How I think of MB now?

@Apandey

Firstly I would like to discuss on the industry side a bit, plz note I can be very naive in my analysis due to the complexity of the industry

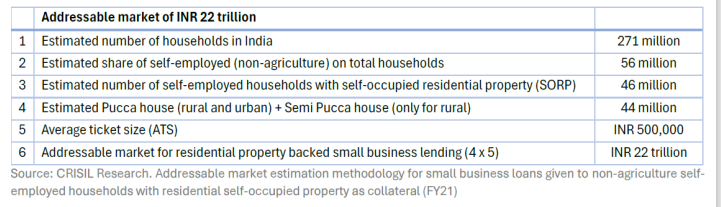

So the total addressable market as per the below screenshot is 22 trillion INR

Some industry numbers for MFI

Portfolio outstanding of MicroFinance industry as on 31st March 2024 is `3,77,706 crore with 1,238 lakh active loans and 6.6 crore unique live borrowers.(From another report)

So what we can see is the loan account are 2x of active borrowers which is like every borrower has 2 loan accounts

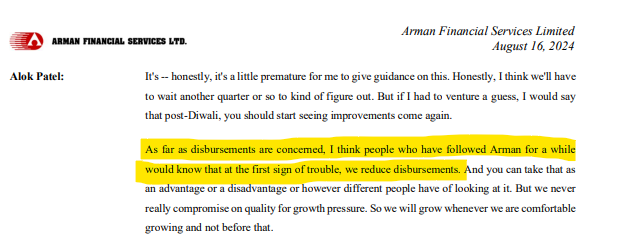

So looks like MFI borrowers are overburdened and on top of this we had election, heat wave, school fee paymet etc etc this is damaging the ability to pay so the MFI are now forced to slow down this growth which would derate them. Below snippet is from armaan call

But the thing is money boxx is not MFI , though the rural distress is a PAN india phenomena I think moneybox kind of model would have faster recovery than MFI borrowers. Here are the following reasons

- 30% of moneyboxx borrowers are new to credit, so there borrowers just have 1 loan account which is with moneybox and their underwriting is more difficult.

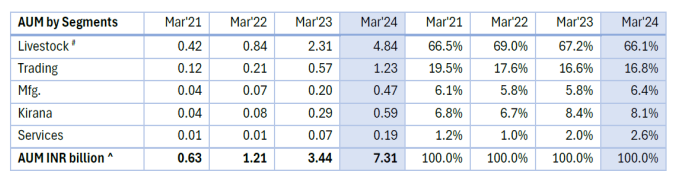

- Below is the screenshot of how the MFI portfolio is spread at an industry level and how is moneyboxx portfolio spread. I think again moneyboxx has an upper hand here because livestock as a segment is less seasonal and more cash generating that agriculture (my guess)

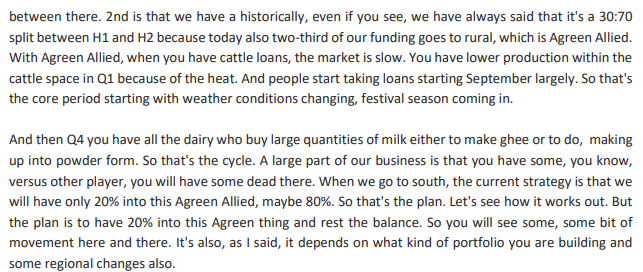

- Their secured book is 27% as on june 2024 which would go to 40% by March 2025, currently about 30-35 branches of MB only do secured. Do read the below snippet from five star.

- On one side we have aarman who doesn’t want to comment on guidance and on the other side we have five star who are very confident of 30% growth. This shows growth varies across ticket size.

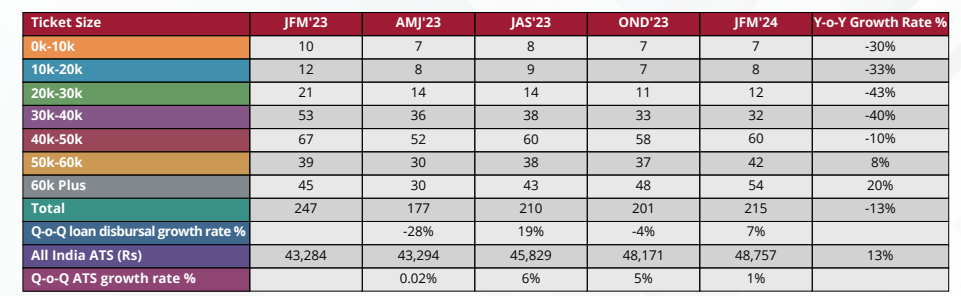

Even if we take different ticked size in MFI we can see marked difference as the ticket size increases

What moneyboxx has to say on growth?

