Understanding Market Coupling, IEX, and Why I’m Still Confidently Holding

Let’s decode what market coupling means for India’s power exchanges — and why I continue to hold IEX despite the noise. A thread for serious investors

- What is Market Coupling?

It’s a centralized regulatory mechanism — all buy/sell orders from various power exchanges (IEX, PXIL, HPX) are pooled, and trades are matched on the most efficient price.

The exchange offering the best rate clears the trade — not the one the user picks.

There is strong speculation in the market that coupling will help HPX & PXIL gain volumes without needing to fight IEX directly in pricing or liquidity.

- Round Robin Explained

Under the phased rollout (starting Jan 2026), exchanges will take turns acting as Market Coupling Operators (MCO) in a round-robin model.

While the exact frequency of the rotation (e.g., monthly, quarterly, etc.) hasn’t been explicitly detailed in the public information I have, the core idea is that the three power exchanges (IEX, PXIL, and HPX) will take turns acting as the MCO on a rotational basis. All trades during that time will go through that operator’s systems. It’s like IPL matches being hosted in different cities — to avoid monopoly and share infrastructure load.

Grid India (which is owned by the Government of India, under the Ministry of Power) will act as the backup & audit operator, ensuring fairness and neutrality — ensuring no manipulation, just like a referee in a match.

This is CERC’s way of avoiding monopolistic behavior.

- Is It Like showing BSE/NSE quotes on broker platforms like Zerodha ?

Not really. Zerodha gives you quote visibility, but you choose where to execute.

Under market coupling, you won’t know which exchange you’re routed through — the algo picks the best.

It’s like IRCTC auto-picking the best route instead of letting you choose the train.

Untill now, IEX was offering lower pricing, due factors discussed in Point 4 below.

- If PXIL Couldn’t Dent IEX for 17 Yrs (HPX for 3 years), Why Now?

Exactly. PXIL (launched Oct 2008) and HPX (Jul 2022) haven’t gained ground against IEX (launched Jun 2008) because of IEX’s:

- First-mover advantage

- Superior tech infrastructure — near-zero downtime, fast execution

- User-friendly UI/UX — for both large buyers and smaller discoms

- Trust built through regulatory alignment + transparent pricing

- Network effect — as volumes built up, more participants joined for better discovery

So while market coupling levels the price playing field, it doesn’t eliminate platform differentiation — which still influences where participants choose to place their bids.

CERC’s order may change the way pricing is done, but it does not eliminate the need for strong, liquid, and trusted platforms. And in that race, IEX is still miles ahead

So yes, the platform strength, consistent reliability, and reputation as the “default” choice created a self-reinforcing loop of trust → liquidity → deeper discovery → more trust.

That’s hard to replicate overnight.

- The Real Challenge of Market Coupling

Yes, price discovery becomes centralized.

But platforms still matter — for infra, execution speed, dispute resolution, etc.

IEX has years of reputation, infra maturity, and trust. That edge doesn’t vanish overnight.

Think Zerodha vs others — same price, different user experience.

- Why I Invested in IEX in the First Place

- India’s exchange-based power trading is just 6–7%, which was just 4% in 2021 (vs >50% in developed nations)

- Massive energy tailwinds: Data Centers, AI, EVs, Residential demand

- Government push for market based energy pricing from traditional PPA.

- Innovation: IGX (Gas), Carbon Exchange, Derivatives

- Clean balance sheet & high ROE

- A dominant operational moat built over time

- Why did IEX divest portion of IGX’s Stakes — Is it a Red Flag

In 2022, IEX sold 4.93% in IGX to IOC, bringing in strategic sector expertise to bring IOC as a strategic partner, drive gas market growth, share risk and capabilities

Strategic motive of IOC behind joining IGX was to become a partner with sector expertise—from LNG terminals to CGD networks—supporting gas market growth and aligning with the government’s push to raise gas in India’s energy mix to 15% by 2030.

This aligns with other strategic investors such as NSE, GAIL, ONGC, Torrent Gas, Adani Total Gas—creating a consortium backing IGX’s scale-up. IEX’s leadership in gas trading moves from being a pure owner to a strategic partner, sharing risk and expanding legitimacy across regulatory and distribution networks. (Source: IEX divests 4.93% equity stake in arm IGX to Indian Oil | Company Business News)

As a result, IEX holds ~47.28% stake; IGX now equity-accounted (not consolidated) as an Associate In essence, IEX pivoted from owning IGX outright to forming a broader gas-exchange ecosystem with other large investors. This was a deliberate, strategic move—not regulatory pressure or retreat—and positions IGX for scale in India’s evolving gas economy.

