Based on my research experience, nd m sure lot of other investors vl agree wid this. The co. has very limited disclosures in its available materials and its not easy to find the answers you are looking for. Unless you have sm specialised scuttlebutt resources at your disposal, I suggest that this investment is a pass if u r looking from a retail investor point of view and the scuttleutt resources availale to him\her.

Disc :- Not invested. Resarched and passed it precisely for less info available and difficulty of obtaining it.

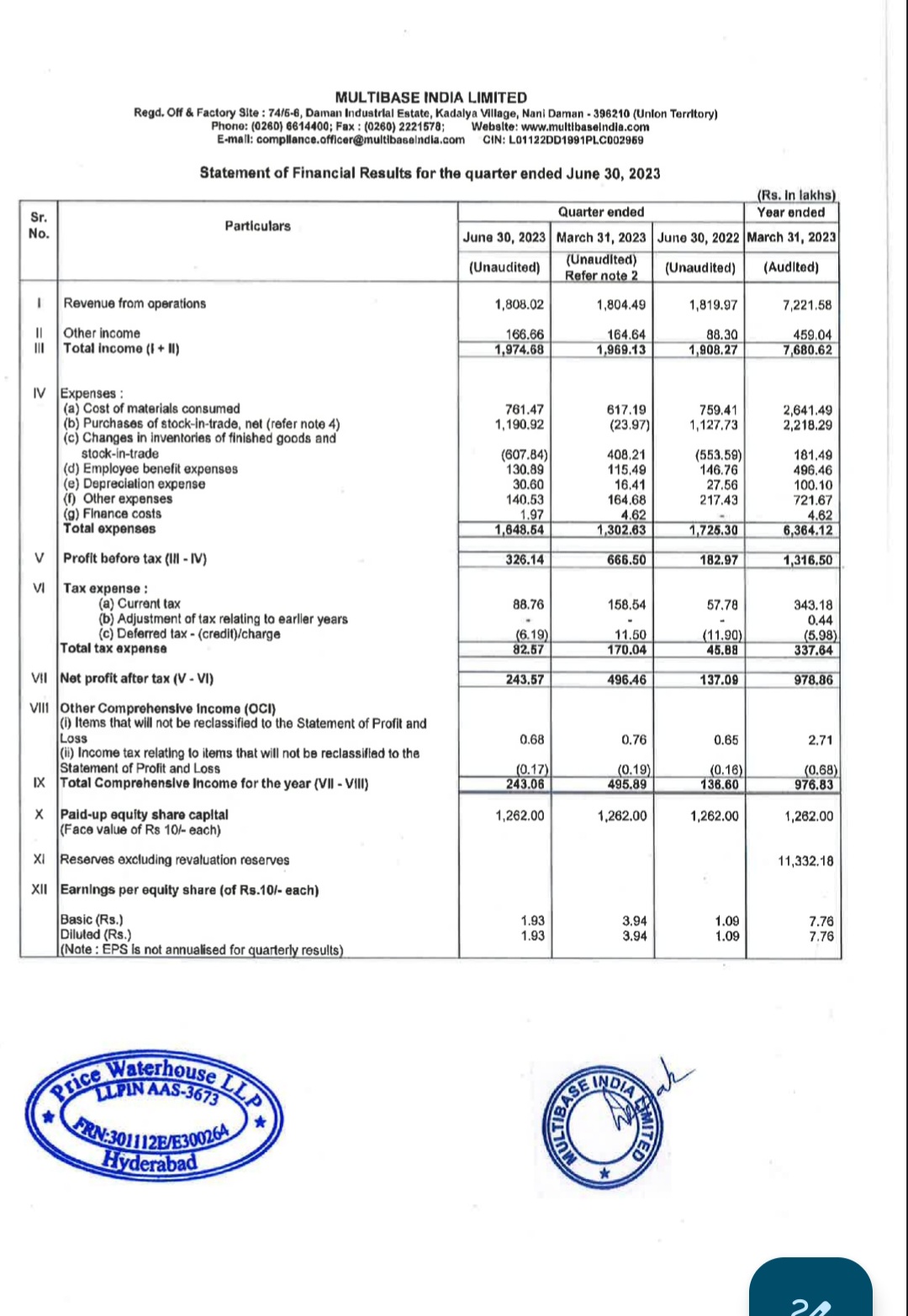

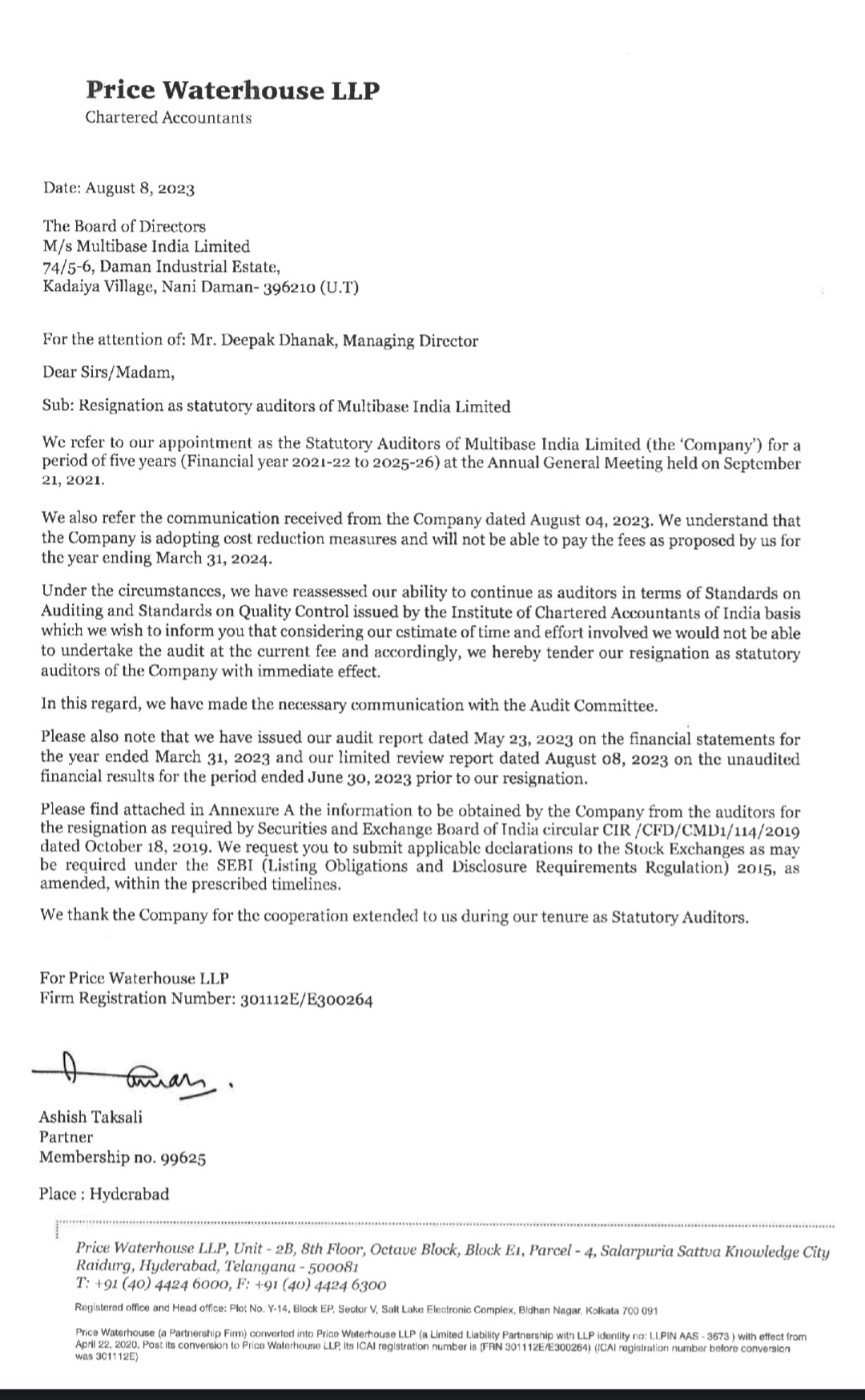

Their Auditers resigned by stating that “Company is adopting cost reduction measures and will not be able to pay the fees as proposed by us”

Auditer charges for FY 22 was 16.5 lakh, FY 21 was 15 lakh ( as per AR ). So probably auditers were expecting about 18/18.5 lakh ( at 10% increase ). Company denied and changed auditers. ( intention to reduce in other expense is visible here as well. )

So it looks like that company is seriously looking to improve bottomline. However, One needs to observe as to if / how they can improve topline as well going forward.

Disc: I have small position at lower price from current levels.

Currently operating at <50% utilization. Focus in not on volume growth, focus is improving bottom line and gross margin

Replacement cost of current capacity is not very high, key strength is technology

Had to stop anti foam product business in 2019 due to global of Dow and Dupont. This product was given to Dow. It used to contribute 40% to sales at 40-45% EBITDA margins. This product line is no longer in any Dupont portfolio

Cash usage

5-6% on fixed deposits, no answer given to give back excess cash

Have a global treasury policy, cannot invest in debt or liquid mutual funds

What is the vision for next 3-5 years?

Over next 5-years, hope to drive export growth from Daman plant

Expand silicon based products, exports from Daman, qualify new products

Target 16-18% margins in FY24 and 8-10% organic growth

Longer term focus is towards growing Multibase’s business in India, move more safety based products to India

