Are you aware why it has fallen 30% in the last one month?

1 Like

Due to no conference calls etc, I had written to the company in beginning May to understand the growth in the last year, guidance for next year in terms of sales and margins. The company finally replied in mid June, and over the email the VP has mentioned they expect 20-25% sales growth next year + maintenance in margins. For me this continued to be a strong thesis once I built in the guided numbers for next year. I would though appreciate if anyone can share the track record of the management in terms of guidance in the past.

A screenshot of the mail is attached, with my queries as the questions and the company’s response in yellow.

Technicals and price action now suggest otherwise though, looking at the moving averages and RSI.

Disclosure : Continue to be invested. Biased. I am not a SEBI registered advisor and this is not investment advice.

20 Likes

Why is dividend yield so low? It is a KPO business which doesn’t need any capex.

1 Like

That was as good as listening to a concall. Thanks for the good questions and sharing it with us. I wanted to know what is the proportion that EV sector contributing to their revenue and future expectation from EV in terms of growth. Let us know if you got these.

1 Like

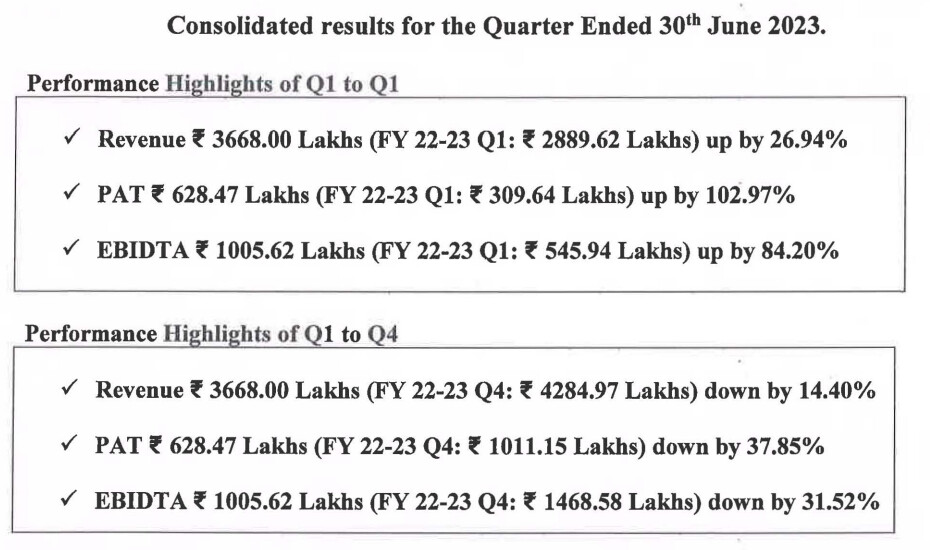

Company delivered good result . Revenue up 27% and PAT up 102%

Looks like management is walking the talk. Few insights:

CES (Civil)

• Q1 generally are less invoiced as compared to end of year (expect much higher number in Q3-Q4)

• 2 Big project worth 20K ton in coming quarters

• Improved project work and quality led to Tier 1 clients

• Expecting new clients in Fixed teams and precast concerte detail and design

MES (Mech)

• Order on hand $ 1.1MM vs. $0.2 MM (450% higher)

• Hired 115 trainee for Civil and Mech

* Looking for acquisition in US in both Civil and Mech division.

10 Likes

Some description of various present and future segments of the company -

Civil Engineering Segment

Steel Detailing

Steel fabrication and structural steel detailing are two important parts of the construction industry. These two groups work in tandem to ensure that structures are made safely, efficiently, and to specification.

- Steel Fabricators: These are professionals or companies responsible for cutting, bending, and assembling pieces of steel into specific shapes or structures. This is often done based on detailed plans provided by structural steel detailers. Once the pieces are fabricated, they’re transported to the construction site for assembly. Steel fabricators often work on projects such as buildings, bridges, and other infrastructures that require steel structures. They also do fabrication for various other industries including automotive, aerospace, shipbuilding, etc.

- Structural Steel Detailers: These professionals prepare detailed plans, drawings, and other documents for steel fabricators and erectors. Using engineering drawings and specifications from architects and engineers, they create detailed ‘blueprints’ for the fabrication and erection of the steel framework. The detailer’s drawings provide all the information needed to cut and weld all pieces together.

There are other entities in the value chain -

- Steel Manufacturers: These are the companies that produce and supply the raw steel that is used by fabricators.

- Architects and Engineers: These are the professionals who design the structures and provide the initial drawings and specifications that detailers use to prepare their more detailed plans.

- Steel Erectors: These are the teams that physically assemble the fabricated steel pieces on the construction site, based on the plans provided by the detailers.

- Construction Companies and General Contractors: These entities manage the overall construction process, often subcontracting the fabrication and erection work to specialist companies.

- Building Owners and Investors: These are the people or organizations that fund and benefit from the final structure

Building owners hire GCs, who then hire steel fabricators and subcontractors, who then hire steel detailers. Their role is to take the initial designs from the architects and engineers and create detailed ‘blueprints’ for the fabrication and erection of the steel framework. Architects and designers are hired by GCs or directly building owners at times. This is key because Mold Tek is looking for prudent acquisition in this space to move into structural designing and architectural services where the value addition is higher. With this, their relations with General contractors (GCs) would increase and they can take end to end responsibility of project architectures, detailing. They want to acquire a company of $5-$10M size where founders can stay for 5+ years with them.

Companies who could be clients/potential clients of Mold Tek in this space -

Major Steel Fabricators:

- Nucor Corporation: One of the largest steel producers in the United States, with extensive fabrication services.

