I have been recently introduced to this community, I used to think that Reddit was a blackhole of investment wisdom and was very happy with reading threads on investments/equities. This community has blown away my mind and the pride that I hold concerning the knowledge I hold on investment instruments.

My Investment Journey (so far):

I started investing during the COVID lockdown and started learning about the Indian equity market. I initially invested in these mutual funds without a clear goal and bought units randomly:

UTI Nifty 50 Index Fund (inspired by John Bogle’s passive investing philosophy)

UTI Nifty Next 50 Index Fund (inspired by John Bogle’s passive investing philosophy)

Zerodha Nifty LargeMidcap 250 Index Fund (Saw this NFO from Zerodha and applied it as I was, I already interested in index funds and also like what Nithin/Nikhil from Zerodha are doing)

Quant Active Fund (impressed by their VLRT approach)

Ethical Fund (initially interested in ethical investing, but no longer contributing)

Rethinking My Portfolio:

After some reflection and further research, I realized my portfolio lacked direction. However, with a recent increase in income and savings, I’m ready to make some changes!

New SIP Plan (Equity Only):

Monthly SIP of ₹1,00,000 allocated as follows:

I removed the Zerodha Midcap and Largecap fund as it heavily overlaps with UTI Nifty twin index funds.

UTI Nifty 50 Index Fund (20%)

UTI Nifty Next 50 Index Fund (20%)

Quant Small Cap Fund (20%) (added for exposure to small caps)

Quant Active Fund (20%)

Parag Parikh Flexi Cap Fund (20%) (added for long-term growth/value)

Additional Notes:

I already have PPF, Sukanya Samriddhi Yojana, SGB, physical gold, and a savings fund for my debt allocation.

Looking for Your Expertise:

I’d greatly appreciate any feedback or suggestions on my revised portfolio. Does it make sense for my long-term investment goals? Should I consider adding or removing any funds?

What are these? This is the first step, which can be used as a base, on which a MF PF can be built. One can invest without any too, but if they are defined, then it will help.

Even without anyone’s help, your overall investments look robust, covering debt, equity and gold.

@ChaitanyaC Thanks for taking a look at my post. The overall investment goal of Equity MF is to build wealth to take care of long-term goals like (Children’s graduation , children’s marriage, and Post-retirement activities )

for short-term goals like( schooling, travel etc I am maintaining debt funds and emergency fund)

Right. Then you can think of a corpus number, have a return expectation, choose funds based on the return expectation and the time you have for the goals, and invest accordingly, also keeping in mind that linear returns are not guaranteed.

Not to mention that, as your knowledge and experience grows with time, you may want to change how you invest, where you invest. So today’s investments are not permanent.

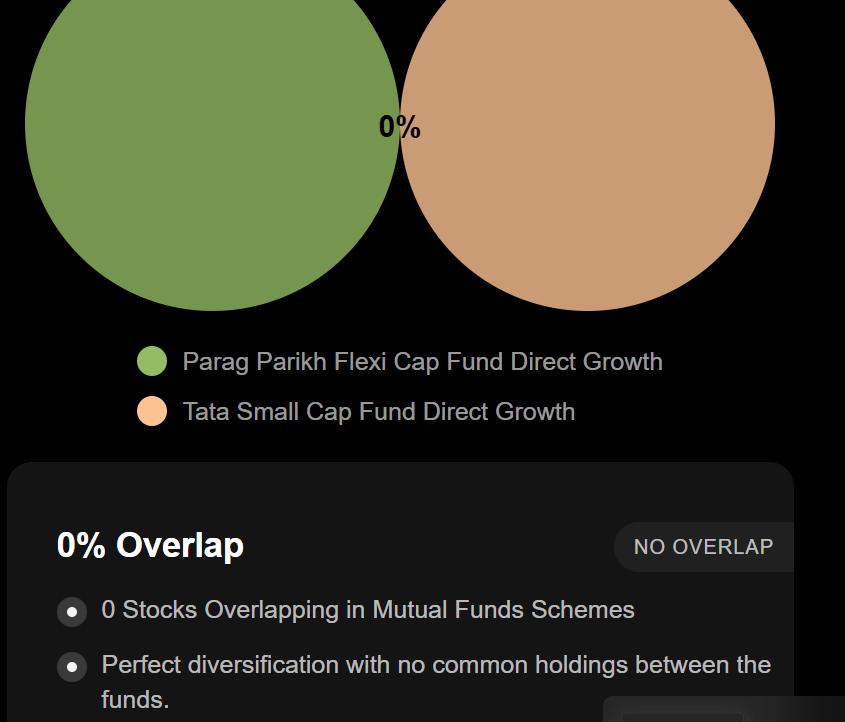

Can you explain your logic to add both these funds. These funds have same fund manager and most of their portfolio stocks are same. Isn’t it better to go for another flexicap fund instead?

