My opinion on Abbott: I think it fits the category: Heads, I Win; Tails, I Don’t Lose Much.

Abbott has the resources (97% of the shareholder’s equity is in cash) to grow faster. However, their growth plans whether inorganic or new launches are dictated by the parent company who will not heed to our wishes. Hence, expectation of higher growth rate is misplaced.

While it kept growing in the past 10 Yrs., shareholder’s equity was mostly converted to cash on the assets side. Also, their current portfolio could grow FCFs @10% (similar to sales growth, which has the lowest growth rate among Operating Profit, PAT and FCF) in the Long Term (20Yrs.) due to inflation, deeper tier penetration, and demographics. Seeing the evolution of the B/S till date, I feel that 10% kind of growth might continue without utilizing much capital from the shareholder’s equity. I have not come across any other businesses that grows at 10% without investing more and more equity.

As of today, company sells at 58xFCF [822 Cr. (3 Yr. Av.)]. With a horizon of 20 Yrs., returns would still be better than FD even if multiple becomes half. In case multiple holds, growth rate accelerates and OPM expands further, returns will be much better.

Like your way of looking at Abbott. Couple questions that come ro mind…

Are other domestic branded pharma businesses like say Glaxo India,pfizer india, sanofi, astrazeneca, P&G health…not have business like Abbott India? If they want, can they not grow at similar rates with their existing portfolio?

Above is assuming the current portfolio is capable of growing 10% yoy for 20 years. Risk is if any major drug is overthrown by any competetors from its leadership position or any other reason it loses market share…

Pls correct me if wrong…

Valuation apart, I always have been thinking since past 5 years or so that is Nestle India a better business or Abbott India…

Hey (@Investor_No_1): Valid Points.

All have a big 140Cr. population opportunity. Like Abbott, I have not followed others and am not in a position to make an opinion on the fly(Edit: Did a quantitative exercise. Details appended at the end.). Equity valuation demands a long term thinking to form a view about the prevailing prices. However, one must take action in the short term as per the change in circumstances since competition was there, is there and will be there.

I read Mudit’s view on another thread and was providing him with another perspective. Needless to say, all opinions are proven wrong sooner or later in the equity market.

Both Nestle India and Abbott are good businesses. Since they are in different sectors, one can keep both on radar instead of choosing one. Mispriced valuation might make either of them a great buy at different point of time. With home work in place, any opportunity knock can result in good financial outcome.

