With a noble wish founded in April 1992, Muthoot Microfin Limited, a subsidiary of Muthoot Pappachan Group, provides micro-loans to female customers with a focus on rural regions in India. http://www.muthootmicrofin.com/

Pros:

Reliable and strong promoter group

Low retail holding, getting lower

Niche targetted group

Good CAGR, high OPM

CONS:

Low interest coverage ratio.

Want your takes on this NBFC.

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/others interested can look to edit the post in order to meet prescribed guidelines. We have the responsibility - especially the thread initiator (assumption is he/she is a savvy investor) - to cater to bringing everyone on same page - quickly - if you know what we mean.

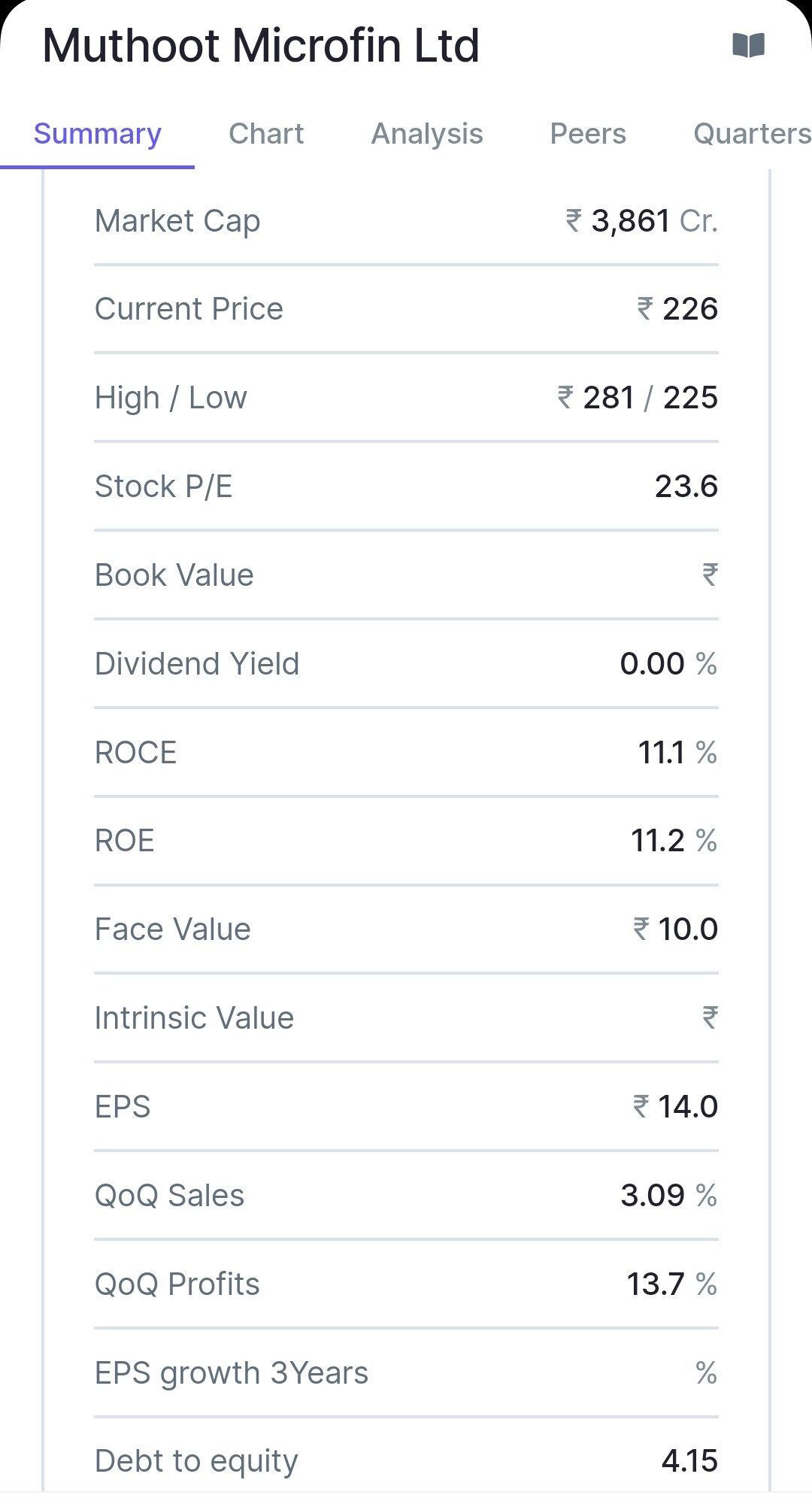

Net profit is one of the important indicators to show the financial health of the company. Net profit of Muthoot Microfin is Rs 163.89 Cr and the compounded growth of profit in the past 3 years is 108.02 %. The PAT margin of Muthoot Microfin is 11.47 %.

Muthoot Microfin, I feel has good growth story ahead, Here are my thoughts about it:

Last year they had 163 Cr Profit. This year they will clock close to 500 Cr.

