I spent the past weeks researching GLP-1 drugs and companies that might benefit from these drugs, what follows is my notes on the topic -

disclaimer - i am not a doctor; most of my knowledge is from reading company fillings / clinical trials and scientific papers, i am long in some of the companies mentioned in this thread.

notes:

In the history of medicine, few drugs tower above all others, drugs which helped patients far beyond doctors’ initial expectations and continue to benefit millions of people every day. We have such a drug for obesity & diabetes - GLP-1 receptor agonists. Glucagon-like peptide 1 receptor agonists known as GLP-1 such as semaglutide and tirzepatide are a class of medications developed to treat diabetes and obesity. GLP-1 RAs have revolutionized the approach to obesity treatment, becoming the most effective non-surgical pharmacological intervention available. Current GLP-1 RAs such as once-weekly subcutaneous semaglutide help in mean body weight reduction of approx 15% in individuals with obesity; Dual glucose-dependent insulinotropic polypeptide (GIP) and GLP-1 receptor agonists, like once-weekly tirzepatide resulted in the mean body weight changes of -17.5%.

GLP-1 is a USD150–175bn global market opportunity over the coming decade. In the United States alone, the obesity epidemic affects over 100 million adults and almost 15 million children, representing 41.9% of the adult population and 19.7% of the child population, which has quadrupled over the last 30 years. Obesity is defined as having a BMI over 30.0 kg/m² and is linked to many significant chronic diseases, including diabetes, heart disease, and some types of cancer. This epidemic contributes to $173 billion in annual healthcare costs. The global market for obesity drugs could increase by more than 15-fold by 2030 as their use expands beyond weight loss to treat a range of diseases.

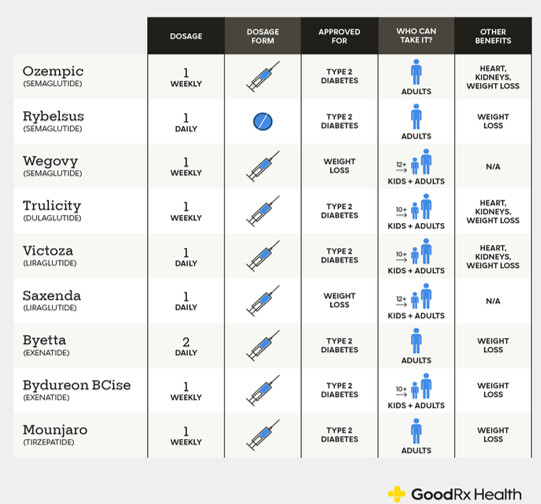

Two companies dominate the GLP-1 landscape: Novo Nordisk and Eli Lilly. Novo Nordisk’s portfolio includes liraglutide (Victoza® for diabetes, Saxenda® for obesity) and semaglutide (Ozempic® for diabetes, Wegovy® for obesity, and Rybelsus® as an oral tablet) – all GLP-1 analogues. Eli Lilly’s offerings include dulaglutide (Trulicity®, a once-weekly GLP-1 RA for diabetes) and tirzepatide (Mounjaro® for diabetes and Zepbound® for obesity, a dual GIP/GLP-1 agonist).

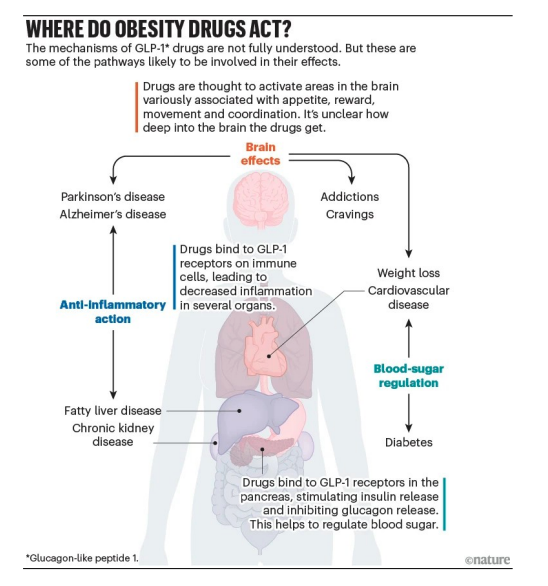

How can a weight loss drug do everything?

GLP-1 is a hormone secreted by special gut cells in your lower intestine whenever you eat carbohydrates, fats or proteins. The primary physiological role of GLP-1 is to connect nutrient consumption with glucose metabolism, acting as a crucial signal to the body that food has been consumed and metabolic adjustments are required. In its natural form, GLP-1 rises quickly after a meal, then vanishes within minutes, so it never makes it far enough to have a sustained therapeutic effect.

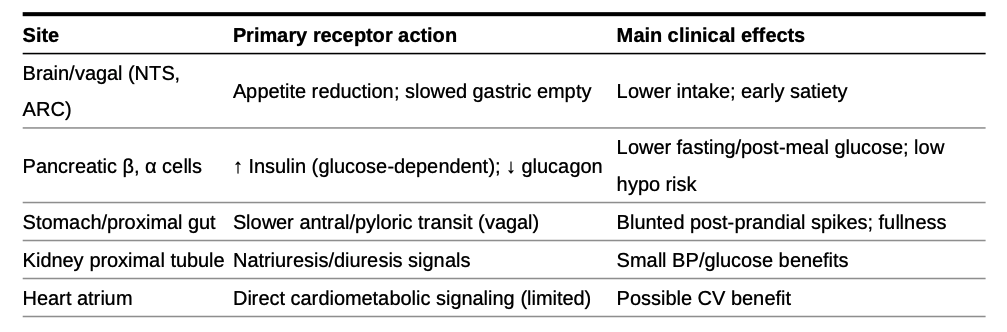

Once released, GLP-1 flips three key switches. In the brain, it triggers the feeling of fullness so you naturally eat less. In the stomach, it slows down how fast food empties into your intestines, extending that satisfied-after-a-big-meal feeling. And it triggers the pancreas to release more insulin lowering blood sugar and less glucagon raising blood sugar.

Drugs like semaglutide work because they combine a fatty-acid “tail” attached to the GLP-1 “head”. The head binds to, and activates, the GLP-1 receptors. The tail protects the head, because it is tough and sticky, slowing down the rate at which the body breaks it down.

The ability of GLP-1 RAs to do everything largely stems from the activation of GLP-1 receptors across numerous organs and tissues in the body, well beyond the pancreas. When the supercharged GLP-1 RAs enter the bloodstream and persist due to their prolonged half-life, they can activate these receptors in various locations, leading to a cascade of beneficial effects.

