Lending is a commoditized business. A consumer will ALWAYS choose a gold loan at 7% from a bank vs same loan from an NBFC at 10%. The NBFCs can never compete with banks on pricing (lending rates). As the country develops, services of banks (particularly private banks) will catch up with well run NBFCs. This means NBFCs business model will slowly collapse and most of them will either vanish or merge with some bank. Muthoot or bajaj, each and every one of them will meet the same fate. RBIs decision to grant banking license through SFBs had further accelerated this process. I am heavily invested in pvt banks and have no investment in any NBFC. As a veteran investor, I will suggest the same to everyone.

5 Likes

Thank you, Sir. For making a post, and extending the word of caution.

I agree, lending is commoditized.

Lending also works on non-negotiable parameters like, say, repayment. The terms of repayment are very different for Muthoot vs Banks. Ticket size too. Therefore, they touch a different starta.

The management is citing slowdown in demand due to low need for working cap due to Covid.

I will let them play this card for another quarter or two.

In the meantime, I feel risk reward ratio is very attractive. No harm in giving it a shot

Yes, you’re on point and who doesn’t trust a veteran.

After all, India’s banking needs TAM is so small and we’re a developed nation.

Micro-finance, affordable finance, vehicle finance, housing finance, gold finance they are all same.

potato/ patato all same .

2 Likes

Was going through Equitas Small Finance Bank’s quarterly report. Their Yield on Assets is 17% and NIM 9%

Could their customers have gone to the lowest cost lender?

Their exposure is mainly to SME, Vehicle, Micro. Nothing that a HDFC Bank cannot service. Then why a sfb.

Reason: they finance a different starta.

Same for Muthoot.

This is the reason why I am holding fort. I believe Muthoot will make a massive turn around within a year’s time.

5 Likes

Does anyone know how Rupeek collects Interest payments from the customer or how does it provide any other service that is to be provided to the customers?

Because if Everytime they will be providing Door service then it will be operationally more costlier

I Belive Covid has gone for a long time, this is just a management excuse for slow growth

Good companies were growing even during Covid

We need to be Cautious rather than exhibiting Conservatism Bias

Disc: Invested with Low Allocation

Yes, but that is unsecured lending and If any bank would have to expand they would firstly target secured lending at Higher Yields that’s why Gold Finance NBFC’s are facing competition.

Sharing my deep dive into Muthoot vs Manappuram for the benefit of VP community here. :

I recently started looking at a business model that has been in existence since the past 100+ years and has shown consistent profitable growth since at least the last 10 years (that’s the period I have studied for this post) - it is that of Gold Loan financing. And there are 2 listed pure-play Gold loan financing companies in India (Muthoot Finance & Manappuram) which I have studied for this post.

Disclosure : I am invested in these companies so the views shared below are biased. Please do your own due diligence before investing.

First, let me briefly explain the framework I have used for this business-cum-stock analysis - it is called “QGLP” and is fantastically described by Mr. Raamdeo Agrawal of Motilal Oswal Securities in this note from Page 28 onwards (https://www.motilaloswal.com/site/rreports/637443115602580742.pdf). QGLP is short for Quality, Growth, Longevity & Price and these 4 factors together help decide whether a business is fit for investment or not.

Quality comes from Return on Equity being higher than Cost of Capital and the business being able to reinvest its earnings at the same or higher RoE. Business should be run by able management as well.

Growth in Earnings or Book Value Per share and Free Cash Flow.

Longevity i.e. there should be a long runway of quality growth ahead for the company.

Price i.e. the valuation that Mr. Market is assigning to the business at the moment and whether that valuation is cheaper than quality and growth metrics of the business warrant.

Why is Gold Loans a Quality business?

- Short tenure (6 months) & secured Loans with highly liquid collateral (Gold Loan companies auction off the borrowers’ gold in case they don’t pay for 3 months)

- 20% yield (significantly higher than the Cost of funds) resulting in double digit NIMs (in the range of 10-12%)

Exhibit 1: Muthoot Yield, CoF, NIMs (Manappuram NIMs are in the same range)

- Both point 1 & 2 above translate into high (20%+) Return on Equity and 6% Return on Assets (there have been 2 periods in which RoE and RoA declined - first, during 2012-14 when adverse regulations were introduced by RBI, and second, post-COVID when competition from banks intensified)

Exhibit 2: RoE and RoA trend

- 60-70% Loan to Value (LTV) ratio helps cushion against decline in Gold price

- Barriers to entry - Banks find it difficult to compete with specialised Gold Loan NBFCs because the business is operationally intensive - valuation, safekeeping & auctioning of gold on a large scale requires a specialised focus which banks and diversified NBFCs find challenging to build.

