unfortunatEly there are just red signals not barricades. Everyone need to take own call. Promoter has no skin. Also if minority is not taken care why in future things will be different is to be answered. Is company transparent , did they announce breach on exchanges. Or you heard from somewhere else. If answer is no why future will be different.

1 Like

Currently everyone is losing money but good to remember these cases in next upturn.

Case study - 2

Stalled Filmi-Chemicals Company (SFC)

January 2025 – IPO

Buzzword: Semiconductor and specialty

Narrative: Structural growth, import substitution, long runway.

May 2025

Analyst: Can you provide an update on the capex for the Timbaktu plant?

Management: We received IPO funds only towards the end of February. March was a strong month, so we prioritised growth over capex.

Share Price: ₹65–75

August 2025

Analyst: Update on Timbaktu capex?

Management: At Timbaktu, we realised we can build a plant with 2x capacity, so we had to redesign everything—hence the delay. Also, we’ve received land from the government at Rajaplace. Phase 1: 5,000 MT Phase 2: Another 5,000 MT This will enable backward integration and improve margins. Overall capex is now ~3x the original IPO plan.

The Investor’s Brain: Capex from 1X to 3X = 3x revenue, 4x profits (higher due to backward integration). Bingo. Multibagger alert.

Share Price: ₹115–140

October 2025

Analyst: Update on Timbaktu and progress at Rajaplace?

Management: Timbaktu capacity is now being expanded to 2.5x the original plan—hence further delay. At Rajaplace, we’ve decided to execute full 2x capacity in one go, instead of two phases.

The Investor’s Brain: Capex from 1X at IPO to 3.5X now. That’s 3.5x revenue and 4.5x profits. Capacity coming faster. Even better!

Share Price: ₹250–400

Side Show: Promoter A(ffu)CTION

October–November 2025: Promoters sells shares in the ₹300–400 range.

Company Press Release: Promoter sold shares to provide an interest-free loan to immediately begin the Rajaplace project. This reflects strong promoter confidence and commitment.

The Investor’s Brain: What integrity! Sacrificing personal upside for the company. Lending interest-free money. Salute to such management. i am sold on management i am buying more.

February 2026 – Reality Check

Analyst: Last time you said Timbaktu would start in January. Now the presentation says March.

Management: Design changes due to size increase caused delays earlier. This time, material from the US didn’t arrive. Commissioning should happen in March or April.

Analyst: You’re raising money through a rights issue?

Management: Yes, our capex plans went up, so we need additional capital.

Analyst: You had sold stake earlier to fund Rajaplace capex.

Management: Yes, and we’ll get shares for that money.

(analyst & investor what?)

The Investor’s Brain (No Brain? Finally realisation?):

Promoter sold shares at ₹300–400. I bought at those levels, believing “bigger plans” and “selfless promoter”. Promoter converts into shares at sub-₹100 via the rights issue. I’m stuck at lower circuits, no exit.

Share Price: ₹175–200 down 50% from top

The Final Shock

Analyst: I notice that IPO funds are still unutilised.

Management: Yes, work is ongoing. We never pay in advance.

Investor & Analyst (together):

You don’t pay in advance, yet you raise more money? You haven’t utilised IPO proceeds, yet raise capital? Rights issue is priced at below 100 ~50% discount to CMP? intent?

21 Likes

Taking the “Other Side” - The Cash Conundrum

A friend of mine — an IITian and a very sharp individual — recently told me that in January 2020 he was convinced that the market would fall sharply in the months ahead. By the end of that month, he had already sold all his mutual funds and investments because he believed that what was unfolding in China with COVID would inevitably spread to India and the rest of the world.

He was right. He could see the risks building well before most people did.

He wanted to go short, but he did not know how to short the market. Even today, he feels that if he had known how to do it, he would have made a fortune.

But that is not where the story ends.

At first, I thought: what a genius — to understand the risks so early and move entirely into cash before a 20–30% fall.

But then I realised something more important: he was never able to get back in. During the full-fledged bull market from March 2020 to 2024, he could not meaningfully participate despite one of the strongest rallies in Indian equities. The problem was not getting out. The problem was getting back in.

The real issue was that once he had mentally taken “the other side” — whether that meant being in cash or wanting to go short — coming back fully and with conviction became extremely difficult.

My friend did not know how to short, but he knew perfectly well how to go long — through mutual funds and direct equities. He could have made enormous money simply by investing aggressively from March 2020 onward. But he could not.