Currently Approved GLP-1 Drugs

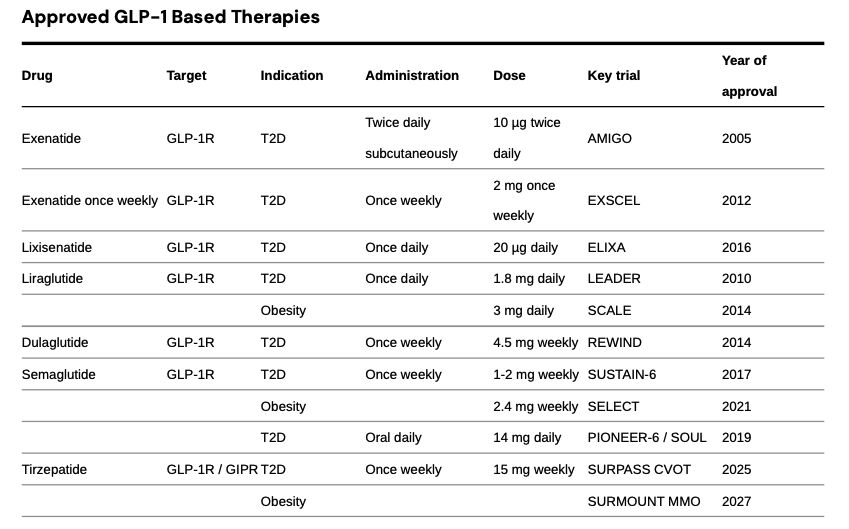

There are six FDA‑approved chronic weight‑loss drugs: orlistat, phentermine–topiramate, naltrexone–bupropion, liraglutide 3.0 mg (Saxenda), semaglutide 2.4 mg (Wegovy), and tirzepatide (Zepbound). Two are GLP‑1–based (liraglutide, semaglutide). Tirzepatide is a dual GIP/GLP‑1 agonist with its own obesity label. Saxenda, Wegovy, and Zepbound are subcutaneous injections; the others are oral.

Exenatide (Byetta; exenatide ER/Bydureon)

Exenatide, the first GLP‑1 RA (2005), is a synthetic exendin‑4 that resists DPP‑4. Byetta 5–10 µg BID lowered A1c with modest weight loss and inconvenient dosing. Bydureon 2 mg weekly improved adherence, but EXSCEL showed MACE noninferiority vs placebo. AstraZeneca discontinued Byetta and Bydureon BCise in the U.S. in Oct 2024.

Liraglutide (Victoza; Saxenda)- Once‑daily analog with proven CV benefit. LEADER: 3‑point MACE HR 0.87 with significant reductions in CV and all‑cause mortality. Saxenda 3.0 mg daily produces clinically meaningful weight loss (SCALE). Victoza generics entered 2024.

Dulaglutide (Trulicity)- Once‑weekly 0.75–4.5 mg with broad primary‑care reach. REWIND showed MACE reduction (HR 0.88) in a population with mostly multiple risk factors and ~31% established CVD; the U.S. label includes reduction of MACE in T2D with CVD or risk factors. Data support renal benefit signals (slower eGFR decline, fewer new macroalbuminuria events).

Semaglutide (Ozempic; Rybelsus; Wegovy) - Single‑agent backbone across diabetes, obesity, and CV risk reduction. Ozempic weekly for T2D; Rybelsus oral for T2D; Wegovy 2.4 mg weekly for obesity and for reducing CV risk in adults with established CVD and overweight/obesity (FDA label March 2024, supported by SELECT: 20% MACE reduction, HR 0.80). SUSTAIN‑6 showed MACE reduction (HR 0.74) but no significant mortality reduction; PIONEER‑6 established CV safety for oral dosing. STEP‑1 showed ~15% mean weight loss at 68 weeks.

Tirzepatide (Mounjaro; Zepbound) - Dual GIP/GLP‑1 agonist setting the efficacy bar. In T2D, SURPASS trials beat semaglutide 1 mg on A1c and weight (e.g., SURPASS‑2). In obesity, SURMOUNT‑1 showed ~15–21% mean weight loss at 72 weeks and head‑to‑head data show greater loss than semaglutide in non‑diabetic obesity. U.S. approvals: T2D (Mounjaro, 2022), obesity (Zepbound, 2023), and obstructive sleep apnea with obesity (Zepbound, 2024)

Ongoing Innovations in GLP-1s Landscape

The obesity pipeline from phase 1 to market now includes 173 drugs, with GLP-1 and combination therapies accounting for majority of trials. We are seeing innovations happening in the oral GLP-1s, dual GIP/GLP‑1 and GLP‑1/glucagon co‑agonists, triple GIP/GLP‑1/glucagon agonists, and amylin co‑agonists.

Oral Formulations

oral GLP-1 are 1) much easier to manufacture at scale compared to the current injectable GLP-1 drugs, 2) much simpler to distribute globally, given no need for cold-chain storage, 3) more attractive for needle-phobic patients who avoid the injectable GLP-1 drugs currently available, and 4) better suited to long-term maintenance therapy, given what we expect will be lower pricing (and lower costs) for orals compared to injectable GLP-1 drugs.

| Drug |

Company |

Description |

Current Phase |

Mechanism |

| SMALL MOLECULES |

|

|

|

|

| Orforglipron |

Eli Lilly |

First oral small molecule GLP-1 receptor agonist with no food/water restrictions; achieved 27.3 lbs weight loss in Phase 3 |

Phase 3 |

GLP-1 RA |

| Aleniglipron (GSBR-1290) |

Structure Therapeutics |

Small-molecule GLP-1 agonist; Phase 2b ACCESS studies fully enrolled, results by year-end 2025 |

Phase 2b |

GLP-1 RA |

| AZD5004/ECC5004 |

AstraZeneca/Eccogene |

Oral small molecule showing 5.8% weight loss in 4 weeks; currently in global Phase 2b VISTA and SOLSTICE trials |

Phase 2b |

GLP-1 RA |

| CT-996 |

Roche/Genentech |

Once-daily oral small molecule; 6.1% placebo-adjusted weight loss in 4 weeks; advancing to Phase 2 |

Phase 2 |

GLP-1RA (biased) |

| PEPTIDES |

|

|

|

|

| Oral Semaglutide (Rybelsus) |

Novo Nordisk |

First and only FDA-approved oral GLP-1 (since 2019); 25mg version pending approval for weight management |

Approved/Ph3 |

GLP-1 RA |

| HRS-953 |

Hengrui Pharma |

Oral GLP-1 receptor agonist in late-stage development for obesity and type 2 diabetes |

Phase 3 |

GLP-1 RA |

| DUAL AGONISTS |

|

|

|

|

| Amycretin |

Novo Nordisk |

Dual GLP-1/amylin receptor agonist; 13.1% weight loss at 12 weeks; Phase 3 starts Q1 2026 |