- Unorganised to Organised shift in market share - Traditionally local moneylenders have exploited borrowers with very high interest rates and no safety of Gold kept with them. Branded players offer safety, reasonable interest rates, flexible payment options and digital convenience that local moneylenders can’t match.

- Low Non Performing Assets (NPAs) - default rates are low because Indians are emotionally attached to their jewellery.

- Doesn’t need external equity capital to grow because of high RoEs so existing equity shareholders are not diluted; internally generated funds & borrowings are sufficient to fund growth and both these companies pay handsome dividends as well because of strong Free cash flow generation.

Quality of Management - Although this is purely a judgement based factor, one way to judge the quality of management is to look at how well it responds to threats to its business. During 2012-14, India’s central Bank RBI introduced stricter regulations to curb supernormal Gold Loan growth and global Gold prices tanked because of Fed’s taper tantrum. Stock prices of both these companies nosedived.

Exhibit 3: Regulations introduced by RBI (Source: IDBI capital research report)

After this episode, management of both GL companies decided to de-risk their Gold dependency by diversifying into other products like Microfinance Loans, Home Loans, Vehicle loans etc.

Exhibit 4: Diversification journey post 2014

Management of both GL companies has also tried to improve operational performance by

- increasing Gold Loan AUM per branch, and

- lowering Opex to AUM %age

Muthoot is much better than Manappuram on operational front.

Exhibit 5: Operational performance metrics

Growth

Gold Loan Assets Under Management (AUM) growth is driven by 2 factors:

- Gold price which has grown at a CAGR of 6.6% pa over the last 10 years broadly in line with inflation in India.

- Volume growth (Gold in tons) which is in the range of 3.5-4% pa over the last 10 years

Exhibit 6: Volume growth

Both these factors combined have helped deliver 8-9% growth in Gold Loan AUM in the last 10 years.

Exhibit 7: Gold AUM growth linked to Gold price growth

Exhibit 8: Book Value per share has grown in double digit CAGR in last 10 years

Longevity

- Needless to say, Indians love their Gold. Gold demand by Indians based on World Gold Council numbers is steady over the last 10 years and as per estimates, 40% Gold stock is concentrated in South India where both the pure-play GL companies are based.

Exhibit 9: Gold demand in India as a %age of Global Gold demand is ~20% making India one of the biggest consumers of Gold apart from China

- Plus, the penetration of Gold loans as a %age of Gold stock in India is very low at around 4-5%.

- Another factor is share of the Organised sector in Gold Loans is still low but growing. Most of the branches of these 2 companies is in Tier 2 and Tier 3 cities i.e. rural India which makes up bulk of our unbanked population, and where people still invest in Gold, and people don’t have proper documentation to avail a loan from a bank in case of need.

Price

Price to Book ratio is the most relevant valuation metric for finance companies.

Manappuram P/B is at 10 year low maybe because the market is spooked by rising competition from banks and other NBFCs! (Source: screener.in)

Muthoot P/B is close to its median over last 10 years due to similar fears

Muthoot vs Manappuram: Muthoot is more richly valued (P/B of 2x) vs Manappuram (P/B of 1x) but that premium might be justified because of several comparative metrics we have seen above; Muthoot is better than Manappuram in terms of:

- GL AUM growth, BVPS growth

- Operational performance,

- RoE, RoA

- Leveraging scale (per branch GL AUM is growing faster for Muthoot coz of greater focus vs Manappuram which is focused on growing other products)

- Lower diversification (helps Muthoot coz gold loan yields are higher vs other products into which both these companies are diversifying)

- Muthoot’s management has a greater stake in success of the business (73% of INR 400Bn) vs Manappuram’s management (32% of INR 80Bn)

What are the key risks in this business?

- People shifting their investments from Physical Gold to “Digital Gold” - this risk is a bit muted because Physical Gold serves a bigger purpose (like jewellery) than pure investment instrument and people with cash income have limited avenues to invest through regular banking channels.

- Regulatory risks in terms of LTV, capital requirements etc which impacts AUM growth

- Banks/other NBFCs offering Gold Loans at a lower interest rates to grab market share (though 2 banks - CSB and SBI - who have aggressively built their GL book during COVID are reeling now with high NPAs)

- GLs are short term loans so GL companies have to constantly hunt for new customers as old loans get repaid. This creates an operational challenge.

- Risk of fraud/theft, employee strikes, flooding in key states which ruins crops and disrupts business activity.

- Govt hiking import duty on Gold like it did in Jul’22 from 10% to 15% on the back of all time high Gold imports. This makes Gold bit more expensive and dampens demand.

- The required cultural mindset shift which is required to grow GL penetration from 4-5% might never happen (as people are reluctant to pawn their Gold as it’s considered a sign of respect and is attached to people’s emotions).