- If we see about 45% of moneybox disbursement came in Q4 for FY24

- Last FY 664cr of disbursement added 386cr to AUM so 60% so to reach an AUM of 1400 cr this year they will have to roughly disburse 1100 (should be less due to secured % increasing) If the number of branches increase to 130-150 by dec 2024 (growth of 30% -50%) Q4 disbursement can grow by 50%-70% implying 450 to 500 cr disbursement in Q4 FY25 (should be more than this)

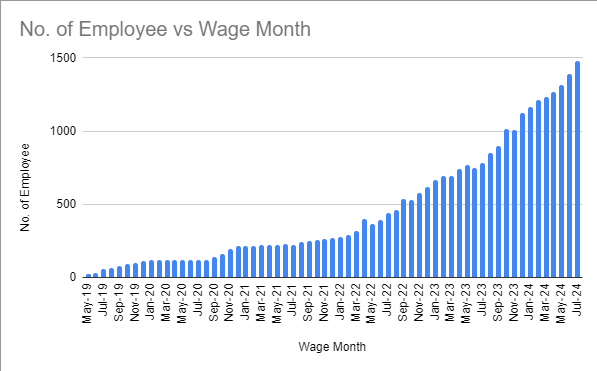

- So for us key monitorable is branch opening and employee headcount growing

Conclusion

My overall understanding is rural is under distress but the segment which moneyboxx catres to will have a recovery much faster than MFI. Aarman says from Q4 they are positive that growth my revive so we can kind of assume from Q2-Q3 MB will turn around in terms of asset quality and growth

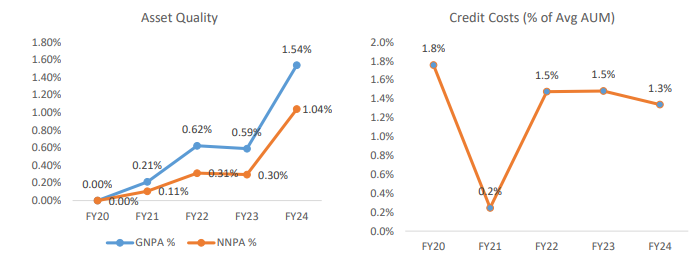

Asset quality

- This is definitely a concern but it is still under management guidance of 2% to 3% credit cost and given that the secured business would pick up the blended credit cost should definitely reduce going forward

Execution capability

This is something very difficult to judge but below is a relative analysis I have performed

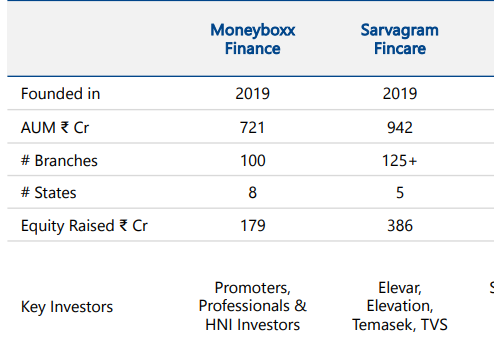

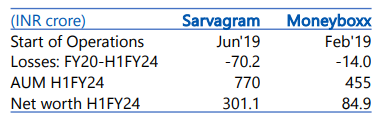

- Comparison with Sarvagram fincare and moneyboxx

Moneyboxx doing 130cr of income on same asset base where sarvagram is doing 80cr. The business model by default is a 20-25% ROE business if u see their interest spread , hence with moving more towards secure and opex/cost of borrowing reducing I see them moving towards achieving those numbers (contingent to asset quality)

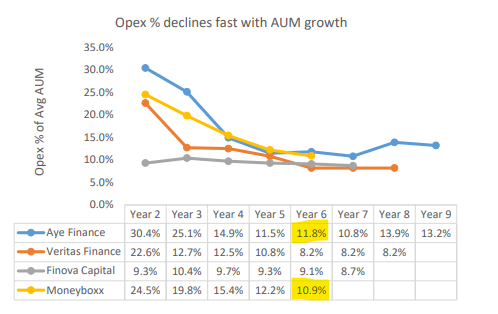

- It is projected on the opex front that MB should do better than Aye and through MB has always had a better asset quality then Aye thought we cannot have a direct comparison as Aye has a larger book but this also something we can track going forward

All in all MB also has valuation comfort and if the grow at 100% while maintaining asset quality they definitely deserve a 3.5 to 4 PB (five star getting 4) which would imply a 50-100% gain from current levels

Dic - invested, can be wrong

Moneyboxx Finance Ltd_Stock Idea_Final.pdf (2.4 MB) (wonderful report to have a look on)