- Steel Dynamics: Another large US steel producer and fabricator.

- Schuff Steel: One of the largest and most experienced structural steel fabricators and erectors in North America, owned by DBM Global.

- High Steel Structures LLC: A company that offers structural steel fabrication for bridge and building construction.

Major General Contractors:

- Bechtel: One of the largest globally operating general contractors based in the U.S.

- Turner Construction: A North America-based, international construction services company.

- AECOM: A multinational engineering firm with construction services among its offerings.

- Kiewit Corporation: One of the largest construction and engineering organizations in North America.

- Skanska USA: An international construction and development company with a strong presence in the U.S.

Mechanical Engineering Segment

BIW Fixture Design

BIW (Body in White) refers to the stage in automotive design or automobile manufacturing in which a car body’s sheet metal components have been welded together. It includes doors, hoods, and deck lids, but does not include the vehicle’s engine, chassis or interior.

BIW Fixture Design refers to the process of designing fixtures that are used in the assembly of the BIW components. Fixtures are essentially jigs that hold the components together in the correct orientation for them to be assembled, usually by welding or similar processes. BIW fixture design involves a combination of mechanical design principles, CAD (Computer Aided Design) tools, and an understanding of the manufacturing processes involved in automobile production.

This design process is important for a number of reasons:

- Precision: Fixtures must be designed to hold components in exactly the right position, to ensure that the final product is assembled correctly.

- Speed: In large scale manufacturing, the speed of assembly can significantly impact the cost and feasibility of the production process. Thus, fixtures should be designed to enable quick and easy placement and removal of components.

- Repeatability: The fixtures should enable the assembly process to be highly repeatable, minimizing variations between different instances of the same product.

- Safety: The fixtures should be designed in a way that is safe for the operators to use, to prevent workplace accidents and injuries.

- Durability: Given the high volumes in automotive production, fixtures must be durable to withstand repeated use over time without wearing out or degrading in performance.

Key players who make BIW fixtures and FFT, VDL, GeStamp are customers -

- Paslin

- Hirotec America

- Fori Automation

- Esys Automation

- JR Automation

- KUKA Systems North America LLC

- FFT

- VDL

- GeStamp

Press Tool Designing and Drafting

Press tool designing and drafting services are related to the creation of press tools, which are used in manufacturing industries to form, shape, or cut materials. These tools are essential components in processes such as bending, punching, forging, or shearing.

Outline of what press tool designing and drafting services typically involve:

- Press Tool Designing: This is the process of creating a detailed and precise blueprint of a press tool. The design should factor in the specific requirements of the production process, the material being used, the shape and dimensions of the product, and the capabilities of the press machine. The tool design should also consider the stresses and forces that the tool will encounter during operation to ensure durability and optimal performance. This often involves using engineering principles, material science, and software tools to come up with the best possible design.

- Drafting Services: This refers to the process of creating detailed technical drawings of the press tool design. Drafting can be done manually, but it’s usually done using computer-aided design (CAD) software. The drafting process creates a visual representation of the press tool, showing all dimensions, parts, and assembly instructions. The drafted plans are crucial for the toolmaker who will fabricate the press tool.

Press tools are used in automotive, aerospace, construction, electronics, medical industry etc.

Key players in press tools in US -

- Dayton Progress Corporation

- Wilson Tool International

- Mate Precision Tooling

- Impressions Stamping

- Anchor Danly

- American Punch Company

Stamp dies segment

Stamping in the engineering space is a metalworking process by which sheet metal or other material is shaped by pressing or punching with a tool called a stamp or die. A “stamping die” is a specialized, precision tool that cuts and forms sheet metal into specific shapes. They are typically constructed from hardened tool steel that can withstand the high stress and wear that comes with continuous use.

The design and manufacture of stamping dies are greatly facilitated by the use of Computer-Aided Design (CAD) and Computer-Aided Manufacturing (CAM) software. These tools allow engineers to create, modify, analyze, and optimize designs digitally before manufacturing the physical tool. This is where Mold Tek would be doing work maybe

Stap dies are used in automotive, aerospace, construction, electronics, medical industry etc.

Key players who make stamp dies -

- Magna International

- Gestamp

- Die-Tech & Engineering

- Schuler Group

- Feintool

- Dongguan Fortuna Metal & Electronics Co., Ltd

- Manor Tool & Manufacturing Company

Wire Harness Segment

A wire harness, also known as a cable harness or wiring assembly, is a grouping of electrical cables or wires that transmit signals or electrical power. They are often bound together by straps, cable ties, conduit, or a combination of these to form a single assembly. Computer-Aided Design (CAD) is often used in the design and engineering of wire harnesses. CAD tools allow engineers to create 2D drawings or 3D models of the wire harness assembly.

Key players who make these -

- Yazaki Corporation

- Sumitomo Electric Industries, Ltd.

- Delphi Automotive (Aptiv)

- Leoni AG

- Motherson Sumi Systems

- Fujikura Ltd.