Want to improve supply and variable cost in Daman factory. Their current raw material supply base is largely in Europe which makes their Indian entity unviable. They are looking to establish more raw material supply base within India, and then expand business of Multibase as then it will be of higher strategic importance to Dupont

Related party

Other 2 Indian Dupont entities: Electronics & water protection business. Product mix is completely different

Customer concentration

Distributors handle end market, that’s why top customer contribution looks high

Miscellaneous

Trading sale margins were adjusted in Q4FY23 which resulted in higher margins. Will keep fixed margins for traded products

Will it help Multibase India to come back to growth trajectory once again or Will we see another value destruction like in the Dow demerger?

Disc: Invested

Multibase India, Dupont US director resigned after AGM and re-election. In fact, Changes are needed in Indian management - who are unable to take the company forward in last 5 years after the Dow de-merger debacle. Hard to imagine such a stagnant company in the thriving Indian market. All other specialty chemical players grew manifold.

Suddenly 3 top management execs have resigned including the MD. Is this a clean up exercise or a fraud or something else? I believe the previous MD had not displayed even an intent of showing any performance

Not sure if the Board is going to clarify. For all 3 execs who resigned, the reason given is Personal reasons. How can 3 senior execs including MD resign in a week for personal reasons? Yet if the Board wanted to clarify, they should have done so by now. I think we should write to the Company Secretary that shareholders are not satisfied with the level of disclosures and will complain to SEBI…

It is the fiduciary duty of BOD to act in best interest of all stakeholders. You are right, keeping shareholders in the dark about the current situation of an empty executive room is a violation of trust. The board is comprised of qualified individuals, I hope they will act promptly, sooner the better.

The BOD has taken a bold attempt to revitalize the company. It is a great opportunity for the new MD, as the potential for growth is ample. Capturing new growth avenue from the parent is critical. Current revamp can tilt the ship to positive direction, yet more efforts are needed to put it into growth trajectory. Hope the new MD will raise to the challenge.