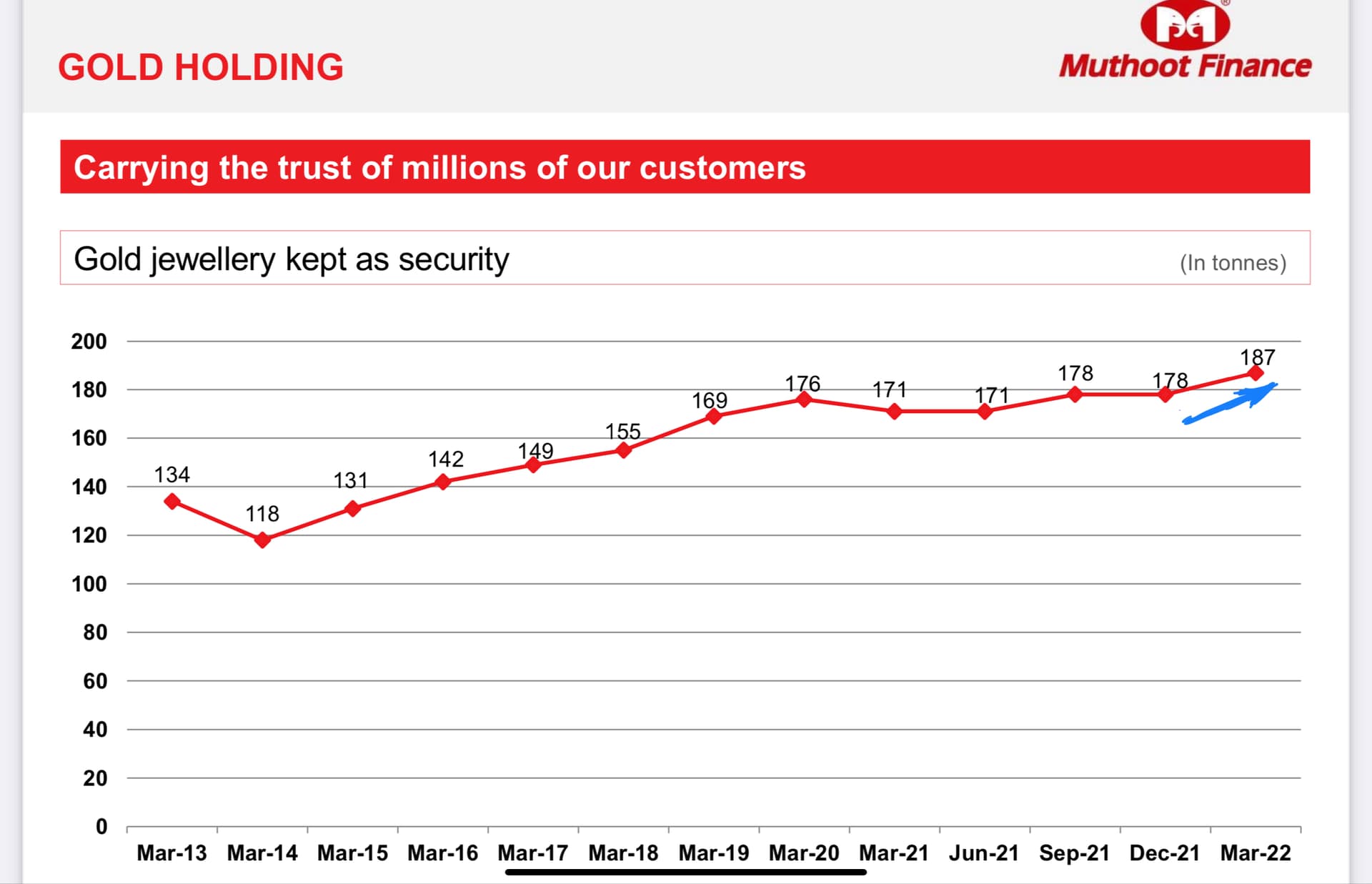

“Sixty per cent of its 5,000-odd branches are in Tier 3 and 4 cities, most of them in unbanked areas.”

the main reason is that the Gold prices were at an all-time high in July and Aug-20, which were early pandemic months. This contributed towards good growth in the gold loan category as a whole for the Co.