- PKC Group (Motherson Group)

Why Mold Tek

- Cost arbitrage as Indian labor is cheaper for American steel fabricators and GCs to hire for steel detailing kind of services

- Relationship and credential built with clients in steel detailing and MES space over last 8-10 years

- Outsourcing in this industry is still very less as fabricators, GCs do not want to compromise on quality but over time with low cost moat and credentials built, Mold Tek wants to outgrow the underlying industry growth

Prominent work done by the company

- Steel detailing for airports, industrial plants, Amazon warehouse, 64 storied building in Chicago

- Did part of steel detailing for World Trade Center

- Awarded by trade bodies in US in field of civil structural engineering

- Worked as tier-2 supplier for BIW fixture design for EV platform for Tesla

- Working with FFT, VDL, Gestamp in EV related projects. These companies call Mold Tek engineers for on-site work and the relations have strengthened over the years

- Did $1.2M work in poles and transmission tower design (non-automobile work)

Strategy

- Move into architectural and design space

- Acquire company in architectural and designing space as mentioned above

- Hired two PE stamp engineers. PE (Professional Engineer) stamp, also known as a PE seal, is a certification mark that signifies that an engineer has been licensed by a state’s licensure board. Each state has its own specific licensure requirements and only individuals who have met these requirements are legally allowed to provide their PE stamp. The PE stamp is used across many disciplines, including civil, structural, mechanical, electrical, and environmental engineering. In the context of structural steel detailing, a PE stamp on the detailer’s drawings signifies that the designs meet the necessary safety and performance standards and comply with applicable building codes. These PE stamp engineers hourly charges can $60-$100 for Mold Tek as against current charges of $28-$30 per hour in steel detailing

- Groom engineers in-house and train them for projects through learning systems made at the company as quality is of greatest importance in this business

- Grow MES segment 25-30% of the pie

- Currently doing most of the work in BIW space

- Get into press tool design and drafting services, stamping dyes and wire harnesses in MES

Competitors

- Tata Technologies

- Onward

- CSG Technologies

- Proteus

- Countries - Romania, Indonesia, Philippines

Guidance

- Guidance to maintain EBITDA margins if the sales growth of 25-30% sustains

- Margin improvement triggers

- If they move higher up in the value chain in architectural and designing services and get direct work from GCs and OEMs

- Target of 55-60 Cr EBITDA in FY24

28 Likes

Initial thoughts:

As a Civil engineer working on similar projects, I feel, the work they do, needs very basic engineering and designing skills with no competitive edge. This industry is very much fragmented with lot of unlisted and small companies. They do the same with basic Tekla license and producing a detailed drawing from structural drawing doesn’t need any sort of skill except a software license.

At present the advantage for them is doing the US projects with cheap designers in India which could be the cause of higher OPM. To know the sustainability of client relations and risk of not getting repetitive clients ( due to quality issues), I will research further to know the clientele, through my friends in the same industry.

I work in UAE as engineering manager and we also offload our work to Indian companies for cost advantage. But Indian companies are struggling with Structural Engineeing, as it’s very less margin business due to higher salaries of Engineers, when compared to detailers (mostly diploma holders and ITI candidates).

In mechanical domain, they are doing good though.

Just started reading about the company and shall try to give more insights with the knowledge and expertise I have in this industry.

42 Likes

Update 2:

As per my scuttlebutt with the Industry people, Mold Tek majorly into detailing and not into Engineering (low margin as explained earlier). They do only connection design as part of Engineering activity (but done using software SDS/2 without much manual intervention required). Like I’ve explained in earlier post, detailing for US projects is high margin business, as you can hire just diploma holders (average starting salary is 10k per month and 10 years experienced is not getting even 60k per month) to get the job done. For client coordination and project management they have US office with PE licensee Engineers, which is smart move and definitely a moat when compared to the small companies. Clients would definitely prefer to deal with the employees sitting in US for saving communication and project management time. Also, they can offset the disadvantage of time difference between Ind and US.

So, as of now, I reckon that, the moat they have is getting projects from US due to established Business development and project management offices at offshore and getting the actual chunk of job done by cheaper resources from India. Also, they have smartly put the resource offices in tier 2 cities like Vijayawada and Nashik, where the wages are too low for the detailers.

Shall keep on update my findings as when I get something.

40 Likes

let’s add a different perspective to this co:

Driving factor: Their abnormal industry leading margins

Disclaimer: Invested and Intrigued.

They operate in two verticals.

- Mechanical engineering services

- Civil Engineering services

About mechanical engineering services:

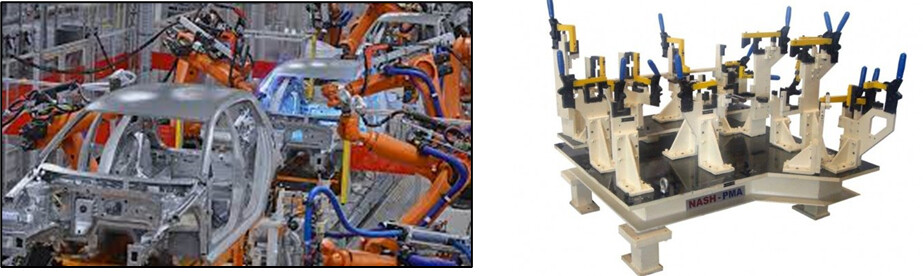

First of all, why do you need BIW fixture design and robotic simulation?

As everyone knows car manufacturing involves different assembly lines for different assemblies/sub-assemblies. For example, BIW assembly line, Door assembly line, Roof assembly line, Engine assembly line etc finally each sub-assemblies will be assembled to make a complete car. So, the total time involved to make a complete car is called “cycle time” (how many cars you produce per time considering you have all the sub-assemblies ready) for example Tesla model 3 cycle time is 64 sec which is half the Auto industry average our Indian TATA Harrier has cycle time 104 sec ( not an apple to apple Comparision) but tesla employees more robots (500+) and less manual intervention (95% automation). So, cycle time plays a very important factor in the overall manufacturing cost! that’s what we call “scale economies” (Ford invented it, Toyota mastered it, Tesla set the standard!) in Musk’s own words,

![]()

to each achieve a particular cycle time you need to design the production line and run a virtual simulation of an assembly line which consist of robots, fixtures and a conveyer belt to move the parts from one station to another as shown in the below picture to calculate whether you are actually achieving or not right!