Phase 3 |

GLP-1/Amylin |

| VK2735 |

Viking Therapeutics |

Dual GLP-1/GIP agonist; oral Phase 2 fully enrolled, results expected H2 2025 |

Phase 2 |

GLP-1/GIP |

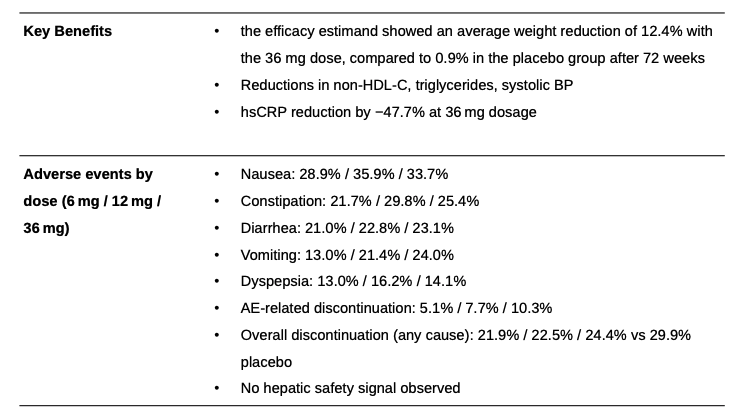

Eli Lilly - Orforglipron (oral, small‑molecule GLP‑1 RA)

Orforglipron is an oral, non-peptide, small-molecule GLP-1 receptor agonist developed by Eli Lilly. The drug is taken once daily by mouth without food or water restrictions and has an elimination half-life of 29 to 49 hours. Eli Lilly reported phase 3 clinical data for its oral GLP-1 drug orforglipron (orfor) on 7 August 2025. That data was presented in the ATTAIN-1 trial, and measured weight loss in an obese patient population. While the ATTAIN-1 trial successfully met its predetermined weight loss endpoints versus placebo, the weight loss percentage realized in the highest dose fell modestly short of investor expectations, with average weight loss of 12.4% versus placebo at 0.9%. most common side effect were mild to moderate gastrointestinal related, treatment discontinuations due to adverse effects across the three doses were 5.1% , 7.7% and 10.3% respectively versus 2.6% for placebo.

Orforglipron’s weight loss is disappointing and falls short of street expectations. Discontinuation rates however are better than expected. Orforg is likely still a viable option for needle-phobic obese patients without food effects and greater manufacturing scalability. Though weight loss data may be a harder sales pitch relative to generic semaglutide.

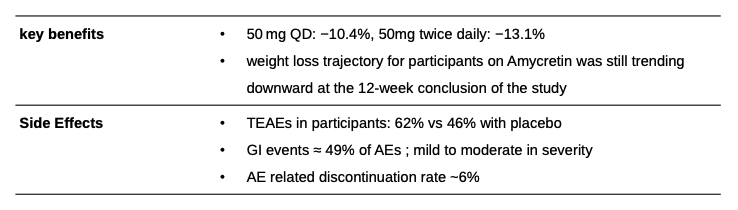

Novo Nordisk - Amycretin (2x50mg daily oral)

Amycretin is a novel, single-molecule co-agonist that targets two different receptors: the GLP-1 receptor and the amylin receptor. Amylin is another natural hormone that is co-secreted with insulin from the pancreas after meals and plays a role in glucose regulation and appetite control. By activating both of these pathways, Amycretin is designed to have a more potent and potentially complementary effect on weight loss compared to a GLP-1 agonist alone. Novo Nordisk recently published first-in-human data for Amycretin and is advancing both oral and subcutaneous formulations of Amycretin into Phase 3 development for weight management. Oral amycretin Phase 1 trial - The trial evaluated the single-ascending dose and multiple ascending doses for oral amycretin, up to 2x 50 mg, in 144 people with overweight or obesity, with a total treatment duration of up to 12 weeks.

After 12 weeks of treatment with amycretin up to 50 mg and up to 2x 50 mg, participants achieved a mean change in body weight of -10.4% and -13.1% respectively, compared to -1.2% with placebo. GI-related side effects were the most common, accounting for approximately 49% of all adverse events.

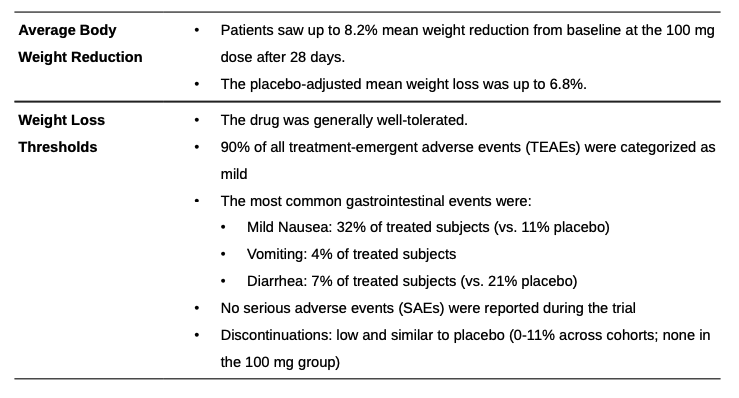

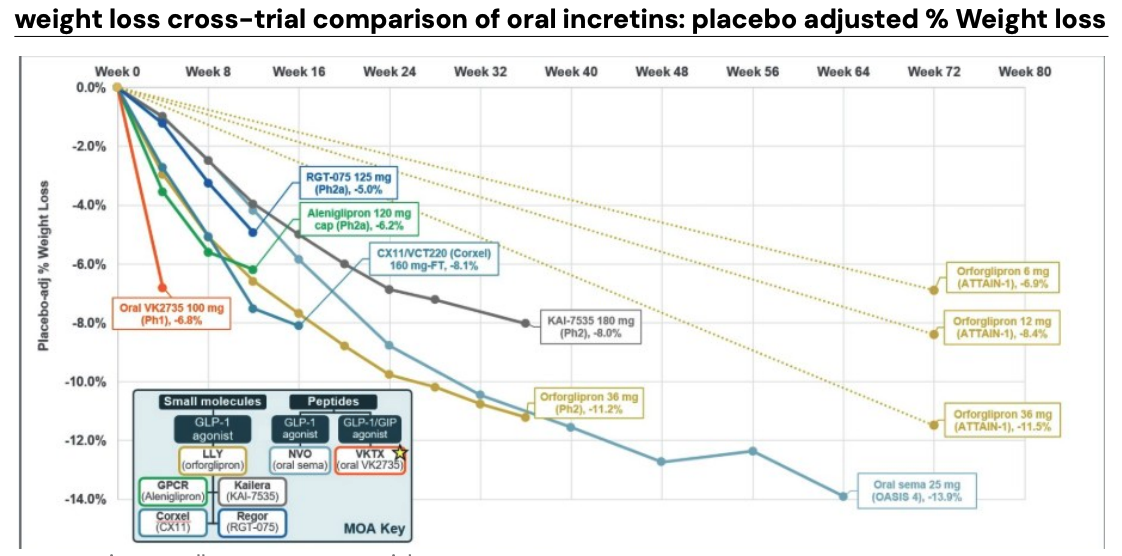

Viking Therapeutics - VK2735 (oral, dual GLP‑1/GIP agonist)

Viking Therapeutics is actively developing VK2735, a dual agonist of glucagon-like peptide-1 (GLP-1) and glucose-dependent insulinotropic polypeptide (GIP) receptors, with both subcutaneous and oral formulations in its pipeline.

