Company background

Motherson Sumi Wiring India Limited (MSWIL) is a leading and fast-growing full-system solutions provider to OEMs in the wiring harness segment in India. MSWIL is a joint venture between

Samvardhana Motherson International Limited (SAMIL) and Sumitomo Wiring Systems, Ltd. (SWS), a global leader in wiring harnesses, harness components, and other electric wires. MSWIL was formed by the demerger of domestic wiring harness business of SAMIL and listed as a separate company on 28 March 2022. It is focused on the wiring harness business in the Indian market, offering a wide variety of harnesses for different vehicles including passenger and commercial vehicles, two and three-wheelers, farm equipment and off-road vehicles.

MSWIL has 26 manufacturing facilities across India consisting of manufacturing & assembly sites and technical centers and employs more than 4,500 people.

What is a Wiring Harness (WH)?

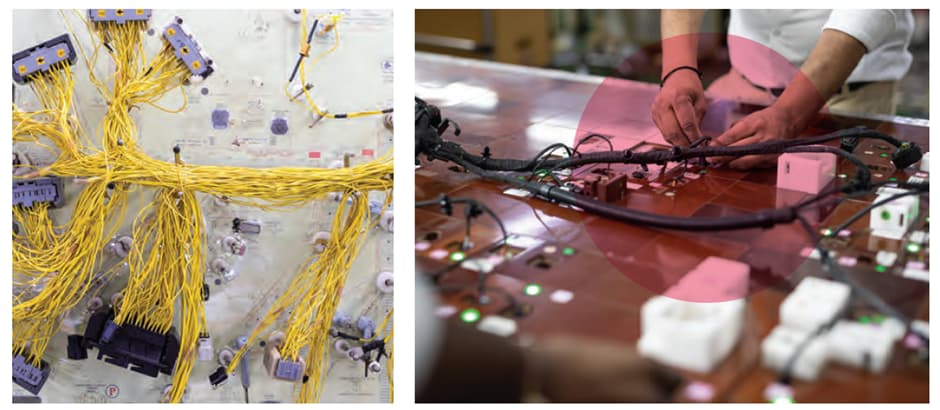

Wiring Harness is the combination of electrical cables, or assembly of wires, that connects all electrical and electronic (E/E) components in an automotive vehicle, like sensors, electronic control units, batteries, and actuators. The wiring harness handles the energy and information flow within the E/E system to fulfill primary car functions, such as steering and braking as well as secondary car functions, such as ventilation and infotainment. An automobile contains many wires and cables which would stretch over several kilometers if fully extended. By binding them into a cable harness, they can be better secured against adverse effects of vibrations, abrasions, and moisture. Constricting the wires into a non-flexing bundle optimizes usage of space while decreasing the risk of a short circuit. With growing focus on autonomous driving, advanced driver assistance systems (ADAS), and infotainment platforms, modern day vehicle requires a sophisticated electrical system which can handle the tasks efficiently and does not generate any electrical hazards for the safety of the passengers and the vehicle itself.

Harnesses are of two types, high voltage, and low voltage. A high voltage harness is used in electric vehicles; ICE vehicles use low voltage harnesses. Even in an electric car the internal working of all the electrical functions of the vehicle, like lamps and other functions etc. work on low voltage. But the charging and the inverter and the motor which drives the vehicle requires high voltage harness. The technical complexity as well as monetary value of a high voltage harness is more than a low voltage harness.

Products

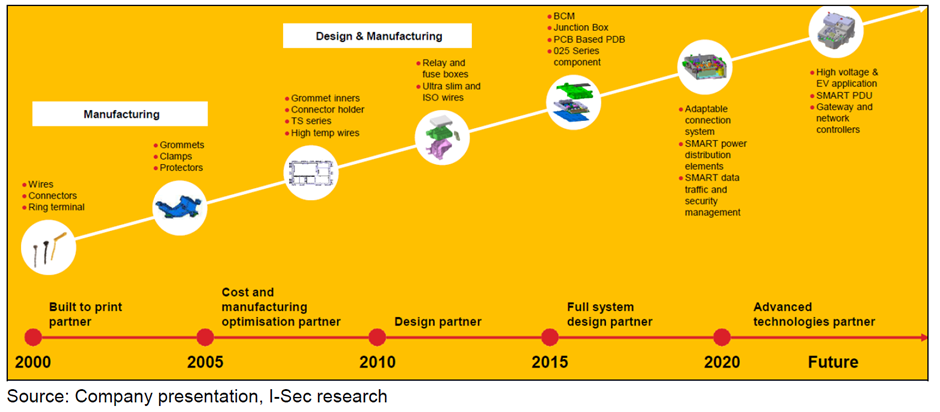

Over the years, MSWIL has moved up the value chain starting out as purely a wire manufacturer.

The company today is a full system solutions provider to its customers and is equipped to cater to their requirements in every step of the supply chain from the initial product design and validation, through tool design and manufacturing, finishing, and processing, assembly, production of integrated cutting edge Electrical & Electronic Distribution Systems for the power supply or data transfer across vehicles to sequencing in-line supplies.