Negativity tends to hit faster and deeper than positivity.

Even if he had managed to short, that trade would likely have worked for only a month or two. Going long, on the other hand, would have worked for the next three to five years.

He missed that entire bull phase because once the idea of “the other side” took hold, it became very hard to shift back.

The danger of cash is not just that it may underperform. The bigger danger is that it can slowly become a mindset. Once that happens, getting back into equities always feels either too early or too late.

That is the real cash conundrum.

34 Likes

Lovely post Jaiprakash!

Our minds work in strange ways. Price anchoring is such a powerful bias - I have lost many opportunities because I “thought” a stock was expensive at x, did not buy when it moved to 1.5x against my assessment, only to see it become 15x! Once your friend missed entering while NIFTY was at 8K, he would find it very difficult to enter 12K. I have realized the only way to take the gain is to endure the pain and what enables us to take pain is to have the ability to survive.

12 Likes

What a company …

You’ve perfectly described Promoter A(ffu)CTION and his Rajaplace “interest-free loan” masterstroke ![]()

Timbaktu… bahaha — every time they say “just redesigning for 2.5x capacity”, I hear “just one more round of capex, bro, trust me”.

I was the official boogeyman in this entire “selfless” promoter journey, okay?

You nailed the investor mindset so hard — “multibagger alert… salute to management… buying more!”

And the best part? You even exposed who actually got paid in advance… it wasn’t the vendors,and rights issue at 50% discount….may be it was more then 50% ..okay !

My tuition fees were fair… but damn, small would’ve been nicer. managed to do rights thing and cover just a little.

Next upturn I’m just gonna re-read this thread before touching any “semiconductor + import substitution + long runway” story…especially if its Promoter A(ffu)CTION type..okay !

2 Likes

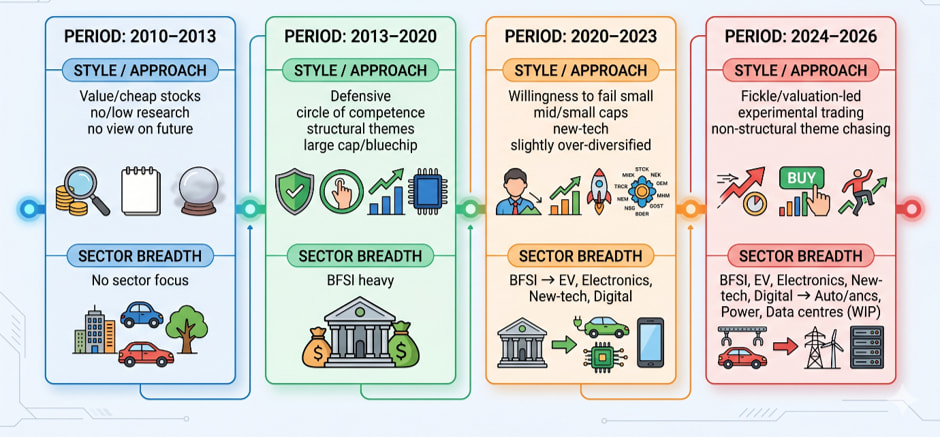

Portfolio Update – May 2026 – random/forced exposure to evolve further, and being dumb

Most of my learning over the years came through blogs, videos and company filings. It comes mostly because I chose what I want to read or what algorithms threw at me. So, there was lack of randomness and forced exposure.

From last 1 year I have been attending monthly investors meet where few of VP members meet and discuss ideas. I am not interested in Ideas; I am interested in their process. Many of them come up with varied industry background and wide network. Fascinating to learn and connect the dots. This exposure allowed me to learn a bit about sectors I never looked at – Power, Data Centre etc.

Learning comes from willingness to accept new, expand horizon and embrace new areas even if there are traces of doubts. So, these meets opened me to areas of power and data centre related stuff. Luckily Jan to March dips were good enough for me to buy some of these at reasonable levels (CG Power, Aeroflex, E2E, KOEL, KSH International etc.). The point is if I was not exposed to right set of people I would not have read about these industries on my own as it was a mental block. Thanks to @hardik_shah1 for opening up my mind to these sectors. Thanks to @SHAIL_APTE who brings lot of industry insights and arranges these meets. Over and above, thanks to this platform.

Coming back: It’s ok to take small steps before the big strides. In investing small steps are good enough though.

