I think its fair to assume now that PUC model is certainly a rewarding model, if executed well. At the same time we need to understand what are the barriers towards scaling that? MT focuses on the colleges that are not doing so well… as they would be more willing to a partnership. Now the question is how easy it is to turn these colleges around?

The other interesting thing I picked up in my conversation was that there were no major brands in the PUC model at this moment. Most of them are smaller players who don’t have the vision or the financial reach to expand beyond their backyard. This provides a good opportunity for a professional player such as MT to consolidate and scale. Maybe talking to competitors local PU college players can provide more ‘insights’. Folks in Karnataka please help

Hey @cool_aksh They are seeing strong traction in Robomate and strong growth in general as well. I think the next few quarters will be again interesting on the following counts:

Margin expansion: The tablet sales that have happened - which is a cost at the moment, should be passed on the the students from next FY. As a result you will see gross margin expansion.

Andhra market : Their expansion in AP should reflect in number by FY17/FY18, I feel the market is ignoring this, for reasons unknown to me. So in AP they have 35K students, at the moment they have some ~ 80-85K students. So AP adding to the mix will be quite a push to sales & profits too

Robomate: This is the joker in the pack for me. Its growing at a good clip.

So long as the cash flows remains intact and the growth remains profitable. It could turn out to be pretty interesting play.

I met a college friend after long time who is also a Lecturer. He shared some great insights -

There is a dearth of quality Physics teachers and there is lot of demand for them. When he went to take up an opening for a Maths position, he was asked to do Physics instead. Of course, he was very capable as well.

He lamented at the quality of teaching at IX and X standard which are arguably more critical than PUC. This was based on the nature of very simple doubts asked by students during his private tuition sessions. Of course, he takes the time to explain the fundamentals and entertain all the questions without judgement.

More often than not, IX and X students who massively benefits from a specific tutor tend to stick with them even during XI and XII. This is with respect to those who had a substantial performance increase of 10% or more. Say from below-average (below 65%) to above average (above 75%).

IMHO, it can be a sticky business assuming one targets the class IX and X students for more focus and improve their fundamentals. If they truly believe in a specific tutor they will stick with them.

Also, competency of Physics lecturers can be a good yardstick to compare against MT’s peers.

Disc: Not invested. On Watch-list and will continue to track.

I am new to this forum. But I have a couple of questions regarding MT Educare if you can help me understand it.

a) In August 2014, managment decided to bring in QIP of 55 crores, which didn’t go forward because they sold managlore college & got the money for required Capex. This year again on 21st Jan, they approved the re-initiation of QIP. Isn’t this wrong that every year they are in requirement to have a huge capex money ? I know it is growing its presence across different states but diluting equity from 39 crore to 39+50= 89 crore ? what is the use of internal accruals & asset light model of PUC then as put forth by management ?

b) will this not impact the share price negatively ? And also, since debt is almost zero, wasn’t it better to have debt rather than equity dilution ?

I have another point to add-They have a dividend payout ratio around 40% in last 3 years which comes to over Rs.27 crore in last 3 years. Why have such a large dividend payout ratio while you have Rs.100Cr expense coming up? This will be like funding dividends through equity dilution, which is not in the interest of shareholders.

The Inital QIP was planned to expand outside K’taka. However as the business got money from Mangalore PUC it didn’t dilute. Which in my view is the right thing. Subsequently the company has invested money in AP/Telangana through its partnership with Shri Gayatri and also in Robomate and its LMS.

The company hasn’t had the need to dilute for these purposes yet. Now given the growth it has been seeing in the robomate there is an opportunity to raise some money and grow faster.Raising debt in this environment could be a slow process. However debt is cheaper than equity.

Regarding dividends, I think they will cut/reduce the payout this year. They were not sure about the Robomate but my sense they have been positively surprised by the traction.

Hi,

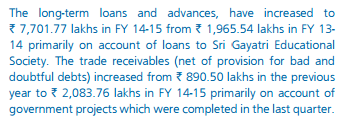

There is a 50 cr amount in “Loans and Advances to others” in the FY15 annual report of the company, for which there is no explanation anywhere and thus looks odd. Can anyone help in decoding the nature of this item?

This is the money that MT has paid to Shree Gayatri - the PUC which they are partnering in AP/Telangane. The company receives interest on the same to the tune of 10-11% .

In return of this loan. They have got an equity stake in the test prep business, whose numbers will start to come from FY17.

Hi guys, I am concerned about the “loans and advances to others” issue. The company states that it has given a loan to Sri Gayatri Educational Society…

Sri Gayatri does not carry this loan on its balance sheet

This does not add up according to me. How can one party carry the loan on its balance sheet and other party not. Can someone please provide some clarity on this. I could be missing something…but I think this is fairly important.

@maven26 According to Rohit’s reply, MT has loaned the money to Shri Gayatri. Maybe it was a mezzanine debt kind of deal wherein debt was converted into equity… I’m not sure. My point is if the loan is still outstanding it has to show up on the balance sheet of both parties. If it is not outstanding then it will not show up on the balance sheet of either party. It is not adding up. Any clarity would be much appreciated.

@rohitbalakrish_ can you please tell us where you found info about the loan. I did not find anything apart from the screenshots from the AR that I have posted.