New advertisement from Muthoot:

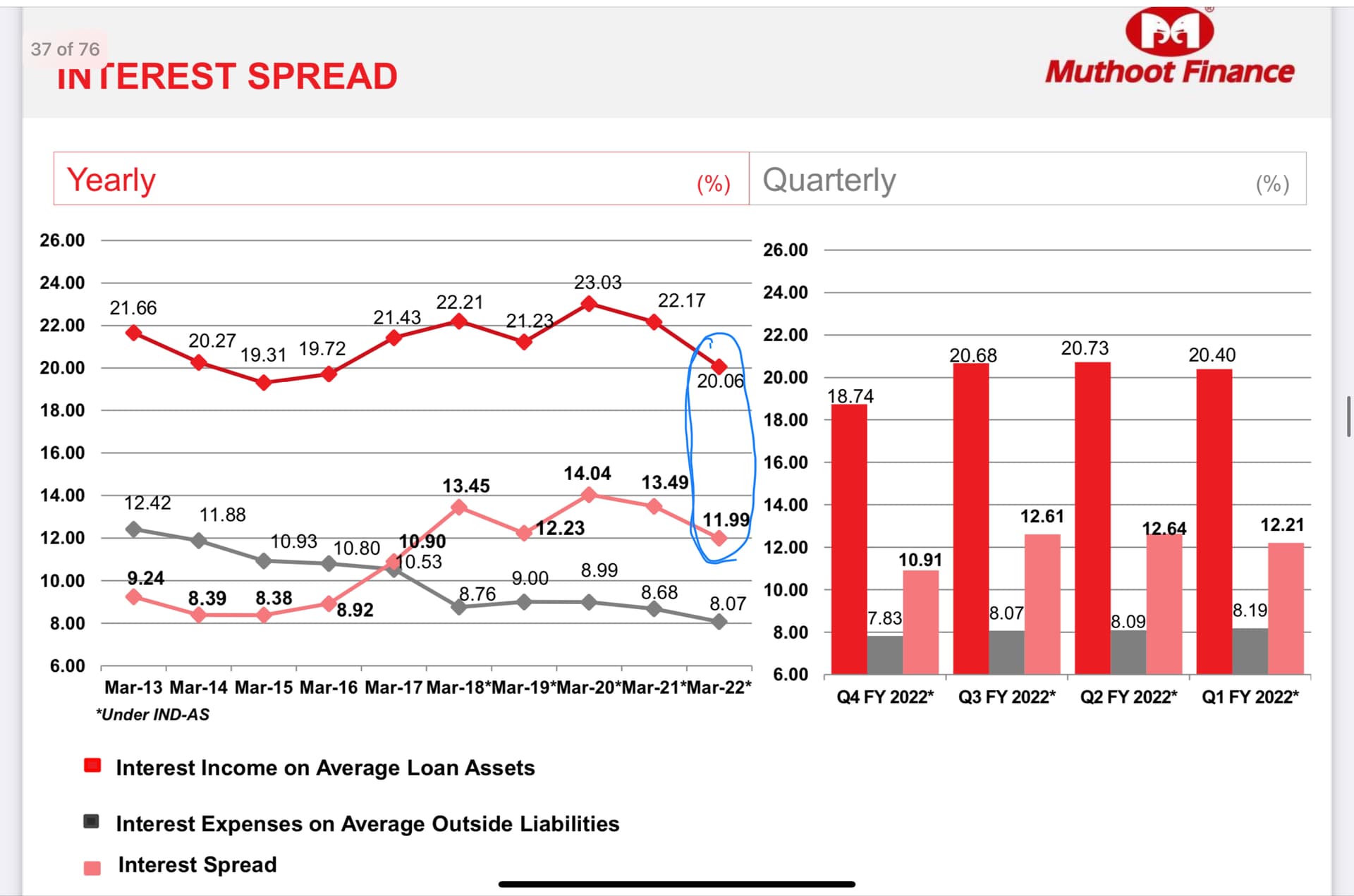

Q3FY22 concall notes

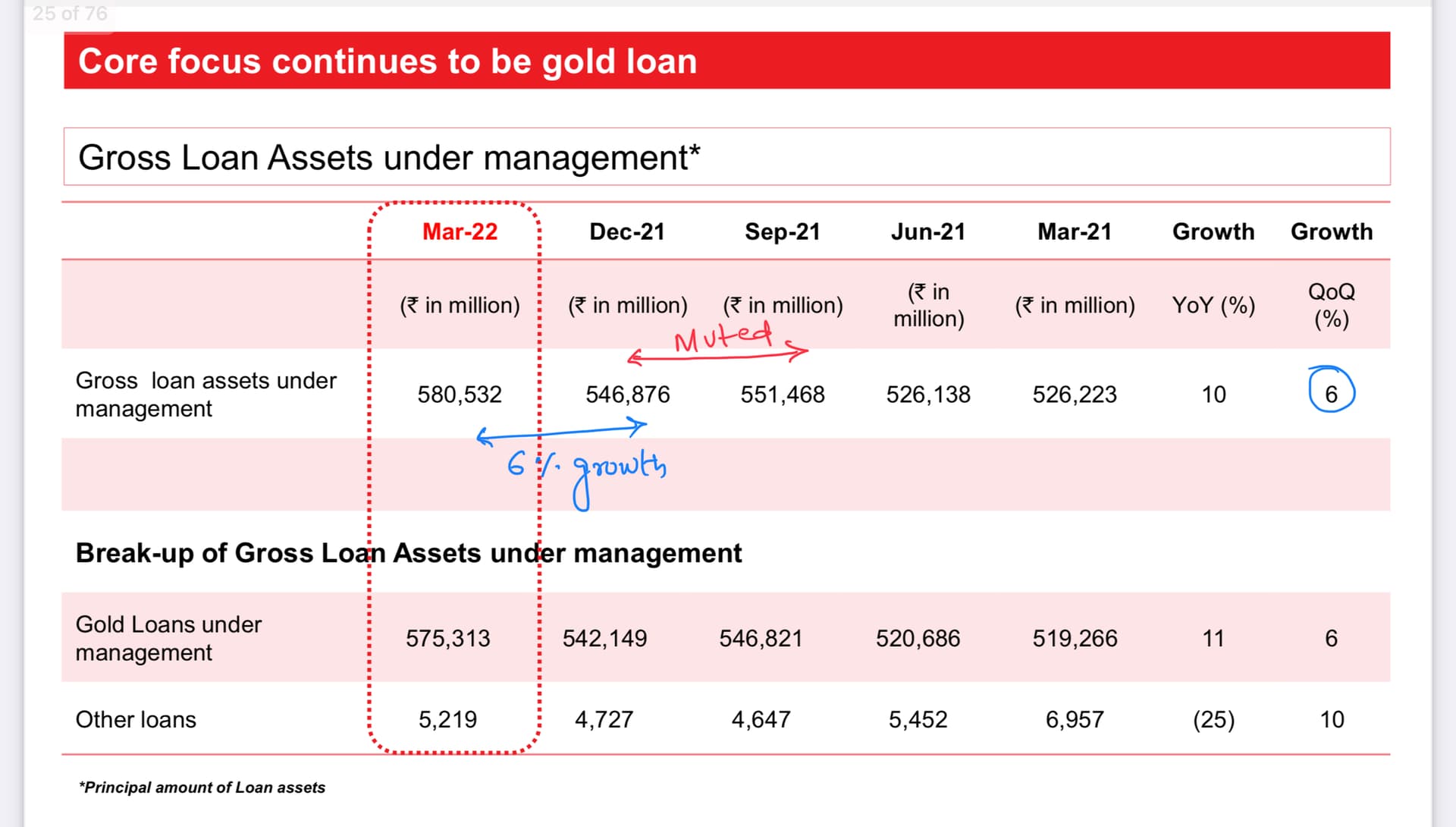

- Number were flat in this quarter.

- Q: Can rising interest rate affect Muthoot?

- Borrowing cost to go up by 50bps points in future, as the interest rate increases.

- Will try to cover that with different products.

- But if everywhere interest are increasing even they can increase their rates.

- Borrowing cost to go up by 50bps points in future, as the interest rate increases.

- For growth, economy recovery and advertisement will help.

- MFI approval received for equity infusion and going forward should do well.

- Auction: 2800cr (3.8%). Majority they took loans from Q2FY21. (Maximum 3 months period they allow after that they auction it)

- LTV come down this 69% as of December. Last Quarter 73%

- Guidance 12-15% for FY22. Management saying things are not fully in their hands. (They said growth will be there but difficult to achieve target.)

- Question from Digant Haria: How important is relationship management by employee with client?

- Sometimes competition takes their employee thinking it is about relationship but that is not the major driver. Brand, trust, turnaround time, and rates are a major driver.

- Added 3.5 lakhs this quarters but many customers closed their account so you can’t see net increase.

