Company Overview Modern Insulators Limited (MIL), established in 1982 in technical collaboration with Siemens AG, Germany, is India’s largest manufacturer and exporter of porcelain insulators. The company operates primarily in the high-voltage electrical equipment space, serving national and regional utilities, Indian Railways, global original equipment manufacturers (OEMs), and EPC contractors across more than 50 countries. The company’s long-standing technical pedigree is anchored by its initial joint-sector promotion alongside the Rajasthan State Industrial Corporation (RSICO) and technical partnership with Siemens AG. MIL features a highly reputed client base with low concentration risk, supplying major industry players such as the Tata Group, Siemens AG, and Hitachi Energy India Limited

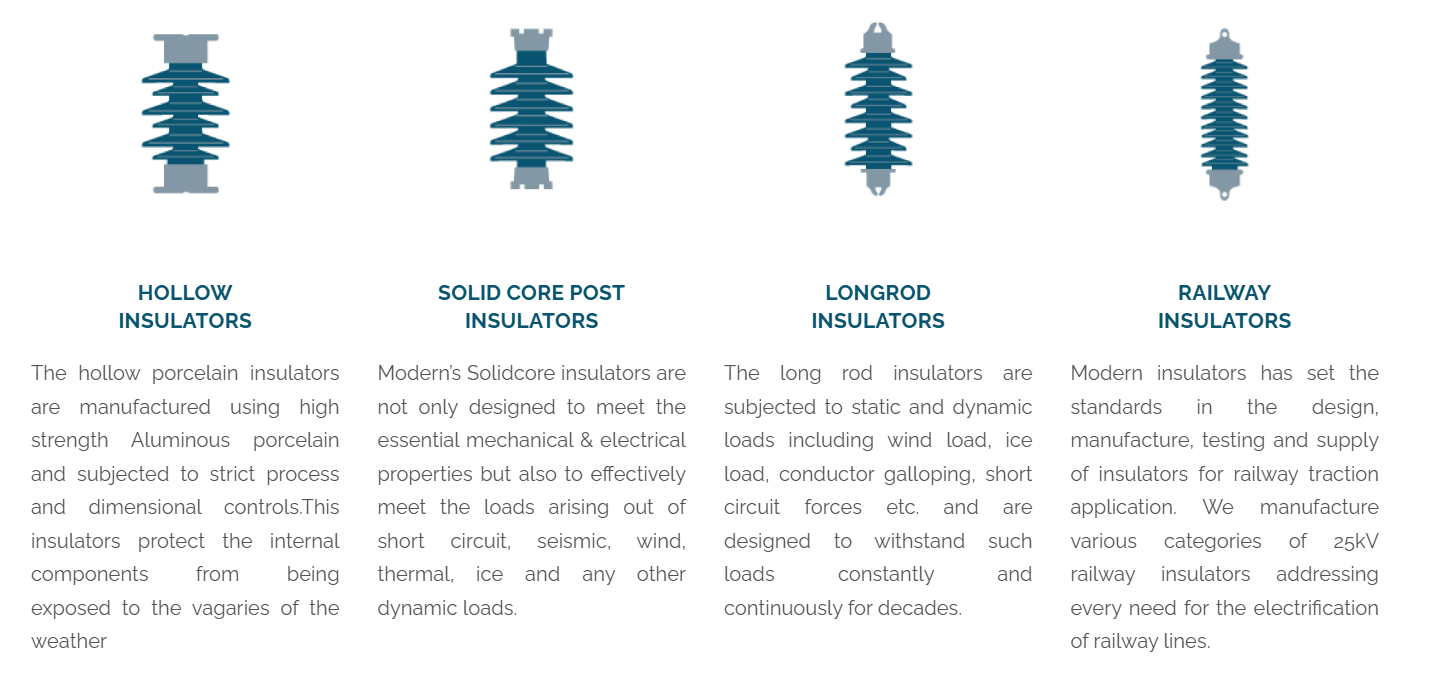

Business Segments The company operates through two primary segments. The Insulators Division forms the core business, generating approximately 89% of total revenue, and specializes in Extra High Voltage (EHV) porcelain insulators ranging from 132KV to 765KV, including solid core post, hollow, long rod, and railway insulators. The Terry Towels Division, based in Gujarat, accounts for approximately 11% of revenue and manufactures terry towel products, which has recently shown a turnaround from historical operating losses to achieve positive operating margins.

