Moneybox finance - Business Overview

- Founded in 2018 by Deepak Aggarwal and Mayur Modi, Moneyboxx Finance is a listed NBFC that offers unsecured and secured credit to underserved micro enterprises. Run by promoter management having significant experience at JP Morgan, KPMG, Bank of America, Deutsche bank etc,.

- Company disburses loans in the range of INR 70,000 to 3 Lakhs in unsecured loans and 2-10 Lakh in secured with tenures ranging from one year to seven years in Tier 3 and below locations (rural/semi-rural/semi-urban).

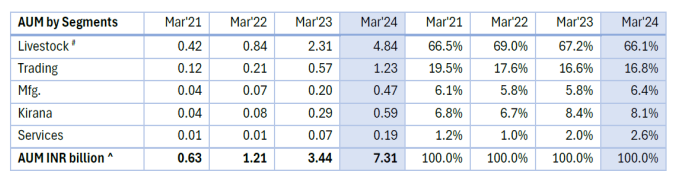

– The key area catered by them is diary. Unlike other finance companies which go by cluster based approach, Moneyboxx is going after essential based approach which helps in protecting in credit cycles.

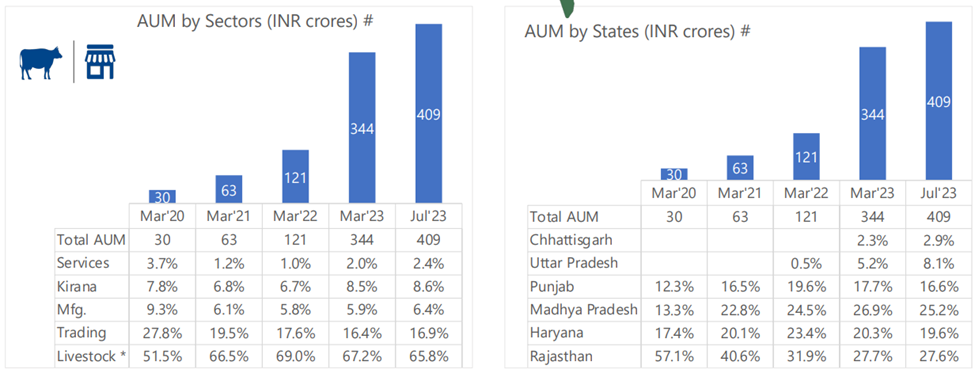

– Diary customer is one with 5 min. livestock and agriculture land. Which gives 2 streams of income. Diary forms 60% of portfolio. Diary is followed by Kirana which comprises 10% of portfolio. They have veterinary doctors in their payroll.

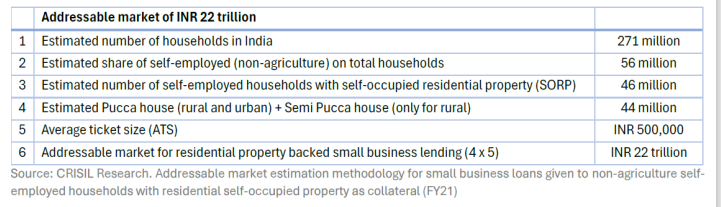

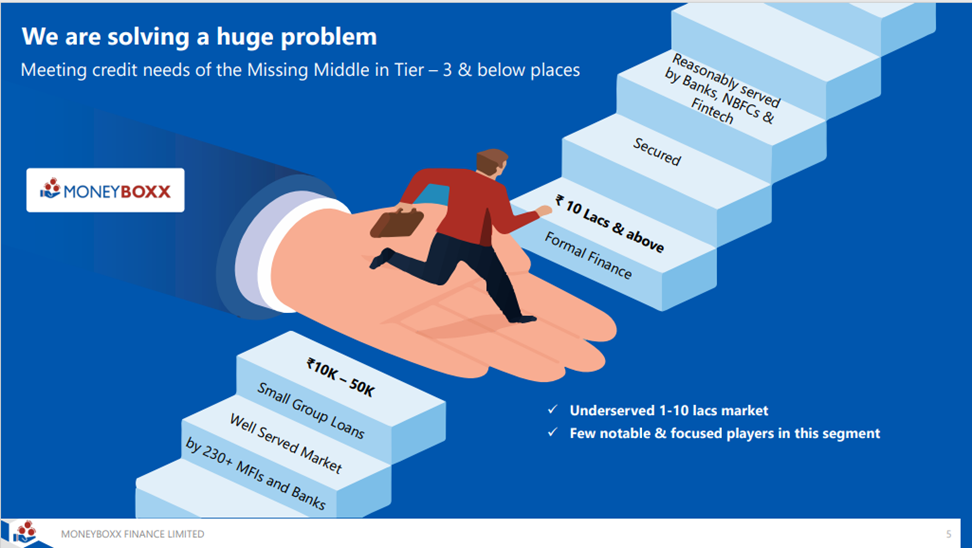

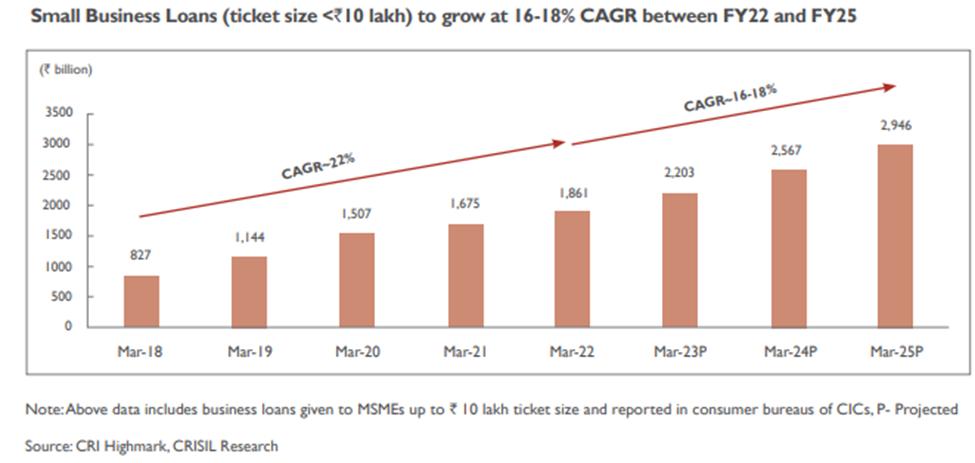

– Opportunity size in 1-10 Lakh loans is 22L Cr. The size in organized in 2L Cr. Alternatively, livestock accounts for 7% of GDP which is 15L Cr. Using both methods of estimation, opportunity size is huge. Kirana is double the size.