Viking’s tablet formulation of VK2735 completed a 28‑day multiple‑ascending‑dose Phase 1 trial in adults with obesity (BMI ≥ 30 kg/m²). Doses from 2.5 mg to 100 mg were titrated weekly. The 100 mg cohort achieved an 8.2% mean weight loss from baseline (‑6.8% placebo‑adjusted) in just four weeks, with the trajectory still trending downward at Day 28 and durability to Day 57 (‑8.3% from baseline four weeks off-drug).

VK2735 delivers the steepest early weight loss slope among oral agents (‑8% in 4 weeks). If the curve remains linear, it could meet or exceed Amycretin’s 12 week benchmark, while its mild GI profile and balanced discontinuation rates provide a tolerability edge over Orforglipron.

Novel Mechanisms

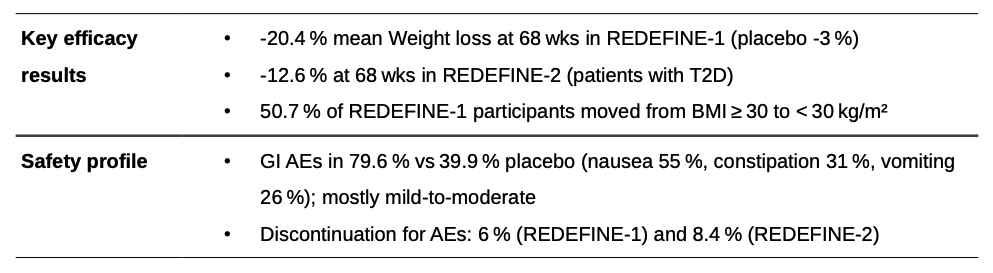

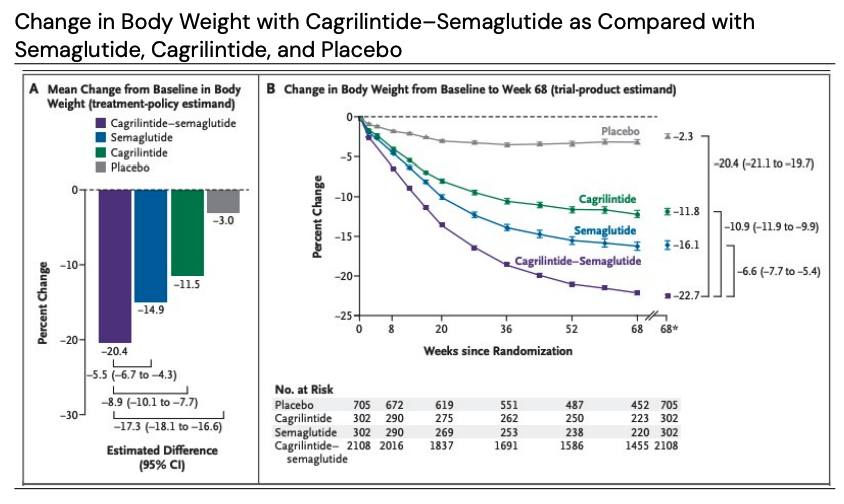

Novo Nordisk - CagriSema (once‑weekly, subcutaneous)

CagriSema is a fixed-dose combination of a long-acting amylin analogue, cagrilintide 2.4 mg and semaglutide 2.4 mg. This combination is designed to provide synergistic effects on weight loss and glycemic control by targeting both amylin and GLP-1 receptors.

REDEFINE is a phase 3 clinical development program with once-weekly subcutaneous CagriSema in obesity. REDEFINE 1 and REDEFINE 2 have enrolled approximately 4,600 adults with overweight or obesity. REDEFINE 1 was a 68-week, double-blind, placebo- and active-controlled efficacy and safety phase 3 trial of once-weekly CagriSema, cagrilintide 2.4 mg and semaglutide 2.4 mg versus placebo in 3,417 adults with obesity or overweight with one or more comorbidities and without type 2 diabetes. REDEFINE 2 was a double-blind, randomized, placebo-controlled 68-week efficacy and safety phase 3 trial of once-weekly CagriSema versus placebo in 1,206 adults with type 2 diabetes and either obesity or overweight.

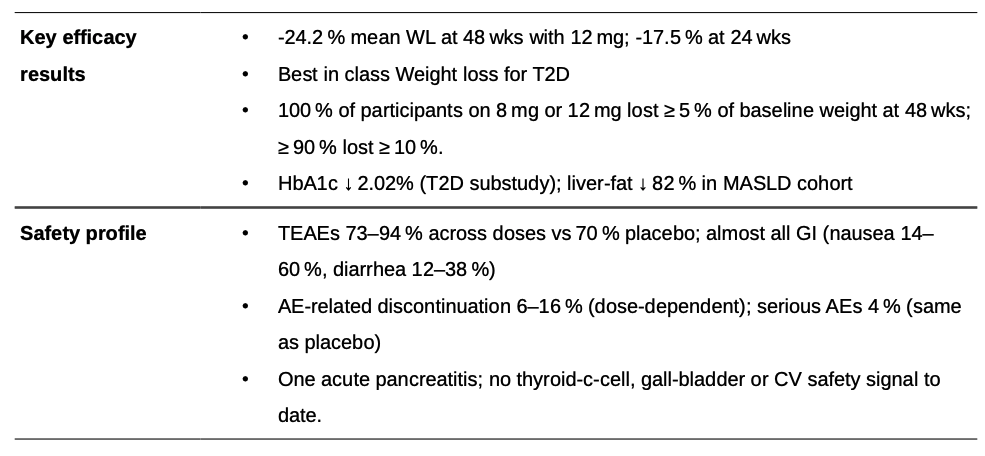

Eli lilly - Retatrutide (Once weekly, subcutaneous)

Retatrutide is a novel, once-weekly injectable triple agonist that targets the glucose-dependent insulinotropic polypeptide (GIP), glucagon-like peptide 1 (GLP-1), and glucagon receptors. Most weight loss occurred within the first 24 weeks, suggesting patients don’t need to wait a year to see clear results. For weight reduction, 92% of participants on 4 mg, 100% on 8 mg, and 100% on 12 mg achieved a 5% or more reduction at 48 weeks.