We were the first company to introduce porcelain Long rod insulators in India – a superior alternative to disc insulators with an unbeatable pollution performance. MIL also introduced an exclusive aluminous body for porcelain insulators- proven for its improved mechanical and electrical strength.

Modern Insulators’ manufacturing plant is situated in Abu Road, Rajasthan and has a currently installed capacity of 26,000 metric tonnes per annum and exports account to about 30% of its annual turnover.

Modern has the most sophisticated manufacturing plant with machinery imported from Germany along with the required testing and inspection facilities and an in-house R&D setup recognized by the Government of India for development of new products & process improvements.

From their site About Us – Modern Insulators Limited**

Key Corporate Developments** MIL is undergoing significant corporate restructuring. The company demerged its yarn division into a new entity, Modern Polytex Limited (MPL), with a record date of October 31, 2025, to function as a pure-play electrical equipment manufacturer. Additionally, MIL is pursuing a long-pending amalgamation with Modern Denim Limited (MDL), for which it has advanced unsecured loans of ₹57.6 crores to settle MDL’s institutional debts. On January 22, 2026, the National Company Law Tribunal (NCLT) disposed of the merger petition, granting MIL the liberty to re-approach after fulfilling specific procedural compliances.

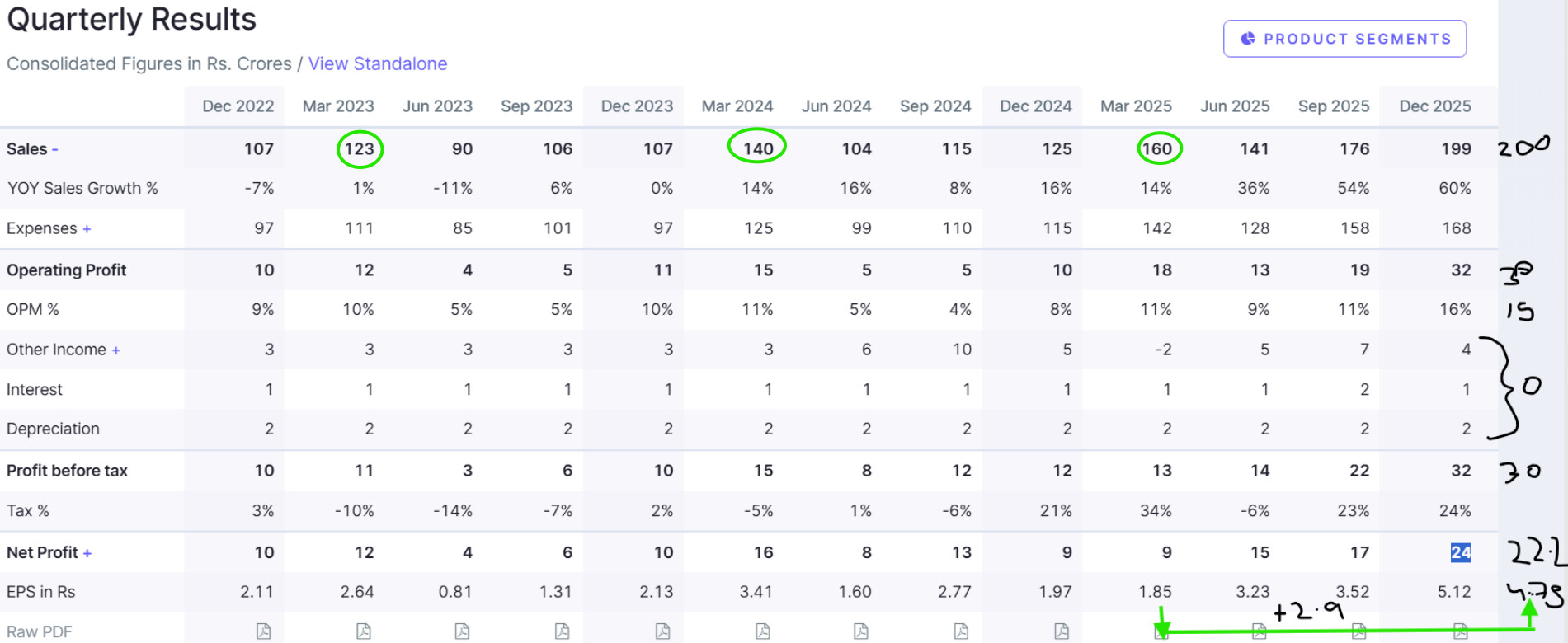

Financial & Operational Performance For the financial year ending March 2025, consolidated revenue from operations grew to ₹503.27 crores from ₹443.30 crores in FY24. Consolidated Profit After Tax (PAT) improved to ₹38.58 crores from ₹36.04 crores over the same period. While absolute EBITDA increased to ₹47.03 crores in FY25, the EBITDA margin experienced a slight contraction to 9.51% from 10.13% due to a higher cost of goods sold. However, recent Q3 FY26 results show exceptional momentum, with standalone revenue surging 60.1% year-over-year to ₹199.46 crores and EBITDA margins expanding sharply to 17.78%. The company maintains a comfortable net leverage ratio of 0.43x.

Segment Highlights / Key Business Verticals The Insulators Division is the primary growth engine, achieving a turnover of ₹417.34 crores in FY25, up from ₹385.45 crores in FY24. This vertical benefits from strong export demand, with international sales reaching ₹192 crores, driven by approvals from overseas utilities and new orders for specialized products like RTV-coated porcelain long rod insulators. The Terry Towels Division also demonstrated growth, with revenue rising to ₹56.87 crores in FY25 from ₹46.25 crores in the previous year, achieving an operating margin of 2.8%.

Capacity Expansion & Capex Plans The company has an installed manufacturing capacity of 24,000 metric tonnes per annum (MTPA) for insulators in Rajasthan and 2,400 MTPA for terry towels in Gujarat. MIL does not plan to undertake any debt-funded capital expenditure on a standalone basis in the near-to-medium term. However, on a consolidated basis, its subsidiary, Modern Composites Private Limited, has availed a term loan of ₹7.65 crores to fund plant and machinery investments.