14 Likes

Nice analysis

Good job

- Longetivity and intense competition in the near term is the major fear raised by many and hence the cheap valuation

Only time will tell the answer .Downside looks limited while upside has no limit - Manappuram with 3% dividend trading at 1x book value has edge over muthoot

1 Like

- Muthoot Finance rating update: Rating update

On lines of my expectations

1 Like

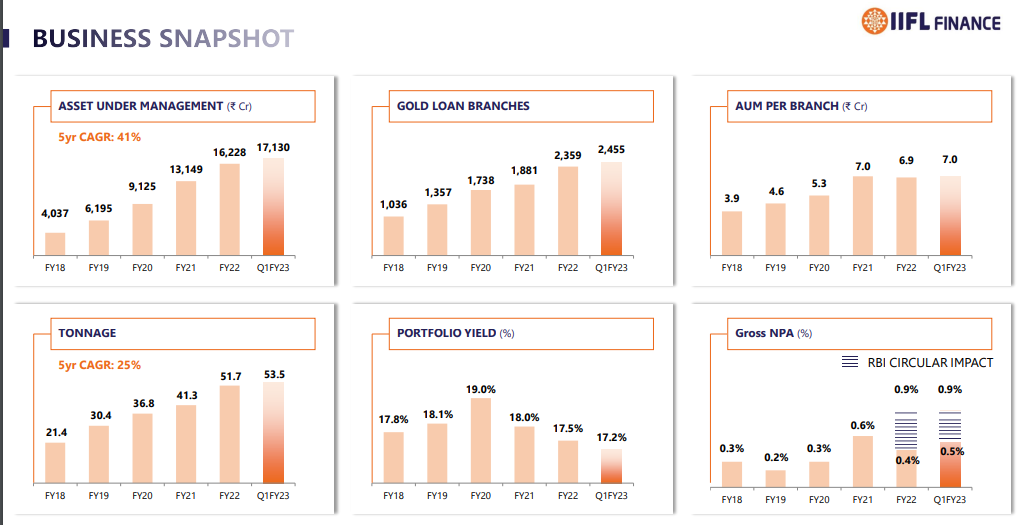

good progress by IIFL in Gold loan segment. shaping up to be a serious competitor to Muthoot & Manappuram in urban space

1 Like

1 Like

1 Like

Alleged major fraud done by Muthoot finance in Kerala. Took money from customers promising to invest in Muthoot Finance NCDs and in turn invested in SREI Equipment NCDs. Now SREI is under liquidation and Muthoot is saying that the money invested is waiting RBI action and has completely given up on the investors. People were fooled under the pretense of investing in Muthoot Finance and was cheated. Lot of people, were cheated of their life time savings.

Video is in Malayalam.

3 Likes

Who has done the fraud? Is it a few employees at a particular branch? Also strange that the investors didn’t realise till now. Srei had been in trouble since a long time.

The fraud has happened at many branches and I think the higher management knows about this. Most people were told that money will be used to book Muthoot NCDs and without their consent, SREI NCDs were booked. When questioned, Muthoot branch officials said investing in SREI is the same as investing in Muthoot and nothing will happen to the money. Issue started last year, when they stopped getting the interest. Senior management have asked time till Jan mid to try to resolve the issue, with the customers.

6 Likes

Muthoot finance results are out https://cdn.muthootfinance.com/sites/default/files/pdf/MFINQ3FY23investorpresentation.pdf

I get the valuations are cheap and the fear of competition from banks might be already priced in. But what I can’t understand is why the growth is not showing up even after 3 years of Covid. Because historically, this competition between banks and gold loan companies is a little bit cyclical. During slow times, banks aggressively pursue GLs. GL companies can’t compete due to higher rates but then in some time, banks go about their usual business and GL companies come back. Is it different this time around? From what I understand, the management of either of the GL companies is not really admitting to this bad growth.

But at the same time, I also believe if banks could take away the business of GL companies they would have done so 3 years back, or 5 years back, or 7 years back.

Also, not sure about this but I think 2point2 capital (which was a huge proponent of GL business, at least as per their past research blogs) has exited its Muthoot position (of nearly 9-10%).

Another perspective is that the target customer of GL’s is a particular segment of around 50k-5l, which has not seen a sharp recovery post covid. So as and when the recovery is more broad based we can see some growth.

Would love to know your views.

Biased since invested

The target segment of low ticket gold loans have not recovered. Both Muthoot and Manappuram are now diversifying to segments outside of gold loans which to my mind is a good thing. Manappuram is already delivering good numbers on the microfinance business. Management has the track record and intent to improve their business footprint. Muthoot is also adding more branches. Most of the negatives are in the price and one will need to wait it out. Invested and hence biased.

also gold loan companies are very cyclical with gold price. trends show that time of outperformance is near -probably 2-3 q away