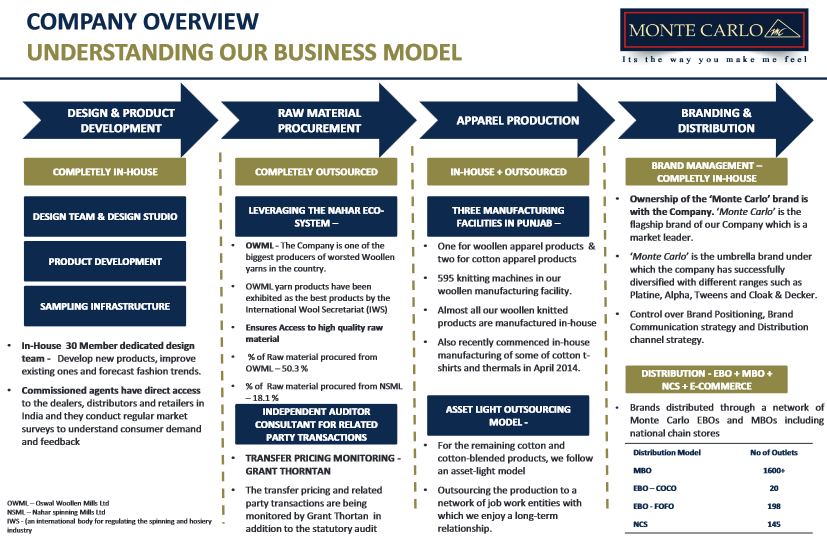

MCFL is a trusted known brand in North India for woolen wear. As someone who has lived in North India for a majority of his life, I can attest they make good products and there is significant demand in the winter season for their sweaters, cardigans and other knitted wear. The company is also into cottonwear for which it is not very well known, but the MC brand helps leverage some growth there too. As of now, both woolen wear and cotton segments are growing well. The business model of the company is captured in the below screenshot:

