In my opinion, in a bull market (like we are in) earnings of Brokers and AMC companies will necessarily be higher and they will continue to post great numbers QOQ/ YOY due to addition of new clients/increased options turnover/ increased market activity. Operating leverage is at play in AMC companies because increased revenue doesn’t necessitate corresponding increase in expense.

But the bigger risk always remains sebi intervention (like the recent f&o decision which brought a fall in price) or whenever the bears take over ( which is to say when the music stops) and that’s when revenue growth will take a hit

Discl : Invested

3 Likes

That’s how markets treat cyclical companies. Low P/E is an indicator of peak earnings and P/E will soon expand as earnings go south. I could be wrong in this case, but this is the modus operandi of cyclical stock price psychology.

Discl: No positions.

4 Likes

You can’t value it on simple parameter like P/E as earning has many components.

1.Operating business includes broking and capital markets + Asset and wealth management + Housing Finance.

2.Valuation of these components vary between 10-40 times earning.

3.They also have 7000Cr which is invested in Equity + PE… on which they book MTM gains/loss…this should be valued at book at max.

Invested

4 Likes

Motilal is 4x from last year when I explained there is huge margin of safety. These opportunities come very rarely and you should allocate heavy and then let compounding do it’s magic. It was my top allocation and yes you could always add more in hindsight but it had reached my maximum allocation. Yes all its earnings are linked to market but it was great play to FnO mania that’s going on. You are casino owner and collect money from gamblers.

5 Likes

Correct. Most of their multiple rerating is because of their wealth management business. If you look at multiples (market cap/EBITDA) of Nuvama, there is still quite a bit of runway left for MFS stock.

2 Likes

In Motilal’s case it’s not true. While AMC business tends to be cyclical, linked to market cycles, wealth management business is a lot more secular. MFS’s revenue mix is more concentrated towards wealth management and that’s why stock is getting rerated.

Stock is still trading below 10 year historical averages so I don’t see any concerns for valuation, especially in the light of their increasing focus on wealth management which commands higher valuations than an AMC business.

4 Likes

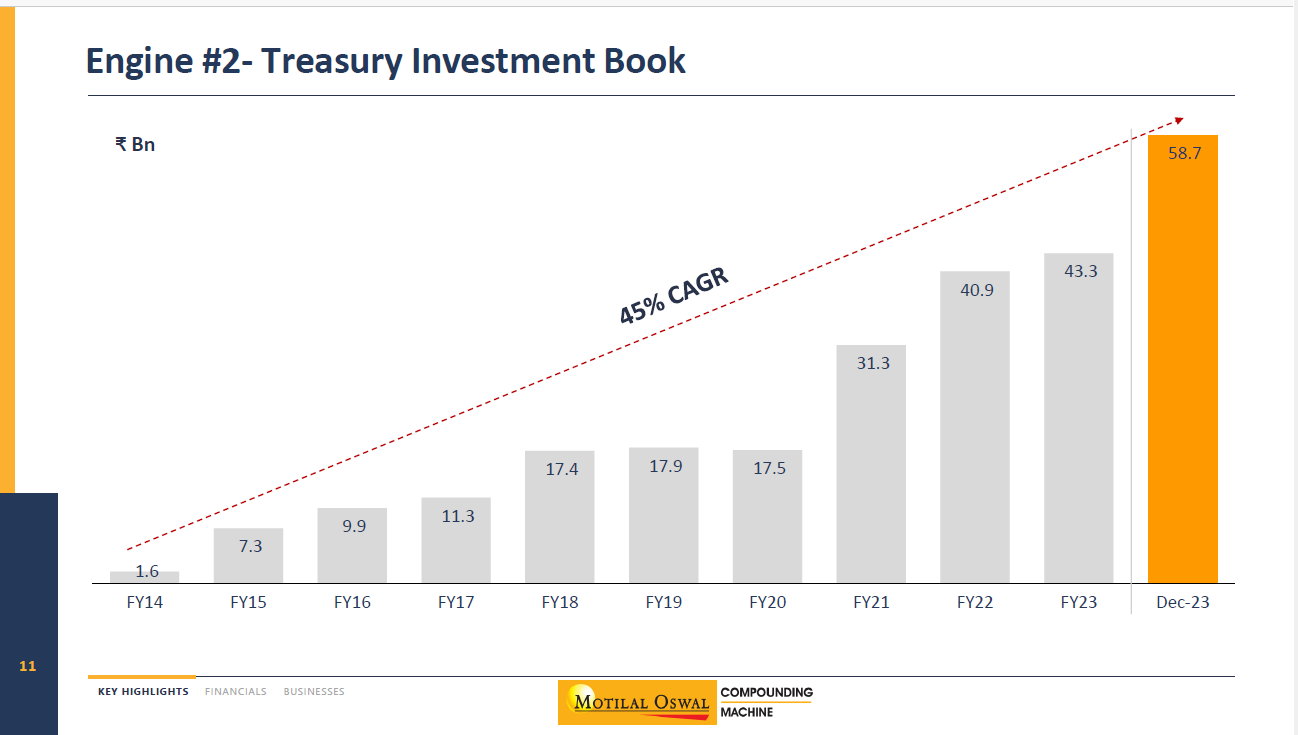

In the investor presentation they mention multiple times about "Treasury Investment "and “Treasury Income” . If you can simplify these two term that will be helpful . Thank you

1 Like

It is a simple concept… You create an income through and invest the income in further income or wealth generating asset. They say in AR,

“What is the bottom-line of all

of this? We need to understand

our double-engine business

model, where free cashflows from

operating businesses are ploughed

back into our treasury. Our treasury

book is 100% invested in equity

and equity products – all the time.