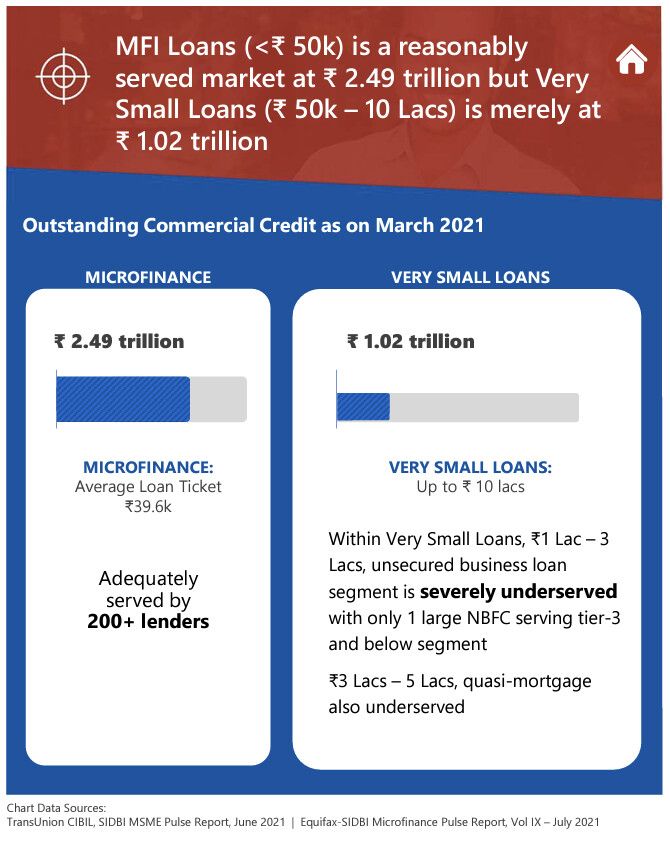

– Microfinance with a ticket size of upto 40K INR is better served with 2.5L Cr credit while very small loans is only served by 1L Cr. This is a dated report (July 21) but gives a picture on the underserved opportunity.

– There are 250 NBFC/MFIs which give loans to 8-10 with a ticket size upto 50k INR. This is a 3 lakh Cr industry running since last 2 decades.

– Moneyboxx wants to address the ticket size above 50k INR. Tenure is upto 2-3 years in case of unsecured and 4-7 years in case of secured.

– The loan target group don’t have ITRs/GST history/Banking history.

– Earlier they were primarily into unsecured loans. Over time, as cost of borrowing started coming down, they moved to secured lending as well. In Q4FY23, 6% of disbursement is in secured and in Q2FY24, 22% of disbursement is secured.