That’s where the 3-D modeling tools like Catia and simulation software’s come handy (each license costs 10L up to 50L and A&M of 2L annually, pretty lucrative right! that’s the power of SW product companies!).

OEM’s gives these assembly line set up (design and simulation) to Tier 1’s such as FFT, VDL, KUKA etc and they will give to Indian or Mexican counter parts! (You know why!). Pls watch the below video to understand how it’s done. Which involves both modeling and robotic arm simulation. Don’t overimagine/overestimate when they use the term “Robotic simulation” because I’ve observed many people get overexcited when they saw the word in their concall report.

Let’s talk about Civil Engineering services:

Structural Steel Detailers: These professionals prepare detailed plans, drawings, and other documents for steel fabricators and erectors. Using engineering drawings and specifications from architects and engineers, they create detailed ‘blueprints’ for the fabrication and erection of the steel framework. The detailer’s drawings provide all the information needed to cut and weld all pieces together. Mold Tek majorly into detailing (low margin) and not into Engineering. Those are not my words management itself says “Let’s say, we are charging $25, $28 or $30 at the most in detailing, we can aim at $60 to $100 in design, member design. But currently, we are not doing member design.”

Now we will discuss operating matrix of the co, with such low billing rates in Civil engineering services ($25/hour) and Mechanical engineering services ($18/hour) they are clocking north of ~30% OPM that’s just Wow right!

Let me tell you before all of you assume that Co is addressing to “Niche” segments which no listing player is operating or left the field. Just look at their employee realization matrix, you will realize that they are grabbing low hanging fruits out there (in terms of type of work)

Moldtek is Rev155 cr/1200 employees = 13 lakhs per employee

Kpit is at Rev 3777 cr/8053 employees = 47 lakhs per employee

LTTS is at Rev 8,716 cr/23,392 employees = 37 Lakhs per employee.

that’s the very reason why KPIT and LTTS just ignored these verticals and focused on other verticals quickly big time. So we must be happy right ! biggies left and you set the prices! Unfortunately, no! There are infinite small/chota/meduim players operates in this space, if you don’t do it for $18 there are plenty who are ready to pick the work @ $15. Pls find few small players below to name few.

Satyam-Venture Engineering Services

Mechanical Engineering Services | Envision Integrated Services Pvt. Ltd. (envisionis.in)

[Group of Engineers] (https://www.groupofengineers.com/)

Two ways to look at the business:

First: You should appreciate the company and be more than happy as the Co is showing how a service company should run to other service co’s despite being having a very low billing rates ($ terms) still be able to maintain OPM north of ~30%. By using some ways like getting talent from Engg trainees by offering low pay + doing some “naughty license proliferation” things etc etc those are different matters altogether ![]() and that’s absolutely fine as long as you are doing great for us (investors) not for employees though!

and that’s absolutely fine as long as you are doing great for us (investors) not for employees though! ![]() )

)

Second: You should start feeling little uncomfortable about how long these type things can continue to work once the company scales up because they day you start doing business with direct OEM they will inspect your infrastructure physically and check your legalities etc.

A bit of overconfidence words from management, which taste sour to me, but you can totally ignore my views! ![]()

It’s fine if you are not aware of what others are up to, considering your busy schedule but don’t assume the things and paint a rosy picture for yourself and to investors. Which will hurt you and as well as investors.

Well, that is an outright lie, you spend three days a month on the company and come on concalls to give these blatant lies.

So, if you don’t spend your maximum amount of time on the company then don’t address the concalls and don’t assume that others are also at your level because they are clearly not! Nothing wrong in aspiring and competing with others but it’s foolish to assume that others are also at your level (you are doing $20 million rev and KPIT is doing $400 Rev and you are saying both are at same level pls take a look at their employee realization and avg billing rate they charge to the client).

Ok, lets try to understand why i said so,

what KPIT does

- Service business : KPIT calls it with a fancy name called “Feature Development & Integration” in their presentations. What it does: provides engineering services to Automotive industry OEM’s and TIER1’s in ADAS (Feature Development & Integration), Connectivity (cloud based) and Electrical vehicles (Architecture & Middleware Consulting) in US and Germany predominantly. Among these services some of them are in-house (i.e., you execute projects Pune and Bangalore offices) and some of them are sending your workforce to respective client sites (H1-B, L1visa types). Net-net these are 20-23% margin types. Absolutely NO IP here

- Inhouse product development : it is trying to develop by collaborating with TIER1’s on products like middleware products/digital cockpits/Autosar extensions etc. currently there are no takers for these but there is an optionality opportunity here at the same time it’s really very hard to penetrate automotive value chain especially with clout that TIER1’s enjoys. So here Zero margins/loss currently. There is some IP here .

- Trying to expand its services into other domains as well, for example in semiconductor industry and energy industry. They are trying to pitch for the chip company Qualcom but are not yet successful. There is another optionality here. Again, zero IP. no sales/no margin currently here yet. As you can see the TAM is huge in each segment that KPIT operates

Things I’m looking forward to as an investor:

-

The company must expand into other verticals because both the current verticals have very limited TAM, I know this being an industry person but if you still looking for confirmation from the management here it is

-

Getting into wire harness and plastic molding tools etc is fine they bring the revenues, but they can’t put the co on par with other E&RD service companies’ capabilities.

-

You just can’t get into the embedded electronics or other tech verticals with this existing team you need different set of leadership and sales team at different scale levels of the company. That’s what differentiates a $20million company and a $400 million or $1 billion service company.