Just summarising for myself how I evolved (for my future reference) (Gemini created):

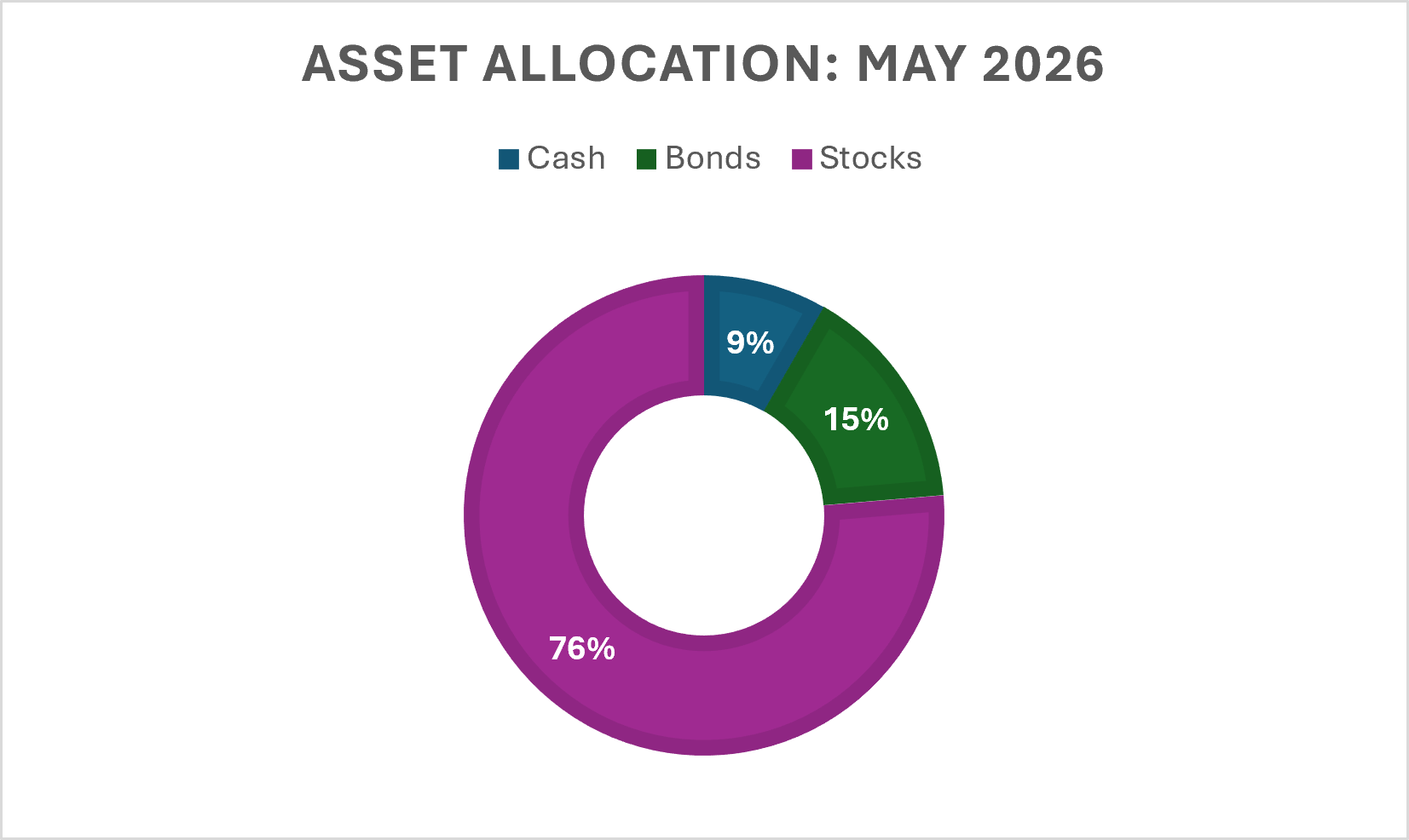

Equity allocation peaked at 85% - being dumb

I do not have any foresight; I don’t have confidence hence I was dumb to ramp up my equity allocation to above 80% as my PF was showing some pain.

A tumultuous period where being dumb to increase equity allocation helped in hindsight. Equity allocation reached peak of ~85% in April, now down to 76% in May 2026. Still at highest ever range vs. last 3 years.

![]()

I would like to bring equity allocation down as I went bit too much aggressive in last 6 months.

