Music Broadcast Limited (MBL), which owns the radio channel Radio City, is a subsidiary of Jagran Prakashan Ltd. It operates radio stations in 39 cities across India.

Revenue

The company earns its revenues mainly by advertising.

- 85% of the revenues come from advertising on radio

- 65% of the revenue comes from metros - Mumbai, Delhi, Bengaluru, Pune, Ahmedabad, Chennai, Hyderabad, and Lucknow. Rest 35% from tier 1 and 2 cities

- Local v/s national advertiser split is 40:60. This means 40% of the advertising is done by companies who want to target audiences only in a particular city.

- Other revenue sources: concerts, activations, digital communities, music streaming via apps

- Central government ad spends contribute around 12% of the revenue and 3%-4% comes from state governments. These have become virtually zero over the last 6 months.

The company has seen sustained drop in revenue since June 2019 quarter due to overall economic slowdown in India. Adversiting is a discretionary expense and is highly correlated with economic activity.

In the Q4FY20 concall, the CEO mentioned that they have been facing pressure on revenues as well as collections (i.e. collecting billed cash) since October 2019. Q4FY20 was a washout quarter due to the impact of COVID-19 as 2/3rd of March had very low or zero revenue.

Due to economic slowdown in the past year, some categories like government, ecommerce, real estate, hospitality and travel have seen drastic reductions in ad spends.

Debt & Liquidity

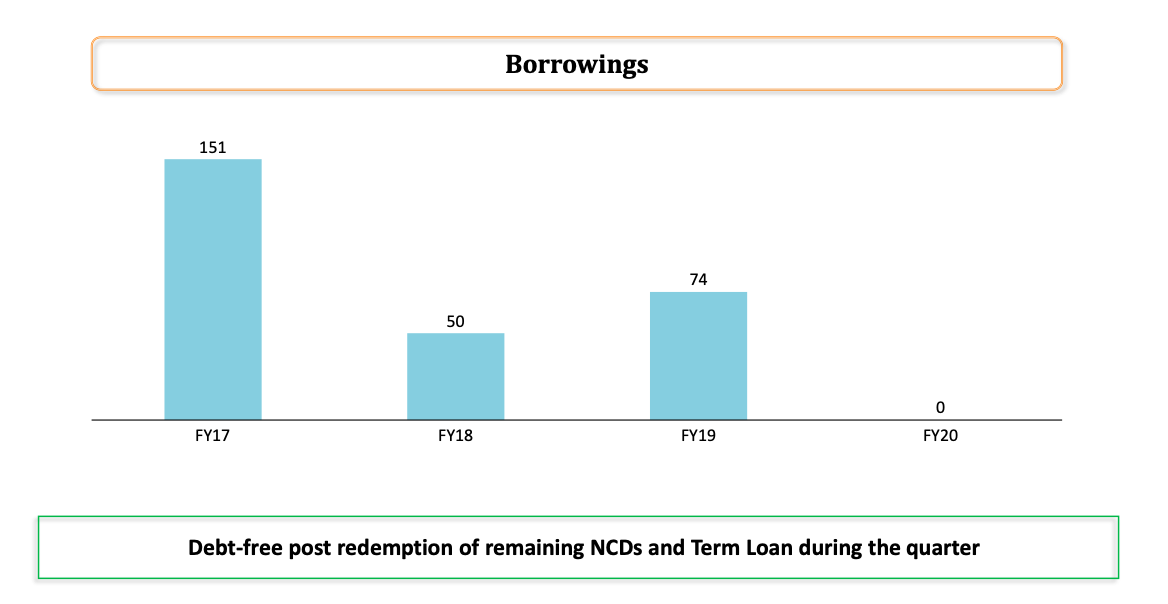

Company has reduced debt over the last few years and as of March 2020 is a completely debt free company.

- Cash and cash equivalents of Rs 220 crores as of March 2020

- Reduced monthly costs from about Rs 15 crores to Rs 11-12 crores

- Undrawn credit lines of another Rs 60-70 crores

COVID Impact

Advertizers started cancelling contracts from the 2nd week of March. The company is operating at around 15% of normal revenue during the months of April and March. Mumbai and Delhi revenues are severly affected. However with zero debt, good liquidity and reduced costs, the company is well placed to handle a pro-longed slowdown in revenues.

According to the company, radio listenership has gone up during the lockdown. However the advertisers are not spending money on marketing because shops & services are closed.

Competitive Scenario

From the FY19 AR:

- No.1 radio station in India (highest listenership)

- Highest listenership share (15.4%) in Mumbai

- Highest market listenership (24.5%) in Bengaluru

- No. 2 radio station in Delhi with 13.3% listenership share

However I am not sure how they arrived at the market position, because Radio Mirchi is present in 63 cities across India vs Radio City’s 39 cities. So it seems Radio Mirchi is a market leader with Radio City at no. 2 position.