-

It’s just their first concall so need to wait how they sound in subsequent concalls

48 Likes

Superb Analysis. Really drills down into why concalls or company presentations don’t really give the right picture and we as investors need to do our own research.

3 Likes

Thanks to you and @Pradeep_Chitluri for the detailed posts and giving us an industry perspective! I have a question to you/Pradeep regarding your observation on limited TAM for both businesses. While management acknowledged that BIW MES would start hitting a ceiling beyond 15mn $ of topline, management was quite confident that civil engineering services outsourcing had a large TAM and a long runway. My questions are:

-

Is civil engineering services outsourcing from USA to countries like India/Mexico/Romania/Indonesia a new trend or has it existed for a long time? If its new and growing, then what is driving it? Have Indian firms levelled up in terms of delivery quality to now get a share of the pie? Management seemed to indicate Romanian/Filipino/Indonesian firms have been in this space before India but India has a cost advantage over these countries.

-

As per management, they are the largest listed player in civil engineering services and while there are 5-6 detailing players in the unlisted space, only one of them is as big as MoldTek. Can you throw some light on their competitors in this space - both Indian and Romanian/Indonesian/Mexican if any? Such few competitors being present could either mean the pie is small or MoldTek is early. Which one is it?

12 Likes

Sales growth continued, but profitability declined. Shares got hit hard.

Net Sales at Rs 165.46 crore in December 2023 up 6.86% from Rs. 154.83 crore in December 2022.

Quarterly Net Profit at Rs. 14.20 crore in December 2023 down 12.97% from Rs. 16.31 crore in December 2022.

1 Like

Mold Tek Technologies Q3FY24 – Concall

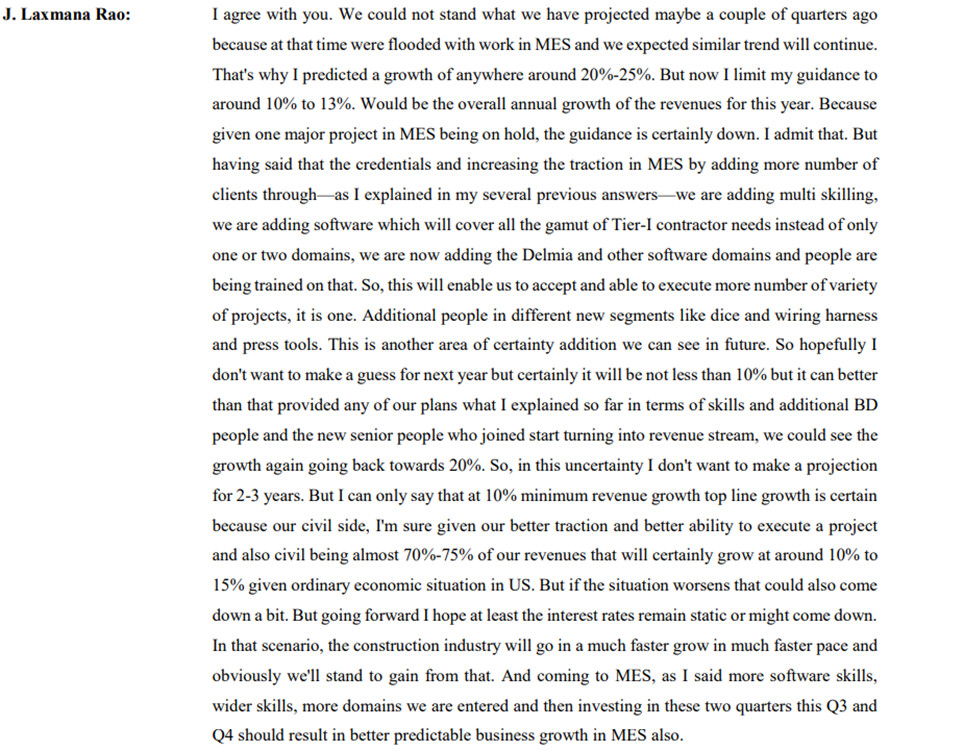

Why Growth was constant?

First two quarters there was a very good rush of projects and revenues by almost 60% this quarter also the number was stagnant. But growth has again stopped because one major project a US based project and the labor issues in US also has delayed the project implementation and they in turn delayed the project execution at MoldTek end.

That has resulted in again MES becoming flattish in this quarter which has grown rapidly in the previous 3rd Quarter. So that is one of the main reasons for our flat performance in this quarter.

As per the last call with the company they have updated last quarter that from February end they will be again starting up.

How growth can come?

However, the positive sign is we have added resources in fields of three segments which will be under marketing efforts now

A major project from one of the leading automobile companies in USA executed by a Mexican Tier-I contractor will open up in the middle of the second half of February and then the work may start from March.

The best and the worst part about Mold Tek Projects – They are full with projects but not

EBITDA Guidance

Maintaining an EBITDA margin in the region of 28 to 30 is possible going forward because this kind of uncertainty in MES will not be there in the next year as they are adding at least two to three new segments but the revenue growth will be from the Q1 itself.

Revenue Guidance

7% to 8% growth in the civil structural detailing, going forward the civil can improve at 7% into at least 12% to 15% next year given the traction now.

The next year onwards aiming at least 20% to 25% topline growth.

Company is expecting the new team could lead the revenue to 20% plus but still only confirm about 70-75% of business growth will be atleast 10-15% onwards.

While they are doubling sales team which will be able to make better utilization of the resources with the established credentials.

Now they are increasing by adding more number of clients.

Q3 could be the worst substantial cost and can be taken as benchmark for underutilization.

