**Music Labels**

**The Most Profitable Internet Business and an Emerging Asset Class**

December 26, 2020

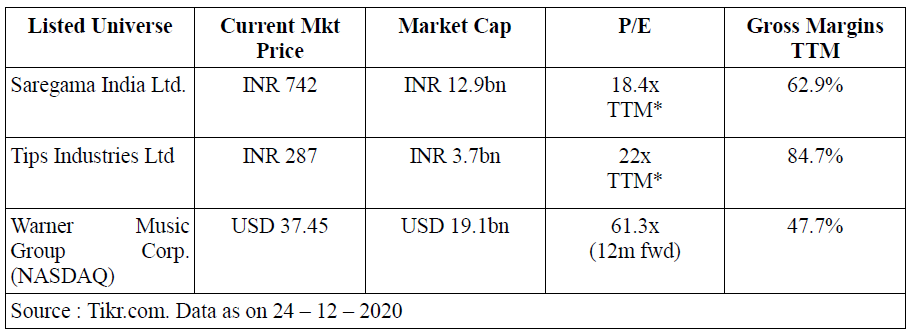

*Notes : * The Indian companies are not under research coverage and hence the database provides TTM numbers only. It must be noted that TTM numbers include atleast 2 quarters impacted by Covid -19 related lockdown. *

Given news paper reports of high growth in content consumption, and recovery in ad-spends in during Q3FY21, SIL and Tips may be trading at substantially lower PE multiples on FY21 basis. Forthcoming quarterly results will be the litmus test.

Background :

The Music Industry is conspicuous largely by its absence in most discussions / research reports on the media industry and also from institutional as well as individual investment portfolios in India.

Internationally, its already acquiring an asset class status with some of the largest pension funds and insurance companies investing in music rights through wholly owned subsidiaries or through private equity funds dedicated to acquiring music rights. In today’s environment its easy to see why these long term investors would covet steadily growing stream of cash flows generated from music rights. These rights would be a good long term asset to match their long term liabilities.

But why are they missing from portfolios of mainstream equity investors in India ?

Perhaps due to their small size, or due to past industry dynamics and/or due to contentions related to corporate governance. Whatever the reason, it has led to widespread ignorance about the industry’s transformation. A peek into history provides some insights :

A Brief History of the Music Industry

The Music label business has been a very profitable one throughout history. It has operated in classic FMCG fashion with a typical distribution network selling Vinyls, tapes, cassettes and CDs / DVDs. The control of the physical distribution chain afforded pricing power to the labels. All was hunky dory until the digital big bang.

Unlike the proverbial, creative big bang, the music industry’s tryst with digitization was hugely disruptive. It started with the introduction of Napster in 1999, which allowed free peer to peer file sharing. Piracy soared. While the music industry was successful in shutting down Napster in its initial avatar sighting copyright infringement, piracy became rampant with the spread of internet.

The truly lethal blow came from the introduction of iTunes. Apple’s radical strategy of offering singles for a dollar each broke the revenue model of the labels, which relied on bundling 10 to 12 songs in a CD and charging 10 to 12 dollars per CD. Listeners rapidly adopted digital listening devices such as the iPod and subsequently smart phones. As a result physical sales suffered and the music labels eventually lost their control over distribution channels. Consequently, their revenues and pricing power declined.

Resurrection

In classic fashion, industry reacted to challenges with consolidation. Between 2000 and 2014, over 300 music labels operating world wide merged into 3 entities viz; Universal Music Group, Sony Music and Warner Music Group. Today these 3 control close to 90% of global music content.

To bring back pricing power, the labels experimented with alternative technologies too. Each of the Big 3 took equity stakes in Spotify and offered use of their catalogues at concessionary rates to Spotify in a bid to promote streaming.

Music streaming eclipsed downloads to become the largest contributor of revenues in 2015. Every year since downloads have been declining, while streaming revenues register robust growth. The Music Labels’ revenues declined from USD23.5 bn in 2001 to USD 14bn in 2014. Since then they have recovered to USD 20.2bn in CY2019. Music is the first industry to emerge from digital disruption.

Metamorphosis Complete – Growth phase underway : The Music Industry emerged from these challenges completely digitized. It is now an internet business and a highly profitable one.

Gone are the costs of manufacturing cassettes, CDs, warehousing and transporting them to distributors and retailers. Music is now recorded, uploaded and consumed digitally. Technology allows every stream to be tracked.

The global music industry still derives a share of revenues from physical sales, primarily from Japan and Germany. But the share of physical revenues is declining rapidly. Most of the other markets are almost completely digitized or getting there rapidly. The Indian market is almost fully digitized.

This new avatar brings several favorable dynamics for the industry.