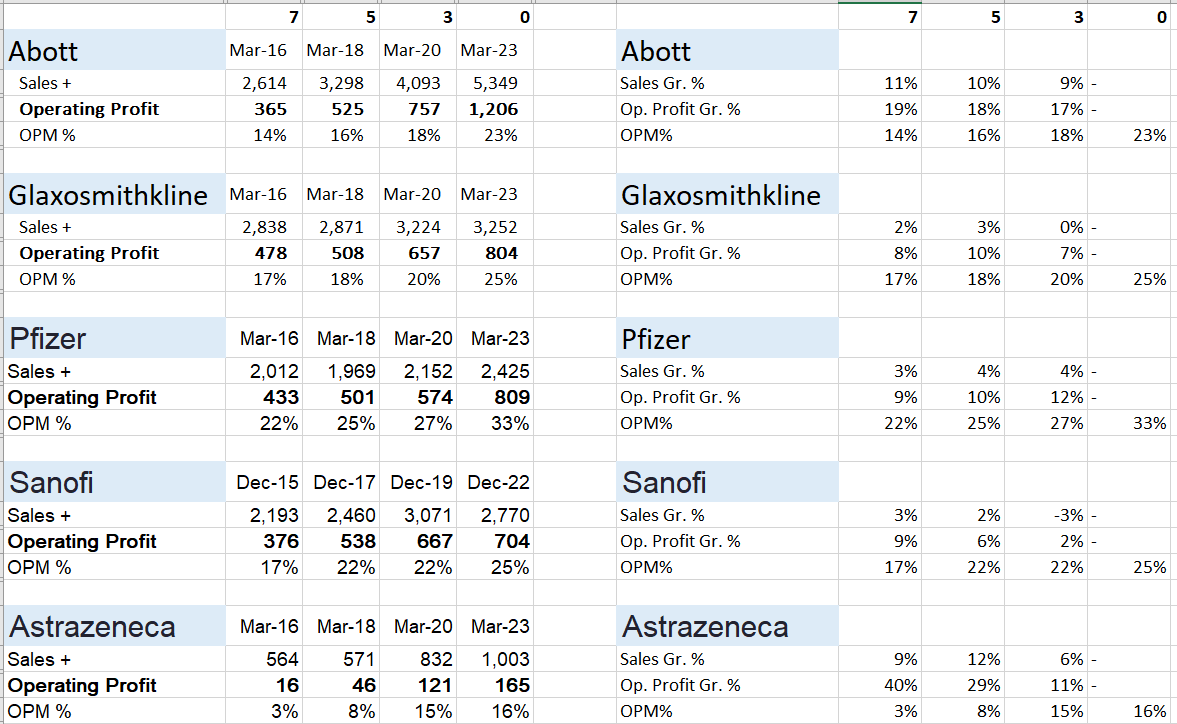

--------------------- Did the exercise using key data from the P&L of the names you suggested. Observations:

- PGHL: Avoided in this exercise as it had a FY change in 2020, making data non comparable

- Considered only 7 yrs. of data for all others to avoid FY changes of both Abbott and GSK

- Abbott: Highest Sales and Operating Profits - 1.7x and 1.6x respectively of the 2nd nearest competitor.

- Abbott: Best sales growth among all when considered for a time period of 3, 5, and 7 Yrs.

Conclusion: Among MNCs, Abbott has done well in the past and the trend shall remain so. To make a firm opinion about others, qualitative aspects [product, brand pull, strategy etc.] need to be investigated. However, numbers of the past performance does not evoke exictement even though B/S of all is strong.

Data Snapshot:

@Mudit.Kushalvardhan : DM pls, if the above shall be wiped to avoid clutter on your portfolio thread.

