In last 3 trading session Promotors have purchased total 364525 shares (Average Price around 562.55). Total value around 20 crores. Good sign of bottom & value.

4 Likes

MOFSL Insider Acquisition: Ramdeo Agarwal & Motilal Oswal (Promoter/Director) have started buying shares from open market. Total Value of Buying is 20.5 cr. (364525 shares) that 0.19% of total mkt cap and 0.8% of free float mkt cap.

2 Likes

Hi Can any one help me understand how the modification on LCTG tax will affect Motilal Oswal or in general fund houses ?

Can anyone explain what is MTM gain/loss and how they got calculated?

I am guessing it is related to investments MOSL PE has made in various companies. Perhaps below post from Jan 2022 can throw some light

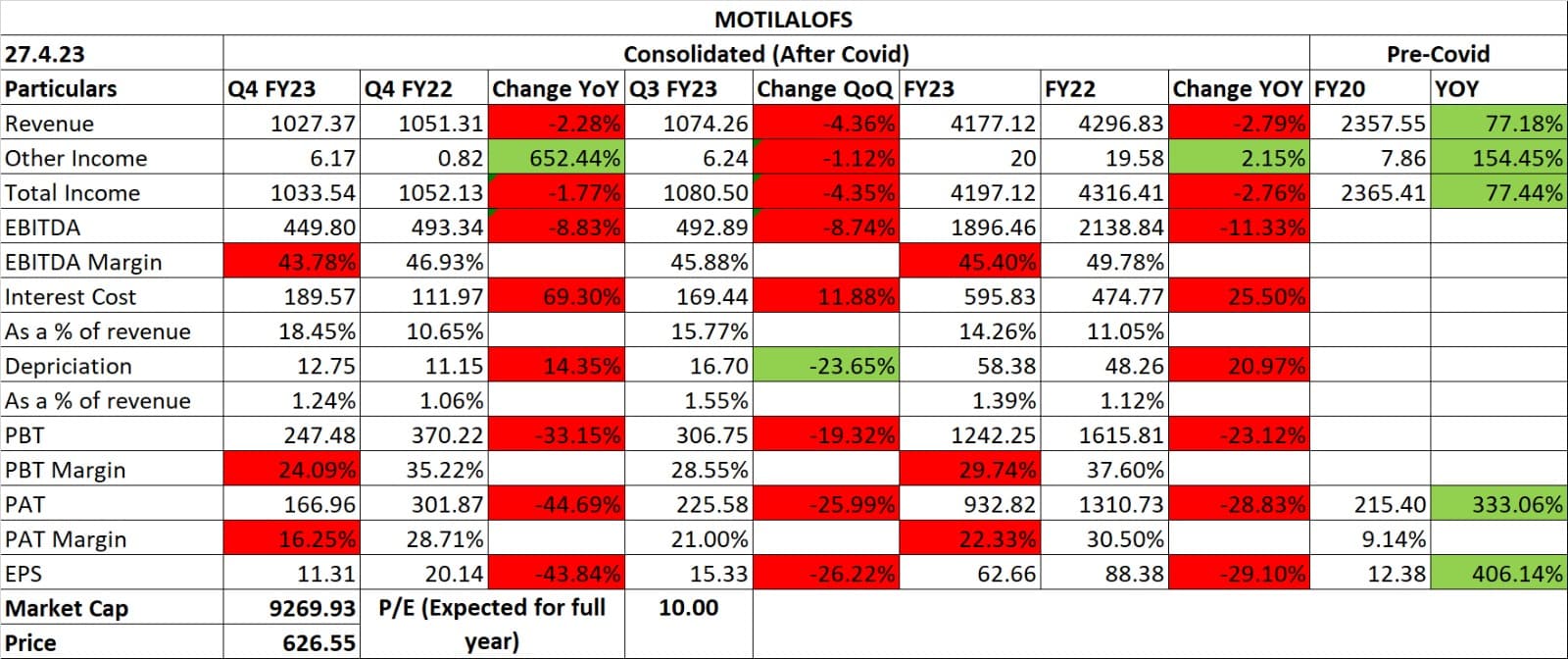

MOTILAL OFS Q4 FY23 Result Update:

- The company’s ROE for FY23 was 18%, compared to 30% in FY22.

- Increase in Wealth Revenue QoQ was mainly due to new AIF tie ups and Insurance Referral.

- Added gross 63 Wealth RMs in FY23. We will continue to invest in this business by further RM additions.

- Active clients stood at 0.8 mn as of March 2023. MOFSL’s rank, in terms of active clients improved to 8th position.

- Insurance premium increased by 120% YoY to ₹ 1.2 bn in FY23.

- Currency market share improved by 360 bps QoQ to 18.5%.

- F&O market share has also increased from 2.7% to 3.9%.

HDFC Securities suggests a TP of Rs. 845

2 Likes

There is a lot of margin of safety. if they do well in 3 years value of investments alone will be 9200 cr. hope their MFs perform which are now top performers in this qtr.

disclosure : invested fromm last 2 yrs and adding so may be biased.