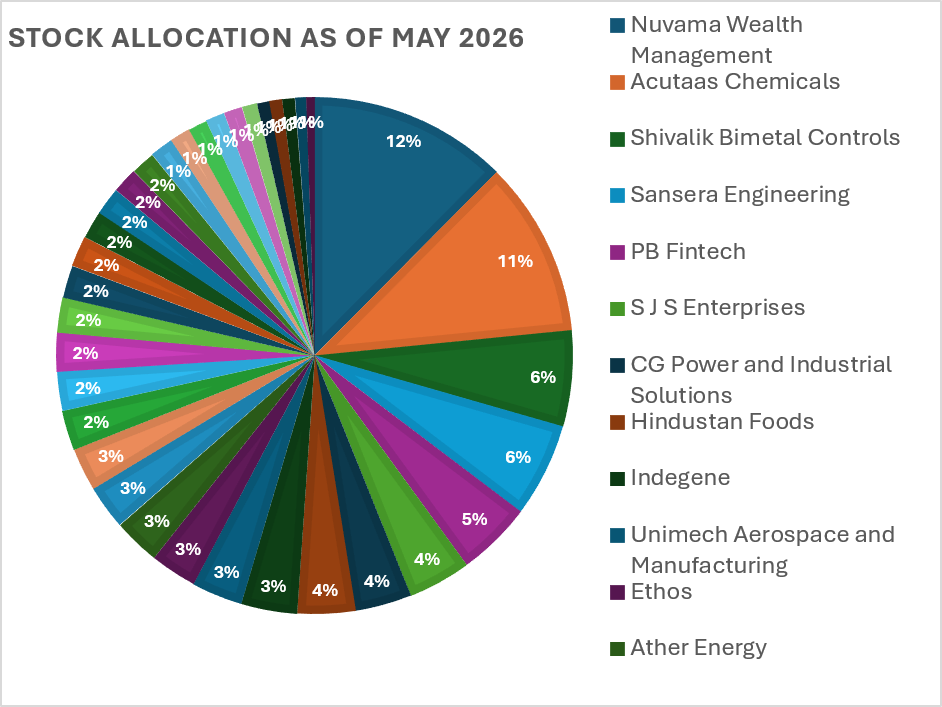

Stocks

Portfolio remains more diversified than I want it to be with 35 positions. However, top 5 and top 10 positions are steady at 40% and 58% allocation.

Largest positions remains Nuvama and Acutaas. I built substantial positions in Shivalik and Sansera so they came to become top 5, the run up in prices also helped.

Some stock stories

Shivalik Bimetal and Sansera are based on expanding the capabilities to higher levels of growth and margins.

Shivalik Bimetal

I was invested in Shivalik in 2021, held it for 2-3 years. Recently I re-entered post its Q3FY26 commentary. The company is getting growth back in its base business (Shunts to US EV customer) and post tariffs they are focusing more on components and assemblies from strips business. Componens/assemeblies are higher margin and at 2-3x higher value. The clincher was its new products “busbar” for Automotives (initially EV late ICE too). This product alone could help grow its absolute revenue 80% in 3-years. While rest of the business could grow at 10-12%. This could double the revenues and more than double profits in 3-years.

I have shared Sansera rationale in my previous post.

I had written about these two companies on my LinkedIn page. I will post this content separately as link may not be allowed.

Breaking the mental block

As I removed my mental block on power/data centres, some defence, they became anchor of my portfolio performance in last quarter. These companies (KSH, E2E, Aeroflex, CG Power, Zen Technologies) went up in 30-100% range. Thereby my PF negated all the downside it could have seen due to external events.

Negatives

As I remove mental blocks, take small steps, portfolio becomes overdiversified. Also, I get a fleeting feeling with regards to many companies I hold. I have changed from strong conviction concentrated investor to fickle-minded overdiversified investor.

However, this has been problem from early 2024. High valuations do not allow me to take large conviction positions. Though I am complaining, outcome (returns) has been excellent so far.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation. I work for an investment advisory/PMS firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.

13 Likes

Mental model: Capabilities

Mental models explain how things work and are powerful tools in investing. One way to build them is by studying great businesses - their moats, revenue models, and evolution over time.

A company selling books online might seem like just a bookseller. However, its true capabilities are:

1. efficient inventory management,

2. lightning-fast delivery, and

3. an easy return policy

These capabilities can be used to sell anything online. So, you gain scale and that’s how you get “Amazon”.

We cover Apple’s case below to elaborate how capabilities helped it evolve over the years.

Apple

Capabilities driving “Niche to Global” transformation

Apple exemplifies how its core capability of design and tech helped it to evolve and create an ecosystem. Its customer base expanded from a niche segment of education sector and select creative professionals to global consumers. Today Apple is a universal aspirational brand.