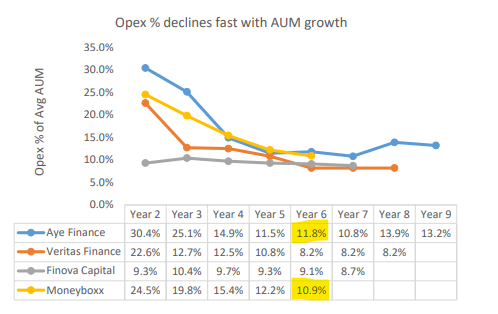

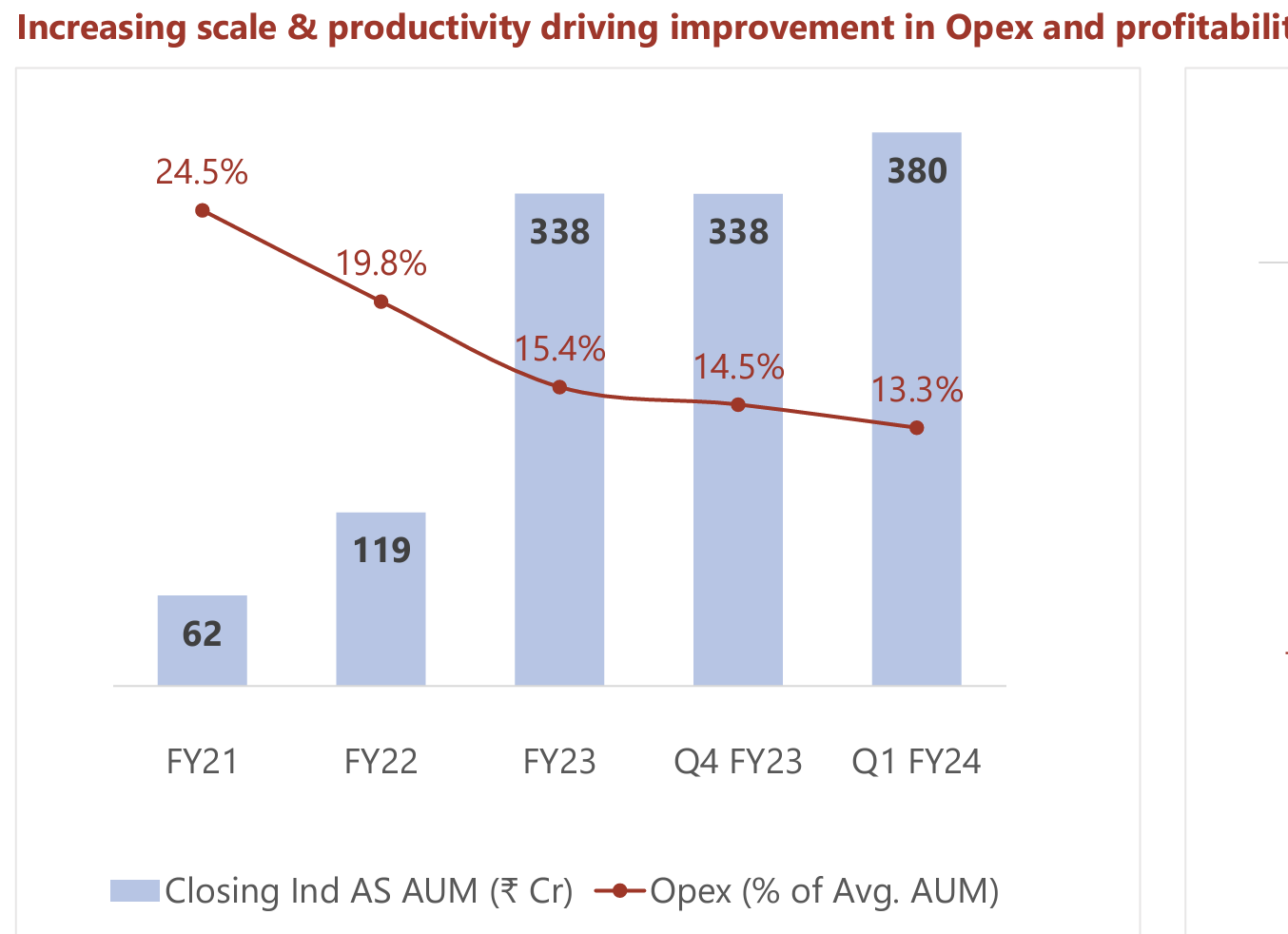

– The model has higher opex in the beginning and it comes down over a period of time.

- This is a branch led model with 100% digital processes where loan officers are hired for the branch and try to source loans in nearby villages. They will be visiting the locations physically to onboard and collect money.

– The Loan Relationship Manager (LRM) who disposes the loan is responsible for the collection as well.

– The incentive structures - bonuses etc,. - are directly tied to the asset quality. - Cumulative disbursements of 917 Cr with 536 Cr Outstanding AUM out of which 17% of outstanding loan book is secured. 64% of the lending is on-book while rest of it is managed.

