Monolithisc India recently came out with an SME IPO of 82 Crs. Mostly they were in market for growth capital where want to increase capacity from 156 KTPA to 574 KTPA (~3.5X).

Monolithisc India Limited is one of the leading refractory solution (Quartz Silica based Ramming Mass) providers to induction furnace based steel re-rolling mills (SRRM)s.

Two key factors on the onset:

- As has been the case, refectory material are those small yet critical consumables that accounts for a very little percentage as cost to final output (less than 0.5%), however are mission critical from operational quality and safety perspective – a la Webers law or put simply like salt in food… does not even get noticed as long as things are going right, however makes all the difference even if less by few grains.

- Ramming mass is very local, voluminous and commoditized product. End product costing anywhere between 6 – 10 Per KG in domestic markets. Transportation beyond a certain geographic range makes it economically unviable (think cement as a parallel). Export market still works despite geographical distance due to better realization if manufacturing capacity has port adjacency (Raghav Productivity). So, proximity to end-user is an edge.

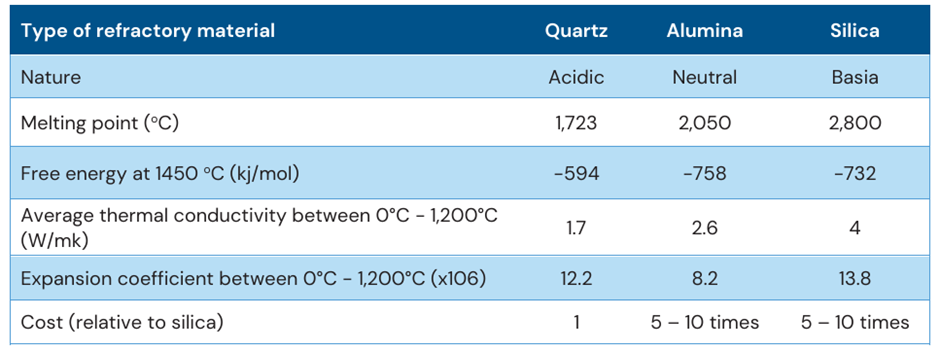

What is Ramming Mass:

The quality of ramming mass has a direct impact on the heating performance of the furnaces leading to the smooth working of furnaces, optimum output and better metallurgical control. Ramming mass is a pre-blended Dry vibratables refractory made from a selected mix of SILICA GRAINS. This blend of grains along with a binder, BORIC ACID forms the working lining in an Induction furnace used for melting steel.

The quality of ramming mass has a direct impact on the heating performance of the furnaces leading to the smooth working of furnaces, optimum output and better metallurgical control. It comes in three variants –

- acidic (made from silica),

- basic (made from magnesia) and

- neutral (made from alumina) – was surprised to know that Saint Gobin is into alumina based ramming base due to RM synergy and back/forward integration.

Advantage of Quartz ramming mass

- It has the lowest thermal conductivity resulting in low energy loss, low expansion coefficient leading to the stable lining, and good resistance to temperature

- High Silica content (>98.9%) facilitates in oxidizing the impurities present in the output charge by forming slag.

- Cost is nearly 10 – 20% low compared to that of alumina or magnesia based ramming mass.

Steel re-rolling mills (SRRM)s.

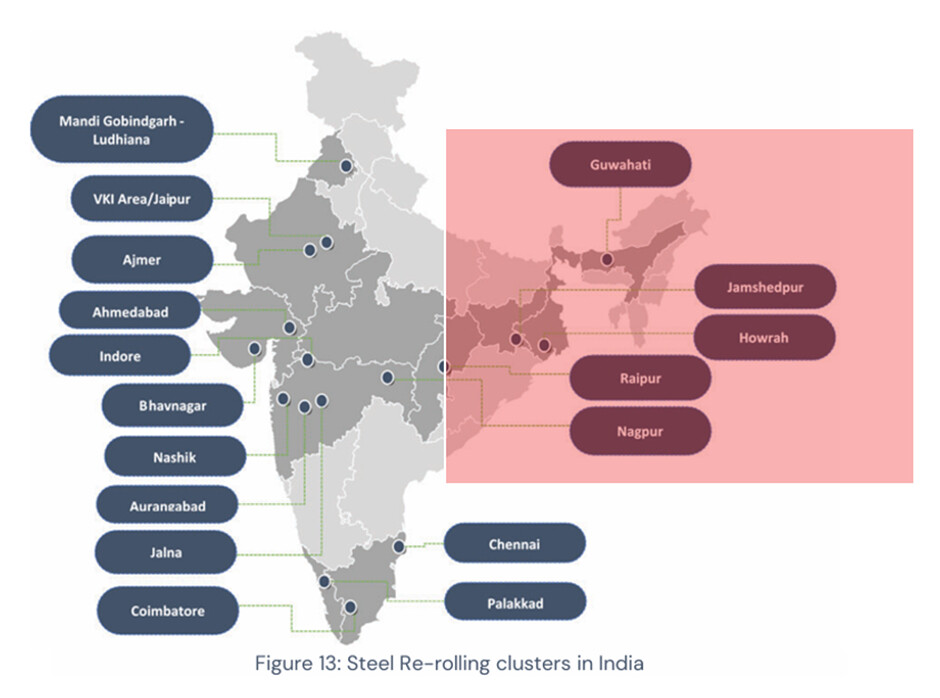

There are an estimated ~1300 working small and medium steel re-rolling mills in India, scattered across the country, and producing ~33 MT of steel. It is also reported that 80% of India’s total exports of bars are sourced from the secondary steel sector. About 65% of finished steel produced in India comes from secondary steel sector rerolling mills

The induction furnace (IF) route share expanded by 6% up from 32% in previous year to 38% in FY25. In absolute terms, IF route accounts for 58 MTPA. Increasing awareness about IF’s heating capabilities, lower emissions, and precise temperature control optionality has increased its adoption over the years.