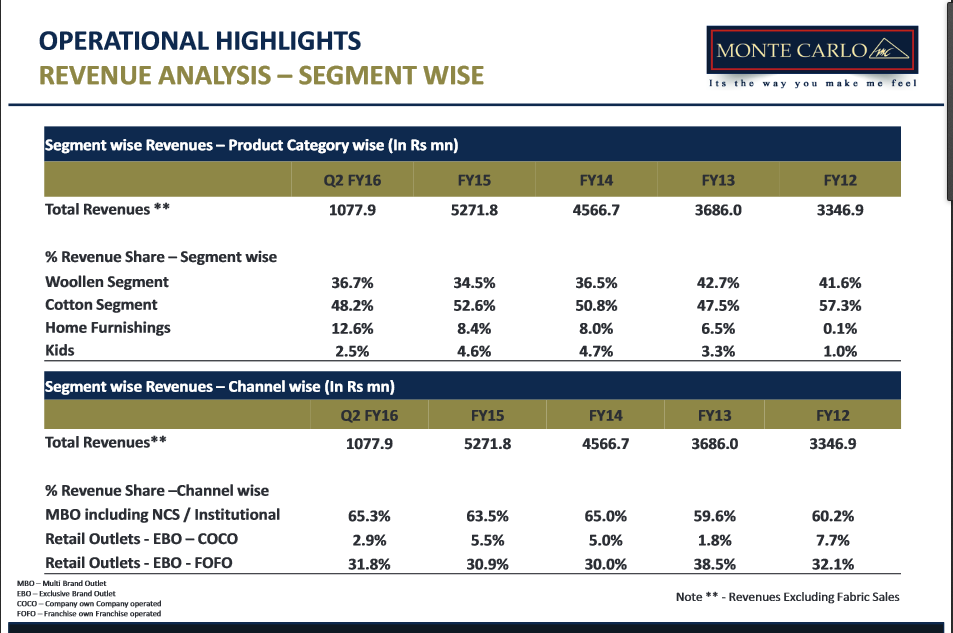

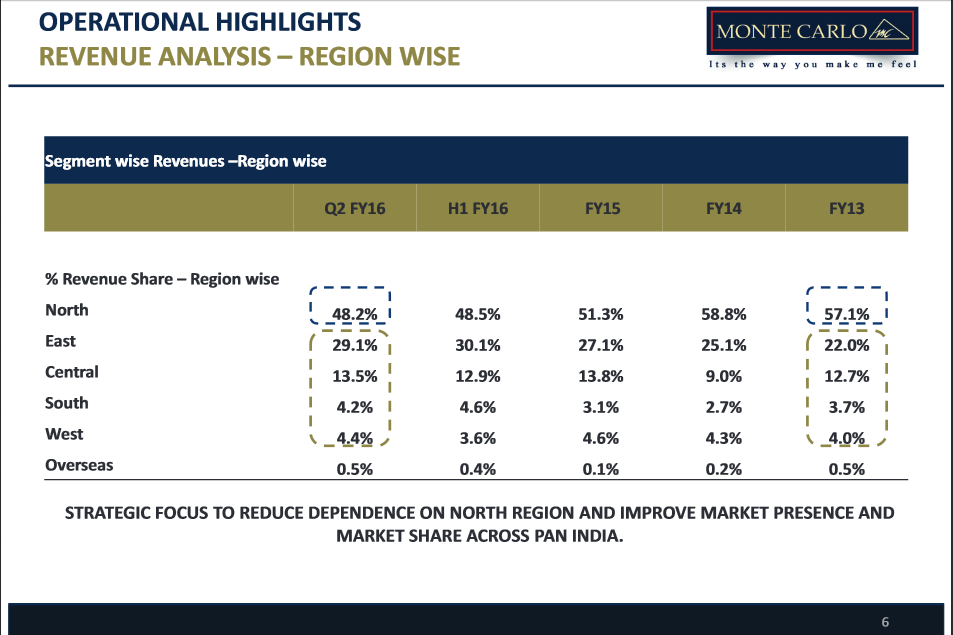

MCFL sells primarily in North and East India but is now expanding to the south and central India. Obviously these are regions where woolen wear is not a big draw. So the focus will be on cotton wear. MCFL is not known for its cottonwear, so growth will depend on leveraging its brand name [more info on expansion to other regions in the link to investor presentation below]

Market share in south and central India is growing, albeit slowly.

Since the IPO, the company has added 22 retail outlets - 220 currently, up from 198.

No major capex planned for next two years - operating leverage to play out.

Key Risks

MCFL is owned and run by the Nahar Group. They have several listed entities, Nahar Spinning Mills being the second largest one. Nahar Spinning Mills makes cottonwear for MCFL on job work basis - related party transaction

Nahar group entities have eroded shareholder wealth over the past years.

High seasonality - most sales in winter only. Year round revenue would depend on growth in cotton wear segment.

High competition in branded cottonwear segment. While MCFL has a niche spot in woolen wear, cottonwear is another animal altogether.

Is it a good entry point?

At a PE of 15.53, MCFL trades below other branded apparel stocks in the market. One that comes to mind is Indian Terrain Fashions Ltd, which trades around 18-19 PE and may trade higher eventually. I am not advocating a short term trade here, I just think this is a good entry point for a long term compounding machine.

Misc

The above is a short summary of my views on the stock. Invite views on why this stock is trading at a lower valuation vis-a-vis the rest of the industry. Is promoter quality a concern considering other Nahar entities have not built shareholder wealth over the years? Any leads on promoter quality would be great.

Nice writeup. I have few concerns though, so please provide insights into below mentioned queries:

Their business is highly dependent on winter wear, though 50% sales come from cotton segment. Majority of their sales & profits are in third quarter (Current one).

Debt is increasing yearly, even though they have cash from IPO, which can be used to reduce debt.

Yes, they have good brand pull, but majority of sales comes from institutional demand where profit margins are less. (In my company, dress is mandatory, we get monte carlo sweaters every year as part of dress)

