What is the record date for bonus shares

Nirav… Promoters are increasing their stake since if someone were to buy

15k shares in markets it will hit UC… What is the link between MC and size

of promoter buying…

Yes Nirav you are right. the amount of 75 lacs does look meagre in front of the mcap of 250cr. However, given the fact that as early as last year, 75 lacs would have got him a 1.5% stake, his buying shares at 500 can have only 2 reasons :

- The fact that the company has a bright future can be seen with greater clarity now. One of the reasons for this could be the jackpot acquisition Singapore they have done

- This is a way to artificially prop up the price. General investors would now consider 500 as a floor and price the stock accordingly.

Only time will tell whether the reason for the allotment is 1 or 2.

1 Like

As per SME norms, each lot is priced to appx 1.25 lacs value evry time they review it. the reason for this is to keep small retail investors away as they may not fully understand the risks associated with such early stage investing.

3 Likes

thanks but what is the special case with MRSS that they want to keep (novice?) retail investors away? not all retail investors know all the risk factors of the companies that they are investing but not many of them do something like this. So I am keen to know why and how MRSS is different in this regard?

It’s a rule set by the exchange/SEBI, not MRSS.

1 Like

MRSS Annual report FY17 states this in chairman’s speech.

“A year ago, at the previous AGM we had announced that we will pursue acquisitions to achieve scale and that we will expand horizons to ASIA. We have been successful in concluding the 1st of what would be a series of acquisitions. This does not in any way mean that the organic growth is affected but this takes us closer to our Vision of being India’s 1st Market Research company to become the largest Independent MR agency in Asia.”

So, we can expect more acquisitions to happen in the coming years.

More importantly, the company has started generating big CFO and FCF. As per AR 17, the NP is Rs 4.63Cr and OCF is Rs 4.03 Cr and FCF is Rs 3.63 Cr. So, about 80% of NP is converted as FCF. This is a big positive as the company will have a bigger cash bag for acquisitions. This is inspite of the fact that debtor days is still quite big at 163 days. But a big improvement in debtor days from 203 days in FY16. If they bring down debtor days from here, they can generate FCF more than their NP.MRSS AR F.Y. 2016-2017.pdf (2.2 MB)

5 Likes

MRSS gets a financial accredition from Govt of Singapore which will enable them to bid for Singapore govt projects worth SG$ 10 M with each Govt department.MRSS 13th sep.pdf (592.2 KB)

4 Likes

This is very helpful. A clarification:

Traditional: Digital share is it 70:30 or 30:70? Thank you.

Disc: Invested and averaging up

Thanks for the exhaustive notes

Traditional is 70 and Digital share is 30.

Thanks for the detail updates. Did they mention by when do they plan to shift from the sme platform to the main exchange?

Isn’t it highly over valued ? company trading at some 300 Cr mcap and net profit is about 4 Cr.

I mean even if net profits grows 4x and Mcap remains the same then it will trade 15 time earnings. i don’t think the growth from low base should be extrapolated they do revenue of 24Cr <<<<< 300 Cr Mcap ?

I am just trying to understand from who are buying today whats the rationale ?

As we are approaching fy18, the expected sales is Rs. 60 crore plus… This

the price to sales becomes 5 times only…

It is a niche play with room for a rapid and long term growth… The stock

appeared expensive before every result till date… But moved up higher on

expected future growth…

MRSS board is meeting on 7th Nov, for a dividend and results. Pls note they have mentioned it as “First interimn dividend”…So there could be one more atleast a final dividend…![]() mrss 30th Oct.pdf (273.3 KB)

mrss 30th Oct.pdf (273.3 KB)

Mindblowing H1 results from MRSS

http://www.bseindia.com/xml-data/corpfiling/AttachLive/e81b6261-c3df-4b1b-bd9f-fc3f5083cb1f.pdf

Revenue up 111%

EBITDA up 165%

PAT up 167%

H1fy18 almost laps fy17 PAT

EBITDA margin shoots by 900bps

PAY margin shoots by 500 bps

Receivables as per normal industry norms

Main board listing soon ( one of the outcomes of the BM )

Stock is up 8x since i posted this thread and its not even been a year. So I will not comment on valuations.

Disclosure : Hold. Since my name comes in SHP will not specify what % of portfolio for privacy reasons

7 Likes

Really great set of numbers but feel the best is yet to come.

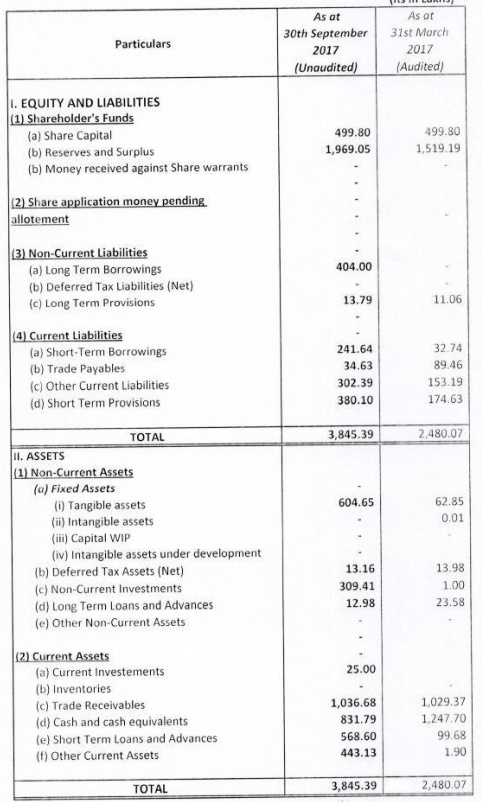

Had a quick look and found that the company had to go for a 4Cr long-term loan which is strange given that 19Cr as reserves and surplus (liability) of which 8.3 Cr is in the form of cash (asset). Any thoughts on why a company would like to go for a loan when they have enough in the bank?

Disc: Invested.

The loan was for purchase of property at Kanakia Zillion. Makes sense to take a loan and keep cash free for acquisitions and working capital

Utsav …

Does the H1 nos include MPA Singapore nos too…If no, from when it will be

aggregated…Also, the receivable days has halved in H1 18 compared to H1

17. Any views on what worked so well for company…

Disc: Invested from lower levels…

1 Like

These numbers do not reflect MPA numbers. They are the joker in the pack and can provide the zing in H2 numbers.

As far as receivables are concerned, I have always believed that as they grow in size, they will be able to negotiate better payment terms with their clients. Its a simple case of a new company bending over backwards to suit client demands to get business, and once set…push for better deals.

1 Like