Morarjee is a name synonymous with fashion. With over a hundred years of experience and modern integrated manufacturing facilities, Morarjee makes cutting edge fashion a reality. It has technical collaboration with Swiss and Japanese companies that sets it’s apart in the industry.

Morarjee is part of the Ashok Piramal Group, a diversified and leading business group in India.

Negative abt the co:-

1.Jv with Just textile is loss making.

2.subsidiary, integra apparels has negative net worth.

so overall there is past history of promoter making bad capital allocation decision.

you can read this for more information https://www.equitymaster.com/outsideview/detail.asp?date=03/22/2011&story=1&title=Morarjee-Textiles-Not-making-any-headway-Luke-Verghese

Positive abt the co:-

- Recent expansion and likely to be succed

you can read this for more info Morarjee Textiles: Better capacity utilisation, operational efficiencies key growth drivers: Harshvardhan A Piramal, Morarjee Textiles - The Economic Times

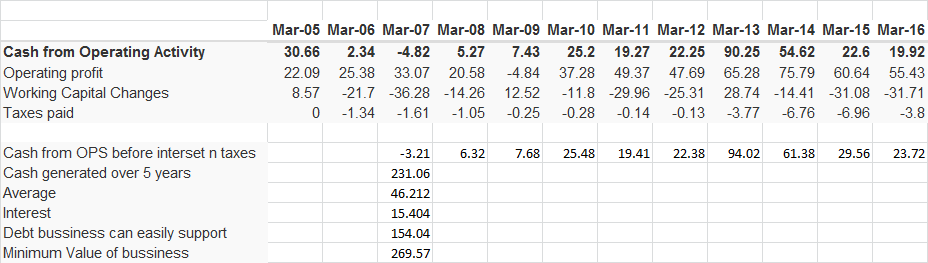

- Minimum value of bussiness.

Also read this rating agency report http://www.brickworkratings.com/Admin/PressRelease/Morarjee-Textiles-BankLoan_457.85Cr-Reaffirmation-Rationale-15Sep2016.pdf

- Good ROE.Good EBITDA

- Dividend yield is around 2.5 %.

Disclosure: Invested 10 % of total portfolio

@bheeshma @Donald @Gaurav_Agarwal @ankitdesai @RajeevJ

Hi sumit

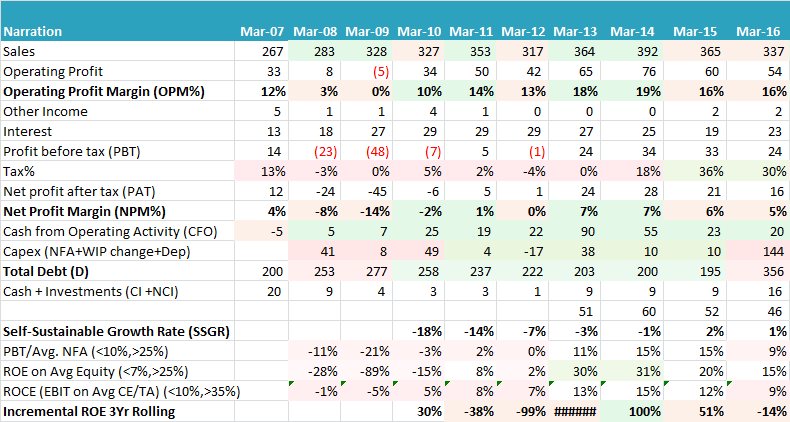

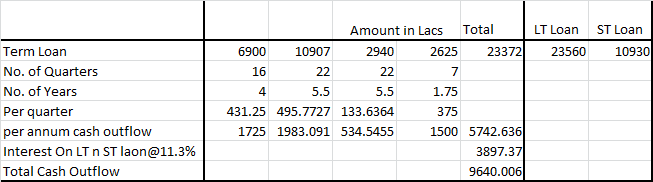

Just a quick take on this - I dont think anyone will lend to Morarjee at 10%, Its int coverage and cash coverage ratio is too low. Its AR16 mentions the rate between 10.60% to 14.25% p.a ( so i would take the upper end for my calculations). Also after going through the notes in the 2016AR i feel that the terms of repayment are very aggressive with tenures ranging from 22 months to 48 months

Secondly, it is already sitting on a debt of 355cr post expansion. Its TTM Standalone sales are 366cr. Clearly, it has taken on debt that is disproportionate to its size in anticipation of better growth prospects. Your sheet suggests that debt the business can easily support is 154cr but it already has a debt of 355cr.

In sum, servicing all this debt is going to be challenge.

All these are causes for concern to me.

Best

Bheeshma

tried to calcualte total cash outflow for d year 2016-17

Assuming 40 % increase in revenue due to expansion, cash from operating activities b4 int n taxes will also increase by 40% i.r 65 cr against outflow of 95 cr . and also from the past history i fell it will also declare div to its shareholders which will be approx 5 cr.

so this year will be challenging but the benefit of expansion will be seen in coming year, i am seeing this story as DEBT REPAYING CAPACITY BARGAIN

@bheeshma thanks for correcting my mistake in taking 10% interest rate

Impact of GST on Textile Industry

Q4FY19 numbers were quite interesting - CAPEX seems to be coming onstream now.

Of course the cash flow for FY19 is unsatisfactory. Approx Net Cash Generated from Operations is -33 Cr (loss)+ 23 Cr (Depn) + 54 Cr (Interest expense) - 1 Cr (Increase in Inventory) + 30 Cr (Increase in Payables) + 13 Cr (Decrease in Debtors) = Rs. 86 Cr.

The reason I say this is unsatisfactory is because 54 Cr is interest expense, which is an actual expense, so (CFO-Interest) is Rs. 32 Cr (most of which, has been generated from increase in trade payables, still not great).

The question for us here is if we can see a Fixed Asset Turn of 1x (at least, which they’ve achieved historically), Morarjee can achieve sales of Rs. 500 Cr+.

GP for this quarter also declined significantly to 45.6% from 55.3%. This could be due to cotton price volatility, or equally likely, them cutting prices to fill up the capacity which has been created.