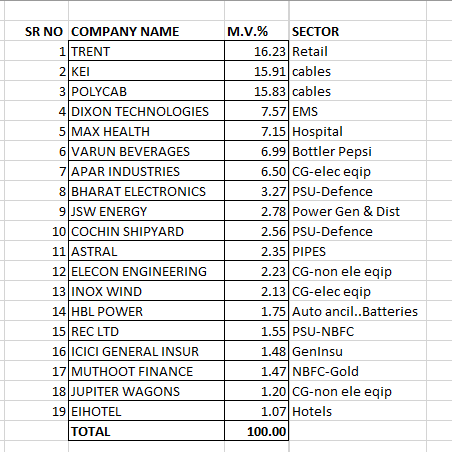

Sorry for late reply. .Actually many old stocks needed to be sold and it was a huge task. Finally the portfolio looks like this : -

Higher weights of top 3 stocks because of two reasons

They increased in market value.

Since I shifted 70% funds to mutual funds, and retained their original weights ( somewhat trimmed still) , compared to new investment amount in direct stocks, their weights became big. I don’t have any plans to trim them further , till they are performing.

Some tail is in lower weights, because recently started adding, and incremental additions will be done with new funds.

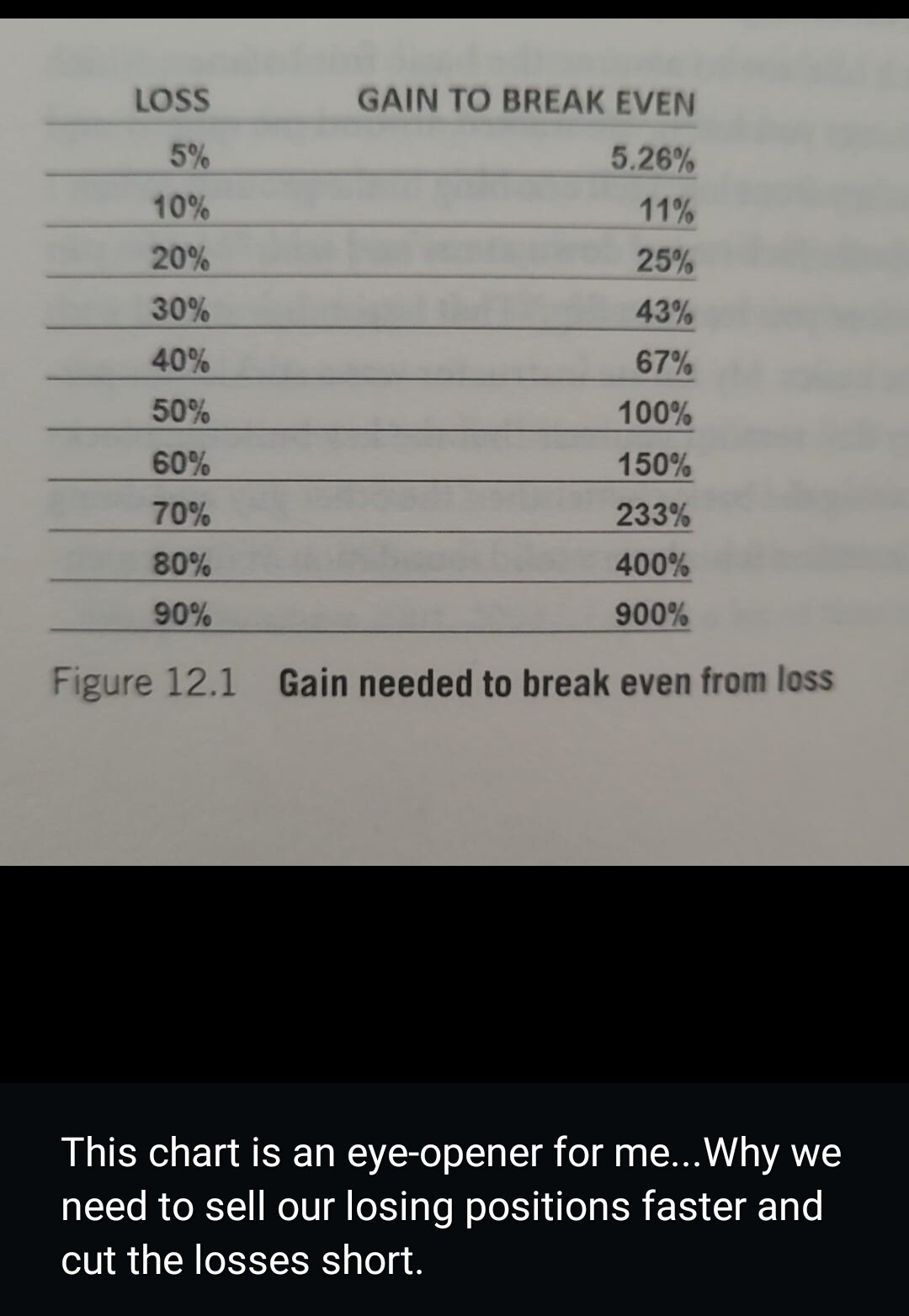

This is from Mark Minervini’s book. This helped me in overcoming a bias of loss aversion and made me comfortable of booking loss and not getting stuck in my old non-performing stocks.

Whats the rationale for 30% in cable stocks (Polycab, KEI)? Valuations are super rich + overhang of Income Tax outcome for Polycab. Would you not be better of diversifying across the energy sector (transformers, solar EPCs)?

Plus wanted to understand what your exit strategy is? Is it purely based on a stage 3 breakdown or would you check fundamentals (valuations, growth outlook) etc?

As he expressed his views about stock picking. Cable and wires which is proxy for power sector, data centres and renewable energy, sector is bullish trend, both the stocks are stage 2 and having relative strength compared to any index.

Yes, Valuations are high but he will ride the uptrend as long as it won’t beach 30 WEMA.

The 30W EMA is 25% from current price for Polycab. If someone is on a 2x on Polycab that means you would lose half your gains waiting for confirmation.

Additionally at the start of a bull run, market is more forgiving of misses on growth. But right now, even an average quarter is being severely punished (e.g., Neuland Labs). At 60 PE, wire companies need to show 30-40% growth which is a hard task on this base. So why put 30% just in cables and wires and not diversify across the bucket.