Listed competitors:

- ENIL: A Time Group company which owns Radio Mirchi. Also a zero debt company. Worth having a look at it as well.

- HT Media Limited - owns radio channels Nasha, Fever. However radio only contributes about 3% of the revenues of the company.

- Reliance Broadcast Network Limited (RBNL) - owns channel Big FM. Struggling with high debt. MBL was in talks to acquire them and valuation was determined at Rs 1050 Crore. However it requires Information & Broadcasting ministry approval (pending) and the COVID situation could change valuations. Company has not totally closed the door on this acquisition yet and the CFO mentioned that they will have another look once I&B approval is in place. Press release: Big FM’s stations will help us command higher market share, says Jagran Prakashan president Apurva Purohit

Valuation Drivers

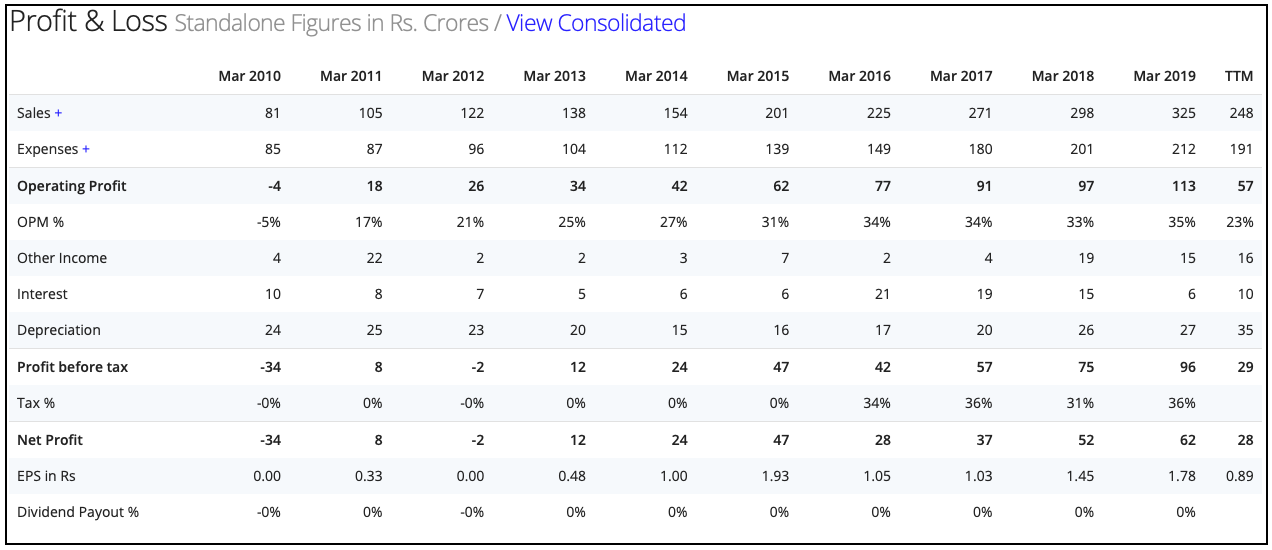

MCap: 447 Cr. FY20 Net Profit: 28.2 Cr. TTM PE: 15.8

The radio industry has grown at best at 10% even in the best economic times. My main valuation driver is extremely cheap valuations. Let me explain.

At 16 times earnings, the company may seem reasonably valued. However this does not capture the full picture. The earnings are highly skewed due to the surprisingly poor performance in Q4FY20. The company had a profit of -9 Cr in Q4FY20 due some one-off expenditures + write-offs (9.5 Cr) and impact of COVID19 for 2/3rd of March. The margins of the company are healthy at 30+ %. As the economic activity picks up, post COVID-19 impact, advertising spends will come back.

Advertisers have limited avenues to market their products - TV ads, newspapers, radio, digital marketing and promotional activites in malls. For local advertisers i.e. advertisers who want to target audience only in a particular city, radio and print are the only major channels of advertising. Print (newspapers) will go through a more prolonged slowdown due to the reluctance of people to accept physical deliveries of newspapers. IMO Radio & digital marketing spends will recover the fastest, if and when the lockdown is lifted.

Negatives:

- Very little product differentiation. Highly dependent on metro cities.

- Advertiser in certain categories like government, real estate, e-commerce, hospitality and travel spending may take a much longer time to come back.

- Company will need to take on additional debt if they go ahead with the RBNL acquisition.

- The company has a policy of writing off receivable which are more than 1 year outstanding. Apurva Purohit (President, Jagran Prakashan) mentioned in the Q4FY20 concall that they have seen some stress in collections in the past year.

- In Q4FY20, the company wrote off some 5 Cr in receivables. There could be more and we will only know the true impact after a couple of quarters.

Disclosure: Initiated a small tracking position. < 1% of my portfolio.