Strategic partnership ≠ weakness.

- If CERC’s own report said there is no benefit, why implement it?

The 2022 report submitted to CERC clearly stated “no proven cost advantage” to consumers.

However, there could be political pressure for fair access to new exchanges, push for de-monopolization of IEX, and Global alignment with European-style market mechanisms.

Whether it helps the market or not — we may only know after implementation.

- Demand Explosion Ahead

India’s power demand is on the verge of an inflection:

- AI already eats up 4% of global electricity

- Semiconductors = power guzzlers

- Data Centers: 1.4 GW → 9 GW by 2030

- Inter-region power transmission lines: 119 GW in FY25 to 168 GW in FY32

- EVs = consistent grid demand

- Rising residential power usage: Even Tier 2/3 AC demand rising fast. AC is now a necessity, not luxury.

All this needs real-time price discovery, transparent allocation, and efficient balancing — and that’s exactly what power exchanges enable.

No serious digital or industrial ambition can succeed without vibrant, market-based electricity systems.

IEX may face cycles. It may get regulated.

But it won’t become irrelevant. So no, I’m not blindly holding — I’m betting on the pulse of a growing economy.

- No Promoters = Bad? Think Again

Some worry about high public holding, and infact it can be a red flag in some cases.

But in IEX’s case, we should respect clean, well-governed business models that run efficiently without a promoter. It’s not retail sentiment driving the core here — it’s FIIs and DIIs taking calculated long-term bets. That speaks volumes about the quality of the business, management, and moat. Ownership patterns alone don’t define risk.

The absence of promoters isn’t a flaw — it’s a design choice. Let’s not forget:

- Zero debt

-

80% margins

- Monopoly-like grip (till now)

- Strong institutional faith: Public holding only becomes a problem when the business doesn’t have institutional conviction — that’s not the case here. the numbers speak louder than opinions

- Strong regulatory tailwinds in the long run

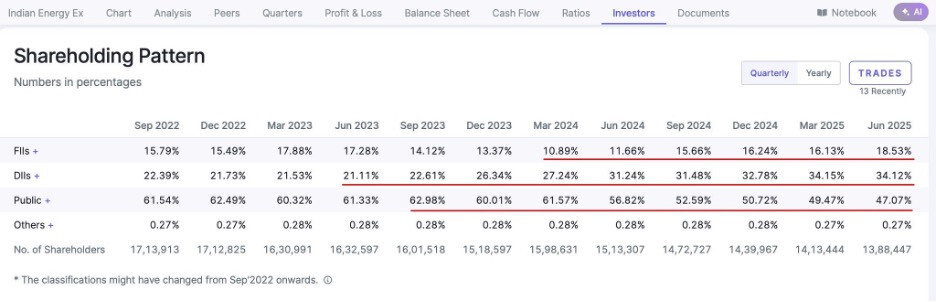

In fact, here’s how shareholding changed (Sep 2022 → Jun 2025):

DII: 22.39% → 34.12%

FII: 15.79% → 18.53%

Public: 61.54% → 47.07%

Attached the trend from http://screener.in

That’s institutional validation in action. While the retail crowd exits fearing uncertainty, the real smart money is quietly accumulating.

- My Take on Market Coupling

IEX may face short-term regulatory headwinds.

But its liquidity moat, infra strength, brand equity, and innovation pipeline remain unmatched.

As coupling clarifies, IEX may gain even more trust as the market matures.

It’s not just a price discovery engine.

It’s the plumbing of India’s digital & industrial growth.

- Final Word

I’m not blind to risk.

But when you’re betting on the system’s core infrastructure — energy rails of a fast-growing economy — you don’t exit at the first sign of change.

You track, learn, position, and ride the maturity curve.

IEX is one of my highest conviction long-term holdings. Period.

Would love to hear your views — agree, disagree, or add to the thesis. DMs open.

Disclaimer: These are purely my personal viewpoints, not investment recommendations. I am not a SEBI-registered Research Analyst (RA). Please do your own independent and thorough research or consult a qualified financial advisor before making any investment decisions. This content is shared for educational and knowledge-sharing purposes only.