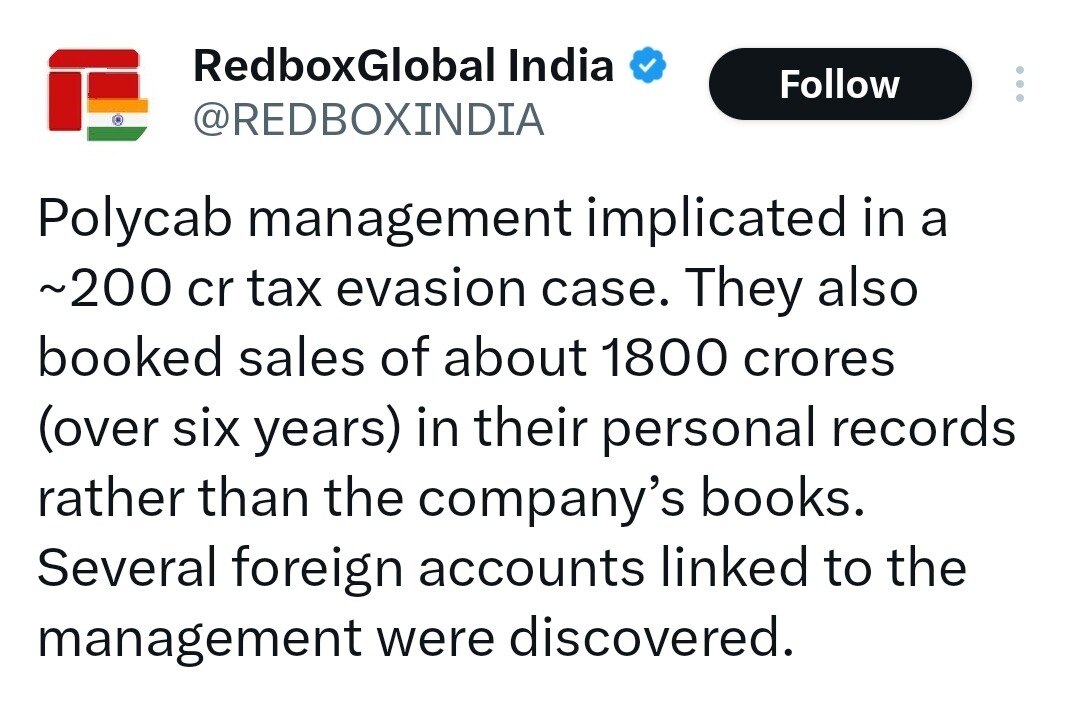

Waiting for clarity…Not taking any action. Stock down 9%. If true , then serious corporate governance issue.

Hi Mudit, Any learnings taken away from the Polycab Episode. What are steps we can take as retail investors?

I think, you have polycab issue in mind.

As per my point of view, cash business has been a tradition for indian businesses , particularly in these segments. Even if you visit your local shops , you will find that they keep two sets of books…One for the tax purposes and one which is real, which includes cash dealings. And when a business gets listed , this habit and tradition continues. I will not take holier than thou approach. Its part and parcel of indian business operations.

I would like to give analogy of another MNC company which I held for 3 yearsand recently sold off. Abbott India ltd. Its an Indian subsidiary of Abbott. Now this MNC parent also maintains a Private Ltd subsidiary called Abbott Healthcare Pvt ltd, which is not a listed subsidiary. Now many good medicines and famous products are launched not under listed subsidiary but under unlisted pvt subsidiary, thus causing loss to the minority shareholders of Abbott India. This is also a form of theft of profit which rightly belongs to shareholders as the cash sales of polycab. But its legitimate and nobody can do anything about it as parent holds listed subsidiary very close with 75% stake. And then there are so many businesses who divert business to their private companies at the cost of listed companies. This is more of a norm and SOP. As and when our markets reacts strictly, some shareholder activism gets established , these practises will become things of the past, but its not going to happen in a hurry. In our lifetime of investing, things will continue and we should not lose sleep over it.