Latest research report from Motilal Oswal on Muthoot Finance. Has some interesting data points, back testing on certain aspects of gold price volatility and its impact and the technology interventions Muthoot is taking up to keep itself relevant to changing times:

http://ftp.motilaloswal.com/emailer/Research/MUTH-TP-20220302-MOSL-CU-PG020.pdf

One important point to note: LTV of 90% against gold loans for banks is ending on 31st Mar 2022. So from 1st April 2022, this should help reduce some competition from banks on LTV front. On the lower interest rate front the challenge will remain and will be test of Muthoot’s execution capabilities

Muthoot Finance RA.docx (25.7 KB)

Analysis of Muthoot Fiannce.

Helpful for new investors who want to invest in Muthoot Finance

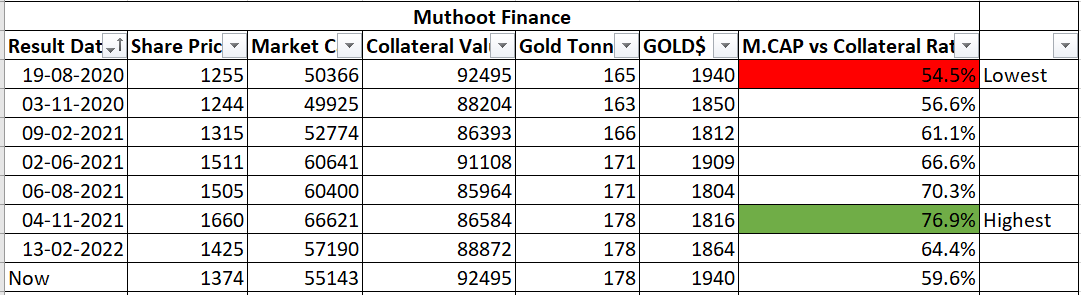

Muthoot Finance MCAP to Collateral Ratio since last 2 years

Commenting on the results, Mr. George Jacob Muthoot, Chairman stated, “Despite the ongoing geo-political crisis and covid related base challenges, Muthoot Finance has delivered a consistent performance in this quarter and was able to achieve a consolidated AUM of Rs.64,494crores, registering a growth of 11% YoY. We achieved landmark level of consolidated profit after tax of Rs.4031crs for FY 2022. As the economy is gradually recovering, the demand for gold loans has been steady and we remain optimistic for the coming financial year. Gold prices have been steadily rising over the last three years and this has attracted new customers towards the product and has positively helped the sector. With Indian Households owning the world’s biggest private stock of gold, and only about ten percent in the organized gold loan market space including gold loan companies, there is huge untapped opportunity in gold loan sector. We aim to keep innovating and maintain our leadership in the gold loan sector.