Progress

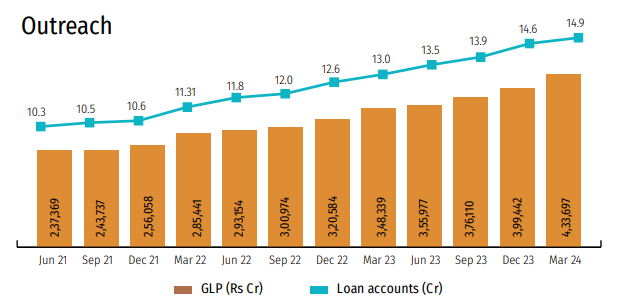

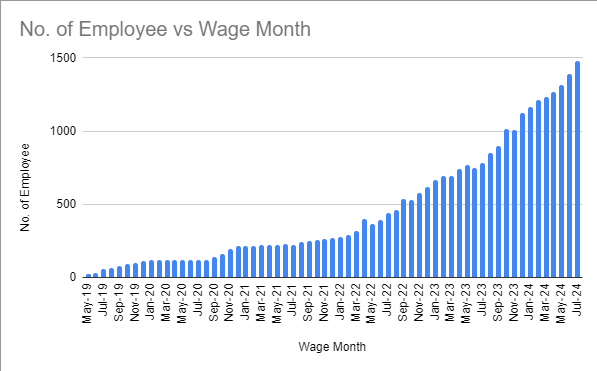

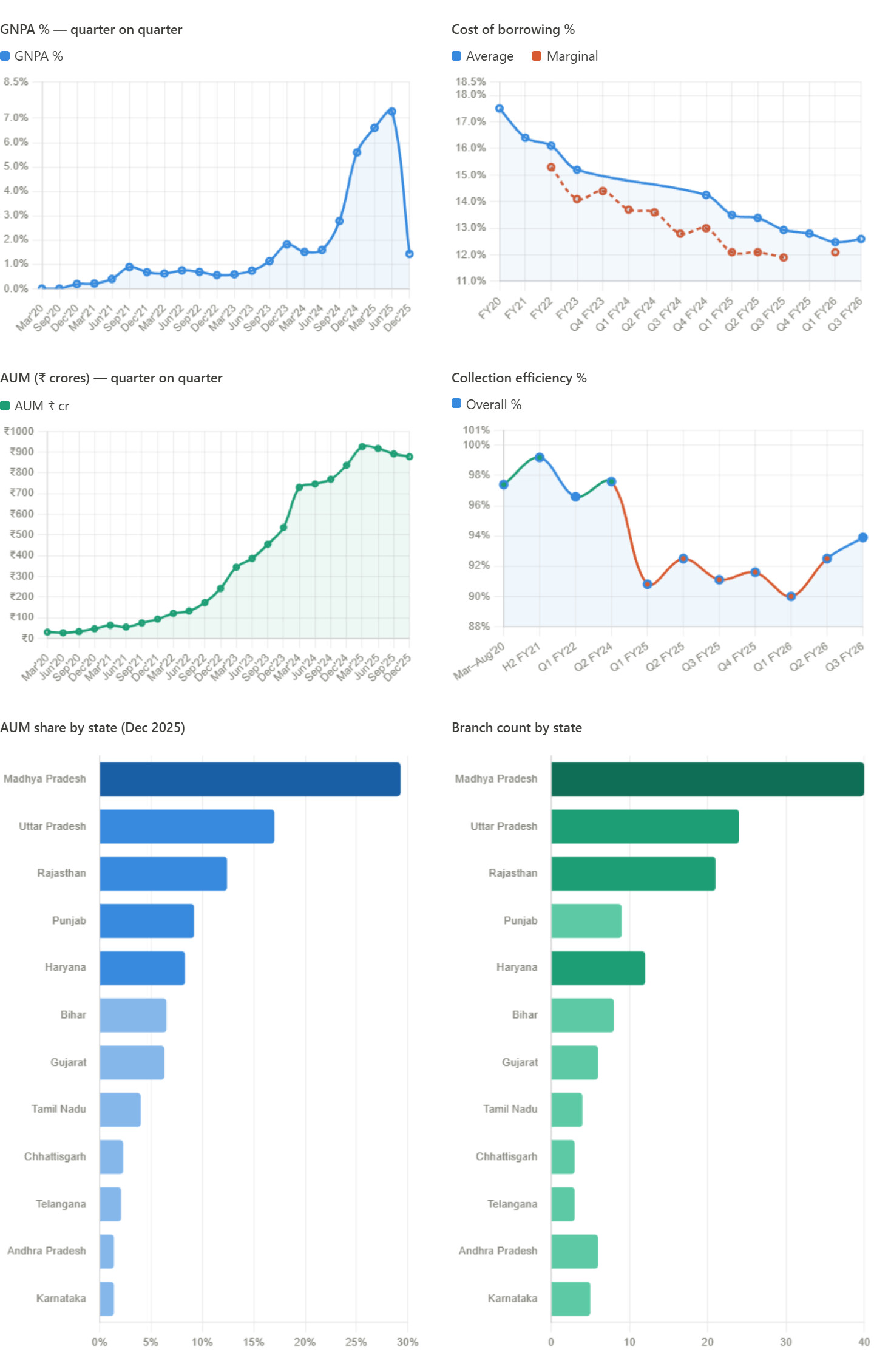

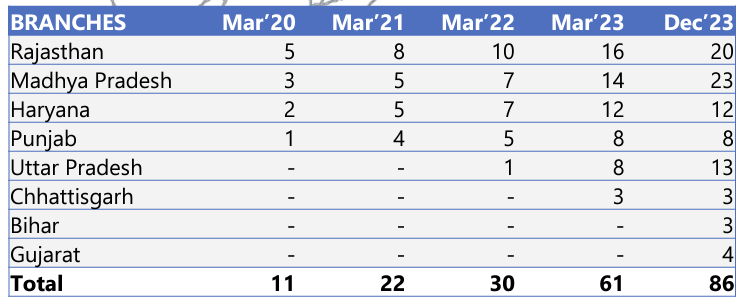

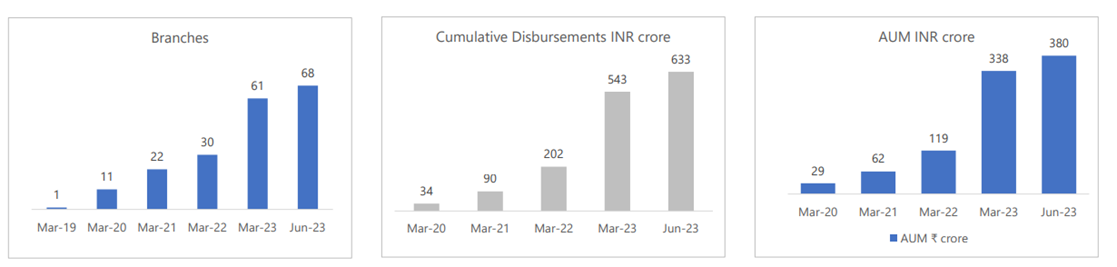

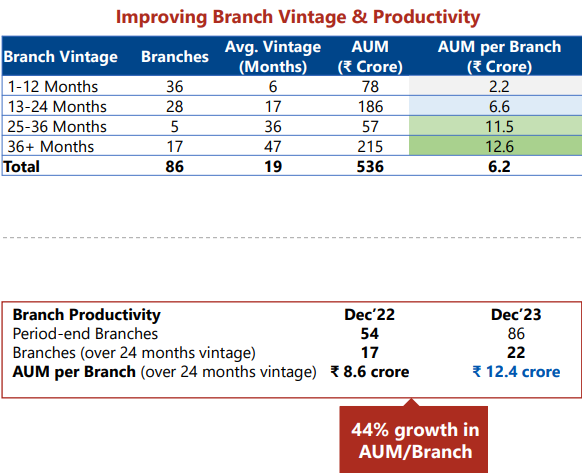

- Branch footprint - Grew from 11 branches/4 states in Mar’20 to 86 branches/8 states in Dec '23.

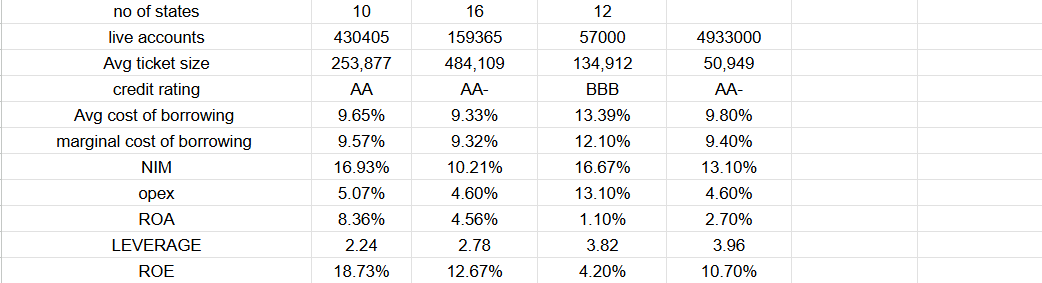

– No state has more than 26% AUM. (In June 22, it used to be 32%. In Dec 22, 29%. Steady improvement)