Over last 10 years, operating profits

compounded at the rate of 34%.”

Richard Wyckoff is regarded as a great trader. His book… How I Trade and Invest in Stocks and Bonds is a classic. He did some trading, and invested the trading income in long term income generating investments. In recent times, Ace Indian Investors Rakesh Jhunjhunwala used 5 percent of the capital in trading, and invested the trading income in long term security holdings.

Motilal Oswal is doing the same. They are investing it in 100 percent equity. They must be getting huge dividend income, and occasional capital gain. I don’t think they will be churning the portfolio much, and thus keeping the tax liability low while increasing the corpus and dividend income.

Motilal Oswal is a wealth compounding machine. On top of that it’s shares are cyclicals and thus easier to accumulate on market downturns. We must use Ramdeo Agrawal genius to create wealth for ourselves.

(Disc: Invested)

6 Likes

True, their passive income is going to overcome operating income.

4 Likes

Motilal uses retained Profits for two purposes one investing in current business and second they invest in thier own Mutual funds and private Equity fund. So this is returns they are generating for shareholders cash.

2 Likes

Article ignores that fact that Motilal is more of a wealth management company than AMC, revenue from the latter being much smaller. So comparison with pureplay AMC firms is flawed and misguided.

Wealth management business is more secular and stickier and if we just look at the multiples that listed wealth management players such as Anand Rathi and Nuvama are getting, Motilal stock has got plenty of scope for appreciation.

Disc- Invested from 200 levels and accumulating at every dip.

4 Likes

SEBI imposed Rs. 5,00,000 penalty for compliance issues.

1 Like

Motilal and Nuvama mentioned.

disc: invested

2 Likes

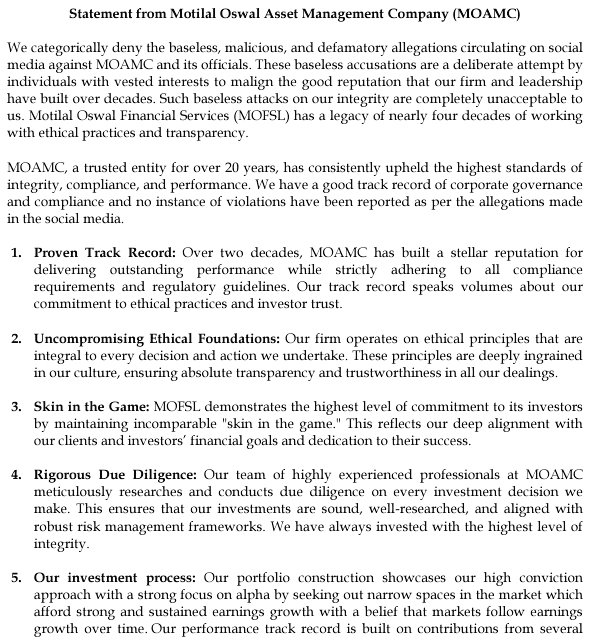

Clarification Alert by Motilal Oswal AMC:

- Denies rumors of bribery related to Kalyan Jewellers investments.

- Terms allegations as “baseless, malicious & defamatory.”

- Reaffirms commitment to ethical investment practices.

5 Likes

Hi, wanted to ask people who have been in the markets for a while-

at cmp MOFS is at pe of 10. If I reduce their margins by half, say covid year margins, and with no increase in sales, even then their pe is 20, which is their 10 year median pe.

Am I missing something?

1 Like

Well i am no professional but shouldn’t we look at the PE of their mutual funds instead of the stock ?

Business transformed a lot like pvt wealth mgmt and asset mgmt grew significantly the cyclicality of numbers will change if mkts dont trend for a while. Their capital mkts will slow down as ipos dry and mkt volumes also will come down then brokerage and institutional research slows down. These 2 businesses are very cyclical compared to other (private wealth, asset mgmt, home finance. Usually, we go by sum of the parts to evaluate business groups with diverse verticals. So purely going by historical pe is not correct. The business looks cheap to me now assuming we are not going to have vey significant downturn like volumes dropping by 50% from current levels.

5 Likes

Currently, most capital market stocks are offering great value. This is a common pattern with such stocks—they tend to be heavily driven by market sentiment and often trade at a discount during bearish phases. Once sentiment improves, these stocks are usually among the biggest beneficiaries.

3 Likes

In motilal I like their treasury book…for someone who advises client on research and risk mgmt…their treasury book is a demonstration that they know their stuff and are putting their own money where they are advising their clients

4 Likes