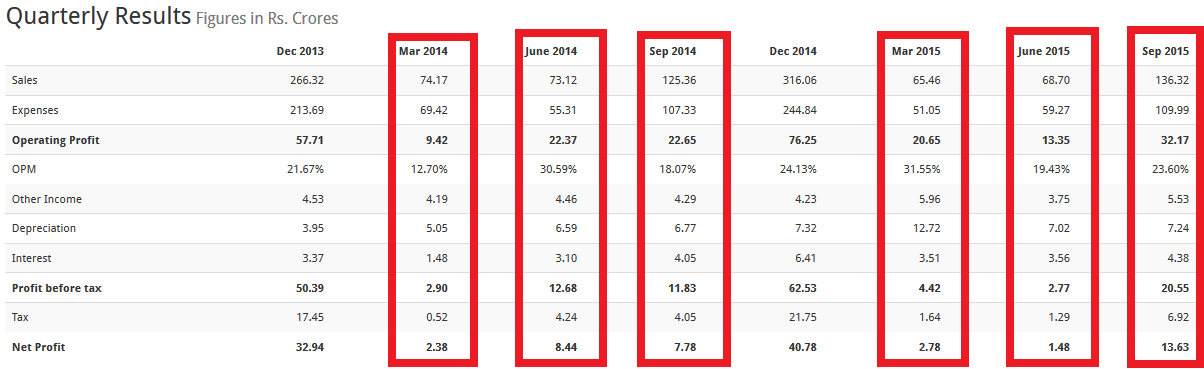

You are correct that 50% of sales are now from the cotton segment. I do not know the margin in this segment as segment-wise analysis is not available in the AR. It is likely that margins are decent. This is evident from the fact that in non-winter quarters the net profit is lower than Q3 but margins are intact(but they seem to vary a lot). Screenshot (there was an adjustment of inventory from June 2015 to Sep 2015):

I would say increase in debt is due to increased store openings. The stores have increased 10% over the last year. Also, the management has indicated in the investor presentation that the company is investing into marketing and advertisement. However, inputs welcome.

I am not very knowledgeable on the institutional arrangements. I know of a few people that buy MC without any institutional tie up. There is a positive spin to an institutional arrangement though - guaranteed sales visibility without marketing and store costs?

u have highlighted the key risk quite well especially RPT

for promoter, its not the only business in textiles/garments - it is just one of the business. They have other businesses in garments which are really mammoth in size

just a perspective - they have the first mover advantage some 20-25 years back and where they have reached. MC is a brand which was synonymous with sweaters but when we look at the scale of operations (sales) - i was never able to connect

Price seems okay, even Samara paid around that 3 years back. But still i have to search for value…

Above mentioned text raises more questions rather than answers. And for me, there used to be even more - when i was closely associated with the group for some equity related activity. Since then i have not tracked it & still at this price, it does not excite me. Wont like to elaborate more on this on a public forum - feel free to PM me, for any specific query - if you are really enthusiastic for it

Lastly - The things might have changed and i might not know. So i deserve the right to be wrong. Needless to say, no holdings

I would request you to at least do some research before asking questions. I have raised an idea here and hope for inputs, not an interrogation and one way flow of information.

To answer your question, June quarter there was an adjustment that led to sales being booked for September quarter. The Company indicated the profit for September would be higher on this account and this was correct.

March quarter the revenue dipped due to change in the way sales are booked.

The company is putting TV commercials. But the commercial has no appeal. All the participants read actor/actresses are girls but all of them were non-Indian. I could not understand who were their target audience. Their TV commercial work is really lousy and proves @Mayank_7772 point that it is one of their businesses.

Hi I am holding Nahar Spinning for more than 2 decades but small quantity.The performance over the period is inconsistent or not constant.Above all, the promoters of all the 3 Oswal group companies are against the interest of the minority share holders.

1 Bindal agro oswal agro etc.

2 Vardhaman spinning, Varthaman Acrilic etc.

3.Nahar Spinnig,Nahar Capital,Monte Carlo, etc.

That is why all the Oswal Group companies shares except Monte Carlo are quoting very low P.E

Dis. Not invested/interested…

Most of the sales is done on pre-order outright basis. Franchise model is asset light.

Future plan

From the AR: Target is to open 275 Exclusive Brand Outlets (EBOs)over the next 2-3 years mainly through the franchisee route and establish a truly pan-India presence by increasing penetration in southern and western regions of India. The Company is also focusing on tapping the rapidly growing online sales platform through its own portal as well as through tie-ups with leading e-commerce portals in India.

Operational cash inflow of 531million (887 for FY 14). Overall net cash outflow of ~ 3million due to investing activities.

Secured bank loan FY 15 - 621 million+

Terms of repayment are quite well defined in the AR. The biggest chunk of loan from Indian Bank will be repaid in full on March 31, 2018.

The company also has 2000 million special reserve allocated for acquisitions and 650 million of free reserves. Debt shouldn’t be an issue ideally.

Dec’16: 9 month ended turnover: 5,555 million against 5,162 million for Dec '15

EBITA: 1050 million vs 1005 million

I think their working capital situation is not good. As they are generating good profit but where is cash flow. even in Fy15 they have generated cash of only Rs.22 crs against net profit of Rs.59 crs. that is lousy. so if anyone has any idea regarding management plan of reduction of working capital?