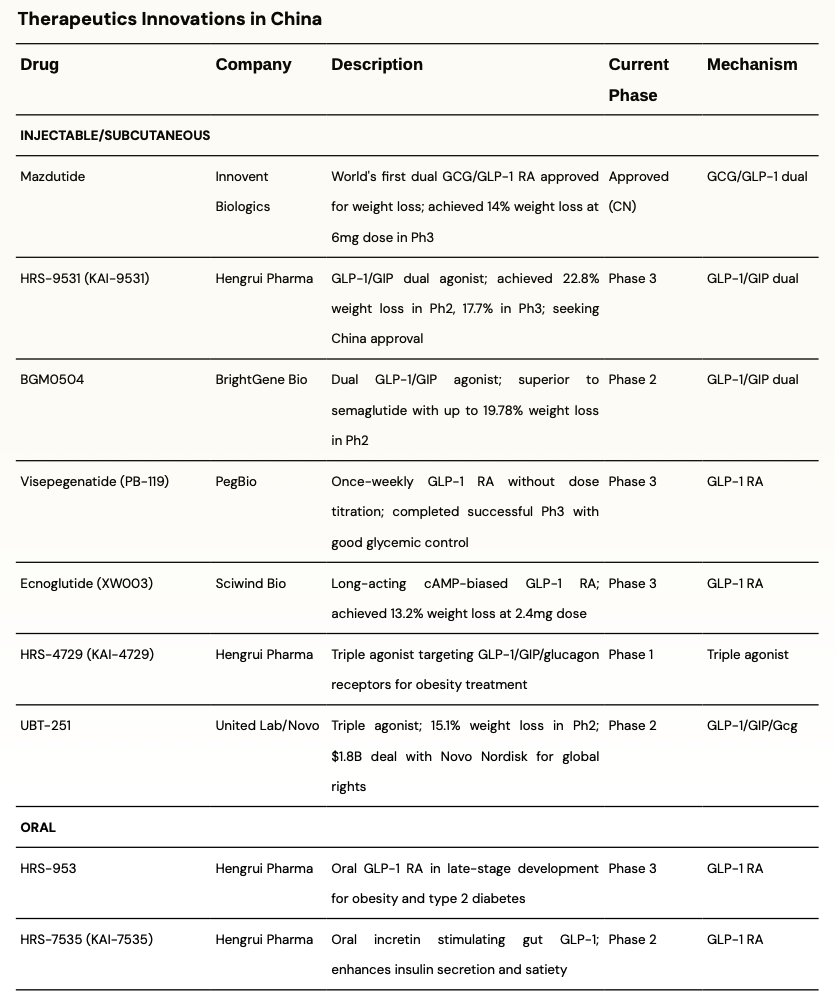

There are some interesting developments from China; the table below summarizes some interesting ones -

Developments in Indian GLP-1 market

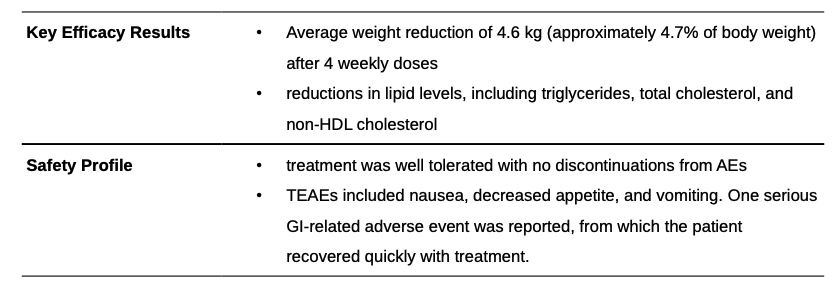

Sun Pharma - Utreglutide (GL0034) (injectable, GLP-1 RA)

Utreglutide is a novel, long-acting GLP-1 receptor agonist being developed by Sun Pharma. It is a once-weekly subcutaneous injection for the treatment of obesity and other metabolic diseases. Healthy, obese male participants (n=24; Age 18-40; BMI ≥ 28 kg/m²) were enrolled into a fixed-dose Cohort 1 (4 x 680 µg) or an increasing-dose Cohort 2 (680/900/1520/2000 µg) and assigned to treatment groups in a 3:1 ratio, receiving 4 weekly doses of either GL0034 or a placebo

Understanding Value Chain

Two companies dominate the GLP-1 landscape: Novo Nordisk and Eli Lilly. Novo Nordisk’s portfolio includes liraglutide (Victoza® for diabetes, Saxenda® for obesity) and semaglutide (Ozempic® for diabetes, Wegovy® for obesity, and Rybelsus® as an oral tablet) – all GLP-1 analogues. Eli Lilly’s offerings include dulaglutide (Trulicity®, a once-weekly GLP-1 RA for diabetes) and tirzepatide (Mounjaro® for diabetes and Zepbound® for obesity, a dual GIP/GLP-1 agonist).

Methods of GLP-1 production

Solid Phase Peptide Synthesis (SPPS) – Eli Lilly produces its peptide APIs, like tirzepatide, using hybrid chemical synthesis platform. This method first creates smaller peptide fragments through the more controlled Solid-Phase Peptide Synthesis (SPPS). These highly pure, pre-assembled fragments are then joined together in a solution, a process known as Liquid-Phase Peptide Synthesis (LPPS), often utilizing continuous manufacturing technology. The key advantage of this method is that peptide synthesis can be segregated and different partners can produce parts of the final peptide drug substance for better utilization of the supply chain. This method is chemically intensive, requiring significant volumes of solvents and reagents which makes it costly.

Fermentation based synthesis – Novo Nordisk’s GLP-1 products are mainly produced through fermentation-based synthesis. It is relatively lower in cost compared to SPPS but difficult to outsource manufacturing. Novo Nordisk maintains tight in-house control over this entire, complex value chain.

Novo Nordisk leverages its deep expertise in fermentation-based API production, manufactures its GLP-1 APIs almost entirely in-house. In contrast, Eli Lilly utilizes a more outsourced manufacturing model for its chemically synthesized APIs. It relies on a network of CDMOs like WuXi AppTec & PolyPeptide Group among many other players. Eli lilly is building in house capacities as well as taking steps to diversify its Tirzepatide API supplies which are heavily dependent on China currently to European CDMOs & Divi’s in India.

