Hi All

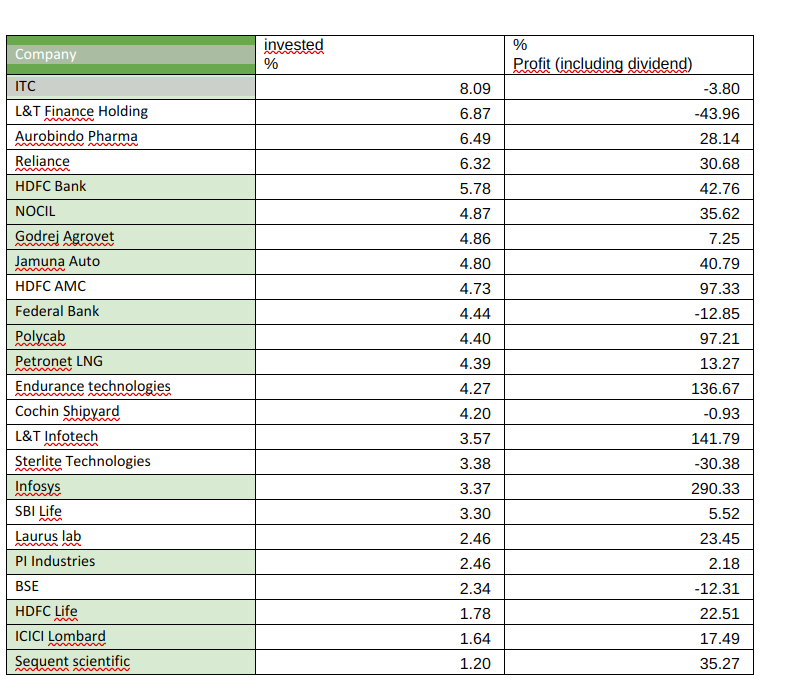

My investment journey started few years back . For the last 3 years i am investing a fixed amount in a group of companies every month (Kind of SIP) . Investment theme is based on value stocks, under penetrated and huge opportunity sectors (Insurance & AMC, Gas sector), cyclical and Digital theme. Below is my portfolio , please provide your valuable feedback

|

Reliance |

7.60 |

I am considering Reliance as a digital company rather than a petro chemical –Oil gas company. Jio digital, JioMart etc. will be a game changer. Company has recently acquired a number of fintech, digital, cloud related company in order to roll out JioMart. If voda-idea goes bankrupt, then Jio will have around 40-45% market share and Jio is more technically capable to roll out 5G services with less capex. As mentioned by an analyst Reliance is a combination of AT&T, Amazon and Exxon. Concerns: Deleveraging plans if not worked out will put pressure on balance sheet which has got 2 lakh core debt |

|

HDFC AMC |

7.60 |

They got 15% market share in Mutual fund industry and got height percentage of Equity AUM. Mutual fund industry is still in nascent stage in India and got scope to grow. Concerns: 40+ AMC are there in market. Most of the funds by HDFC AMC’s are not in top rating of CRISIL but somehow customers are sticky to it |

|

ICICI Prudential |

7.60 |

Why not HDFC Life or SBI Life? From a valuation perceptive ICICI pru is behind both of them and their strategy to increase Protection business will gain traction in coming years and they will finally catch up with peers. Insurance is long term story and I believe all these players will gain in a continuous manner |

|

HDFC Bank |

7.60 |

No need to talk about their retail banking. Their card business has got best RoA among peers. HDB will be listed soon and market is expecting around 1100+ rs for a share. Bank has got excellent digital capabilities and their myApps is gaining traction. Concerns: who will be the successor of Aditya puri, will it be an insider or an outsider and how the new CEO will fit into? |

|

L&T Finance Holding |

6.46 |

Largest financier in Renewable energy, top financier in Vehicles & Tractor I am considering it as a turnaround story. Current CEO has clearly articulated their strategy “Right to Win” and attain ROE of around 20. Because of L&T parentage their rating is AAA and no funding worries even in this turbulent times. Their NCD’s is getting oversubscription. They are now moving into city gas distribution financing and consumer lending which I guess which will be the next growth levers. I believe they will sell their AMC business (L&T mutual fund) just like defocused business and will concentrate on Lending business alone Concerns: higher exposure to Real estate, wholesale lending especially supertech builders, |

|

Polycab |

6.08 |

Largest Wire & cable player in organized players. FMEG is picking up at a steady pace. ROCE is 20+ and 600crore in cash. PE ratio is less compared to Havells, v-guard etc. |

|

L&T InfoTech |

6.08 |

One of the best IT Midcap company They started concentrating on Digital many years back and currently got 40+ % revenue from digital. Merger with Mindtree which is imminent in future will make it 4/5th biggest IT company in India. Not many verticals of both these companies are getting overlapped that’s a huge advantage Parent L&T has started a new company called L&T NXT which is purely engaged in Digital. Need to see how this will play out |