Distribution : The penetration that digitization has brought is underappreciated. In India today, to buy bread, candy, pan masala, soap or shampoo sachet, or any other daily necessity, a person would have to walk to the nearest “pan ki dukaan” at the street corner or go to the nearest convenience store or grocer. But music is available at the touch of a button, on a device sitting beside you 24 /7. Even in areas with low internet speeds, technology ensures uninterrupted streaming even on feature phones. That’s right, “distribution is now per capita”.

Convenience : The pulls and pressures of today’s busy life has made convenience a top priority for consumers of all ilks. Evolution of technology has brought convenience to music consumption. In ancient times, when one went to college in the late 90’s, a music aficionado required to carry a Walkman, head phones and cassettes to listen to music on the go and spend on frequently dying batteries to power the contraption. Now everything has converged into the smart phone and one need not even buy music. High fidelity sound quality is available for free on multiple apps and listeners can access 60 million songs on Spotify, “on demand”.

Piracy : Technology has disrupted piracy the most. There is no longer an incentive for people to visit obscure websites for downloading songs and risking virus / trojan attacks on their expensive devices. Licensed music is available for free on You Tube, Spotify, Gaana, Saavn and a host of other apps.

Cheap Data : India has the lowest data costs in the world and that provides impetus to consumption of licensed music. Globally too, declining data costs are aiding subscriber penetration and growth of streaming.

Smart Devices : Penetration of smart phones and smart speakers like Google Home, Amazon Echo are making music available through a voice command. Imagine a person working from home says, “Alexa play Arijit Singh songs”. Music streams without the person having to “lift a finger”. Such innovations and advances are increasing time spent on music consumption, by making it available seamlessly. Consumers are now listening to their favourite music at times, which would have been unthinkable previously.

Sticky Business : According to IFPI, in 2019, Indians spent 19 hours/ week listening to music compared to a global average of 18 hours. Americans spent 26.9 hours on average but American teens and millenials spent 32.6 and 29.7 hours respectively, listening to music. Despite the gyrations of the industry and emergence of new options such as video games, music remains a popular mode of entertainment.

Pricing Power : Globally 3 companies own almost 90% of music rights. Telecom, Television, Radio, and OTT pay licence fees to music labels to use their music. In almost every country there are more than 3 players in each of these categories while there are only 3 music licensors. Clearly, pricing power has shifted back to music labels. Additionally, the internet provides alternate monetization models for content, which has weakened the hold of distributors such as television channels.

Its also visible in the revenue sharing arrangements with OTT players. Spotify pays out almost 70% of its revenues to music labels. You Tube pays 55% of advertising revenues to content providers.

Intellectual Property Rights : The key driver of pricing power is copyright protection accorded to music. In India copyrights are protected for 60 years. In USA, the protection is for 70 years with ongoing lobbying to extend it to 100 years.

This is the longest IPR protection available to any industry. For eg : New drugs discovered by pharmaceutical companies get patent protection for only 20 years.

Paid Subscriber Growth : Spotify has the distinction of growing its paid subscriber base at 45% CAGR since its inception in 2008 until its listing in April 2018. In the first quarter of CY2020, the number of music streaming subscribers worldwide amounted to 400mn, up from just under 305mn at the end of the first half of 2019. This means 5.3% of the global human population now pays recurring monthly subscriptions to music service platforms.

Spotify has 144mn paying subscribers across 92 countries (out of 195 countries in the world). This provides reasonable hope that the willingness to pay for music is a global trend. It is mirrored in Netflix’s 195mn paying subscribers too and believe it or not, mutual fund SIPs are a form of monthly subscriptions too.

FICCI – EY Media and Entertainment Report 2020 cites Indian subscription revenue growth at 50% yoy. It expects total subscription revenues to cross Rs 2000 cr in the next 3 years. This amount is expected to be equally divided between music and video.

Where Will Advertisers Go ?

Indian media industry is largely advertising driven. However, in this age of cord cutting and “Content On Demand”, television is unlikely to remain the mainstay of marketing strategies.

As such, advertising attracts no viewership and therefore has to be couched within content and viewers lured with the offer of free content. In the “On Demand” age, advertisers will continue to follow audiences and embed advertising into content streams. Since internet makes distribution a more level playing field, popular content and not distribution heft, will attract more advertising revenue. This is a stark departure from the existing television ecosystem. Music being a popular entertainment option will now see more flows than before.

Indian digital advertising spend is growing at 30% CAGR and expected to reach Rs 50,000 cr by 2025. This provides a natural tailwind to the music label business.