I had already replied at HS portfolio. Posted again here

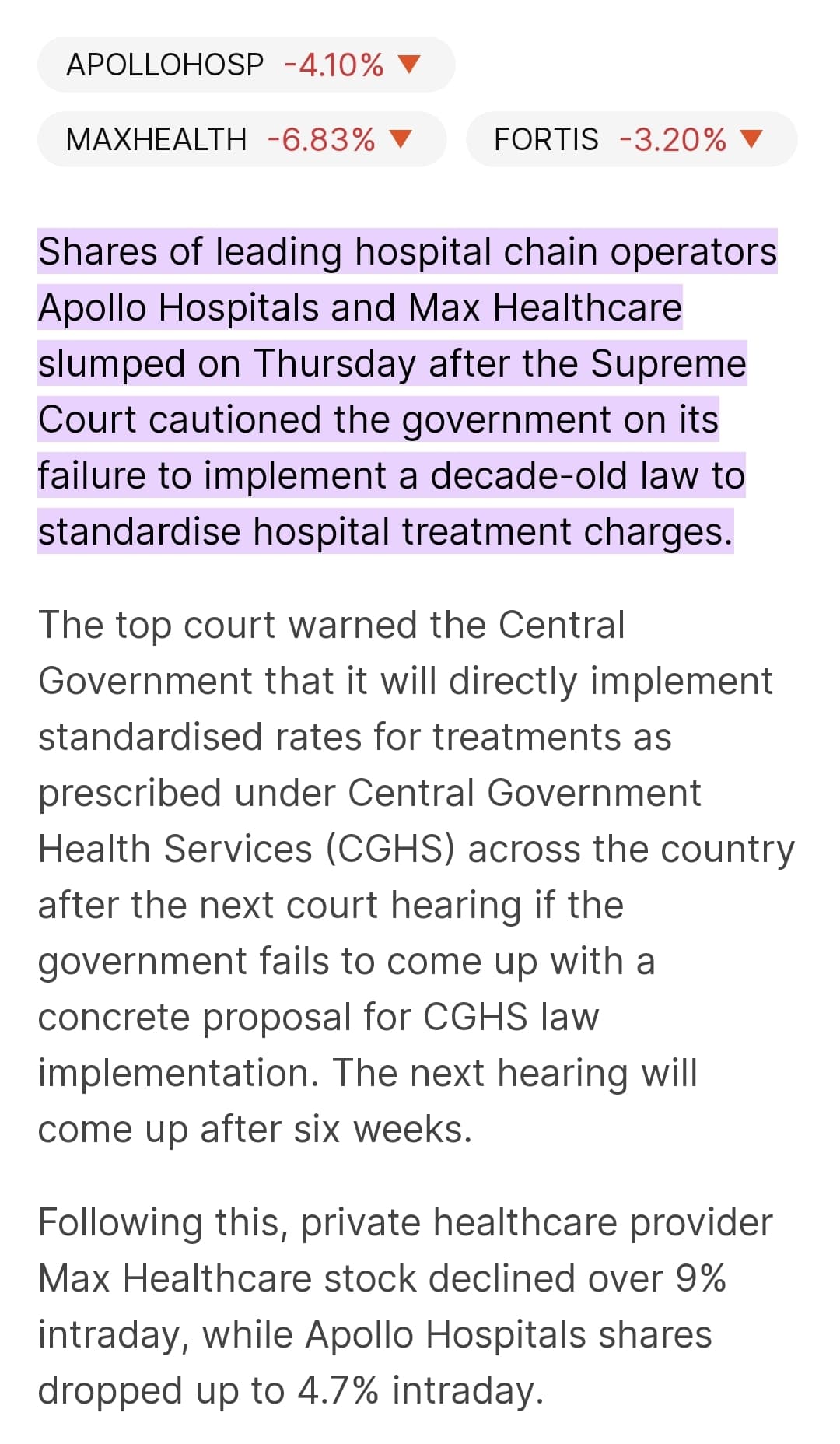

Today One of my portfolio holding, Max Health care was down by 7% . Above is the reason for it. If any of our group members are holding hospital stocks, what is the way going ahead? Will this standardisation rates be a reality ? And Supreme Court is talking of implementing it in 6 weeks, is it a great threat for hospital companies going ahead? How we should look at this?..

@Mudit.Kushalvardhan Hi sir…

I am following your thread regularly.thanks for the valuable insights.

There are regulations already in some states (Karnataka private medical establishment act)to control the private hospitals.Latest intervention of supreme court is definitely a threat to the operating margin s of buisness.As honorable supreme court has issued directions government may do something before court implement it or take some time to execute.Whatever is the process,laws will be definitely not in favour of hospitals.

We can see it as a shrinking margin.But as you know health care in inda has tremendous opportunity size, for growth, and these regulations will affect smaller hospitals more than larger one i will take it as a short term problems (maybe couple of quarters).And definitely derating can occur because of these developments and chances of decrease in profits.

Disclosure… Invested in Unihealth consultancy for the same reason because it operates mainly in Africa region.

Lets say the government and court allows Hospitals to even charge higher than CGHS rates as hospitals will not bow down easily. They will use different techniques to maintain premium pricing power.

Even then margins will drop. Ebidta margins of 30%+ and 20%+ NPM will be unsustainable. Look to it dropping to more sustainable rates. 10-15% NPM are global average. So, it would settle there.

But since the government depends on high FDI and investments from PE and SWF capital to boost the sector, it’s also possible it may drop just a few points and not drastically.

All depends on how seriously government manages the contradictons.

After a long time…Update on my portfolio. some Major revamp …some portion increased to Mutual funds.

Valuable discussion is found in this valupickr thread

Hi All, Update on my Portfolio…

Major revamp…After studying Stage Analysis and Relative strength, I have changed my portfolio approach drastically, mostly in favour of momentum investing with stage analysis.