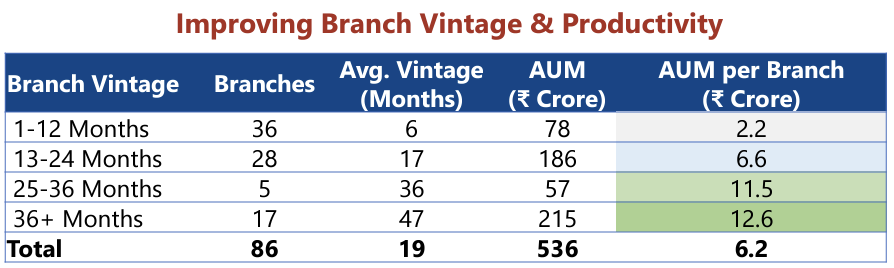

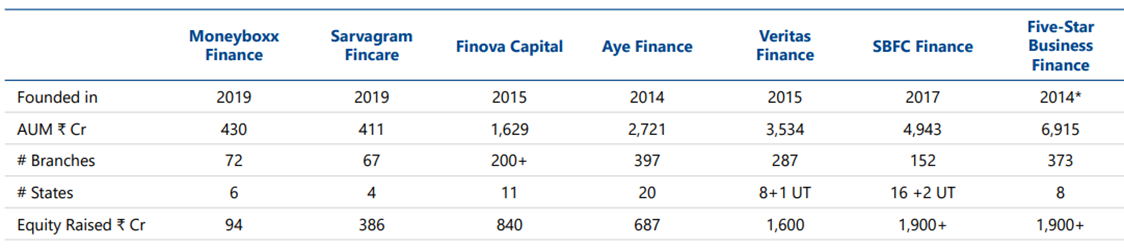

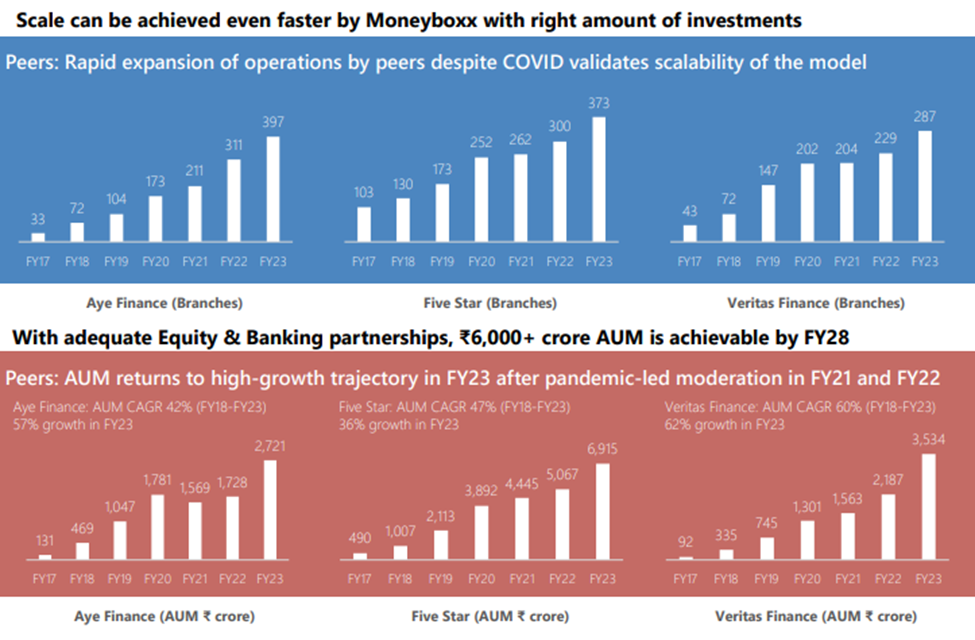

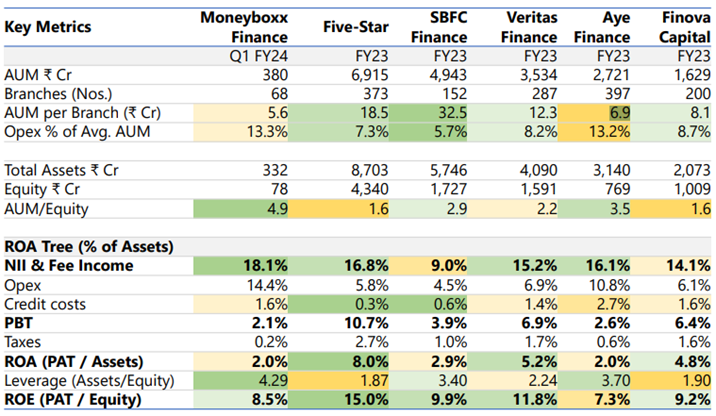

– In case of larger players like Finova, Sarvagram, Five Star, Veritas top 3 states form 85% of portfolio (mangement’s words). - Average AUM per branch goes up as the branch ages.

– 27.1% loans are from repeat customers

– An average branch takes 2.5 Cr AUM and 6 months to break even.

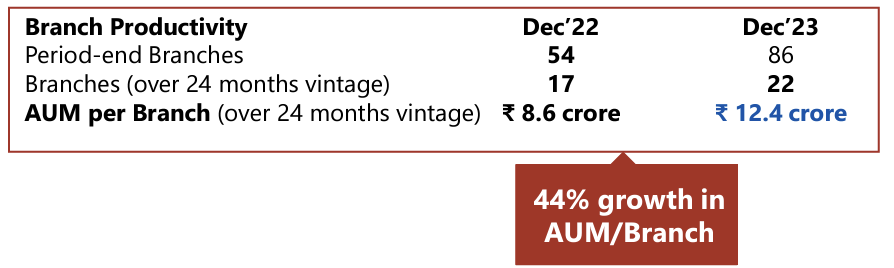

– There are branches which did 10% PBT at 11-12 CR AUM. - AUM/branch (aged > 2 years) grew by 44% YoY.

