Here is a narrative I have prepared for how I think the story will unfold for MT Educare and the coaching industry. The main objective is to verify whether digital content can change the game to the the extent that, the traditional coaching business will go from being very local and fragmented - to a winner takes all market (or somewhere in between). I would love to hear your thoughts on this. MT could be in a moat development phase - arguably an opportunistic time to enter.

Note: I currently have a 5% position in MT Educare. My views may be biased.

The coaching industry

Education is a $100 billion market in India (source: IBEF, Nov, 15). The proportion of students taking private coaching is ~26%. The coaching industry is estimated to be $10 billion plus market, expected to grow at 10-15% over the next 5 years (source: CRISIL, company presentation).

As per a report by the Centre for Education Growth and Research, the Indian education system is short of faculty members at-least by 30-40%. This along with several other factors such as inadequate existing school infrastructure, high student to teacher ratio, inability of teachers to give personalized attention, lucrative job opportunities, working parents, changing curriculum, growing competition amongst students and shortage of quality institutions, have led to strong demand for supplemental education.

The coaching industry can broadly be segregated into subject based tutorial coaching and entrance exam preparation coaching. Subject based coaching is primarily for K-12 classes. The size of the subject based tutorial coaching is estimated at 80% of the coaching industry while entrance exam preparation coaching forms he remaining 20%. The entrance exam preparation coaching can further be segregated into graduate test prep (JEE and AIPMT) and post-graduate test prep(CA, CAT, GATE). Graduate based text prep makes up ~80% of entrance exam prep and has grown at a CAGR of 10% over the last 7 years, while post-graduate test-prep makes up the balance 20% and has grown at a CAGR of 18.5% for the last 7 years (source: company presentation).

The coaching industry is very fragmented. Most of the industry is unorganized, eg. Teachers running tuition classes from their own homes/independent classrooms for students in a particular area. Even the organized sector is very fragmented, wherein one or a few players do not dominate the market. The main reason for this is that running coaching classes is a local business. Parents/students choose which coaching class to enroll for depending on what other classmates in school are doing, what seniors recommend, and logistical convenience. What students in other parts of the state/country or even city for that matter are doing, or how many cities a particular coaching class operates in, is of little relevance. Even individual payers that scale a little bit, at most benefit from brand recognition in a particular area. Organic expansion is hard, and as evidenced by MT’s story, players must rely on strategic partnerships and acquisitions for growth.

The major changes taking place in the industry are consolidation and adoption of technology for better classroom learning and on-demand digital content. The organized sector is gaining market share from the unorganized sector. So Lakshya IIT in north India, or MT in Mumbai, is probably gaining market share from independent tutors leading to consolidation. The main players that are emerging as a result of this consolidation are trying to create their own digital content. Some new players are creating only digital content. The digital content is available as a smartphone/tablet app for online access, or as a memory card/usb that can be plugged into a tablet/computer. The content is either curriculum focused or general, free or paid, exclusive or accessible to all. Content also varies on the breadth of curriculum covered, eg. K-12, IIT, CA. etc. Currently, there only 2 players that have curriculum focused content that is accessible to everyone through a smartphone/tablet app are MT Educare and Byju’s. The others are either in the process of creating their own apps or do not wish to make their content non-exclusive. Toppr is another player that has an app, but it only focuses on practice tests for IIT. Of the content currently available as an app, only MT’s robomate app is free. However the SD card is chargeable. It wouldn’t be practical for any regular user to consume heavy data and buffer lecture videos all the time, so in effect regular users would eventually have to opt for the SD card/tablet option.

This is what I think is going to happen moving forward…………….

Digital content will add tremendous value to price-sensitive and self-motivated students. Digital content will serve as a practical alternative to students who cannot afford expensive coaching classes or who do not wish to go through the logistical hassle of travelling to a classroom several times a week. Sharp students who can grasp concepts quickly will also prefer such a medium as they don’t have to waste time in class while the teacher is explaining something/solving doubts for a topic the student understands really well. Students in tier 2 and 3 cities and towns will have access to teaching and content, that could never be delivered by the teachers they currently have.

Watching video lectures and giving tests on a tablet is a big change for students. But for reasons mentioned in the narrative there is an immense shortage of teachers and content, and a digital platform addresses this need. In only 6 months since its launch, Byju’s has managed to get 120,000 paying annual subscribers. (source: http://www.livemint.com/Companies/zaIz12mD9y9Wx6hlyP2JjM/Education-technology-startup-Byjus-raises-75-million.html). After 3 decades of being in the business and with over 1250 faculty members and 270 locations over the country MT served ~83,000 students as of FY 15 (source: investor presentation).