WH typically constitutes just about 1.75 - 2.25 % of the value of a vehicle but is a very critical component as it is linked to several functional components in the car and has implications to passenger safety as well. MSWIL company makes over 20,000 different types of harnesses. Top 10 customers contribute around 70 %-75 % of the company’s overall revenues. The business is entirely OEM driven, with almost no B2C / aftermarket revenues. Around 60% of revenues are contributed by Passenger Vehicles (PV) segment and remaining revenues come from commercial vehicles, 2 wheelers, off road vehicles etc. All revenues are from the domestic market and there are almost no exports.

Promoters

Promoter holding in MSWIL is 61 %, which includes the Sehgal family owned Samvardhana Motherson International holding 33 % and Sumitomo Wiring holding 25 %. Institutional holding in the company is high at around 28 %. Shareholding pattern has not changed much since listing of the stock in 2022. There is no other equity dilution, no ESOPs. Company made a bonus issue in Nov 2022. Promoters have been generous with dividends as can be seen from the fact that dividend payout for MSWIL was 65 % for FY22 and 59 % for FY23, which can be considered as very good. Parent SAMIL has a long history of making acquisitions. However, it may be noted that with the focus of MSWIL being exclusively domestic market with a handful of players in it, chances of MSWIL going for any acquisitions are low.

Sumitomo Wiring Systems (SWS) of Japan is a co-promoter in the company. SWS is a global leader in wiring harnesses and controls a quarter of global market in the product. MSWIL can access technological advancements from Sumitomo at the cost of 50 bps of royalty payment other than itself spending 50 bps on R & D. However, it may be noted that SWS sold 4 % stake in SAMIL on 6 March 2024. SWS said it intends to further dilute its remaining stake in the company over a medium to long term duration as Motherson’s currently diversified business lines are not core areas of focus and expertise for the Japan-based firm. Due to this explanation, chances that they will sell their stake in MSWIL seem low. However, this is a factor that needs to be tracked.

Mr. Vivek Chaand Sehgal is the Chairman and a Non-Executive Director of the company. Mr. Anurag Gahlot is a Whole-time Director and Chief Operating Officer, and Mr. Mahender Chhabra is the Chief Financial Officer of MSWIL.

For more details on the promoter and pre-demerger business of the company, refer to the thread related to the parent company given at the end of this post.

WH Industry

WH sales are closely linked to the automobile sales in the economy. Domestic automobile volume growth in the country has been in the range of 6 to 7 % which can be considered as the steady state growth rate for the wiring harnesses. However, premiumization and electrification of the automobile sector implies a much higher growth rate for the segment. Premium cars & SUVs with more and more sophisticated requirements and features are using more and more electrical systems, increasing the need for higher value harnesses. Similarly, EVs require almost 2X wiring harness content than ICE vehicles. Both these provide a natural tailwind for the sector. It implies a growth of at least double digits for companies like MSWIL are easily achievable. So, it is no surprise that MSWIL’s revenue grew by almost 11 % CAGR in FY12 - FY22 as against 2 % CAGR in domestic PV production.

Domestic wiring harness segment of automotive components industry is dominated by a handful of players such as Yazaki India, Lear India, Aptiv, Kyungshin, Furukawa Electric etc. MSWIL is the market leader and caters to most of the top automobile OEMs except Hyundai and Kia.

Operational performance

In the previous decade (including before demerger), MSWIL’s (WH) revenues have grown by CAGR of more than 10 % whereas PV segment production in the country grew at around 2 %. The company has consistently grown faster than the market, implying increased market share. MSWIL is backward integrated with SAMIL and a significant percentage of raw materials and components are being sourced directly from parent companies SAMIL and SWS. MSWIL also utilizes manufacturing facilities and offices of SAMIL as per agreement at the time of group reorganization and demerger of MSWIL.

