MRSS India ( 539229 ), is a small company that is listed in the BSE SME exchange.

What attracted me to the company initially was the level of corporate information and disclosure they had put out, which was disproportionate to the market cap at which I entered the stock.

MRSS ( http://www.mrssindia.com/ ) is India’s only listed market research (MR) agency. What differentiates MRSS from the other MR agencies is the fact that they use the latest tech to conduct their surveys.

( http://www.mrssindia.com/about-mrss-india/leveraging-technology.aspx will give a better idea )

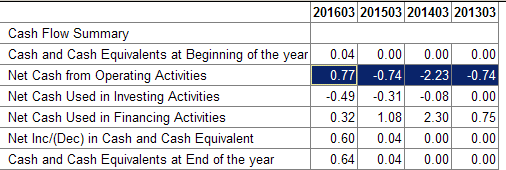

The company declared the following numbers for H2 ( quarterly numbers not disclosed by companies listed on SME platform )

http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/7A12BF9B_7398_42DB_919D_E83DD87E0D34_114541.pdf)

Digging deeper, I found the following information.

About the company

- the only listed market research (MR) co

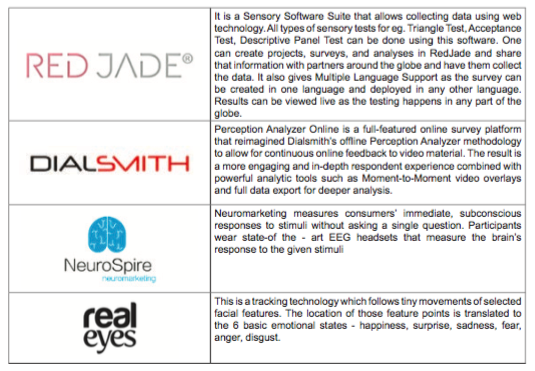

- specialists in digital MR. Have introduced technology such as eye movement tracking, pulse tracking , webcam based face reading, etc.

- top clients from across genres…including HUL, Voda , Cipla , Yamaha ,etc.

- impressive management lineup. For example, the guy who heads the auto practice is the guy who founded tatamotors MR division and worked there for 35 years.

- The MD Sarang Panchal used to head asia pacific region for AC Nielsen ( http://www.mrssindia.com/about-mrss-india/our-team.aspx )

- total 47 employees across 3 cities. Looking to increase headcount with increase in business.

- pure digital is currently 30% of rev…aim to take it to 60%

- 65% operating margin on pure digital work…after tech/direct/incentive costs

- 65% is repeat business. Look to maintain it at 65% despite aggressive client additions by increasing share of clients MR wallet.

About the numbers

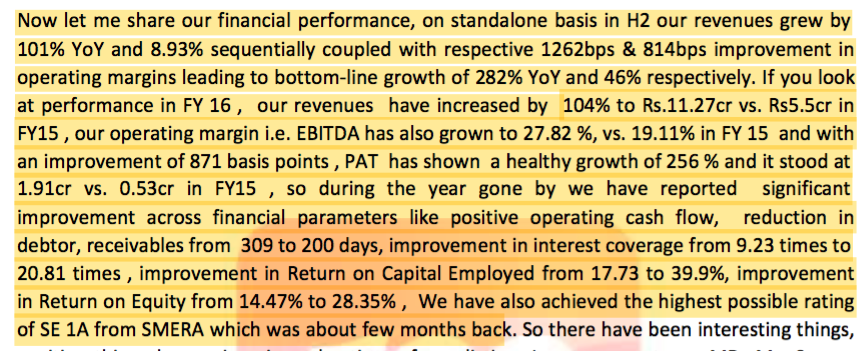

- H2 numbers are really impressive

- the co is growing at 100% cagr…should do around 20 cr revenue this year with 4-5 cr pat.

- Roce is upwards of 60%

- long term debt zero.

- margins improving due to operating leverage as well as higher proportion of billing of newer technology

- company gives a very detailed ppt about the numbers…very unlike a company with a sub 100cr mcap

( http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/FC43B8B4_B6B6_462D_9F2B_E1A40DC0E549_192657.pdf)

About the OFS

- 10 cr amount

- ~18% dilution

- promoter stake to come down to 61%

- lot size to be reduced from 2500 to 1200

- first ever follow on offer on bse sme platform

- 8.5 cr to be used for working capital. Rest as down payment for purchase of office at Mumbai. Currently on rent which will be saved driving margins even higher by 2.5% on current revenue level.

- OFS closed with 1.6 times oversubscription. Shares now listed

Areas for concern

- no bad debts till now…may change as clients get broad based.

- receivables are high. I guess as the company becomes larger , it will be able to command more stringent payment terms. As of now working cycles are long…typically 90 to 120 days after project finishes._ -

MD Sarang Panchal hardly owns any equity. is may get corrected when they issue ESOPs. Ideally I would like to see him pick up some shares from the open market

- No dividend - No q1 and q3 results…so no way to know what’s happening for 6 months. Hopefully, the stock should get listed on main BSE platform soon…thus bringing about more transparency.

- challenges are balancing growth and receivables, avoid complacency.

- company still small in terms of revenue

Size of runway

- Indian MR industry size only 4% of ad market compared to 11% in USA and 25% in UK

- Co has the potential to grow revenues 100% CAGR for next 2/3 years due to small base, size of opportunity and niche product offering

- recently added social research person…see huge upside

USP

- pioneering implicit research in india…not asking direct Qs

- huge demand for this service by clients which MRSS able to resolve thanks to technology…example : eye tracking glasses. Generates heat map of stimulus response.

- getting good work from tv channels…send ads of forthcoming serials to 1000 respondents and tracked 7 muscular responses via webcam

- best part is that the survey need not be done in a controlled environment…respondents can go about their lives as normal

- attracting global tech enquiries since listing

- aim to be a marketplace for MR tech

- the moat is in the research design

- deal only with large cos.

- co is causing disruption in the MR field

- barriers to entry is access to tech and contacts with clients

- no significant competitor right now

- key usp is fast TAT…typically takes 25% of time as compared to traditional methods

Disclosure : I own the company and applied in the FPO as well. Will look to add more as the story plays out.

MRSS aims To become the largest and most profitable Independent Asian MR agency by FY 2018.

I am betting on them to make it happen.

Mcap when posted : 70 cr ( post FPO )