has bounced back magnificently

2. COSMO FILMS LTD. : CMP Rs. 605

- BEST PICK IN LAST 2 years. Among top 3 in packaging material co. Supplies to TOP MNC’s around the world. Have almost 57% turnover from high margin specialty films – some invented by it.

- Very Strong financials with high growth expectations in coming years.

- Investor friendly. Dividend last year Rs. 15. This year interim Rs.25. High dividend yield.~ 5%. Committed Dividend payout policy. Very liberal tender based buyback at over 30% over prevailing price.

- No pledge. Low borrowings. Low PE (below 6) on FY21e EPS – 100+.

- High promoter holdings – 44%.

- Old established co.

3. TV18 Broadcast : CMP 34

Once merger completed, it will be a part of the largest digital player in India Network18

- with content production,

- event management,

- broadcasting news and entertainment including regional channels,

- most popular Stock Market portal in Moneycontrol,

- llast mile connectivity for TV and internet through Hathway and Den,

- most popular business channels in English, Hindi and Gujarati.

- Profit making. Owned by the largest corporate in India – Reliance.

- All this put together could turn out to be money spinner like Reliance Jio in few years.

4. QUESS CORPORATION : CMP Rs. 620

- Largest manpower provider in the country,

- very large business solution IT setup,

- largest HR solutions IT company - Allsec,

- Tie-up with Amazon for post sales services for appliances,

- largest facility management organization,( services list is endless),

- low debt could be debt free by end of FY21, high promoter equity, high free cash flow.

- Have started integration of subsidiaries.

- CON : Has not paid any dividend so far. But could be generous pay master by next year

5. STERLING & WILSON SOLAR : CMP Rs. 240

- Largest EPC contractor in India, probably no. 2 or 3 in the world,

- MNC in true sense,

- large order book,

- in fast growing line of business i.e. solar power generation, pollution free.

- Have started adding third party solar plants to its portfolio on operations and maintenance basis, very asset light and high margin activity.

- Also involved in data centres setting up, the heart of cloud computing. As the cloud computing is growing exponentially, so is the need for larger and larger data centres.

- The low price only due to controversial loan repayment issue, which will get sorted sooner or later, as the hearing in the parent co. matter with Tata Sons has been concluded and judgment could be out shortly. And then it will fly.

PAST INVESTMENTS : In addition to the above, I also own Bajaj Finance, Bajaj Finserve, SRF, TVS Srichakra Tyres, Piramal bought when they were relatively unknown names 5-7 years ago.

Had invested in specialty chemical cos. Atul, Amal, Akshar Chemical, Ashahi Songwon, Bodal Chemical long before the fancy for the industry began. Got out of Akshar at almost 10 times in 3/4 years ( 65 to 650) and multiple times gain in others, although not as stunning.

WORST LOSS IN AVADH SUGAR , bought at close to peak at around 1100 initially and finally got out at around 400 ( adjusted for bonus). Other Major losses in Trigyn Tech, Sinclair Hotels, L&T Finance, Indusind Bank ( bought around 1600, sold at ~450), Piramal Enterprises ( Bought around 2600).

BASIC THOUGH PROCESS :

Look for the best but not BEST KNOWN.

Do detailed due diligence before increasing exposure.

Don’t get scared by market moods.

Falling knives are best catch if you are convinced about the potential, but add slowly.

Added all the above mentioned shares in March / April 2020 fall. Doubling / tripling the holding in some cases. Some of them near their all time lows.

Tripled the holding in Cosmo Films post declaration of Q2 and Q3 - FY21 results as the conviction grew. It did nothing much for 4/5 months gaining only about 20% in a roaring bull market. Finally, the patience paid off last week when it picked up 25% in 1 week.

Portfolio losses are heart breaking but keep your cool(very difficult).

In case of conviction holdings I AVERAGE on both sides. ADD slowly when falling and SELL slowly while rising.

I am convinced that this portfolio is not the type what one generally finds favour with lots of forum members, but I firmly believe that these cos. will do well in next 3 to 5 years solely on the basis of their unique business models and financial strengths.

My latest additions to portfolio are Alembic Ltd. and Granules India