MOIL has been posting some really good production numbers for the past 2 months. Any idea what is happening? From where is the production ramp up happening and is this sustainable?

OT, this made me laugh for the explanation given. Rules are rules, people. from the latest concall transcript

1 Like

Oh you should see the video of that investor meet, some of us sitting there could simply not stop laughing.

MOIL Limited, a government enterprise, reported a 35% year-on-year increase in manganese ore production in November 2023. The company has also achieved a remarkable growth of 43% year-on-year in the current fiscal year, with production of 10.9 lakh tonnes of manganese ore from April to November 2023. Sales growth for November and April to November 2023 was 18% and 52% respectively. The company has been focusing on exploration, with a significant increase in core drilling activities. The CEO expressed confidence in sustaining the high performance levels.

1 Like

I am surprised by lack of discussions in this counter on the recent market developments.

South32’s Groote Eylandt Company (Gemco) has been suspended because of a tropical cyclone - till Jan-March 2025. Gemco contributed 3.5-million wet metric tonnes - or c. 10% of world production.

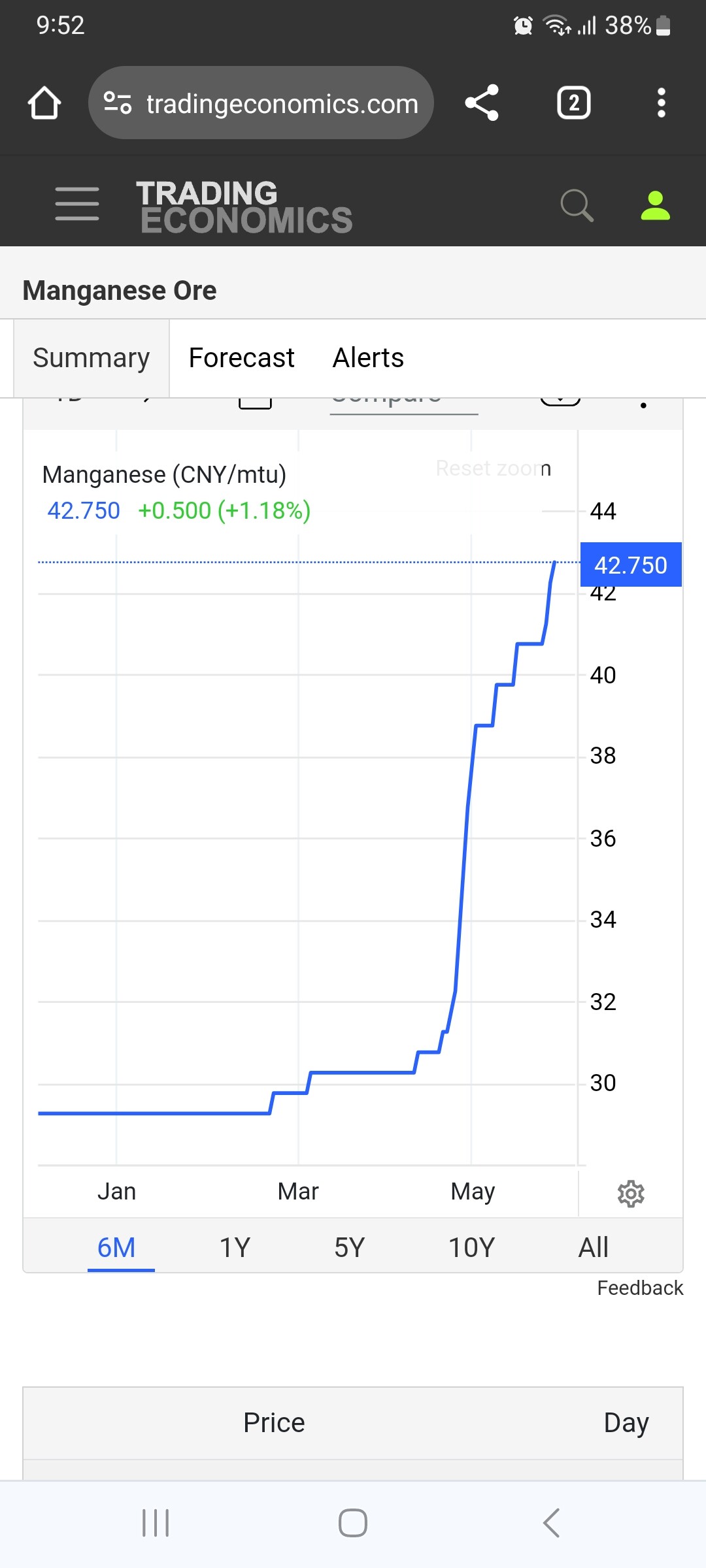

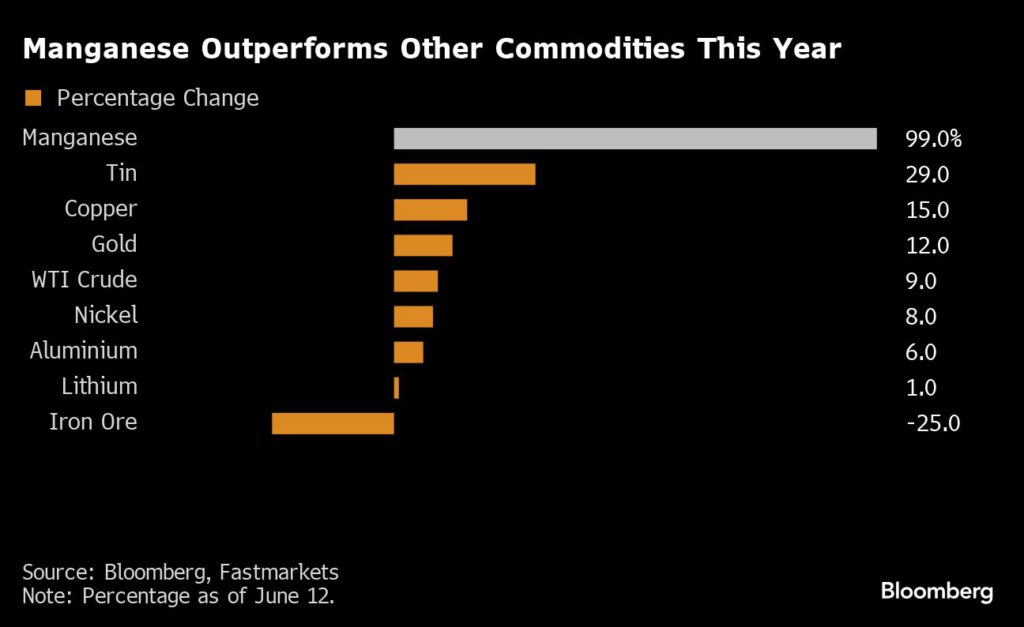

This loss in production caused the global Manganese ore prices to shoot up, with MOIL increasing prices by 25 to 40%. Moil shares rise 10% after 40% hike in manganese, ferro grade ore prices (upstox.com)

Manganese ore index, 37% Mn, cif Tianjin, $/dmtu (fastmarkets.com)

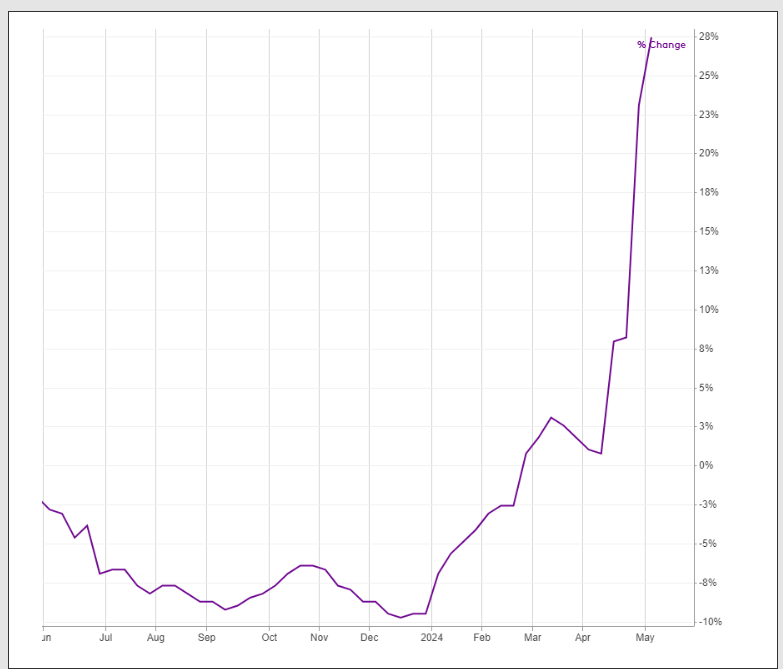

The stock reacted positively over the last month and is already up more than 50% - but with operating leverage, I expect profits to increase multifold.