To start with,

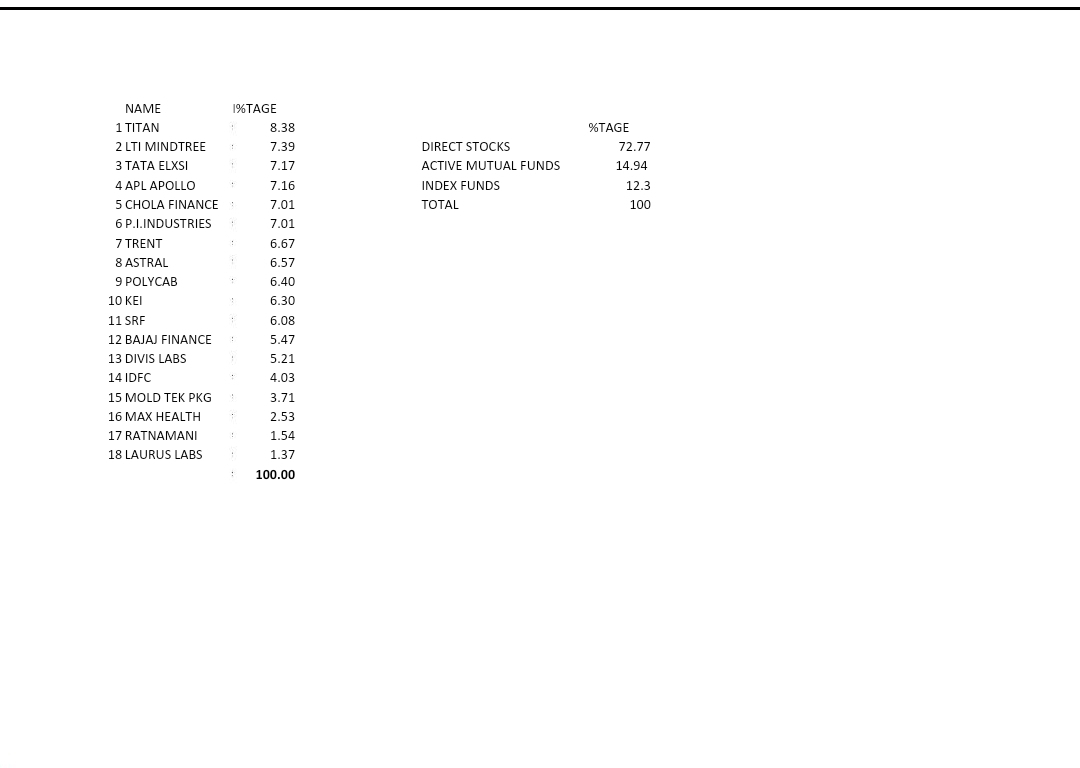

major radical change is, I have allocated my portfolio as

Mutual Funds 70%

Direct Stocks 30%

In mutual funds all 3 categories namely

- Index Funds

- Factor based index

- Active funds are included…

For direct stock portfolio…I would post in 1-2 days, when things settle down a bit…But for those who know me and my earlier style of investing, its going to be a shocker… ![]()

Before posting update on portfolio. Please elaborate on stage investing and relative strength. Also what was the thesis to change your style of investing. Because I am also in similar dilemma

As anybody can see from my earlier posts , I was a Fundamental-oriented investor from start. Reading Annual reports, concalls, credit rating reports ,brokerage house reports, following news related with my portfolio companies, watching Management Interviews etc is what my M.O. for selecting and tracking the companies. I was never into technical analysis and never beleived into it…and even today also I don’t beleive more detailed technicals and I consider it as hoodoo.

And in last 2 years, when overall market was in strong bull phase ( and still is in)and even my mutual fund investments were giving very good returns, my direct stock portfolio was giving very very ordinary and disappointing returns. All my stocks were good. take Bajaj Finance, SRF, Pidilite, Divis Labs, Nestle, Tata Elxsi, LTI MIndtree, Kotak Bank, HDFC bank, Muthoot Finance etc. All are good quality companies and I was tracking them fundamentally and still Portfolio performance was so-so. And I was desperately finding the reason for my poor performance. And I came to know about Stage Analysis and read Stan Weinstein’s book…and it kinda opened my eyes.