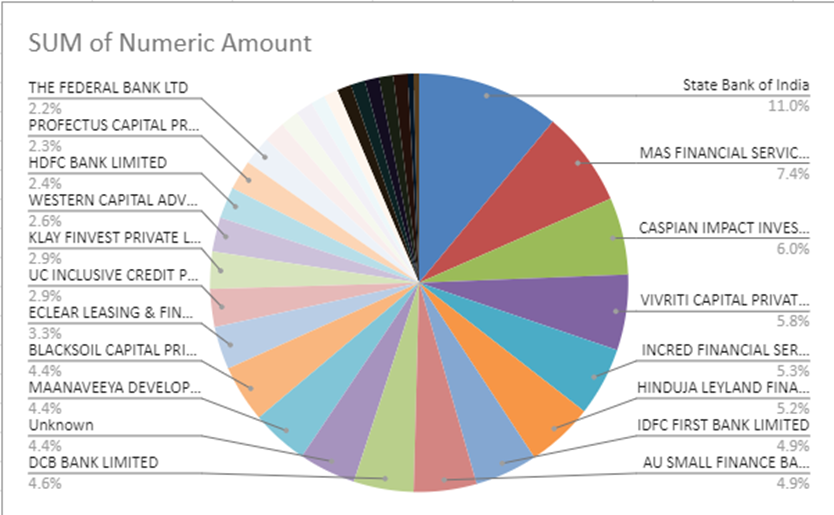

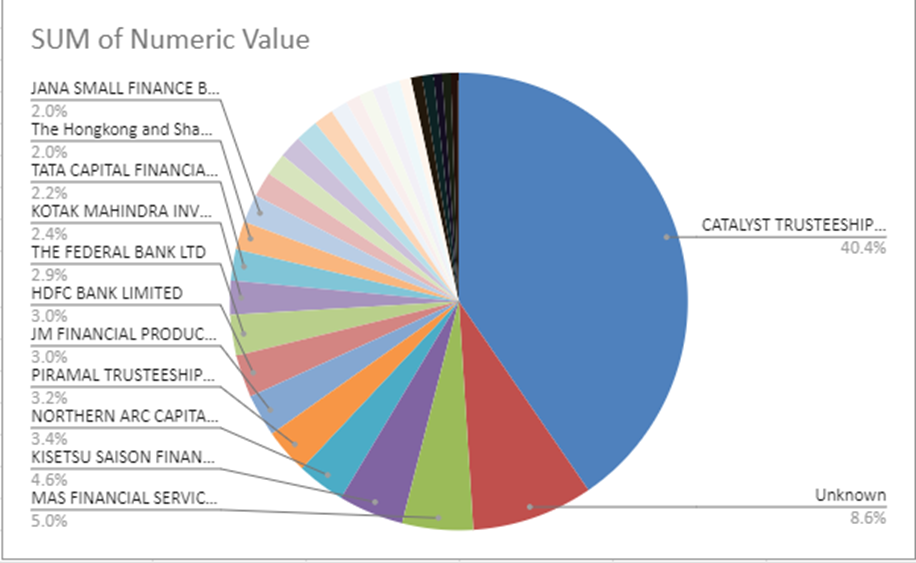

- Lending Partnerships - working with 30 lenders including 9 banks. Testament to their underwriting to be able to work with many reputed lenders.

- They’ve a co-lending/BC line of 35 Cr per month from Vivriti Capital, MAS and Utkarsh SFB

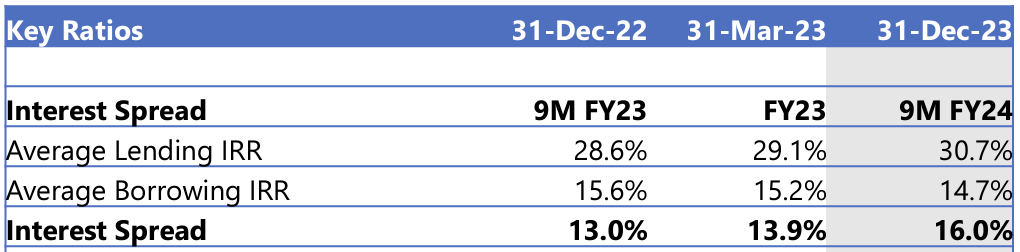

- Improving Spread - Spread improved by 3% due to increased lending IRRs and reduced borrowing costs. 32% yield in unsecured and 24-25% in secured. Cost of borrowings used to be 17.5% in FY20, 16.4% in FY21, 15.2% in FY23. Incremental borrowing cost is 12.48%.

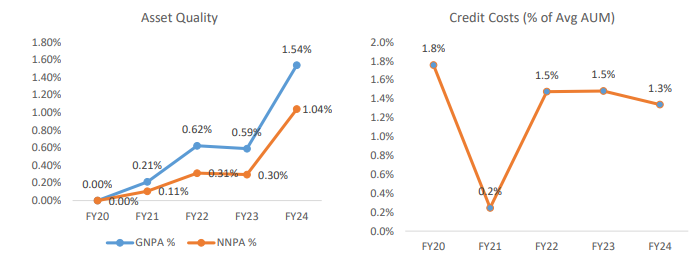

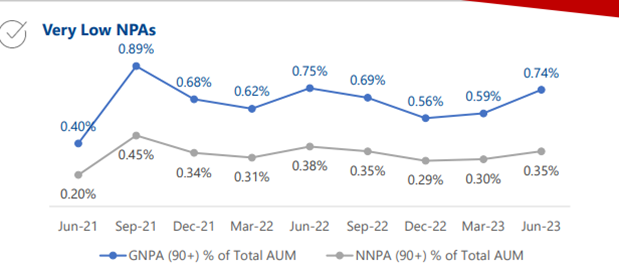

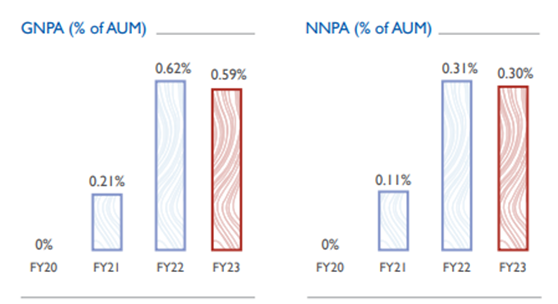

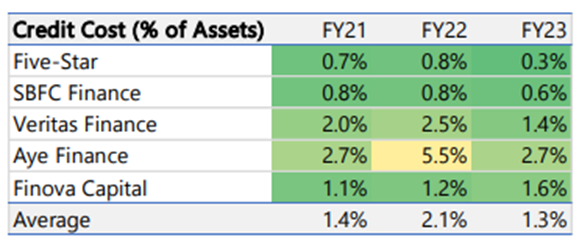

- Asset quality - Credit costs are in the range of 1.28% to 2%. Reasonable for 13-16% interest spread.

– management is guiding 1.5-2% credit costs in unsecured loans and ~1% in secured loans.

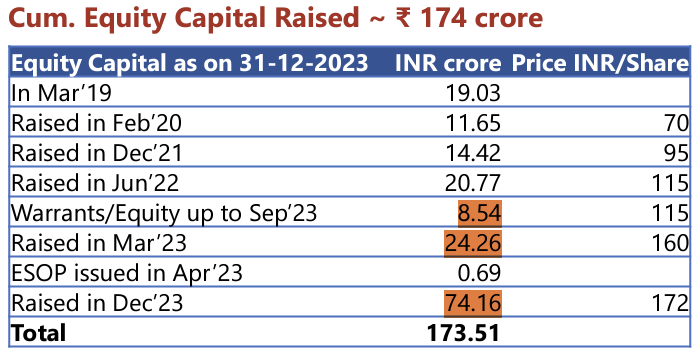

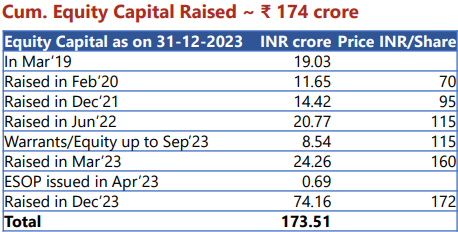

– lead generation to asset quality ratio is in the tune of 13-14% - Equity capital - Company has raised a cumulative 174 Cr equity capital from March '19 to Dec '23 out of which 99 Cr raised in this financial year.