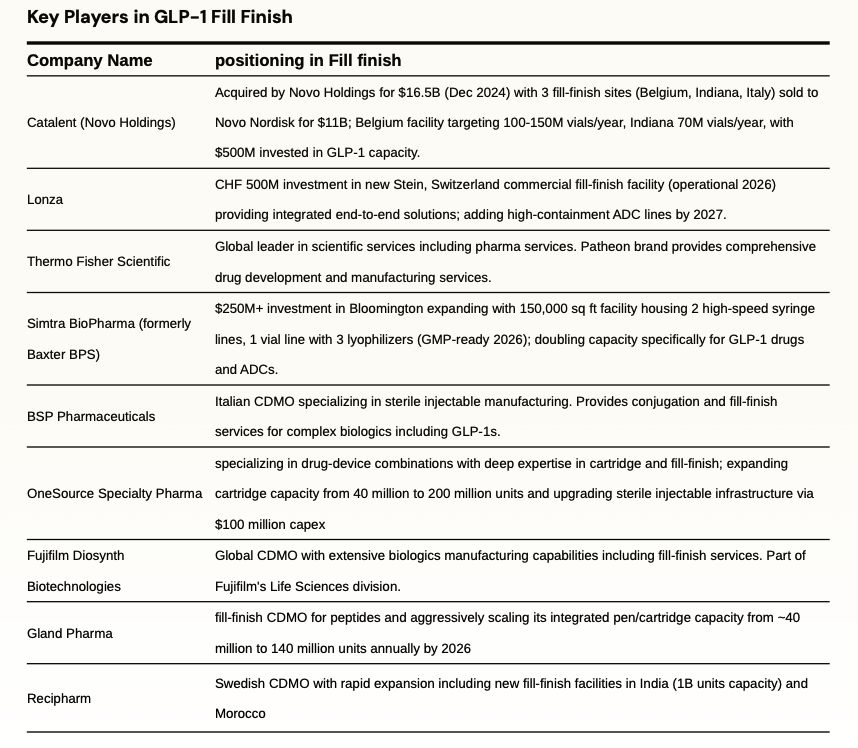

fill finish

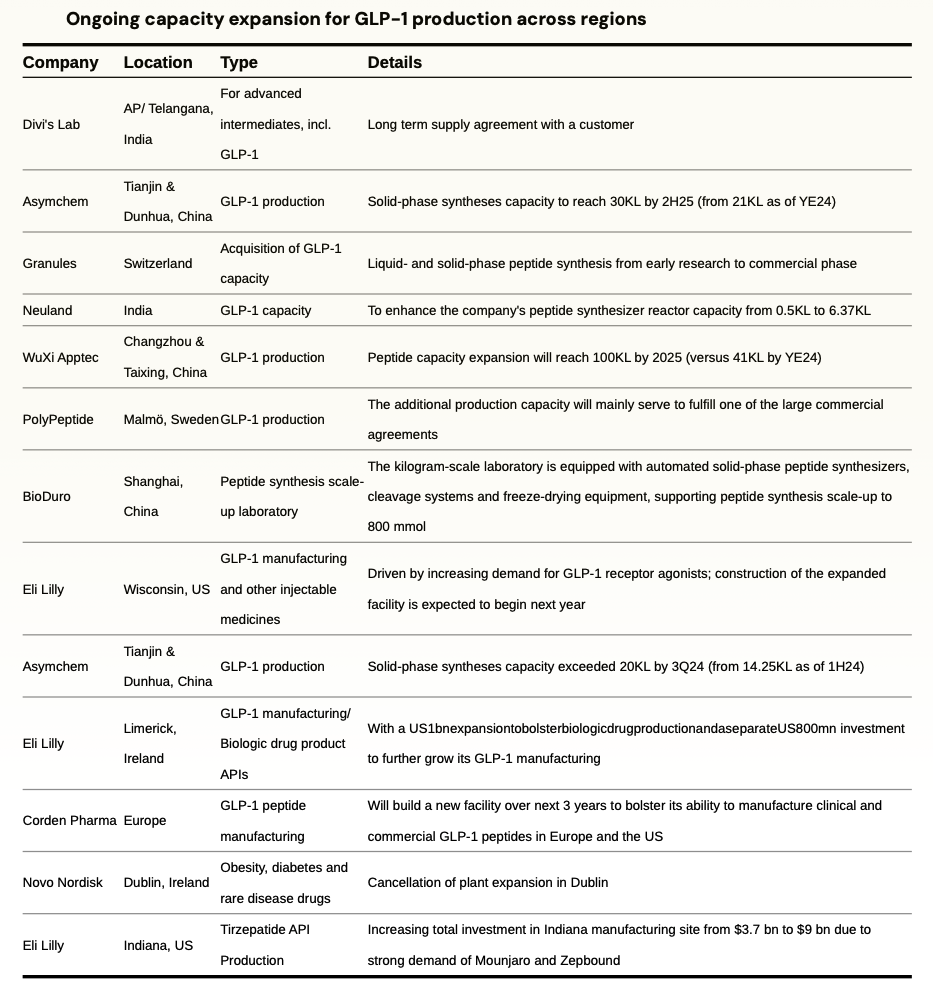

Fill–Finish refers to the final step of the manufacturing process that entails sterilization and standardization of medical containers and addition of drugs to the containers before sealing them. Both LLY and NVO were capacity-constrained, which limited the volume of sellable GLP-1 doses and caused shortages and are undergoing massive capex plans to expand capacity, including fill and finish pen device capacity, which represents the most significant bottleneck in the supply chain.

Novo Nordisk is investing $4.1 billion in a new 1.4-million-square-foot facility in Clayton, North Carolina, dedicated to filling injection pens for Ozempic and Wegovy. This massive fill-finish plant—with completion phased between 2027 and 2029—will match the combined floor space of Novo’s three existing U.S. sites. The company is also ramping in-house pen filling in Europe. Additionally, parent company Novo Holdings completed its $16.5 billion acquisition of CDMO Catalent in December 2024, immediately selling three strategic fill-finish sites (Anagni, Italy; Bloomington, Indiana; Brussels, Belgium) to Novo Nordisk for $11 billion. These sites will begin contributing to GLP-1 pen capacity from 2026 onward.

Eli Lilly has raised its Lebanon, Indiana investment to $9 billion (up from an initial $3.7 billion) to scale tirzepatide API production, with operations starting late 2026 and full ramp by 2028. In April 2024, Lilly acquired Nexus Pharmaceuticals’ Pleasant Prairie, Wisconsin injectable facility and is investing an additional $3 billion to expand it, with production expected to begin by 2027. Lilly has also partnered with contract manufacturers—including Resilience in the U.S. and BSP Pharmaceuticals in Italy—to add pen-filling and finishing capacity for Mounjaro and Zepbound.