One can look at cluster specific details here:

SRRM Cluster Details.docx (237.6 KB)

Total Addressale Market:

Total Estimated steel production through Induction Furnace Route 55 TPA

Average Ramming Mass Consumption 30 KG per Ton

Steel Ramming Mass Market (derived) 1.65 Mn TPA

Additional, Export and Misc Deman 0.35 Mn TPA

Total Demand for Ramming Mass: Approx 2 Mn MTPA

Competition Landscape:

Significant Capex by two large players - will industry consolidate towards organized players or end up into supply glut?:

-

Raghav Productivity Enhancers capacity: RPEL set up a manufacturing plant for silica ramming mass, which is a greenfield expansion of its existing plant at Newai, under its wholly owned subsidiary, RPSPL. The plant has manufacturing capacity of 2,70,000 MTPA, thereby increasing the combined capacity of the group to 4,14,000 MTPA (20% of India TAM).

RPEL is strong in exports market. Largest exporter from India today to 36+ countries across Middle East, South-East Asia & Africa. For REPL, export contribution to revenue is ~90 Cr to topline in FY’25. In volume terms, export is 77KMT (33%) of total sales volume of 257 KMT.

-

Monolithisc India Ltd.: Came out of with an SME IPO of ~82 Crs. Are planning to increase capacity from existing 156000 MTPA to 574000 MTPA (~3.5x) or 27% of INdia TAM

There customer base has gradually grown from 38 customers in Fiscal year 2022 to 55 customers in Fiscal year 2024 along with a CAGR 69.29% growth in revenue from operation.

As expected, most of the revenue contribution is from WB (66%), Jharkhand (16%) and Odisha (16%).

Additionally, Company is looking to acquire unit near western part of India to tap exports from Mundra port and secondary steel manufacturers in western part of India

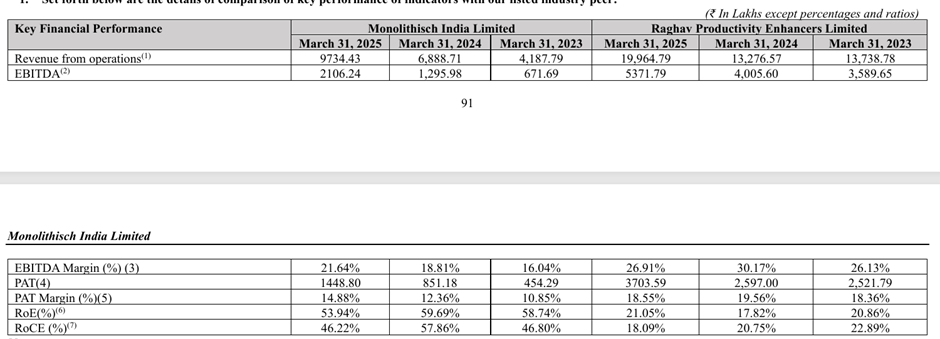

Comparison of financial numbers between the two: Monolithisch having comparatively lower (but growing) EBIDT to RPEL however better ROE/ROCE due to capital structure.

Closing thoughts:

Creating supply side dominance is one side of the equation, enough uncrowded demand is another side of the equation for shareholder returns.

-

5,74,000 MTPA Ramming mass working at 80%+ utilization will need ~18-20 Mn Tons of re-rolling steel production under Induction Furnace route within geographical catchment area.

-

Monolithisc has easy access to eastern India re-rolling steel mills cluster having ~300 SRR mills. [Howrah (100 Re-rolling Mills), Durgapur (50 Re-rolling Mills), Jamshedpur (20 Re-rolling Mills) and possibly to expand to Raipur cluster (135 Mills)]. For context, currently they have penetration to 60 – 65 SRRM clients.

-

Further, quasi export to neighbouring Nepal, Bangladesh are other optionality that management has spoken about- provided the geo political challenges are well covered.

-

Wishful thinking if management decide to have geographically diversification by greenfield capacity in western India on the way to reaching the overall capacity target of 574,000 MTPA. Will bring them in direct competition to RPEL however will open up access to high quality RM from Rajasthan Kota belt and access to middle east and far east (turf of RPEL) export market where realization and margins are much better.

-

Organic steel industry growth is in low teens. Shift of market to Induction Furnace route of production is fast (600 BPS last year). Put together, fair to factor-in market growth at low double digit. (10%-12%)

-

Additionally, operating leverage is expected to kick-in with higher 3.3x capacity by FY27. Monolithisch is expected to report increased margins while spreading fixed cost to higher production base. Additionally, being equity funded capex, not much borrowing cost to eat away the margin.

-

On risk side, is an NSE SME listing. Trading at headline PE of 60+

Disc: Studied this purely from business understanding perspective. No investment POV at this stage.

Regards,

Tarun