30% allocation to 60PE stocks which are well discovered and can only compund 15-20% seems extremely risky

Disclaimer: Invested in Polycab from 650 levels (started trimming post Q4 results to get allocation below 8%)

He has not invested 30% in polycab or kei… The stocks have gone up significantly making most of its stake. Also, 25% sales growth and 30% profit growth expected YoY for next 2-3 years and PE stands at around 50-60 which seems fairly valued. Polycab is entering UHVC segment starting from this FY which will further benefit the company’s revenues and topline. It’s a non-cyclical proxy to infra and construction. If he was able to buy those very early on then it seems fair in my opinion.

Disc. Sold Polycab few days ago because of better opportunities available. still tracking

@sheethal27

I am sharing my mutual funds portfolio here, but many ppl will not like this as generally ppl think 3-4 mutual funds are enough and it gives enough exposure to most companies. But my list is exhaustive, covering most types of funds available with enough exposure to Active funds, Index funds, Momentum funds and even factor funds…

Thanks Mudit. CAGR (indicative) of this MF PF entries will be helpful, if you can share…it will tell perhaps, whether it is a recent entry or you have been there with it for a while …thx

PS - I don’t subscribe to the view that one must have less number of funds. The tragedy of Indian MFs is that the top 2 funds had kept shifting, every 2 or 3 years, in the last 30 years. In the reverse chronological order, it is Quant funds now, before that Axis was ruling the roust (until the scam broke out), before that Mirae could do no wrong, Kotak for sometime, ICICI funds, HDFC, Good old Reliance funds…while one need not always look for top quartile funds, one ends up with some and they kind of hang around PFs, even though they are not top quartile…at least that is my experience

You are making huge change to your strategy here. And since you compare your portfolio returns with mutual fund returns. I wanted to get similar info. To correct mistakes quicker.