However, taking into account the age group of the students, Indian psyche on education, and the fact that although the student is the consumer, the parent is the customer, digital content alone - is not enough. It has to bundled with a physical classroom experience. Without a teacher following up on a student’s progress, testing in the presence of an invigilator, embarrassment faced by a student in class who does not do the homework etc. students may slack. A digital + physical model wherein students use the digital content for study material and studying tools but go to the classroom once a week for doubt-solving and testing will best address the current need.

Digital content will also add value for teachers. Teachers from the unorganized sector, especially in small towns and cities do not have the resources to create high quality digital content. Partnering with a digital content provider may be a suitable course of action for them as well.

Is there a network effect up for grabs?

As mentioned earlier, traditional coaching classes don’t really benefit from network economics. However, bundling digital content with a classroom experience could give coaching players a network effect competitive advantage. Here’s why. Digital content provides single-player utility to both students and teachers. Single-player utility is the utility a user gets independent of how many other users are there. Single-player utility is often very important to get a network going. The real question is whether the digital content platform - connecting students, teachers, digital content, and classrooms -will benefit from cross-side network effects common in a marketplace structure. Airbnb is a an example of a marketplace structure that has a cross-side network effect because more hosts leads to more guests and more guests leads to more hosts. For digital content platform X (hypothetical), more teachers will definitely lead to more students for reasons already mentioned. I also think that more students will lead to more teachers. As there are more students using X’s content, they will need more teachers in wi-fi equipped classrooms to provide the “learning management system” experience. Customer acquisition becomes easier for teachers that move to X’s platform.

Simply put, a network effect occurs when a product or a service becomes more valuable to its users as more people use it. This is exactly what I think could happen in the case of X, or a player that bundles its digital content with a traditional classroom experience.

Note: For more clarity on the structure of player X and the “learning management system” see -https://www.youtube.com/watch?v=fulTFa5iXZ8

For a better understanding of network effects, the lingo used etc. see - http://www.slideshare.net/a16z/network-effects-59206938/34-AirbnbT_W_O_S_I

More on why MT could develop a network effect…

I think cross-side network effects comes down to whether you think digital content has to be be paired with physical teacher-student interaction in a classroom. Content will not change much with additional teachers or students. For this reason Byju’s will never really have a network effect. However I think more students will lead to more teachers. From my meeting with MT Edu, I gathered that Kunal, who is an independent teacher running a coaching class can get access to MT’s content and LMS software if he brands himself as Kunal MT Educare Tutorials. It would be in his interest only to make the move if it will enable him to serve more students and thus make more money. As more students start using Robomate there will be great demand for classroom time as students will have doubts to solve and parents (for the several reasons I have mentioned) will require this. If there is enough demand then by moving to the MT platform the teacher will be able to charge a higher amount per session and still run at full capacity. It is perhaps appropriate to make an analogy to Uber’s success. By moving to the Uber platform cab drivers avoided downtime which earned them no money. As more customers joined Uber, it became easier for Uber drivers to pick up the next customer at the location of their drop-off before waiting for someone to hail there cab or waiting on the radio. More drivers led to more customers and vice-versa. People who were not cab drivers, but were capable of driving also became Uber drivers. The same could happen to some degree with MT. More teachers leading to more students is relatively intuitive. But I think more students will also lead to more teachers and therefore there are cross-side network effects. Like Uber however, the network effect will be local. For Airbnb, more hosts in LA benefits guests in Mumbai. But for Uber only drivers in Mumbai benefits riders in Mumbai, drivers in LA are irrelevant. Likewise for MT, the teacher student network effect will be local - teachers in Delhi will not have an impact on students in Mumbai. So while it is not the strongest kind of network effect it is still a pretty strong moat.

Anybody, anywhere in the country has access to digital content, as long as they have a smartphone or tablet. More students using digital content will lead to more teachers adopting it, leading to a larger network of classrooms, leading to more students. As mentioned before, only two players currently have curriculum-focused content that is available as an app - MT and Byju’s.

MT Vs. Byju’s

MT has a traditional classroom business for the last 3 decades and has launched its app only 2 months back. Byju’s is solely a digital content provider (no classroom business) and has launched its app 1 year back. MT has bragging rights for the numerous toppers/rank-holders it has produced over the years vs. Byju’s, that has only been around for a year. MT has bundled its digital content product offering with a classroom experience. Prospective students will definitely have doubts that need to be solved and physically meeting a teacher to have questions and doubts clarified seems intuitively preferable over doing so over Skype. Furthermore, the parent is the one paying and even if the student says he is self-motivated and won’t cheat on the tests, the parent doesn’t want to take that chance and spend the extra time ensuring that the student is delivering on his/her promise. By bundling digital content with a physical classroom experience I think MT will better bridge the gap between technology enthusiasts/visionaries and pragmatics/conservatives.