Onesource speciality

OneSource Specialty Pharma is an India-based CDMO spanning biologics, complex injectables, soft-gel capsules, and drug-device combos. Five USFDA-audited Bengaluru plants can output over 100 m sterile doses, 2.4 bn capsules, and assemble autoinjectors and pens. The company is investing $100 million to expand production fivefold (increasing cartridge filling from ~40 million to 200+ million doses annually) to support day-one generic launches post-2026. Management expects GLP-1 generics to contribute over 10% of revenue in the first full year of launch and is targeting a 15–20% share of the global generic GLP-1 market by FY2028.

gland pharma

Gland Pharma makes sterile injectables for global markets with USFDA and EMA cleared sites in India and Europe. It sells via B2B development and CDMO work and via own-file launches, and it added EU capacity through the Cenexi deal. Formats include vials, prefilled syringes, cartridges, bags, and lyophilized drugs across oncology, anti-infectives, ophthalmics, and hormones. It has entered GLP-1 with a liraglutide launch and has two GLP-1 supply contracts. Cartridge output is rising from 40 million units by adding 100 million more by CY2026, with new lines for pens and cartridges. It targets GLP-1 fill-finish in cartridges and pens for partners in regulated markets.

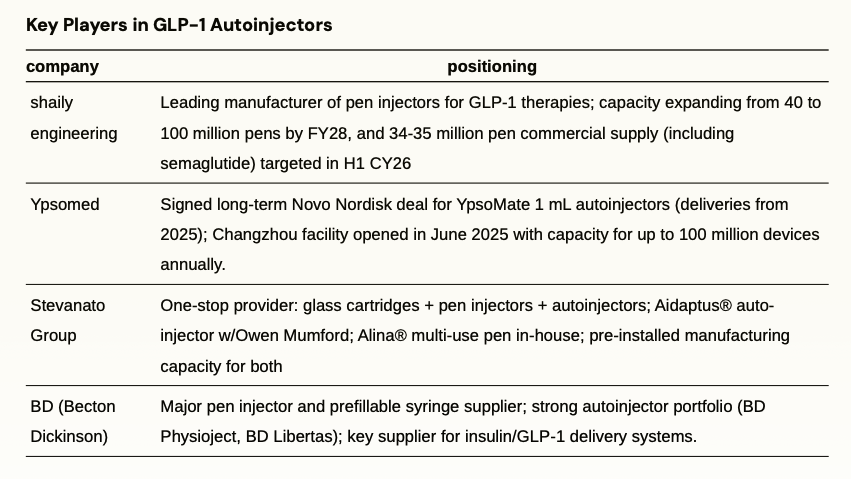

Autoinjectors & Drug Devices

Autoinjectors deliver pre-measured doses through spring-loaded needles that activate with a button press, eliminating manual injection steps. These devices reduce dosing errors and improve compliance for weekly GLP-1 therapy. With the patent expiry of semaglutide in emerging markets; GLP-1 volumes will see substantial growth which will drive massive demand for pen and autoinjectors.

shaily engineering

Shaily Engineering Plastics is a leading Indian manufacturer of value-added, precision-molded plastic products, supplying global majors across healthcare, consumer, and industrial sectors, with over 75% of FY25 revenues from exports and long-standing relationships with clients like Sanofi, Aurobindo, IKEA, and GE Appliances. Shaily has invested heavily in its healthcare vertical, now comprising advanced drug delivery and injectable device platforms. The company is rapidly scaling as a contract manufacturer for GLP-1 therapies, including commercial launches of pen injectors for semaglutide and upcoming supplies for tirzepatide and dulaglutide devices, supported by seven pen platforms developed in-house and through its UK subsidiary. Shaily has signed eight contracts for pen and auto-injector platforms—particularly for semaglutide and related drugs— with first commercial supplies in FY26, and is expanding pen manufacturing capacity from ~40 million to 80–90 million pens a year, targeting both generic and innovator pharma in regulated and growth markets such as Canada and Brazil.

second order effects from GLP-1 drugs

| Category |

Second Order Effect |

| Food & Beverage Consumption |

Reduction in overall caloric intake and grocery spending; decline in demand for high-calorie foods, soft drinks, juice and alcohol; greater interest in nutrient-dense, smaller portions and functional foods |

| High-Protein & Functional Foods |

Shift towards high‑protein bars, shakes and nutritional supplements; growth of meal replacement drinks, macronutrient blends, and GLP-1 nutrition products |

| Frozen Foods & Grocery |

GLP‑1 users purchase more frozen fruits and vegetables and seek high‑protein frozen meals; interest in portion-controlled and healthy frozen foods |

| Apparel & Fashion |

Shifts in clothing sizes: more demand for smaller sizes, activewear and athleisure; potential decline in plus-size and big & tall lines; retailers must adjust inventory and size curves |

| Fitness & Exercise |

Rising demand for resistance training, gym memberships, and digital fitness programs tailored for GLP‑1 users; gyms and wellness platforms offering programs to prevent muscle loss |

| Aesthetics & Skin tightening |

Rapid weight loss causes skin laxity (“Ozempic face”), loss of facial volume and sagging skin; increased demand for fillers, Botox, radiofrequency microneedling, high‑intensity focused ultrasound (HIFU), fractional lasers, body contouring and hair restoration treatments |

| Sleep Apnea & Medical Devices |

Although GLP‑1-induced weight loss reduces apnea severity, many patients still require CPAP machines; GLP‑1 users are more likely to adhere to therapy; obesity is not the sole cause of sleep apnea |

| Bariatric Surgery & MedTech |

GLP‑1 drugs reduce the need for bariatric surgery, leading to lower procedure volumes and impacting companies providing surgical instruments and hospitals |