Currently it is having a PE of 23 as per Screener, after they report annual results it will be close to 8, that will be dirt cheap.

Recently they got 750 Cr in IPO money which is not costing them anything. so considering any Microfin charges 22-23% interest, they are set to get additional 200 odd crores of profit.

They are expanding beyond Kerala and hopefully that growth will add additional headwinds.

Whatever i read about the group, looks like they are honest set of people.

Also, CEO is a professional and not from family which i feel is additonal plus.

Family holds good amount of holding, meaning skin in the game.

If i look at the other listed players, this stock should be going to around 20K crore market share easily in next few years.

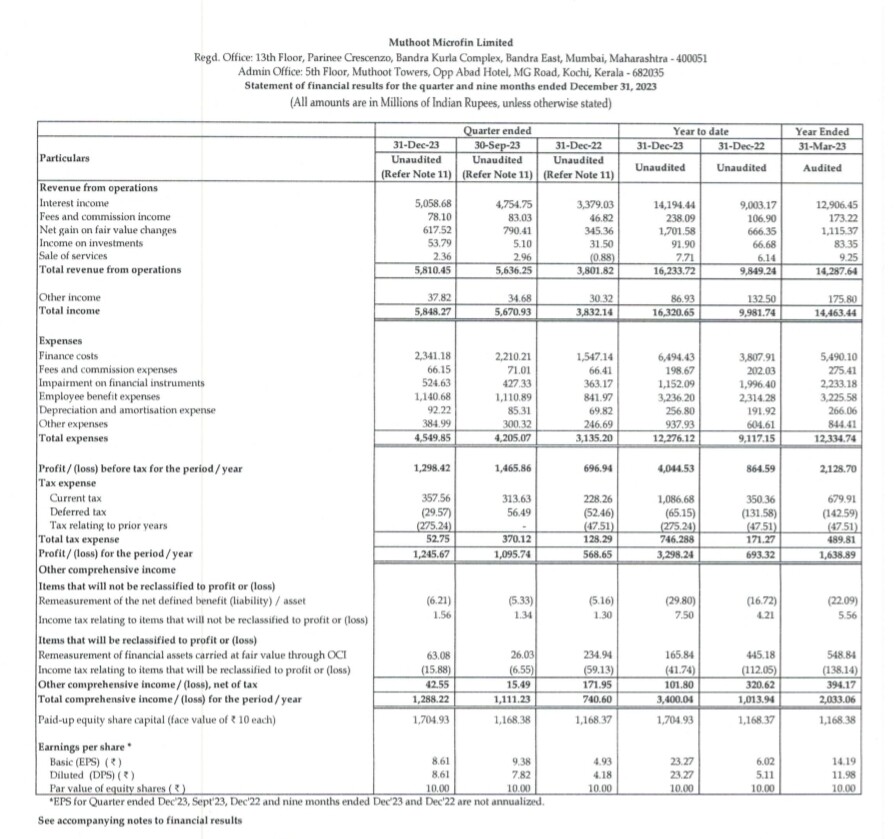

Company has delivered a very good quarter and Year with CAGR growth of 39% for last 3 years. For FY 25 as well they are aiming for similar growth. I think this will be great for us as a shareholder. I hope with opening so many new branches(335) they will be able to diversify themselves from TN and KL to other geographies as well!!

Hi, I am relatively new in this field and trying to learn things, I did research on muthoot group there are 3 companies I found muthoot finance, Muthoot microfin and muthoot capital services, I know this thread about Muthoot Microfin but I wanted to know what happened with Muthoot Capital services from 1200 to 290. I am not able to find any reason of it. They give bonus in 2017 but stock crashed in 2018. If someone knows anything which I didn’t get please let me know also provide the source if you found it.

Muthoot Finance is of different group. It is the better and popular group providing gold loan.

Muthoot capital and microfinance are part of Muthoot Pappachan Group.

Muthoot microfinance is providing small amount loans to groups and have higher risk than gold loan.

Muthoot capital services provides 2 wheeler and 4 wheeler loan and their business is dependent on auto cycle. Any downturn in auto market will reduce their business. It has shown irregular margins with no growth in the past.

I was afraid of fusion like results, over the past few days.

Due to election quarter.

But I think, results are fair.

Growth has tapered , but that’s in line with expections , management has stated in last concall only, they are expecting a subdued quarter due to elections.

Will know how market reacts to it,but I think results are more than fair, beating the expectations, if compared with peers.

Yes there will be times of cycles in economy , where consumers repayments aren’t being met, due to cyclicality with the individual sectors like agri distress or rural or urban economic distress, is when the npas of these lenders shoot up.

But if one looks over a period of time, that evens out.

If we look at the history, best value creators have either being consumer facing companies, or lending businesses.

That is the primary reason why I have invested 36% of my portfolio in Ugro Capital and Muthoot finance, Unfortunately, both of them are not performing for long time now. I still believe in my hypothesis, just waiting for the rate cycle to take downturn, hopefully 2-3 rate cuts this years may re-rate the these companies.