Barriers to entry

I think due to a combination of the reasons mentioned above, more students will opt for MT’s content offering over Byju’s. Sinhal Classes however, also has been around for a few years and has some brand recognition in and around Mumbai. As a thought experiment, let’s say Sinhal Classes also decides to create digital content that is accessible through an app. Let’s assume that Sinhal classes is able to match MT’s content in terms of quality, and because Sinhal has a track record of a few years and has similar bragging rights to MT’s in terms of toppers and rank holders, parents and students may be as willing to use Sinhal’s content as MT’s content. However, by now MT has a head start as it already has a million users. This creates a barrier to entry for Sinhal. Many students are familiar with Robomate and so teachers would much rather partner with MT than with a new entrant. As a result of this Sinhal will never be able to scale its network of classrooms, while MT’s network will keep getting bigger.

Sinhal’s captive students will probably use Sinhal’s app. But look at the decision tree for students in tier 2 and 3 cities. They have to choose between a) going to some independent tutor who cannot provide the benefits of “a learning management system” b) chose MT’s hybrid option which gives the student access to digital content and the option to meet a teacher once a week c) use Sinhal’s app alone. Sinhal does not have a network of teachers in tier 2 and 3 cities and will find it very hard to create one for the same reason that another online taxi service (apart from Uber and Ola) will find it hard to get drivers on it’s platform. Uber offers a commodity type of service pretty much. MT can still differentiate itself by virtue of its brand and a superior product, making it even harder for Sinhal to get teachers on its platform, once MT has established itself.

MT has a clear advantage of brand over Byju’s. With respect to other traditional classroom players, MT has a a first-mover advantage, which means that MT is best poised to get the potential network effect that is up for grabs.

This is just a hypothesis of course. I could be wrong entirely.

What if there is no winner takes all network effect

Even though I have been making an analogy to Uber/Ola, to think that MT will become as big as Uber/Ola is ridiculously optimistic. But there are a number of situations that could play out.

-

MT really does reap the benefits of the winner takes all network effect as I have laid out in the narrative.

-

The network effect could develop in clusters wherein other players start pursuing a similar model in different parts of the country. If this happens I think there will be a few players(not 100’s) and the market for a digital content platform will be a lot more consolidated than the market for the traditional classroom business.

-

I may be wrong about the fact that digital content has to be paired with a physical classroom experience, in which case there will be no network effect at all. However, even in this case Robomate could still to very well on the strength of its brand resulting in robust tablet/SD card sales.In 9 months in FY16, Robomate has already gone from nothing to a segment that generates 34cr in revenue, and services ~47,000 students. Like I mentioned before, in the 6 months since Byju’s launched its app it is already servicing 1.5x the number of students that MT was able to service in FY15 through its classroom business after 28 years of being in the business.

In all these situations, earnings will go off the chart. Finally, there is the situation that Robomate fails entirely, in which case you are paying 20x earnings just for the traditional classroom business. There was a little bit of skepticism about the prospects of the core classroom business. Student growth in the school segment was flat and they had to cut prices. While this is a negative sign, MT has had phenomenal growth in the other two segments, especially the science segment. PUC tie-up model is doing really well. Core classroom fee income has gone up 10.3 % for 9MFY16 compared to 9MFY15 (see investor presentation). Even if Robomate fails I think as an investor you won’t lose much by paying 20x for a decent business - asset-light, negative working capital, strong FCF generation, fee increases that lead to operating leverage, minority shareholder friendly management etc…

Feedback would be much appreciated. I hope this gets a discussion going.

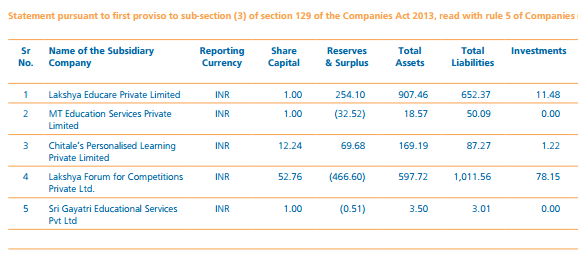

Shree Gayatri is in AP/Telangana.

Shree Gayatri is in AP/Telangana.