| Mental Health & Psychosocial Effects |

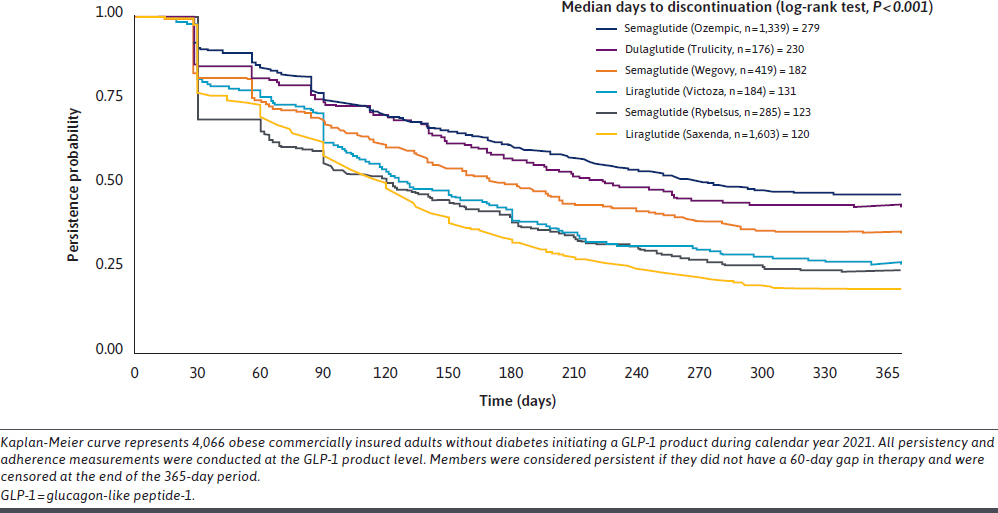

GLP‑1 drugs quiet “food noise” and improve self-efficacy but may trigger mood changes, depression, anxiety, or altered pleasure responses; weight loss can exacerbate body image concerns and disordered eating; half of users discontinue due to side effects |

| Travel & Leisure |

High cost of GLP‑1 drugs may reduce discretionary spending on travel and entertainment initially, but improved self-confidence could later increase demand for active vacations and wellness tourism |

| Dialysis & Renal Care |

Improved glycemic control from GLP-1 slows progression to end-stage renal disease, moderating dialysis patient growth |

| Retail Pharmacy & Tele-health |

Spike in direct-to-consumer demand for GLP-1 prescriptions and refill logistics |

Indian Obesity Landspace & Opportunity

Obesity rates in India are rising with obese/overweight adult population potentially growing from 180mn in 2025 to 450mn in 2050. Obesity rates for women in India increased from 1.2% in 1990 to 9.8% in 2022, and for men from 0.5% to 5.4%. According to NFHS-5, 24% of women and 23% of men in India are overweight or obese. India has more than 100m diabetic patients with an equal number in pre-diabeties. India is considered “diabetes capital” of the world.

Market for GLP-1s is still nascent in India but is growing rapidly evident by rapid growth in sales for Wegovy and Mounjaro. Mounjaro (priced at 14000-17500 per dose) has crossed Rs 100 crore in sales in India in just four months of launch, making it one of the country’s fastest-growing prescription brands ever by value.

A host of Indian companies are gearing up to launch semaglutide generics when the core patent expires in March 2026. Adoption of GLP-1s can be rapid in India, given India has over 100 million obese adults and another 180 million overweight individuals. Companies directly involved in supply chain - APIs, fill-finish, autoinjectors, manufacturers will be the obvious beneficiaries. As adoption for GLP-1s picks up, second-order effects will be visible across multiple industries like diagnostics, dairy/protein, hospitals, fast food chains, restaurants; however, these effects are likely to emerge gradually over the coming years.

patent expiry for GLP-1 drugs across markets

| Company |

Molecule |

Brand Name |

Mode of administration |

First US Patent Expiry |

Canada |

Brazil |

India |

| Novo |

Semaglutide |

Ozempic |

Injectable |

2031 |

Jan 2026 |

Mar 2026 |

Mar 2026 |

| Novo |

Semaglutide |

Wegovy |

Injectable |

2031 |

Jan 2026 |

Mar 2026 |

Mar 2026 |

| Novo |

Semaglutide |

Rybelsus |

Oral |

2031 |

Jan 2026 |

Mar 2026 |

Mar 2026 |

| Eli Lilly |

Tirzepatide |

Mounjaro |

Injectable |

2036 |

2036 |

2036 |

2036 |

| Eli Lilly |

Tirzepatide |

Zepbound |

Injectable |

2036 |

2036 |

2036 |

2036 |

Positioning of Indian Pharma companies in GLP-1s

| company |

positioning |

| Shaily Engineering |

Leading manufacturer of pen injectors for GLP-1 therapies; capacity expanding from 40 to 100 million pens by FY28, and 34-35 million pen commercial supply (including semaglutide) targeted in H1 CY26 |

| Gland Pharma |

fill-finish CDMO for peptides and GLP-1s; launched liraglutide in Q4 FY25 and aggressively scaling its integrated pen/cartridge capacity from ~40 million to 140 million units annually by 2026 |

| Divi’s Laboratories |

leading peptide API partner for global innovators, offering both solid-phase (SPPS) and liquid-phase peptide synthesis (LPPS), with recently commissioned SPPS capacity and strong backward integration into high-purity peptide fragments ; actively expanding its portfolio in GLP-1 and related analogs, working with several innovators at multiple stages |

| Nueland Laboratories |

Over 15 years of proven expertise in peptide chemistry, including complex purification and large-scale capabilities; expanding peptide manufacturing from 0.5 KL to 6.37 KL; engaged on multiple peptide projects including late-stage/Phase-3 candidates in the CDMO pipeline |

| OneSource Specialty |

specializing in drug-device combinations with deep expertise in cartridge and fill-finish; expanding cartridge capacity from 40 million to 200 million units and upgrading sterile injectable infrastructure via $100 million capex focused on new drug-device lines and lyophilization |

| Lupin |

advancing its pipeline with internal and partnered development of oral and injectable Semaglutide targeting the first wave in India and select ex-India markets by FY27 |

| Dr Reddy |

Global leader preparing Day-1 semaglutide launch across 87 countries including india, canada, brazil; building a robust global pipeline of peptides including GLP-1s |

| Sun pharma |

GL0034 (Utreglutide) Phase-1 completed showing promising weight loss results; ramping peptide manufacturing and has pen delivery partnerships to enable a Day-1 semaglutide launch in India |

| Glenmark pharma |

First to launch liraglutide biosimilar Lirafit™ in India, capturing over 65% share in the Indian liraglutide segment with ~70% lower therapy cost; expanding its GLP-1 and anti-diabetic injectable portfolio. |

| eris lifesciences |

developing synthetic and recombinant semaglutide with validation underway at its EU-GMP injectables sites; scaling up fill-finish capacity with a cartridge line at Bhopal, targeting one of the first GLP-1 launches in India/ROW from March 2026 |

| torrent pharma |

gearing up for first-wave launches of both oral and injectable semaglutide in India from 2026; phase 3 trials for oral underway and injectable secured via partnership; building capabilities and IP in complex peptides |

| cipla |

Early-mover securing early partnerships for pen delivery and targeting launch by March 2026 |

| zydus lifesciences |

targeting day-one launch of generic semaglutide in India and other emerging markets post-patent expiry |