Source: cbsnews.com and AI (gemini)

Mac computers accounted for 90% of Apple’s revenues until 2000, iPhone contributed about 50% in early part of 21st century. Quarter past 21st century, 2025, now it is a complete consumer device, entertainment and media ecosystem. As of today, its high-margin and high growth businesses - Services and Accessories, account for 50% of Apple’s profits. Services segment comprises App store, Apple Music/TV, Apple Pay, iCloud etc.

Apple’s customers and segment evolution

The core capabilities helped Apple expand its business from niche segment to become a global aspirational consumer brand. In early years, key customers were mainly affluent and high-income earning businesses and individuals in the US. In the recent years, it is not just an aspirational brand but a craze among Gen Z and Millennials across the globe. Affordability is no more a limitation, in India, a massive 70% of iPhone purchases are on EMIs.

Source: Korman capital and AI (Gemini)

The Indian context

It is critical to continuously refine our investment framework. We looked at an Indian auto ancillary business a year back, its key product, connecting rod, is used in ICE cars. A dying or low growth business, we assessed. However, company’s stock did well to deliver ~30% returns within a year. We re-evaluated the company. We noted that it started reporting strong revenues from high margin Aerospace, Defence and Semiconductor (ADS) segment. ADS division’s revenues doubled within one year and it also launched few products in EV and tech-agnostic segment.

The issue in our investment thesis was our fixation on products, not capabilities - like forging various metals, casting, and precision molding/crafting. Viewing a company as a mere product maker limits you to narrow customer segments and sectors. Reframe this auto ancillary as a ‘precision engineering’ firm, and your thinking horizon expands dramatically. Opportunities then become visible across new sectors and customer segments.

Now having deeper understanding of this mental model, we are assessing few Indian businesses which are strong in capabilities and at the cusp of next big opportunity. One of the examples is a niche components company which is expanding its customer segments from consumer electronics (2005) to autos - both EV and ICE, smart meters, and now to data centers. Electron Beam Welding is the key capability of the company.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation. I work for an investment advisory/PMS firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.

7 Likes

if its ok, can u share why these businesses were a mental block? was it because of asset heavy nature, execution risks, dependency on government spendings, capex risks, previous infra cycle shadows or simething else?

why i ask is because i also have multiple mental blocks, have been working on some aspects…

This is an excellent point. This understanding comes when we see underlying companies with a vision shared with the promoters. If promoter is ethical & management top class, sooner or later business will evolve with its enviornment.

@Investor_No_1 I have been investing since 2010 and reading financial news from 2006. I have seen bad power cycle. Hype was similar to what we see now. My friends fell in love with this theme they invested in Ujaas, Suzlon (all time favorite), Tata power in those times. They never made money. So i have baggage of past.

Then off-course why I never invested - as you noted asset heavy nature, execution risks, dependency on government spendings, capex risks. In fact you talked about previous shadows (but on my friends).

Cost of being right: Also being vindicated for so many years - I was right, did not allow me to change side.

Now how did it change -

1. Someone (@hardik_shah1) talked about CG power with huge confidence - Some great said never underestimate a confident/overconfident person. I met Hardik sir over many meetings and could sense his good judgement. I was sold on the story but not on valuations - but that’s where “taking small steps in traces of doubts” came in picture.

Later when CG power’s margin held up vs. many transformer guys saw decline, I could see an evidence it is in different league, I ramped up.

2. Margin of additional risk was low: Stock Prices were 25-50% down or valuations were cheap (KSH at <400 was 15pe on Fy27). I ramped up when in weak market it did not fall much (sign of strength). While CG power was down 25-30% from top and E2E was down 50% from peak so margin of additional risk was low.

3. Governance clearance - CG Power we know, in KSH Malabar was invested.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation. I work for an investment advisory/PMS firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.

4 Likes

bang on, the infra part of power was something many of that time tried to stay away from (including me) c g power demerged (or whatever) from CG and i was more interested in the consumer part of CG….last 2-4 years have been excellent for the infra part of such businesses…i happened to be a part of this rally unintentionally via one of my pick that i bought for superior tech and not for infra….so yes a mental block was/is there and for good reason….though have had some learnings around b2b businesses, including these….

btw valuations are indeed crazy so i consider my infra power stock as 1/3rd its value in my portfolio, if not less….