|

Petronet LNG |

6.08 |

Largest importer of LNG India gas demand is expected to double over next few years. With Cochin-Mangalore pipeline completing in March, Utilization levels in Cochin will increase considerably. Not much competition from others players for Dahej and no hope of ONGC increasing gas production till FY22. |

|

ITC |

6.08 |

I believe, ITC is hugely undervalued. Much debate is there in forum on this topic so not taking it up. My belief is that with the upcoming ICMLs, and 25000 crore capex they can surely increase market penetration. Taking profit out of Tobacco and investing in other business is increasing their bottom line and in future FMCG will contribute to Topline also. HUL also went through this phase in the past. Concerns : Sin stocks are getting de rated worldwide and overhang of GST |

|

Endurance technologies |

4.56 |

Largest aluminum die casting producer, prominent market shares in Transmission, braking and suspension. Caters to 2W, 3W and 4W. They got family tie up with Bajaj auto and Bajaj was their major client few years before. Now they all major auto players in their kitty and client concentration is decreasing Focus on EV vehicles (Management indicates that they will EV related business) ABS for 2 wheelers will be the next growth levers. Limited impact on EV Concerns: Auto slowdown |

|

Jamuna Auto |

3.16 |

Largest Leaf and Parabolic Springs producer in India (70+ market share) and second in world. Performance depends upon the CV market and hence down in the current slowdown. Company is trying to increase the after-market share in recent years and slowly seeing some traction. Got excellent ROE and ROCE. No impact of EV |

|

NOCIL |

3.04 |

Market leader in Rubber chemicals Problems in China, Large capacity expansion in Dahej, increasing international exports and concentrating into value added products definitely aide them to gain further market share. No impact of EV Concerns: Auto industry slowdown |

|

Cochin Shipyard |

4.56 |

Largest ship building & Repair company With the completion of ISRF and Dry dock and takeover of many ship repairing ports, CSL will become largest ship repairing company by FY 21/22. High order book and quality management (Not the government). Not much debit Concerns: Inclusion of CSL in CPSE will have an impact when they come up with CPSE ETF. Govt asking for more dividend and buyback of share. |

|

Sterlite Technologies |

4.56 |

Largest Optical fiber & cable producer in India (40+ market share) From being a cable producer they have moved to complete end to end solution provider. Recent acquisitions, huge Cloud & 5G opportunity, smart cities in India, good margins etc are my convictions. Concerns: Pledging of shares by promoters in recent past, oversupply of fiber. Delay in 5G implementation |

|

Aurobindo Pharma |

4.56 |

2nd largest Generics in USA after Sandoz acquisition, and within top 10 position in many European countries Company has got 500+ ANDA in US, started biosimilar trials, trying to enter china market, increase in oncology business, market share increase from recent acquisition (Sandoz, Apotex, Spectrum, Generics). Management expects to debt free by FY22. Concerns : USFDA regulations this is any way new normal for all pharma players |

|

KNR Construction |

4.56 |

Want to have a share in infra sector and this company has got best in class balance sheet among peers (excellent Working capital & debit to equity is around .2). Recent sell down of road projects to Cube is a big positive. Management is known for its execution capabilities and doesn’t want to aggressively go after growth Concerns : Slowdown from NHAI |

|

Federal Bank |

4.18 |

A Kerala based bank which is gradually increasing their market share. Consolidation of PSU banks helped them to gain market share in Kerala and getting traction in other southern states. ROE is increasing every quarter. Because of huge NRI deposits, no concern on capital Concerns: Inconsistency in performance, asset quality changes back & forth q-o-q. Planning to shift to ICICI bank or HDFC bank |

|

Godrej Agrovet |

3.41 |

Largest Palm oil producer and got animal feed and crop protection business. My bet is on Astec life science which will get merged with this company in future (earlier merger was called off). India imports 75000 crore of Palm oil every year. Recently India banned palm oil imports from Malaysia and currently drafting a bill to increase oil seed production to double Concern: Mainly a commodity kind of business, less margin |

|

GMR Infra |

2.19 |

A wealth destroyer in the past and not so worthy promoters (Pledging of shares). Then why this risk?? This is a contra bet because of the assets they got. Company will soon split into 2 companies with Airport and other business. GMR airport is I am interested in they got operational Delhi, Hyderabad and Cebu airports, under constructing Goa & Crete(Greece) airports. Both Delhi & Hyderabad airport has got huge land banks. GMR airport has got other strategic investors like Tata, GIC, SSG etc. Their Infra and power business is nothing to be mentioned. |