All sites generally give information about 1 day top gainers and 1 day top lossers. But as a long term investor we need gainers and loosers data for much longer peeiod. Like , 1month, 3m, 6m, 9m, 1y, 2y,3y , 5y and 10y.

I beleive we have to constantly compare our direct stock portfolio retuns with the index nifty100, nifty200, and nifty500. And also major mfs like ppfa flexi cap.

When the other make better retuns in any time period. We have to find which stock is giving those retuns. And we will be able to know what is missing in our portfolio.

In the bear phase. We will know what should have been avoided.

Unfortunately we dont have any single website where we can get this data. If you guys are aware of such one do let me know.

since you seem to have done good research, lets take the midcap category, timeframe of 10 and 10 plus years and base fund as HDFC midcap opportunities growth. Now how much cagr this fund gave vs someone who switched top performing fund in same category every 2-3 years? (although its impossible to know this in advance) …so real comparison maybe cagr of someone who held 6 different funds of same category.

I could not go back 10 years but took a look at 5 years and here is the comparison of HDFC Midcap Opps Direct Growth vs Direct growth TOP fund of the midcap cat fund in that year…

2020

2021

2022

2023

2024

HDFC Midcap Opps Direct Growth

22.58

40.88

13.09

45.45

13.2

PGIM, PGIM, Quant, Nippon, Quant

51.13

66.92

19.94

49.76

26.3

Difference

28.55

26.04

6.85

4.31

13.1

Over 5 years, this works to 15% difference on an average. There will be taxes, when you switch like this but assuming that anyway you will pay taxes, even if one exits from HDFC fund eventually (and the difference can be at best 5% between LTCG vs STCG)…My quick conclusion - the difference between top fund and HDFC fund is not much, in years, when the entire category does not perform. In years, where there is outlier out-performance, the difference is much more stark…

Thanks for the data, couple points - 5 year data is of not much relevance as its not even one cycle.

As rightly said by your last statement, during bulls the difference will be big…its the bears and the bulls thereafter which matters and hence 5 years is of not much relevance.

Second, it is impossible to switch to next best performing fund every year. These are not businesses one can track. So best possible result any mortal can get is by forming a basket and hope that basket holds best performing funds every year…but will that workout over 10-20 years or more is important because any time frame less than that is for the boys to have some delta fun…just my thoughts and I maybe wrong!

Also, an investor should not look at just returns but the Volatility of the Fund using SD.

If you are ready to accept higher SD for higher returns then you can go ahead and change funds.

Also, keep in mind that, today’s leaders are generally tomorrow’s looser.

Similarly last few years underperformer could be today’s winner.

Hence, you need to select funds based on your risk appetite, SD, Alpha, Fund Management corporate governance, and few other parameters and stick to those funds for longer time to deliver, else too much churning may not yield much benefits but you may end up paying frequent taxes.

I may be wrong in my analysis and observations.

I have changed my approach after 10-12 years of my mutual fund investment journey and I focus more on my risk appetite and financial goals rather than looking for 4 and 5 star funds. This has given more stability to my approach. This will not suit all, as this is more suitable towards your retirement or later part of career or later part of investment journey!! During initial years, you should experiment more and find what is suitable for you.

@RohitNarayanam I agree with you. When stock price runs very fast, there is a large gap between 30 week EMA and current price, sometimes more than 25% , as you have observed.

Earlier I used to think, that profit belongs to market and initial Investment is mine. So If my profit erodes by lets say 25% , I should not become uncomfortable, but if my purchase price erodes by 25% , I should become sad, BUT thats a wrong preception. Profit too belong to me very much. Everyday Market value of my Portfolio is my Everyday Purchase price .So I have to protect my profit just like I would protect my own investment.