I think a large part of the cash flow gets impacted due to loan repayment. They’ve 2 major loans from PSU banks which are being repaid and most of the debt should finish by March 2018 I believe.

MCFL results are due on May 30 but I’m not expecting the Company to meet management guidance.

The management has been repeatedly giving a guidance of 10-15% growth, latest in Feb in an interview with CNBC.

FY 2014-15 full year turnover - 582.58

9 month ended Dec '15 turnover - 556.95

FY 2015-16 turnover (15% growth) - 669.97

Q4 turnover to meet guidance - 113.07

FY 2014-15 Q4 turnover - 65.74

Although it seems baffling that MCFL’s Q4 turnover was 1/5 of Q3 turnover considering winter wear sales remains steady atleast until end of February in North India.

Even at guided growth rate and steady FY15 OPM margin (as claimed by management), NP growth is ~25% assuming there are no shockers in operational costs. The Company trading at 15PE still appears overvalued.

On the short point on winter - winter in North India was exceptionally brief and relatively warmer than past years. So that is a definite impact on previous quarter.

Regarding Monte Carlo outlets… i had stayed in bangalore and their outlets were not having good collections… Also there were very less customers… So my personal view is they r not upto mark in fashion…

I would like to avoid this because of the track record of the promoter group as mentioned by many they have eroded minority share holder wealth. so even if the company is growing if the management is not shareholder friendly there is no use in investing in it as we minority shareholders are totally at the mercy of promoters. I think it will be better to go with ABFRL as it has many brands and has pan india presence, yes it has high debt but they should be able to get through it, with sales of 6000cr they will soon find the ways to take care of debt. Promoters have to be shareholder friendly in any company we invest orelse there is no use at all

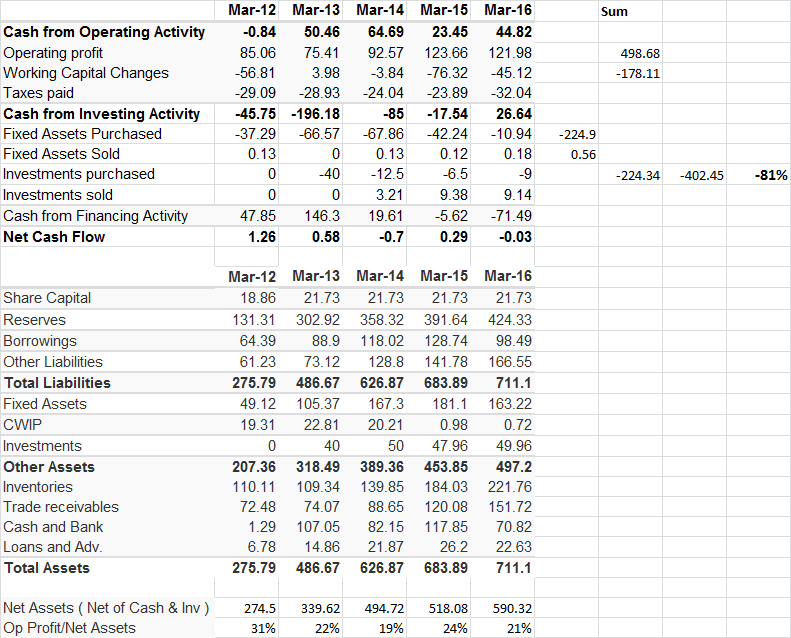

Its not a bad company - from what i can make out from the cash flow statement. However, over the last 5 years 80% of its cash flows have been used in the working capital & capex investments leaving very little to cheer. However i am enthused by the fact that its operating profit before working cap & taxes has been more than 20% of its net assets ( total assets less investments & cash ), which is a sign of a good company. Its a nice company and i think it will do well in the future for sure. Not Invested though

one more thing you can see is in the last 1 year promoters are buying shares from open market around 400rs range and till now they have bought stocks worth of 3 cr. so maybe its good , I dont know . I am not taking any risks as I am not comfortable with the promoters

Hi,

Now its time to revive this thread MC_PPT.pdf (2.5 MB)

Find enclosed Investor presentation . MC is not only typical seasonal winter player selling sweaters but also launched winter wears and doing pretty well.