3 Likes

Current value of investments is 4800 cr. Can you explain how that value is going to almost double in 3 years? What are your assumptions? I agree that margin of safety is there at CMP. I am not able to understand why market is not giving higher multiples to this business. They are not a pure broking business like ICICI Sec or Angel one. I think AMC and wealth management business is the dark horse here.

Their mutual Fund business performance and PE performance is Tied to this corpus growing in my calculation they can do 26 % IRR vs 18 to 20 % due to improved conditions in India and they are mostly in a growth kind of business which should do well in next 3 to 5 yrs. Also add they will generate 400 crs minimum (last two years it has been 800 cr) of free cash flows every year for next 3 years.

They can clear issues in MF and AMC business - Once performance changes then the market will come back at the moment they are tied to the likes of old age brokers like ICICI.

Do genuine issues exist.

Can you help me finding some one ex employee to understand culture in AMC

MOTILAL OSWAL AR 2022-23 NOTES

Chairman’s Message:

At MOFSL, we reported highest ever operating revenue of ₹ 4,319 crore in FY2023, registering a growth of 8% YoY. Our operating PAT touched an all-time high of ₹ 879 crore. Our consolidated ROE stood at 18%.

Equity Markets: On the capital markets front, Indian equity markets ended on a flattish note. Number of new entrants into the stock market declined as industry witnessed 2.5 crore new demat account being opened in FY2023 as compared to 3.5 crore in previous financial year. While FIIs were on a selling spree for second consecutive year, DIIs offset the pressure and recorded highest ever inflows.

Equity Retail Business: On the back of our strengths- “Phygital Business model” and “Research and Advisory”, our broking business recorded highest ever broking revenues, profits and Average Daily Turnover (ADTO) in FY2023. We added 6.5 lakh clients in FY2023, taking the total retail client base to ~35 lakh. We had one of the highest Average Revenue per User (ARPUs) in the industry. Our derivative market share was at multi period high in FY2023. Our distribution AUM stood at ₹ 21,300 crore and has huge head-room for growth. During the year, we launched Options Store and Research 360-degree App, further strengthening our offerings.

Institution Business: Rankings and Clientele remain robust. Completed largest private equity deal for Investment Banking Business.

AMC Business: Our AMC AUM which includes MF, PMS and AIF stood at ₹ 45,620 crore. During the year, we on boarded Prateek Agrawal, an industry veteran, to lead business and investment strategy. We strengthened our Risk Management framework and revamped investment process to deliver consistent returns. There was improvement in gross sales and a decline in redemptions. Fee earning PE and RE AUM stood at ₹ 10,280 crore. Our wealth management business AUM recorded a growth of 51% YoY at ₹ 52,000 crore. Our net sales was at an all-time high of ₹ 5,800 crore in FY2023.

Housing Finance Business: FY2023 was a landmark year where we reported highest ever PAT of ₹ 136 crore, with a 44% YoY growth. Disbursements crossed ₹ 1,000 crore milestone, registering a growth of 57% YoY. During the year, ICRA upgraded rating to AA/Stable from AA-/Stable. Our cost of borrowings for FY2023 stood at 8.0%, down by 24 bps YoY. Further, we have expanded our sales force with 690+ sales employees’ currently in place and we are present in 109 locations across 12 states/UTs. Our collection efficiency remained robust at 100.1% in FY2023. We have strengthened legal unit to pursue legal actions aggressively such as SARFAESI, section 138 and arbitration cases. As of March 2023, our GNPA stood at 1.1% and NNPA at 0.5%.

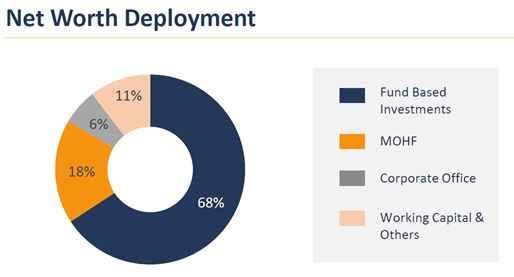

Fund Business: In our fund based businesses, our total investments including alternate investments stood at ₹ 4,280 crore with a since inception IRR of 16%. Our QGLP philosophy, niche expertise in equities, proven track record and belief in ‘skin in the game’, augurs well for our fund based business.

Business Development: Keeping in mind our growth aspirations, we on boarded 63 RMs during the financial year, taking the total count to 182. We will continue to invest in this business by adding RMs. With improvement in the vintage of RMs, the profitability of our wealth management is poised for further traction.

Opportunities:

Positive long-term economic outlook will lead to opportunity for financial services.

Growing Financial Services industry’s share of wallet for disposable income.

Regulatory reforms would aid greater participation by all class of investors.

Leveraging technology to enable best practices and processes.

Corporates looking at consolidation / acquisitions / restructuring opens out opportunities for the corporate advisory business.

Strengths:

Strong Brand Name

Experienced Top Management

Integrated Financial Services Provider

Independent & Insightful Research

Largest Distribution Networks of 550+ locations

Established Leadership in Franchisee Business

Strong Risk Management

State of the art infrastructure

Financial Prudence

Future Outlook: Strategy is to further diversify our business model towards more annuity sources of earnings. Adding more RMs will increase scale in wealth management business. Housing Finance business has witnessed turnaround by improving disbursement and profitability parameters. Our brand is now being recognized across each of our businesses. Each of our business segments offer huge headroom for growth and we are well placed to benefit from this.