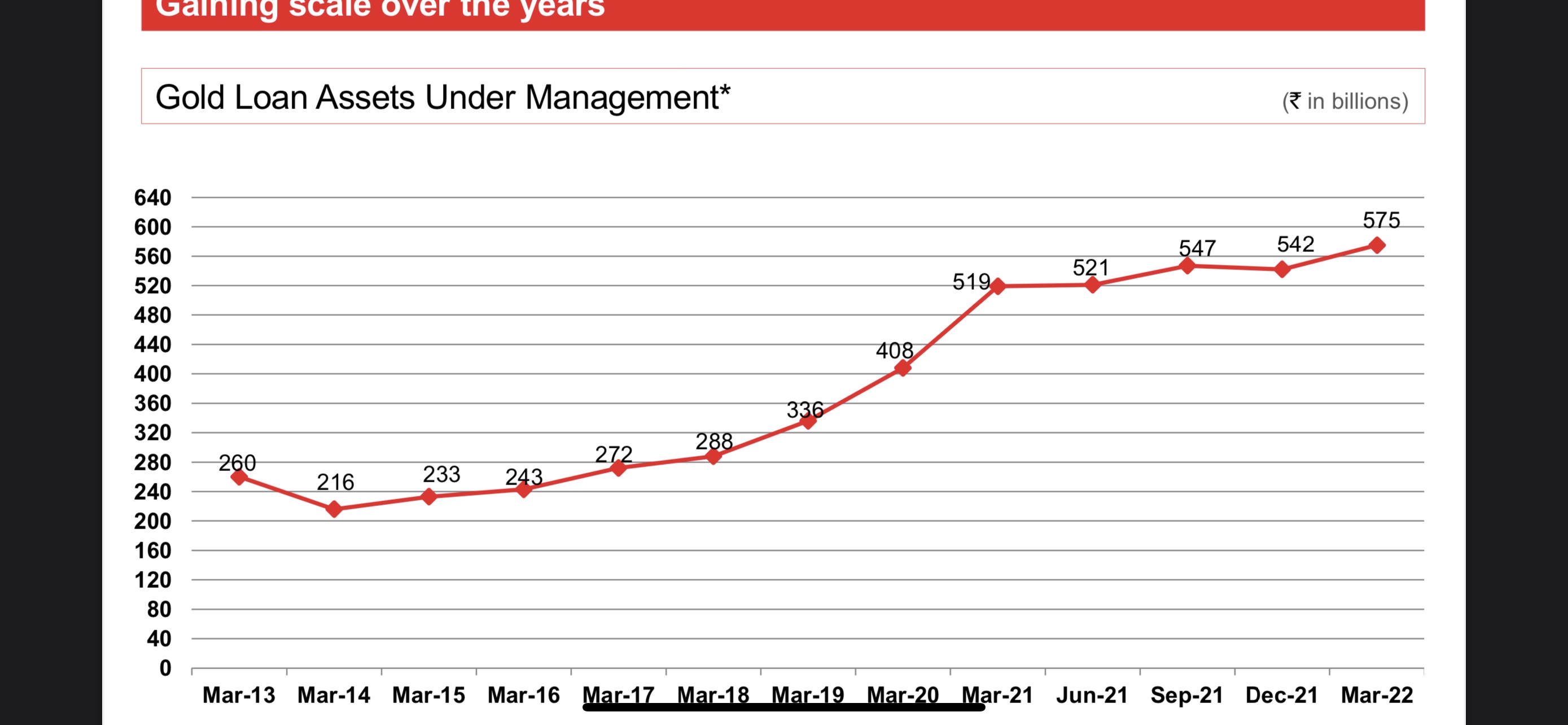

Mr. George Alexander Muthoot, Managing Director said, “Since we are witnessing signs of recovery in the economy, the RBI rate hike may not dampen overall demand scenario and we are expecting borrowing cost to go up gradually during the year. Gold loans are a great option both, in times of rise and drop in economic activities. As the economy recovers and overall economic demand revives, our focus will be to make the most of the opportunities and keep innovating further. Gold Loan AUM grew 11% during FY22 and we remain optimistic about a growth of 12-15% in Gold loan AUM for FY23 as well. The digital initiatives like AI-powered Voicebot platform enabling real time conversation with customers , launching of a new & improvised Muthoot WhatsApp experience and facilitating digital repayments through PayTM, PhonePe, Google Pay, WhatsApp etc. are enabling factors towards growth. We have recently also revamped our Gold Loan@Home services and plan to expand the service across 4600+ branches in India

Muthoot Finance is down by more than 30% from recent high…Business is doing good…still Its hammered. Even if overall market is down…but this is gold financing company with 70% loan to value ratio…What can be more safer than that? kindly throw some light on why such a treatment to a gem of a company?

I think it’s because of almost flat gold loan aum growth since last few quarters

Previously growth was strong

Once I economy picks up ,may be we will see uptick in growth

Slowly rural economy is picking up pace

Monsoon is coming and schools will reopen

Let’s see

I think there are 2 reasons behind this.

- Market thinks Muthoot will find lot of difficulties in AUM growth, as many private sector banks entered into gold loan. And on their lower base growth looks rosy.

- Becoz of this competition, yield will go down. This will reduce the profitability of company,Which is seen in this qtr.

However during Concall, management explained for higher growth they came with some offer for lower yield loan in last 5 months. This reduced the yield and going forward it will further moved up.

But spread guidance is 10% , which is much lower than present.

Thanks for this information. If you say that market thinks that due to competition, it would be difficult for further growth and lower margins…but then what stand an investor like me or you should take? what is the probability of market assessment coming out right? Should we add to the current position or just hold? If we accept the market perception, then where is the chance to get asymmetrical returns? Should we take contrarian view? and if yes, what are the grounds for that view? Kindly guide. This same confusion is there in many other good stocks too ( Divis labs, alkyl amines, laurus labs etc…where market has some view and I am not sure, if contrarian approach will be rigt or wrong)

Expectation was Muthoot to grow between 15-18% with 22-25% ROE’s but this year growth disappointed.

Further management guided conservative between 12 - 15 %.

Valuations is too cheap at 11.8x P/E and 2.49 Price to Book. So downside seems protected.

I think with big correction in many good stocks, it would be better to cut some from Muthoot ( reduce weight) and deploy where market provided good opportunity.

Can anyone share data on the market share of organized gold loan players including banks?