Other factors to consider

Hired 173 people with 45 lakhs payroll per month increased the cost and even 12-15 Senior level officers around 1.5 lakhs per month too, even new software led to increase in the depreciation and amortization cost too.

They are also going hard on M&A

For an investor questioning about previous guidance of 20% odd growth, the answer was their over expectation set them up wrong because of the flooded projects in H1FY24, which has gone down now and management is openly admitting that and now guiding around 10-15% growth.

Pardon me if there are any mistakes occurred by me while preparing this

Thanks,

Akash

7 Likes

Thanks for the jist.

Their repeated underperformance just reminded me how not to get fooled by “1st time concall” and “big guidance”. After Q1 they told Q2,Q3,Q4 would be much better subsequently because the invoice of the projects gets into account at the latter Qs of FY. High promises on topline and Ebitda margin.

After Q2 they said Q3,Q4 would do better.

Now the goal post keeps shifting and excuses of market condition, some other player taking their market share keep coming. Those might be genuine reasons but then why show overconfidence in concalls!

Disc: Invested

6 Likes

Mold – Tek technologies – Mann Ashar – March 9, 2024

- Started by J. Lakshman Rao of Mold – Tek Group

- Mold – Tek packaging known for Asian paint’s Bucket is a demerged entity from Mol – Tek Tech

Let’s Understand What Mold Tek Does

Mold Tek Tech is a pure play proxy to US infra space with asset light business

Let’s Dig deep into it

So, Let’s get 1 thing clear that for US unlike our Indian way of building Sky scrapper or any piece of residential or commercial Infra through bricks and cement is not known they prefer more of Steel fabricated buildings due to low weight to build ratio – Basically how much weight to add on for every floor addition in tower – Marginal Increase in weight and cost is lower for high stories

Let’s Understand the value chain for the preparation of the above structure

- Steel Fabricator – the person who provides the steel for the Structure giving the precise cutting of length and breadth of which steel part to cut and which is to be built

- Steel Erector – the steel parts received are Assembled into a building stated above

- Mold Tek Type Consulting Companies – So how will a fabricator know how much roads and much steel to provide for in what shape and dimensions to be cut into? And for Erector how will he know which pieces fit together since usne thodi na specification diya he?

- Here comes Mold tek Type companies who has 2 things to do

- Provide information to Fabricator on steel req. through detailed drawing and exact minute detail of which part will be required

- Provide detailed Drawing of where each part will fit into the building

While other 2 are asset heavy AF Mold tek is completely asset light model

The fact of matter is that they started this business around 2010 and as per concall they require 8-10 years if gestation period to establish themselves as a good comp.

Considering that as per them that period for mold tek has been achieved around 2 years back

While the steel Detailing doesn’t have any specific industry size as per Mold tek the cost of the same is around 3 – 5% of total Construction cost of building

Considering the above a person will not fuck up his $ 1m Construction sight just because the person offered detailing of $ 30k against $ 40k of the whole project

75% to 80% of the detailing work is still done within USA at a higher prices because when a fabricator is using the detailing services, he would be definitely interested to save cost, but he will not forego quality and reliability at the cost of that savings. So, still majority of the work is done in US

Typically, project flow starts towards the end of the first quarter of US, that is Jan-March ending. All the new projects are generally initiated at this stage and they start picking up pace from April onwards and by second quarter, that is July to, till Jan or even up to March, there will be progressive delivery and progressive invoicing in our company. So, that’s why the Q1 tend to be the starting of the busy season, but Q2 to Q4 in our Indian FY, the invoicing improves and the numbers also sell

Management is looking for acquisition in Civil side but waiting for right opportunity for the same

Company Has been able to successfully execute Amazon warehouse or 64 storied building in Chicago and World Trade Centre when it was rebuilt, we did a part of the detailing and connection design work. So, that way we have established ourselves.

The company mainly is in the starting phase of the Steel structure’s construction

Generally in this business since it’s a back end Job (Simulations) there is no site visits but their office in Atlanta has direct connections with contractors and Project managers to cater to their needs

For each job in Fixed charge segment they Charge 3,000 – 3,500 $ per head per person utilisation of the same can be checked by their clients

The EBITDA margins are more than 50% in such segment à the share of such business right now is 10 % they intend to increase the same to 15 – 20%

Operating leverage in the business – company hires trainee engineers and the same are then put into training for the Job since a minute mistake can cost the client 1000s of $ hence for 6 – 9 Months you expect 0% output or utilisation, and for 1 year you can expect 20 – 30% Utilisation

You need a back dated hiring in the business – Meaning if you want to execute a project 1 year down the line you need to hire staff today for 100% utilisation

Look below for example

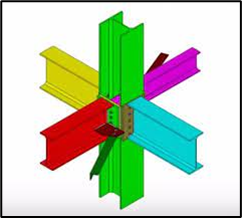

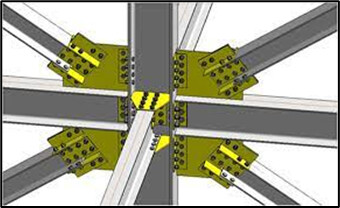

Connection Designing

These various steel members are interconnected using Rivets, Bolts, and Welding. This is known as a connection. Connections can be of various types, based on different criteria. Based on the method of fastening, the connections are of three types-Rivets, Bolts, and Welding.

So Connection design is basically into architectural side of business with bit of steel detailing, Through a proper acquisition of a firm in architectural cum structural designing company they will be directly be dealing with general contractors and take end to end responsibility of the project design, project architectures and even detailing, 3D and 2D detailing. Currently, they are only in 2D and 3D and little bit of connection design, but our connection design is now well established.