7 Likes

Hello Lajja

I find Motilal Oswal interesting because it is part of 3 broker owned outfits which moved into capital market activities like Investment banking , asset management etc, others like IIFL and Edelweiss are well known.

Motilal has stayed away from risky lending activities and shored up balance sheet . They may not able to match up to Angel one and Zerodha in terms of technology platform so dont expect leadership here …

In asset management they are working very hard to set up passive management business where a lot of institutional money is going in future.

The icing on the cake will be alternatives business where they have made some good calls and this will bring carry income in future . You need to just hold on an wait for the good days

Their business does not need excessive capital and yet generates steady cash flows

Hope this clarifies to an extent …

Malolan

5 Likes

I believe this is going to be game changer for Motilal Stock. Demerger of wealth management business.

Disclosure: I have investment in this stock.

4 Likes

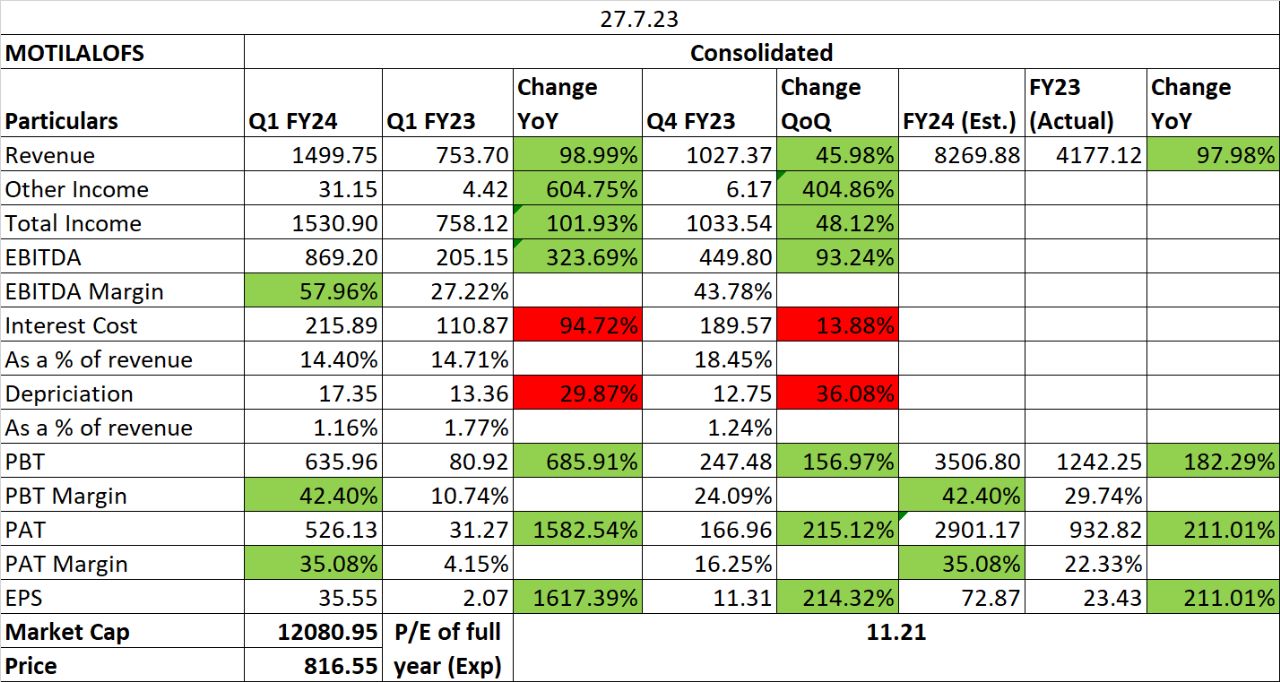

Seems like very good set of numbers with higher margins QoQ and YoY. (Disc: Invested)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/df1106c9-befb-4dc8-b899-052adf80942a.pdf

1 Like

- Their guidance of adding ~300 RMs by 2026, the management expects to reach this target before time with the current pace of growth towards the same.

- The management expects the cash market volumes to pick up, going ahead.

- Plans to strengthen sales force in home finance business to drive AUM growth.

- Wealth Management business focused on expanding relationship manager base and strengthening leadership positions.

- Focused on acquiring quality clients and increasing ARPU in the broking business.

2 Likes

Excellent Q2 result by Motilal Oswal.

1 Like

Demerger of wealth management .very unlikely. Promoter family is not going to dilute their holding or or pledge their holding and they dont need to do this " unlock " as you mentioned . They will just take dividend as malai … if you dont mind this " desi " phrase … They are not overly concerned about valuation of MOSL …

1 Like

Stock has given splendid move in the last 1 year which I thought was more of valuation-driven than the earnings. Price action gives an impression as if market is pricing in a potential demerger of wealth management.

looks picture perfect based on data. but PE is very low

why? anyone know? is it corporate governance?

1 Like