Music Business

There are only 3 listed music companies (to my knowledge), of which the largest is Warner Music Group (WMG) which listed on the Nasdaq in June 2020. The other two are Indian, Saregama India Ltd (SIL) and Tips Industries Ltd. (Tips)

The global music industry is driven by rock stars (literally) while the Indian populace cavorts to the rhythm of film music. These are deeply entrenched cultural tastes and not easily changed. Therefore Universal Music Group (UMG), WMG or Sony are not able to bring their global repertoire and grab market share. Moreover they do not have sizeable catalogues of Indian music and therefore remain marginal players in India.

The differences in business model are reflected in margins. The global giants have seen their EBITDA margins improve from 15% to 20% over the past 4 years. However, Indian companies steal the limelight with 50 to 70% EBITDA margins. Tips has reported the highest CFO both as a % of EBITDA and Music Sales in this small universe. It also displays superior capital allocation compared to SIL.

Emergent Asset Class : Large pension funds and insurance companies are investing in music royalties. A glance through the following articles provides enough evidence to conclude that music rights are being seen as a separate asset class due to the non-correlated and inflation protected nature of their royalty streams.

-

Hipgnosis Songs Fund : USD 1.6bn of AUM listed on LSE to provide pure ply exposure to music rights.

Hipgnosis Songs Fund - Wikipedia -

Kobalt Capital – Fund 2 raised USD 345mn to invest in music copyrights, from institutional investors led by UK pension fund RPMI Railpen in 2017.

-

Round Hill Music Royalty Partners a private equity firm dedicated to investing in music copyrights raised USD 291mn as equity commitments for its third fund in November 2020. Fund two raised USD 260mn in December 2017 and Fund One raised USD 202mn in July 2014.

-

Dutch Pension Fund Manager : APG Opportunity Fund invests in music royalties ( 2013)

Rock ‘n’ roll yield | Features | IPE -

Ontario Teachers Pension Fund, CPPIB investing in royalty streams since 2010. CPPIB has USD1bn investments in royalties at end of 2014.

Intellectual Property: For music copyrights the beat goes on -

USD 3.2 bn invested in funds focused on music royalties by September 2019.

Investors in Search of Yield Turn to Music-Royalty Funds - WSJ

Scalability : The following is a purely hypothetical scenario :

What if, by 2025, there are 5 cr Indians paying Rs 100 / month (USD 1.35 at current exchange rates; not factoring further depreciation of INR) for music ?

Then subscription revenue would total to Rs 6000 cr. Assuming the music labels retain 70% of subscription revenues, they would collect Rs 4200 cr from subscriptions.

Digital ad-spends are already growing at 30% p.a. and contribute bulk of industry revenue. Taking the current industry size at Rs 1300 cr and assuming that grows at 20% p.a. Advertising’s contribution would be Rs. 3234 cr. That brings the potential market size to Rs 7434 cr.

While these macro numbers seem probable to me; I re-iterate these calculations are purely hypothetical and every investor should do their own ground work and arrive at their own conclusions.

Valuation Disparity

Despite the higher growth and superior profitability the Indian companies are trading at substantial discount to WMG. Before going private in 2011, WMG was listed on the NYSE. However in June 2020 it chose to relist on the Nasdaq instead of the NYSE, clearly indicating the internet driven nature of its business. Occam’s razor suggests there’s information asymmetry due to which Indian capital markets are not yet viewing these companies as internet businesses or pricing in the growth and inflation protection offered by music copyrights.

Given the higher margins, cash flows and ROCE’s of Indian music companies, I would argue for the Indian companies to trade at multiples similar to WMG. UMG’s listing is planned towards the end of 2021. May be that will provide a fillip to Indian companies’ valuations.

Comparing the listed plays on internet in India, i find that most lack IPR protection. Additionally, their growth rates are similar or lower and cash flows abysmal, compared to the music companies. Accounting is complex and attribution of returns is difficult in the best of cases.

In contrast, the music companies provide a pure play on growing internet penetration and on the prevailing trend of “on demand” content consumption (possible only over internet). Like other internet businesses, their revenue models offer non-linear growth, which flows down to bottom line due to negligible variable costs. At current market caps of SIL and Tips, its difficult to overemphasize the potential for value unlocking.

As the information asymmetry narrows, I believe there will be a substantial re-rating of these companies.

**Risks :**slight_smile:

Smart Phone Prices : Import curbs on Chinese products can lead to higher smart phone prices, slowing their adoption.

Data Prices : Rising data costs could cause a shift from streaming, although no alternate technology is visible just now.

Execution : While there are several tailwinds supporting the sector, management’s execution capabilities will matter in creating value. Optimal re-investment of free cash flows will be critical.

Regulations : Any change in regulation favouring platforms over music labels could adversely impact sales and profit growth.

Disclosure : Invested in WMG, SIL and Tips