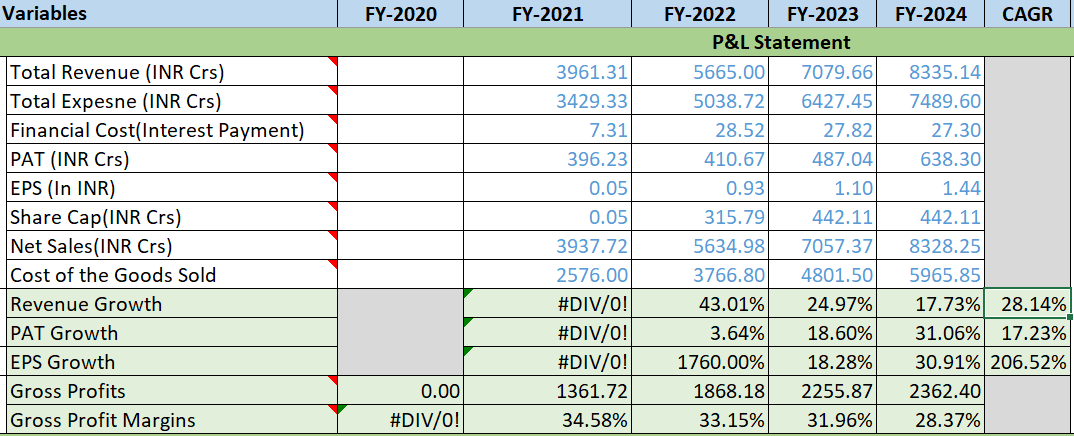

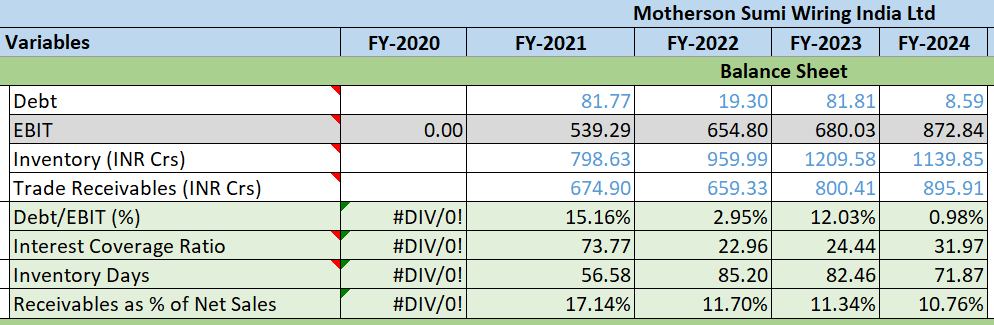

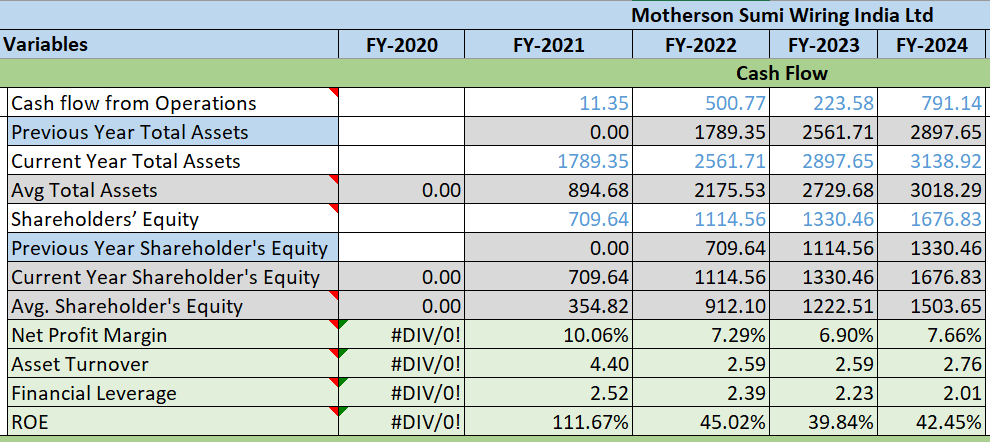

Since listing, MSWIL’s operational performance has been excellent. Return ratios are very strong, with ROCE and ROE in the 40 - 45 % range. There is almost no debt, except for lease liabilities and minor debt. Sales have grown extremely fast from Rs.3938 crore in FY21 to almost Rs.8000 crore for TTM Dec 2023. Gross margins are around 35 % range. Operating margins have declined from 14 % in FY21 to 11 % in FY23 but are at 12 % currently. Cash flows have been widely fluctuating but have been good in the current year. Working capital days and cash conversion cycle has been at less than 3 months, as per screener. Brief operational metrics of the company are given below:

MSWIL’s operational metrics are reportedly far better than that of its peers, though none of them are listed and hence detailed numbers are not available.

Copper is the main raw material for the company. Copper price is between 18 to 22 % of the raw material cost. For EVs, it is higher. MSWIL has back-to-back arrangements with its clients to pass on changes in raw material prices to the customer, which happens every three months.

Valuation:

The stock is currently trading at around 46 X TTM P/E at a market capitalization of Rs.27,000 crores. Strong parentage, tailwinds of premiumization and electrification in the automobile sector and strong operational performance make MSWIL an interesting story to watch.

Sources and links:

-

Parent company thread on VP:

https://forum.valuepickr.com/t/motherson-sumi-recent-opportunity-to-buy/2953 -

Annual Report FY2023

https://www.bseindia.com/xml-data/corpfiling/AttachHis/93c5e071-539b-4a46-8157-b65154586d33.pdf -

Company Presentation (Q3 FY24)

Covering Letter-presentation and Press Release.pdf (bseindia.com) -

Concall Transcript (Q3 FY24)

https://www.bseindia.com/xml-data/corpfiling/AttachHis/6fabc4e1-2024-4a54-a7c7-a6fc66855b08.pdf -

Company website

https://www.mswil.motherson.com/

(Disc.: Tracking, no position at the time of writing)