So as You have said, if I wait for 30 week EMA , for sell trigger then I would be losing 25% of current value, which should not be tolerable. Some of my VP friends have suggested me, not to keep 30 week EMA as threshold, but to lower it, may be 30 days EMA breach should trigger selling of half of my position. I would very much like to request your opinion on this too. Sometimes my entry has been very late. Instead of VCP or nearby, i have bought very faar from 30 week EMA too. In that also ,i am currently under work-in-process selling mechanism. As far as Polycab and KEI together amounting to 32%, that was , as I mentioned earlier, due to twofold reasons : Due to transfer of funds from direct stocks to mutual funds portfolio and also they have doubled from my purchase price. As retail investors, we have this luxury of putting high amount in particular sectors or companies, which public fund managers dont have. We can exploit this in our favour. But we need to be on our toes, and first to sell, when tide turns.

@KS16

Frankly speaking, from last 20 years of experience in mutual funds industry as ARN holder and Mutual Fund Distributor, I can tell you that, no AMC has a magic wand and everything boils down to 14-15% over a very long period. No matter how many times you jump from one AMC to another and one scheme to another, you wont be doing anything better. Funds which are today in top quartile will go in 2nd or 3rd or 4th quartile in next 2-3 years. So no need of any deep research into all this. If you expect retuns around 14-15% , and also want to preserve your capital by not taking very high and idiosyncratic risks that we retailers tend to do…better shortlist top 4-5 AMCs in country and invest in their main stream funds. They will not take too much risk but will not give more than 15% returns, and since its the prestige issue( atleast I tend to think so) they will try to give 1-2% extra than Index funds to justify their expense ratio.

If you want more returns than that, then you have to.invest in direct stocks and do all those things, that we all do on Valuepickr…seperating wheat from chaff. Hopefully we dont accumulate too much Chaff.

@KishoreVignesh

Actually I dont compare my returns from direct stocks with mutual funds. That wont be fair.

Right now to get new watch list of stocks, what I am following is Relative outperformance on trendlyne on weekly , monthly and quarterly basis. This will also give you an idea, about which sectors are becoming hot currently, so u can watch more stocks from same sectors. Once you get these names, see their chart, basic fundamentals , VCP for entry… This much currently I am following and trying to fine tune this process. If any member want to direct me in some more fine nuances, pls do it…I very much require it.

" Profit too belong to me very much. *Everyday Market value of my Portfolio is my Everyday Purchase price" - I have had pretty much the same journey as you on realizing that capital invested in the market is not the money I put in but the current value of my investments.

Currently, I am using the 50DMA to exit stocks where I feel valuations are high (PEG>2), stock hasn’t moved after great results and QoQ and YoY results will stop showing multiple digit growth. I feel such stocks will sooner or later enter stage 3. A case in point is KPIT, I exited at 1500 despite great results as 50 DMA has been breached multiple times and Q1’25 will definitely be lower that Q4’24 - enough for derating to start. Let’s see how this thesis plays out

As we all know, currently Metals, Wealth Management and capital goods sector are hot and in momentum…

I have created a list after studying their charts and bit of a fundamentals…

Requesting all of you to comment on this.

I have not studied these cyclical sectors in detail…and their cycle can change anytime. But given the infra work going on , basic metals demand will be intact in next 1 year atleast…

Metals

Hindalco

National aluminum

Jindal steel & power

NMDC

Hindustan Copper

Hindustan Zinc

Wealth Managers

CAMS

Nippon India AMC

Motilal Oswal

CDSL

Real Estate

Oberoi Realty

Phoenix Mills

Godrej Property

Capital Good

ABB

Siemens

Energy sector, Defence sector and railway sector I have not mentioned as I already have them in my portfolio. I am in the process of shortlisting and adding out of this list.