Firstly, biggest challenge while studying this company is absolute lack of information by company. Further, not on the radar of many research houses etc.considering 500Cr ish MCAP.

Actually, this superb return ratios with low re-investment need got me started on this company.

My assumption (as I mentioned, very limited sources of info at disposal), company is majorly into value-add processing and trading activities rather than integrated end to end manufacturing in typical sense. Most likely leveraging wide base of group companies to source masterbatches and TPE. Out of the ~66Cr of COGS, ~34Crs are sourced as related party transactions.

| Purchase of raw materials |

|

| Multibase S.A, France |

140,968,780 |

| Dow Corning Corporation |

33,013,313 |

| Dow Corning LimitedBarry |

10,204,796 |

| Dow Corning Europe S.A. |

45,129,271 |

| Dow Europe GMBH |

108,746,414 |

| Dow Silicones Corporation |

2,246,185 |

| Dow Corning Toray Company Limited |

106,268 |

| Total |

340,415,027 |

Another way to corroborate the fact will be to check the employee strength. 36 permanent employees only.

Dividend Payout Issues:

Very true that net margins are consistently improving for last couple of years. 6% in 2012 to 18% by FY18. Still company is not paying ZERO dividend. One distantly possible explanation (rather plausible excuse) that I can come up with on behalf of company.

Dow and Dupont are pursing merger and re-organizational exercise since 2015 which got culminated recently. Knowing the overlapping nature of product profile, Multibase SA could had a fitment in two of the three resultant entities namely material science (Dow) or Specialty Products vertical (DuPont). (Trivial: Actually, Multibase was initially aligned under Material science only, however had ‘targeted readjustment’ under Specialty Products vertical Link). In context of the large scale corporate re-org exercise, company may have found it reasonable not to deplete the reserves by issuing the dividends. More so, this may be perceived as an excise where Dow taking out money home by virtue of majority shareholder (75%).

Again, this is more of my personal conjuncture and I find it prudent in part of Dow NOT to reward itself dividend while going through a multi billion re-org.

Client concentration:

| Top Three clients |

|

|

|

FY’18 |

FY’17 |

| Top Cutomer |

218,063,094 |

68,442,476 |

| #2 Customer |

85,526,661 |

48,062,143 |

| #3 Customer |

83,546,812 |

53,146,834 |

| Total |

387,136,567 |

169,651,453 |

On one hand this becomes a risk where ~35% revenue is concentrated with top 3 customers. Whereas, on the other hand, point worth noticing is the steep jump of revenue for each of them. More prominent one being the top customer where they have a 3x revenue.

Boarders who are tracking this counter- any clue who are the top three customers, at least the industries they belong to? My hunch is on auto sector though.

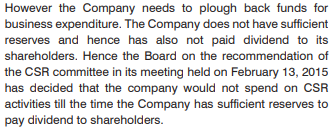

CSR spending:

Though I was able to reconcile myself with no dividend, however, a closer look at the CSR spend is

leaving my in a state of disgust (for lack of better expression).

Section 135 of companies act (prescribing a minimum 2% of average net profit for CSR spend) came in existence in 2013. Our dear company has paid NOTHING, absolute NOTHING till 2017. In 2018 they became socially responsible and spent ~55 thousand (drum rolls please). Net net, 55K spent against required 80 Lac spending so far (between 2015-18) and looking for more 'appropriate and suitable opportunities."

Equally ridicules were the explanation for previous years. Same junk year after year, just copy past the dates:

In summary, numbers are good, ratios are improving and and balance sheet looks strong. However, difficult to ascertain what is mojo here - considering the lack of info source. Also, looking at dividend issue in conjunction with CSR issue is not inducing conviction on leadership style.

Thanks,

Tarun

Disc: Multibase was on my radar for some time and took a bait once price was very favorable. <5% of PF.