Changing the lense

Recenly I was reveiwing an NBFC, grew its loan book 75% YoY in FY26, and Q1 FY27 loan book grew at 82%. However, just before Q1 FY27 update I changed my view on the company - on valuation angle.

Most of the times we just see what company is and what it can be in the next 2-3 years. In this case company guided for 25-30% loan growth in medium term. I look at that, i look at ROA/ROE and I thought it should trade in 3-4x price to book value.

However, I changed that view. The said NBFC released its AR just last month. The annual report outlined the ambitions - “Looking ahead, we are laying the foundation for future growth and diversification through the proposed establishment of subsidiaries in areas such as Asset Reconstruction Company (ARC), Alternative Investment Funds, Insurance Broking, and an AI-led tech platform. This reflects our forward-looking approach toward building a more comprehensive and resilient financial services platform”. Source - https://www.bseindia.com/xml-data/corpfiling/AttachHis/931fe3c5-d70e-441a-8222-f9a1ee2ebdfb.pdf

What changed?

Now i dont see this NBFC as defined by numbers. I see it as defined by ambitions. I see it as a group (APL Apollo group) trying to becoming a giant. Financial Services is an ocean so its a right place to emerge as a giant. A place for next gen to prove.

Now i dont look at it as an NBFC to trade in 3-4 P/B band. I see it as where this family will be satisfied to see the company in 5-7 years. 1L crore loan book or 1L crore mcap? so my markers have changed.

Right way to think? - offcourse financial services is pretty bumpy place need to track the execution and capital allocation.

Disclaimer: bought today and holding it from last 3-4 months. This is shared just for educational purpose not an advise. I may exit at any point of time without updating here.

10 Likes

Journal - 9th July 2026.

Equity allocation - 80%+

I feel market is highly polarised. Some themes with fast growth and fast growth potential are trading at very high valuations (may be optically to my untrained eyes). Sectors - AI/DC and power proxies.

The rest of the market which is not hyped has modest or no growth but good established franchisees which are seemingly trading at low valuations (again may be optically). I put Banks, insurance, consumer etc in this category.

Then there is one area which is bit lost in this polarisation - recovery or steady performance lost in the noise of extreme plays. That’s what I am targeting right now. Good past couple of quarters or good commentary of near future.

Some examples:

- A watch company -

What’s working - sales growth of 25%+ for last 12/13 quarters.

Source: Screener.in

Stock Price: down ~20% from top in the last 18 months.

Challenges - margins are under pressure due to store expansion and rupee weakness.

Follow-up - One has to take call or track above two issues will they change in the next 2-3 years?

- A grader with 60%+ market share:

Whats working - The industry growth is very strong (15%+), company has strong revenue growth (20% average) in last 3 quarters and stable margins YoY.

Source: Screener.in

Stock Price: down ~40% from top in January 2025.

Challenges - Got bad name during IPO due to valuations and growth fell to single digit.

Follow-up**:** Growth issues seems to have gone away and management guidance (20% EBITDA growth) for FY27 is decent. Now we have to see if investors forget the bad experience of IPO. Growth has revived, do investors think that company has a defendable moat - crucial for re-rating to my expectations of 30PE. Stock is currently trading at 20x FY27 earnings.Now what PE shall we give to a company which is growing at 20%, ROE/ROCE of 40/50%, its B2B customers rave about it that its products are being graded by this company.

Disclaimer: I own both the companies, I am adding these on daily weekly basis. I am not a certified advisor. Please do your own due diligence. I could exit these or add more without any prior intimation.

5 Likes

Is company no 2 in financial services, consumer,Healthcare or industrial??

Markets can stay irrational for a long time - But we as investors try to find opportunities and stay rational and accumulate steady and high margins and high return ratio businesses and stay long.

The second company is IGIL.

2 Likes

Note to self:

2point2 letter reminded me of missing Tata Elxsi and LTTS. I made 20% and got out. After that both stocks went up 10-15x. I could not have rode it as I never understood business but when stocks run up 20% in short-time - I should go and try to understand the business or at least see what management has to say on future.

Some excerpts from note for future reference:

“If a position was sold and the stock subsequently rose, the eager learner concludes “I sell too early” and adjusts their behavior, perhaps holding longer next time, even when the next position genuinely should have been sold. If a position was sold and the stock subsequently fell, the eager learner concludes “my instinct was right” and grows more confident in a decision-making process that may have had little to do with the actual outcome. Both conclusions turn a single datapoint, contaminated by market noise and mental bias, into a flawed rule.”

6 Likes