Order Book / Recent Orders / Contracts As of September 2024, MIL reported a robust short-term order book of ₹192.4 crores scheduled for immediate execution over the subsequent three months. The company has successfully secured frame contracts with European utilities and won significant orders from a major Gulf utility for RTV-coated insulators, highlighting its competitive positioning in international markets.

Growth Drivers & Future Outlook Management anticipates sustained revenue growth fueled by India’s transition to a power-surplus nation, extensive integration of renewable energy, and massive government capex in transmission infrastructure. Global grid modernization and the replacement of aging infrastructure act as strong tailwinds for the export business. The company expects EBITDA margins to improve in the medium term by shifting its product mix toward higher-value, high-margin EHV insulators and incorporating price escalation clauses in contracts to mitigate raw material volatility.

Subsidiaries & Strategic Initiatives MIL has established a wholly-owned subsidiary, Modern Composites Private Limited, to manufacture composite insulators, which reported an initial stage loss of ₹93.77 lakhs in FY25. To diversify into EPC contracting, the company formed several joint ventures, including Shriji Designs - MIL (JV) for railway EPC tenders, which successfully turned profitable in FY25 with a net profit of ₹31.92 lakhs. Additional JVs, such as SEC-MIL and Akhandlamani-MIL, have been formed to bid for power distribution and railway contracts, with MIL executing the projects and paying commission fees to partners.

Financial Position & Funding The company’s financial position is stable, characterized by adequate liquidity and strong cash generation. Operating cash flows improved to ₹45.6 crores in FY25, supported by favorable working capital changes. The standalone entity is virtually debt-free regarding term loans, and credit metrics remain comfortable with a gross interest coverage of 10.96x. The promoter group maintains a 60.18% holding with zero pledged shares.

Risks / Red Flags A primary red flag is the statutory auditor’s qualified opinion regarding the non-provisioning of taxation and interest liabilities. The company has not provisioned an estimated ₹19.15 crores for FY25 (cumulative ₹118.44 crores) in anticipation of tax benefits from the pending Modern Denim amalgamation. Furthermore, the business suffers from an inherently elongated net working capital cycle, peaking at around 199 to 210 days, primarily due to long inventory holding requirements for imported raw materials like clay. The extended delay in the amalgamation process with the loss-making Modern Denim Limited also remains a key rating constraint.

Management Commentary / Qualitative Insights Management projects a highly confident tone regarding the macro-environment, citing a “virtuous cycle” of domestic energy demand and international orders. They emphasize a strategic pivot towards high-end technological products, such as HVDC insulators and semi-conducting glazes, to protect market share against intense global competition. Despite regulatory delays, the board remains committed to executing the Modern Denim merger to unlock administrative synergies and tax breaks.