I wanted to have exposure to Multicap fund - hence Quant active fund( Nifty500 Multicap 50:25:25 - TRI)

Small-cap fund is to have specific exposure to small-cap funds.- Hence Quant small cap fund (TRINifty Smallcap 250 - TRI)

the logic is Active fund also invest in Small cap companies but there is a limitation (25-50% only) where as Small-cap fund can invest in small-cap companies (65-100%).

can you please elaborate on this statement, as per my understanding there can be an overlap of a few companies but it can’t be like 100% of stocks are the same.

Please correct me if my understanding is wrong, I am open to learning and correcting.

I have been investing in MF for past 8 years now. The understanding about the MF investing has evolved during this time.

From regular MFs to Direct MFs.

From multiple # of MFs to a very few MFs.

From large cap MFs to index funds.

From funds with overlapping stocks to less overlapping.

From funds under one AMC to different AMCs.

Here is my current MF investment philosophy, it might/might not change again

Value fund : I decided to go with Parag Parikh Flexi cap

Growth fund : Small + Mid cap : SBI small cap and Axis mid cap

Momentum fund : Quant Momentum fund

Index fund : I decided to go with UTI nifty next 50 instead of going with Nifty index fund because the % of overlap between PPFAS and Nifty 50 was higher compared to nifty next50.

Few basic principles that I follow

I avoid theme or sector based MFs.

I also avoid investing from third party brokerage sites like Coin, Groww.

On days and months like June 4 , 2024 or March 2020, I invest the through lumpsum before 2 PM.

I am still learning. I hardly sell (I lack the skill of selling)

Any specific reason for this? I find it convinient to invest on Coin since I have DMAT account with Zerodha. I can track all my Investments in single window instead of visiting different websites of Fundhouses.

I have UTI nifty 50 index and nifty next 50 index fund in my portfolio. I have also bought Zerodha Large Midacap 250 fund at NFO. As far as I know, there is a huge overlap between Nifty twin index funds and Zerodha Large cap mid cap 250 funds.

I have UTI next 50 – current XIRR is 37.22 %

UTI 50 - - current XIRR is 24.15%

Zerodha LM 250 - new folio is currently at 14.69% absolute returns.

Per my research and understanding, I am stopping SIP in Nifty 50 and Nifty next 50 and continuing SIP in the Zerodha LM 250 index fund.

what do you think about this? any comments /suggestions.

Yes, your understanding is correct. These funds have around 40% overlap only and individual stock weightage differs as well.

What I meant is, when the fund manager is same, their thought process of investing will be same across the funds they manage (regardless of the Benchmark Index of the fund). Even with the restriction on Multicap fund to invest only 25-50% in small cap, they can still choose their best investment from their small cap fund and use that for the Multicap fund.

Hence isn’t it better to go for different fund managed by different manager? The reason I am asking is that I have Quant active fund and planning on adding one more fund from either small cap (Quant Small Cap) or Flexi cap category (Helios Flexi Cap).

You’re right. While that’s true about NAV allotment, does it really matter for long-term investments (more than 5 years)?

In my opinion, for such long time horizons, the NAV allotment on specific days (T+1, T+2) becomes less significant.

If your goal is to capitalize on lower prices, then ETFs are a great option, especially for broad market indexes like Nifty 50 or Next 50. They allow you to benefit from market downturns, but you do need to stay somewhat attuned to market movements.

For Groww site, I observed, if I place the order before 11 or 12 pm, I will get same day NAV allotted.

Good discussion, so adding my perspectives in general about SIP’s. Been doing SIP’s since 10 years, though increased the weightage of flow into SIP’s (vs direct equity) since 2020. Core idea behind SIP’ is its gives you the discipline and eliminates all the biases about market movements. To build a corpus and to continue your saving journey, SIP helps you immensely.

Though I started with few Small caps, value funds and blue chip, later I realized, since maintaining a direct equity investment/demat, its better to go with index funds and ensuring general market returns on my SIP’s. So tilted a bit towards Nifty 50 and next 50, along Balance advantage fund to ensure stability of PF. The following are few points I found over the years, and I am still learning.