They have professional engineer in all that has the stamping design for almost each state in US

Reason for acquisition is – if they were to go on their own it’ll take another 8 – 10 Years like steel detailing to establish themselves as a player in this market à With acquisition they are looking for the promoters who will likely stay with them for another 5 – 6 years helping them to grow

So Steel Designing or Detailing Is very low value adding service or basically a commodity à but Connection designing is high value business basically a high end detailing

Connection design means how do you connect the members. The member design itself is high-end and that member design cannot be outsourced unless there is a PE stamping the drawings calculations

Stamping means the production engineer certified by the Board of American Structural Society or whatever it is. They are only, like, say, your Chartered Accountants here in India or our so-called structure licensed engineers who need to stamp the drawings for a municipality or a city corporation

Civil Engineers have to give exam every year in order to have the authority to sign the stamp

In detailing their main focus is fabricator right now, but with Connection design they intend to deal with architects and structural engineers who deals on behalf of general contractors.

The revenue per hour is double of that of normal detailing à from 25 – 30$ per hour to almost 60$ - 100$ per hour à Such business is around 3% - 4% right now only

- In US firms charge 120 – 150$ per hour in such scenario for the same credential it’s better to pay Indian firm $ 60 - $ 100 per hour

- Potential à maybe 10 times or 100 times in the next few years, but it all takes a proper way to approach the market, gain the conference of the architects and sectoral engineering, I mean, general contractors through a proper execution of variety of projects or through an acquisition.

overall cost of architectural and designing will be typically 4% to 5% including detailing, architectural structural detailing itself would be more than 2% to 3% while detailing maybe around 2% because of the value addition the quantum of hours that you spend in architectural and structural design are much less where your hourly rates are more than double

However this also adds the Risk if they acquire a company – If during restamping the misconduct is found they will face the legal consequences à however professional insurance covers the monetary risk, reputation risk might be something to look out for

Mechanical Side

BIW (Body in White) Fixture Design refers to the process of designing fixtures used in the manufacturing of automobile bodies, particularly in the initial assembly stages known as the Body in White stage. The Body in White stage involves assembling the metal components of a vehicle’s body before painting and other finishing processes.

Fixtures are specialized tools or devices used to hold and position individual parts or components during the assembly process. In the context of BIW fixture design, these fixtures are specifically designed to accurately position and secure various body panels, frame components, and other metal parts of a vehicle’s body as they are welded or joined together.

Basically BIW Fixture is the tool which holds the car roof in particular way such that various assembly function happens on the same

Every OEM requires the BIW Fixture designs in every root of the way

What mold tek does is it prepares the design for the same after proper consulting on site with the client regarding their needs

I think KPIT and Tata tech provides this service

Mold tek has been the supplier to tesla in their BIW designing needs

work on hand for MES has shot up from 200k last year to 1.1 million, s four to four-and-a-half times, and we anticipate the accumulative increase in the project flow in MES because we also entered into Press Tools designing and drafting services and the pilot projects are going on with couple of clients, and hopefully in few quarters, that will emerge as another new segment of business and revenues. So, that is how the MES is shaping up

The company started as pure play 2D design company now they are into robotics, 2D, 3D and even simulations

Let’s Look at anti thesis –

The company is owned by renowned J. Lakshmana Rao Sir who is promoter of mold tek Packaging

Having a business endeavour that is already well-established gives one question does he still have a hunger in himself to build another giant company?

The company is highly linked to US economy which I don’t like very much since there’s a fragile nature of US based private owned business( if anyone who is following private deals in US knows what I’m Talking about)

Recent Concall Takeaway – Q3

Civil Business’s revenue remains flat to slightly positive

They have ventured in 2 – 3 new business division in MES à Wire harnessing, Press tools dice, and SPM à no mention but In my opinion the same will be in regards to design and simulation only

have added resources in fields of three segments which will be under marketing efforts now

business development managers are being recruited not only in India, but also shortlisted a couple of Americans in USA who will be coming on board very soon

leading automobile companies in USA executed by a Mexican Tier-I contractor for the robotic simulation, supply of robotics and simulation. So that project has gone into hold during the last weeks of November December and just now they are talking about reopening it. à This had lead to slower growth

173 new trainees this year which is the highest in last 10 years

RFQ stage we have reached for some of these new segments. But the revenue addition I won’t see happening immediately, at least from April quarter onwards

we are doubling our sales team from 5-6 to around 10 now. All are qualified with experience in MES, mainly MES and a little bit in civil and that impact also will be coming from Q1 onwards, I hope

So now we have decided to go with little established names in M&A and we are now in talks with a couple of them

structural designing side, that will be at a very high cost, somewhere around $50 to $80 per hour even for offshore resources. And that kind of business will also give us direct contact with the general contractors, GCs and architectural firms

Annual people you can easily calculate even at the entry level cost of around 25,000 almost 45 lakhs per month is the additional cost

we have taken at least 12 to 15 seniors whose cost will be something around 1.5 lakhs per month, with experience in different fields. So about 8 to 12 people I think we have taken. So that is another additional cost of about 15 lakhs per month

BD will be 1 or 2 of them joined and other 3 people are ready to join most probably from March.