Happy to hear thoughts/counterthoughts on this thesis.

Disc: Invested, c.5% of my portfolio. This is not an investment advice.

4 Likes

Moil rises prices by another 30%-35%.

The international prices are still rising strong due to reduced inventory in ports.

1 Like

MOIL -

Notes from Annual Report 2024-25 -

Company’s Infra -

India’s largest producer of Manganese. Their operations span over 11 mines in Maharashtra and MP. Company supplies aprox half of country’s Manganese requirements

Company’s Ferro Manganese plant is located at Balaghat in MP (12000 MTPA capacity)

Their Electrolytic Manganese Dioxide Plant is located at Dongri Buzurg Mine in Maharashtra (1500 MTPA capacity) - only EMD plant in India

Their renewable energy infra stands at - Wind mills - 20 MW, Solar plants - 10.5 MW. More than 56% of their energy consumption is through renewable energy

Company is debt free

7 of their mines are located in North East Maharastra ( bordering MP ). Another 4 mines are located @ South East MP ( bordering Maharastra )

FY 25 Financial outcomes -

Revenues - 1584 cr, up 9.35 pc

EBITDA - 638 cr, up 20 pc ( margins @ 37 vs 34 pc )

PAT - 381 cr, up 30 pc

Q1 in FY 25 was exceptionally good because of very high Manganese prices due to unscheduled mine closures in South America

Company aspires to achieve an annual production of 3.5 MMT by 2030. Company was granted an additional Environmental clearance capacity of 1.9 lakh MTPA taking their total EC backed capacity to 2.67 MMTPA

India aims to be producing 300 million MT of steel by 2030. 11 million MT of Manganese will be required to achieve this target. MOIL intends to be supplying 3.5 million Mts out of this total requirement of 11 million MT

Capex spends in FY 25 stood @ 321 cr. Capex projection for FY 26 stands @ 325 cr

Company continues to expand their resource base through strategic partnerships and new drilling initiatives. In Gujarat, a joint venture is in process with GMDC in the Pani area, where resource estimation indicates strong mining potential. In Madhya Pradesh, extensive exploration in Balaghat and Chhindwara has identified two viable blocks. Detailed feasibility studies are underway to further enhance their value-accretive strength

Estimated Manganese ore @ Pain Block in Gujarat stands @ 9.51 MMT

Area resered in MP for company’s exploration stands @ 1337 Sq Km

In FY 25, company added 16 MMTs of Manganese to its reserves via normal exploratory activities that the company undertakes. In FY 25, company undertook exploratory drilling of 1.07 lakh meters

Out of company’s 10 mines, 3 are open cast and 7 are underground mines

In FY 25, company produced aprox 1.8 million MT of Manganese

Company is open to exploring any mineral in any geography, provided it makes economic sense. Manganese mining has given the company an expertise in both open cast and UG mining. So, they can literally indulge in mining any other mineral as well

As the company keeps ramping up its production output by 12-14 pc CAGR for next 4-5 yrs, the cost of production at the corporate level should fall by 5-7 pc / yr ( as a lot of fixed costs won’t go up in the same proportion ) - an important factor likely to drive future margins / over and above the global Manganese prices

Company achieved best ever production of Ferro manganese and Electrolytic Manganese dioxide @ 12000 MT and 1350 MT in FY 25

Company aspires to produce 2.05 MMT of Manganese in FY 26 ( basically a 15 pc growth over FY 25 ). In Q1 FY 26, company produced 5.02 lakh MMTs ( highest Qtly output ). Company also hiked the prices of Manganese alloys by 2 pc in Q1

Company aspires to keep producing incrementally higher quantities of Electrolytic Manganese Dioxide and higher grades of Manganese metal - in order to improve their realisations

Company’s H1 FY 26 outcomes -

Revenues - 696 vs 785 cr ( Q1 in last FY was exceptionally good due to some mine closures in South America )

EBITDA - 179 vs 293 cr

PAT - 122 vs 202 cr

Company’s production till Nov 25 has reached 12.69 lakh MTs ( up 8 pc YoY vs Mar - Nov 24 period )

Disc: not holding, studying, not SEBI registered, not a buy/sell recommendation

3 Likes