– equity capital helps with new branch initial capex/opex till branch becomes profitable, FLDG and to maintain debt/equity ratio.

– Covenants from lenders allow them to do 750 Cr AUM on 100 Cr Equity. However, they’d like to do 500 Cr AUM for 100 Cr equity so that debt/equity stays at 4:1

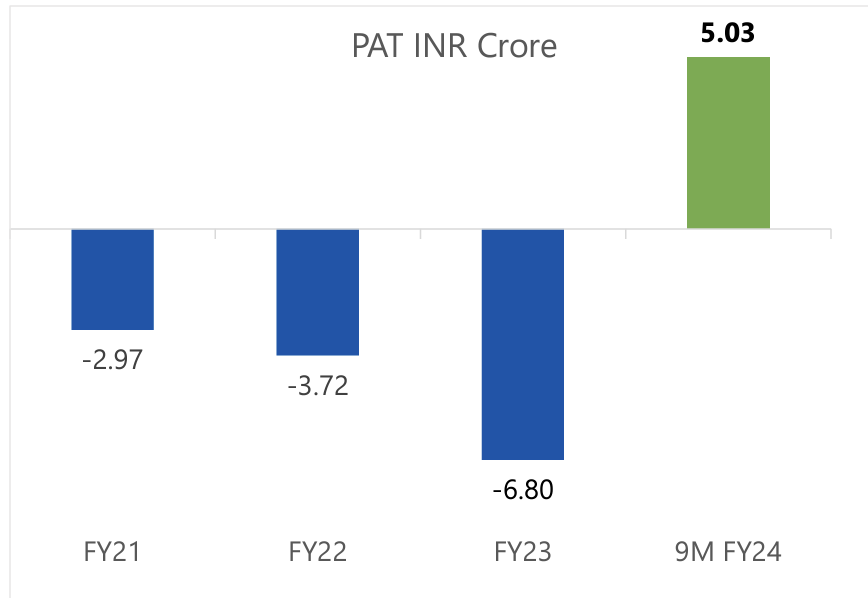

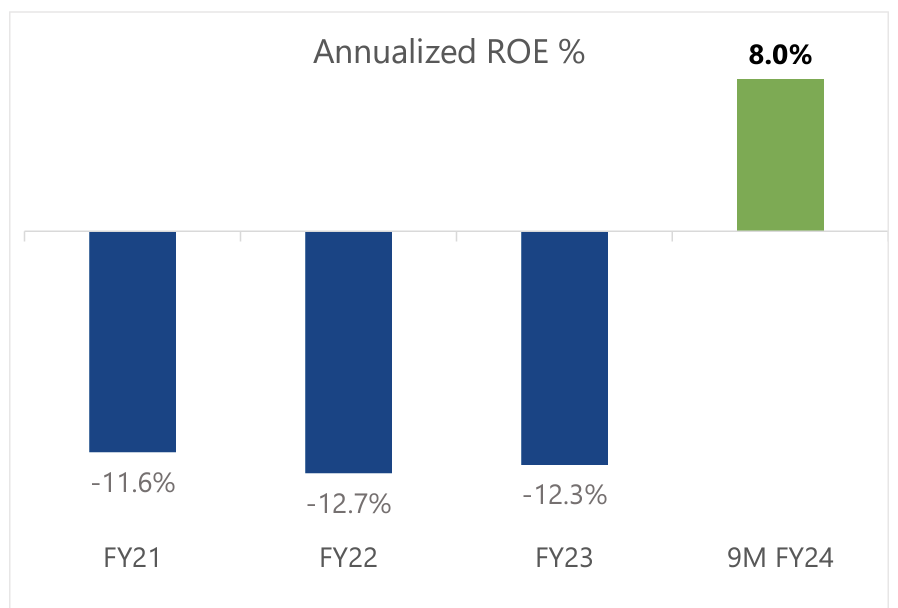

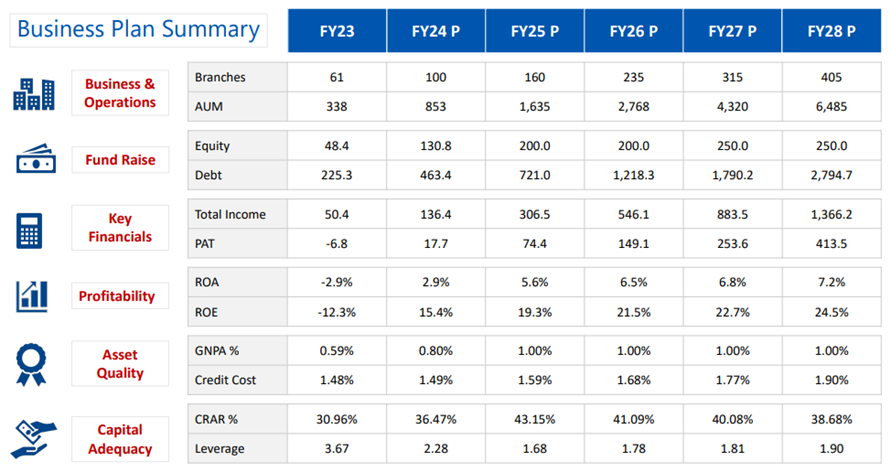

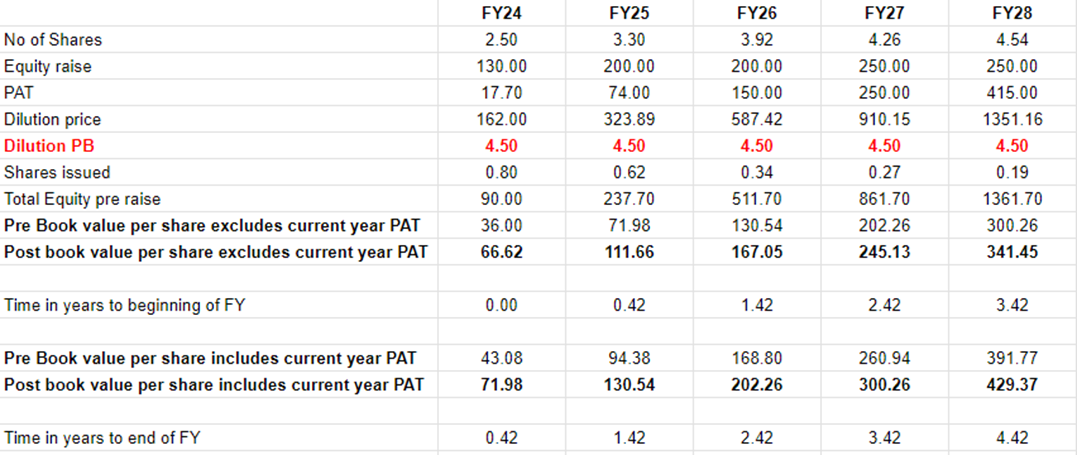

– To hit the target of 6850 Cr by FY28, management assumes 1500 Cr equity is needed. From the current levels of 175 Cr networth, 800 Cr could come from additional equity in next 4 years and remaining from profits. - Aided by increasing margins, average age of branches, company became profitable in FY24 demonstrating increasing ROEs YOY

– management is guiding double digit ROE soon. - Opex % coming down as AUM scaled over time

- Ratings - Currently rated at IND BBB- (Positive). FY24 is turning out to be a profitable year and company subsequently raised 75 Cr. Could result in ratings improvement. In case of NBFCs, better ratings help in negotiating better interest rates.

Ambitious Targets

- FY24 - 800 Cr AUM/100 branches. As per filing on Jan 1st week, company reached 90 branches.