Companies may be good quality , having moats, superior business models etc…but one thing was missing in my portfolio stocks and that one thing was momentum.

We make money, when share price of our companies go up …very simple truth…not when our companies make good profits , although that also can happen simultaneously.

First time when I started seeing Price and volume charts of my companies and it gave me a shock to see companies like Bajaj finance, consolidating for 2 years at a stretch , LTI Mindtree at same level for 1-2 years and I am blindly holding them , hoping that the price will appreciate soon, not understanding that there are currently more sellers for these stocks than buyers. Then I applied Stage analysis to all my stocks and when I entered into them and I was shocked that I was actually buying them either during consolidation or during their downtrend. That was the reason for my failure.

While those companies which I bought during stage 2 , uptrend like Trent, KEI, Polycab, have doubled in just 1 year or so.

We need to understand that share price of our stocks will increase when more people buy our companies and in large quantities. And such buyers are invariably big players, either promoters or Institutional investors, insiders. And we have to agree that they have informational advantage over us. We would like to think that there is no insider information or informational asymmetry but in practical world everybody knows that we are the last people to get any information about our companies. All results, all critical information first goes to big guys. And if they act on that information, it will be seen in the chart on price and volume. So we cant know the exact info but we can piggyback these big guys by following this price and volume action. Thats the only option we have. Ultimately all information will translate into price. Then why not track the price?

And I am not talking of trading here. Investing by piggybacking big investors through the price-volume action…Thats Momentum.

Then I started applying Stage 3 and stage 4 rules to my failed investments like Laurus labs, Divis Labs, LTI Mindtree and came to know that had I applied stage 3 rules, I would have exited these stocks much much earlier thus saving myself from big losses. And also by avoiding consolidation phases, I would have deployed my funds in growing stocks. So most important thing I realised is to avoid stage 3 and stage 4 stocks and if any of my stocks enter in such stages, I would exit at earliest.

A well thought out change. I think that you also need to widen your fishing area (cover more names) as well as find the fastest way to be in the best fishing spots (ongoing price bullishness), keeping fundamentals as the bedrock since a lot of questionable stocks go up during bullish sentiments. Best of luck.

Yes. Thats another angle and for that I use relative strength.

My portfolio will show that. In stage analysis some basic rules are:

- Market has to be in uptrend…so market needs to be bullish.

- The sector needs to be in momentum…So my mistake was …I entered in Divis Labs, LTI etc when these sectors were at their fag end or going down,They were not the growing sectors or leading sectors of the bull phase. So now I have corrected my mistake. Some of my stocks now are from power sectors, Wind energy sectors, defence, PSU also. Some companies earlier I never heard of before.

- Stock has to be above 30 week EMA and that also should be increasing one.

- Dont enter very late

5)Volume has to be good …More investors should be interested in your stocks

6)Relative strength should be good compared to major index or that sector index

7) And Dont buy such stocks where nearby overhead resistances are strong…That will not allow your stock to go up.

8) Continue your journey and ride the stock, till it doesnt enter into stage 3 or stage 4…and this period can be 3 months to 3 years to 10 years also…So it can be short ride or a very long ride

Request you to share your process for the above 3. Intend to learn and adopt. Much Appreciated. TIA.

What you will do in the bearish market phase?

Simple definition of relative strength is price of your stock should be increasing more compared to nifty index or that sector index. Like today Nifty was down 0.66% but one of my stock Dixon technology was up 6% or Kilburn Engg was up 5% so these two stocks were relatively more stronger than Nifty Index. Similarly today Bajaj Finance was down by 7.72% so it was more weak compared to Nifty Index. Simple way to find the relative strentgh stocks is compare the Relative outperformance of stocks to Nifty 500 Index on Trendlyne website. These you can select your desired universe Nifty 200 or nifty 500 or nifty 750 etc. This realtive strength you can comapre on daily or weekly or monthly, quarterly , yearly option. Mostly Using monthly or quarterly option is better so you can avoid some abnormal daily outperformance and you want consistent monthly or quarterly outperformance. Once you get these list of stocks, you can check their chart on Trading view from stage analysis point of view.