Nifty 50 Index fund from ICICI was doing well for 4-5 yrs, but recently I found that its better to go with Factor funds with an index like Momentum/ Value, Low Volatility etc. So gradually shifted to Mom 30 and Low vol (out of 100/200).

Few thematic fund like PHD, (Pharma, health, diagnostics) started prior to COVID, and still continuing. Pharma as a sector, not an easy segment to invest directly. Although I do have exposure to few pharma/hospital stocks, after 5-7 yrs, what I realized is we do miss a lot of good investment stories here. I believe, India has a lot of space/segments (within PHD) here to grow, and will continue to expand the global market share as a supplier of critical medicines. Maintains a specific annual increment in SIP here.

US fund has been doing since 7-8 years, so continue to it, though didn’t want to increase the annual SIP. The idea is to maintain at least 3-5% of overall PF exposure into US blue chip funds.

Started a china fund, a year back as a bottom fishing idea… considering cheap valuation and thought the bottom is around… Here, am not expecting much as the % overall PF and SIP is too low to do any bit to total PF. The idea is to keep track of global-china movement, and continue with a small allocation (5-7 yr view) and if required, move out once the valuation is in favor.

India Technology fund was started 2 yrs back, when the IT sector started to hit bottoms. Here too, similar to pharma segment, its one of the key GDP contributor to India and should do well over the next decade. So a thematic fund was a go to option for me.

Has a Focused fund and Quant fund (focused), both contributes to around 10% of overall PF. Here too, idea is to continue watch the performance closely, and to evaluate over 5-7 yrs.

Criteria for choosing the fund is the fund size (liquidity), churn ratio (mind set), expense ratio and fund house/manager credibility.

Some of the funds have few overlaps, though not at exceeding levels.

Booking/selling is to the minimum. Though I do try to trim a bit from index funds, Debt funds if the market seems to show froth and corrections are due…, and normally it helps me to maintain the 5-10% cash requirement in direct equity investments (where mostly into small/mid caps).

Nothing much more, will add further upon your comments and feedbacks.

Personally I am not in favour of small cap/midcap funds. Flexicap fund should take care of everything. Please take care of asset allocation as well. As the markets are volatile, it helps if you have excess cash to invest during turbulent times. You may consider investing in liquid/overnight funds and dynamic asset allocation funds

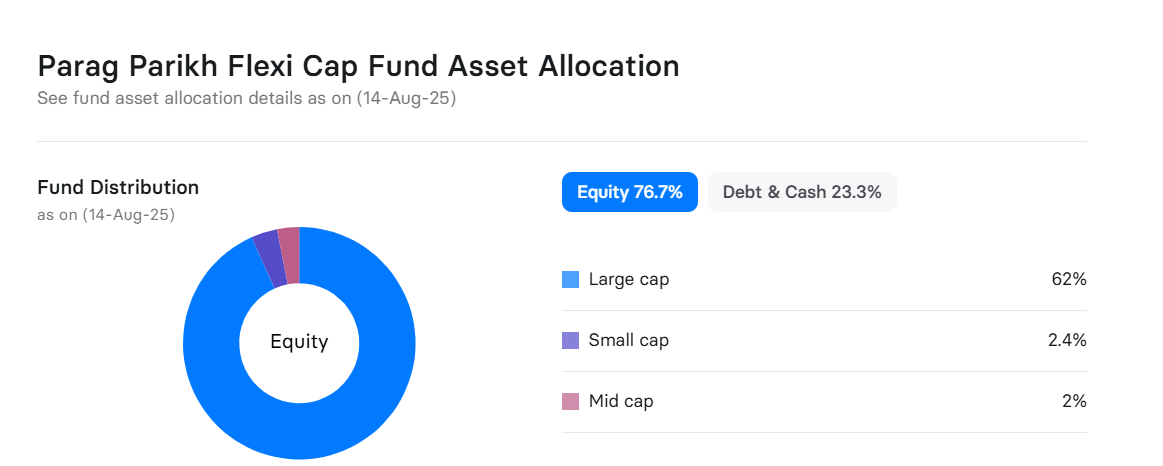

From the image, we can see they’ve invested only a small portion (around 2.5%, maybe up to 10% later) in small caps. But if you look at value small-cap funds, they usually allocate a much larger chunk (60%+), so the chances of higher returns are better—especially if we’re talking about a long horizon like 20+ years.