- FY25 - 1600 Cr AUM - presence in 3 additional states - karnataka, telangana and tamil nadu. Expecting to cross 15% ROE. With secured loans, AUM goes up quickly as loan sizes are bigger.

- FY 28 - Long term AUM Target of 6485 Cr (20x AUM growth), 400+ branches (6x growth)

Cons/risks -

-

Higher valuation - At a CMP of 277.5, Company is richly valued @ 5.26 times book (Book Value Per Share = 53.86).

-

Political risk - during elections, loan waivers result in NPA spikes.

-

Credit rating stayed the same BBB- since last 4 years of their operation. Dropped a note to moneyboxx team. Will update once I get response.

-

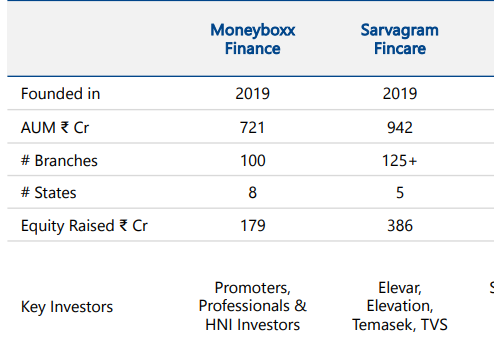

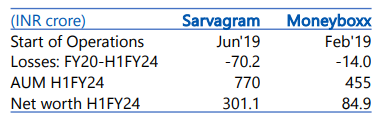

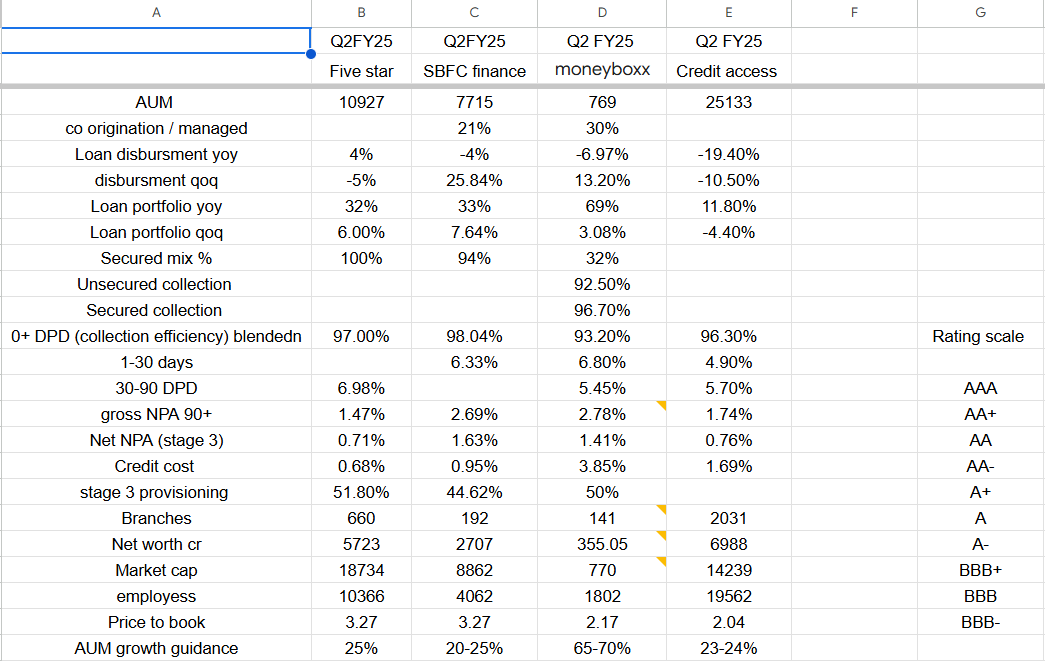

Competitors: Five Star Finance, Finova and Aye Finance, Vistaar, Veritas, Sarvagram (Gujarat,Maharashtra) etc,.

Conclusion: It is easy to give loans. To grow reasonably well, one has to maintain good asset quality over long period of time. In India, there is huge underserved opportunity beyond banks. However, maintaining asset quality is important. Company is at an inflection point with reducing interest rates => Increasing yields and moving to secured portfolio => reduces credit costs.

Disclosure: Interested. No position yet.

–

Sources:

Some key points

Some key points

!

!