Attaching SS of J. Laxman Rao sir since, there is no better way I could summarie the same myself better than him

There was a Guidance draw down or Mis understanding in Concall Where management guided 25 – 30% of Growth in CES and then went to 10% excluding acquisition that caused the share price to drop from high of 390 – 399 to 200 currently and still some people bashing on Twitter to management

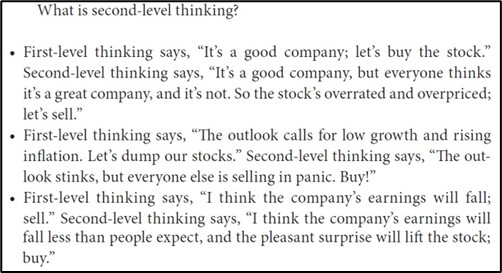

My thesis follows around Howard Mark’s second level Thinking

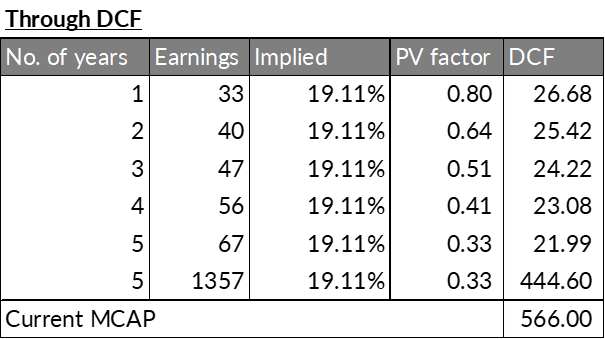

See the below valuation analysis

If the company is able to undergo the acquisition for the company to pay 25% p.a. Return the company would have to grow it’s earnings at 19%

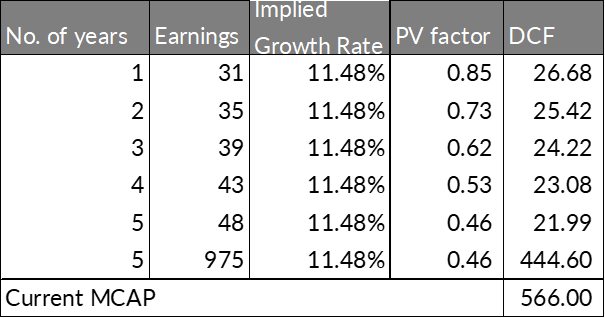

Which sounds hard may be doable? So if we notch down the hurdle rate to 17.5%

Implied growth rate comes to 11% which is definitely doable

The company which grew its top line at 16% p.a. in initial stage of business in last 10 years in raging bull market is trading at 17x, 1 Year forward will be less than 15x, Being impatient I have avoided the same in my personal PF but added the same in my family PF where past average holding period is more than 5 Years giving me immense time to hold business → My Personal PF churn is significantly high where as Family PF There has been 1 Exit in last 1.5 Years

I believe for business of this niche, the value will emerge and funny thing is the company was everybody’s darling 8 months Back, and now after 50% Draw down nobody is giving a damn, LOL.!!!

IMHO the business will continue to underperform at least until Completion of H1 25 Due to high operating leverage on Negative side if they find suitable candidate for merger or aquistion they could fly early

One thing I’m not understanding is why management so fixated on Civil business when there is enough tailwinds with multiple business engines as someone stated above regarding KPIT and Tata tech having high TAM where are Niche of this company is basically substituting business where they under cut the prices competition is something i have to understand still (from emerging countries of course or else where will you hire a Engineer for 300 Dollars per month)

Disclaimer – Very Minute position in Family PF and Will Inch up

Not a buy or sale Recommendation

18 Likes

Actually the owner being Mr J. Lakshmana Rao boosted my confidence in this company and was a major factor in buying this as my thought process is, if he built plastics to what it is today at an impressive growth, he can do the same for this, and till now YoY it has proven right. Their reviews online by employees is rather poor and is an issue to consider.

2 Likes

Very opposite view here

- the management/BOD is completely family owned

- the salaries/perks are around 12-15% of bottom line given back to family only

- the unfair compensation policy where 4 cr of salaries of Promoters from Mold tek packaging and technology

The share will be at the discretion of management.!!! - the management themselves stated that apart from his son in law they spend less than 2 -5 days a month in Technology

Then why more than 70% of overall compensation withdrawn from technology business? Isnt that prudent to withdraw on basis of time spent in business

Hence ethically major remunaration from plastic business

For management it doesn’t make any difference but for us it makes difference since every shreholder in tech isnt the shareholder in packaging

- some of the concerns are common for business where one entity has been being big

Hence my above concern–> does the management have what it takes to build anothe gaint?

It doesnt only mean in terms of revenue or profits

It also means in terms of high corporate governence practice

Make the board independent if you cant find way to be non partial towards both business

Or be competant and consider minority shareholders as well

Hence i have bought but not upto certain level generally i buy around 10% of total pf as starting position if i find idea to be convincing enough

But there are many puzzles here, will see how it pans out, have invested but total position around 6% of total PF

Than will think Weather to inch up or not

6 Likes

https://twitter.com/Mann_ashar/status/1785604845053034917?t=KC7rE1jvbeeLEQcFe5jS3A&s=19

My take on Result as on March 31, 2024.

Much on expected line.

Track the developments in SPM, Wire harness and something about telecommunication infrastructures.

Disclaimer - Invested with 4-5% of weight in my PF

1 Like

Is the outlook positive post US elections along with the rate cuts? If anyone attended AGM please share the management commentary on the same.

MoldTek Tech & Interarch Join Forces for Global Expansion!

MoldTek Technologies (MTTL) partners with Interarch to target global markets, earning a 5% commission on export orders. Initial plan spans 2 years, extendable by mutual agreement.

![]() Key Highlights:

Key Highlights:

- MTTL & Interarch sign MOU to focus on export orders.

- MTTL provides engineering design; Interarch handles manufacturing & shipping for PEMB & structural steel projects.

- 5% commission for MTTL on export orders, with possible project-based adjustments.

- MTTL’s Atlanta office to support Interarch’s international marketing.

3 Likes