Yes, @shyamdsundar and @stockhunter, I am Leading_Nowhere on Twitter as well.

You can find the original post here: https://twitter.com/leading_nowhere/status/908585649501900800

Thank you for the credit @parkhi_nazar

Yes, @shyamdsundar and @stockhunter, I am Leading_Nowhere on Twitter as well.

You can find the original post here: https://twitter.com/leading_nowhere/status/908585649501900800

Thank you for the credit @parkhi_nazar

You should know that investors gave them an earful about guarantee commission on the last earnings call. Management has promised to look into it. Will be interesting to track how this moves. In any case, if you are considering an investment in Mirza, you should be aware that it is not a paragon of corporate governance. The bottom line is that those who are invested know this, but have taken the view that the company’s growth will provide enough for minority shareholders even after the promoters have chomped off a few bites. Corporate governance is a monitorable, but there are other monitorables that are far more critical for Mirza at this juncture

Discl: Invested from low levels

After having mulled the results, here are my thoughts.

Sales up a paltry 4% and profits down about 10%, OPM down to 16% from 18% makes it look bad optically but this needs to be broken down. My thesis for investing in Mirza is the focus on domestic business where the opportunity size is relatively large and the cheap valuation (which happens to be due to lack of growth and corp governance issues).

The domestic business revenues have grown at a whopping 40% YoY and 12% QoQ. This is a very good sign and shows that the new stores are contributing to the growth. However, profits for domestic business have grown only 11% YoY and 12% QoQ. Maybe the discounting is hurting the margins - Is it the discounting only or is it the upfront costs that have to be borne to open new stores? Or is it the ad spends in building the brand? In other words, is there scope for margin expansion is something we need to watch for.

Another reason for PAT being lower is the finance costs. So topline growing is the single biggest sign here that is very encouraging. Exports are also up QoQ which is also slightly encouraging. This is in line with exports figures for “Footwear of leather” to UK.

Markets do like to signs of improvement on a quarter on quarter basis but in this case I think we have to be patient to see if the investments being done to the brand (ad spends), stores presence, product quality etc which are all intangibles in the scheme of things contribute going forward. There is going to be a delay before these things show up a numbers (if at all) so for now I think we need to hear the management out and see what they are doing.

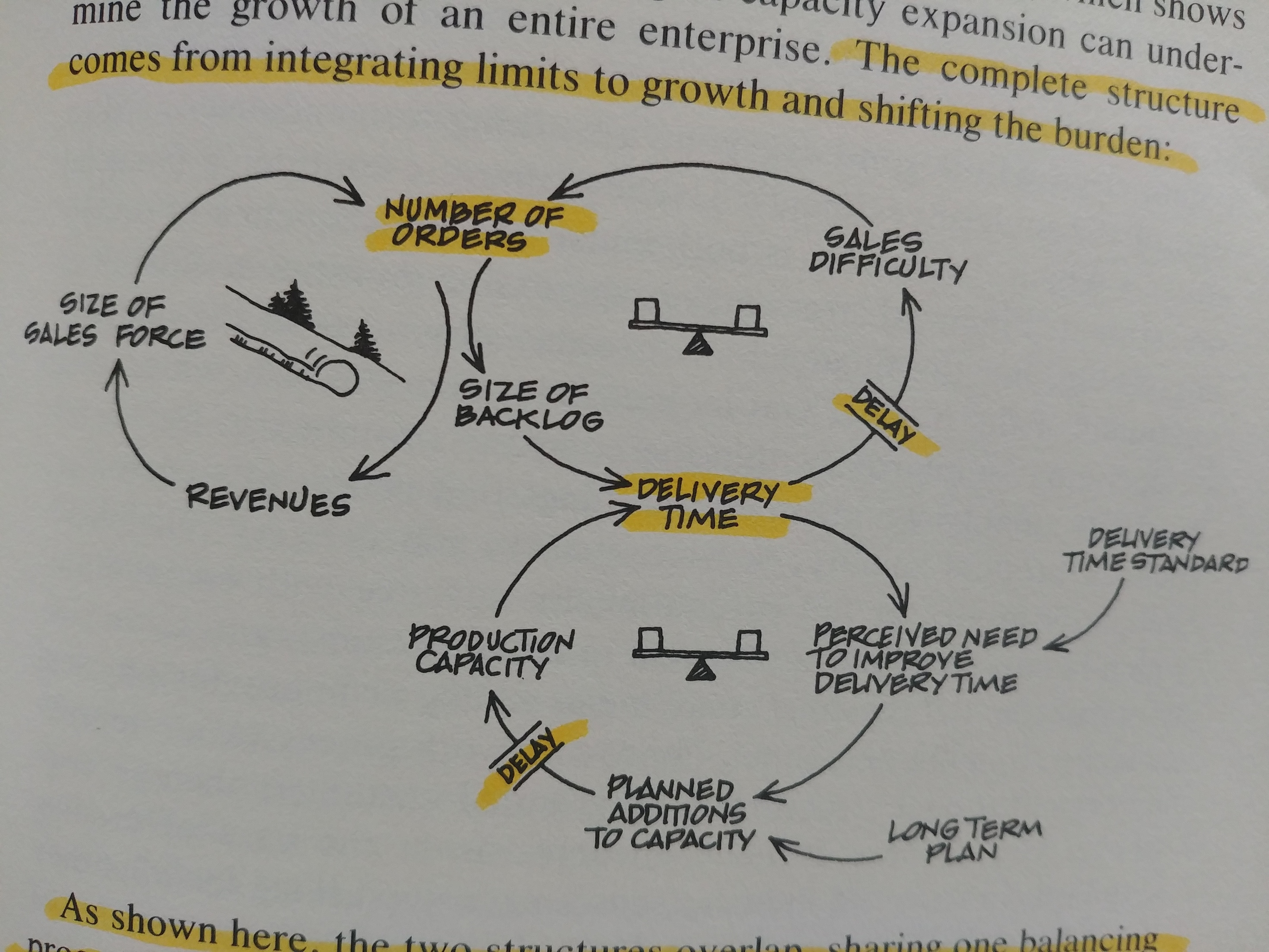

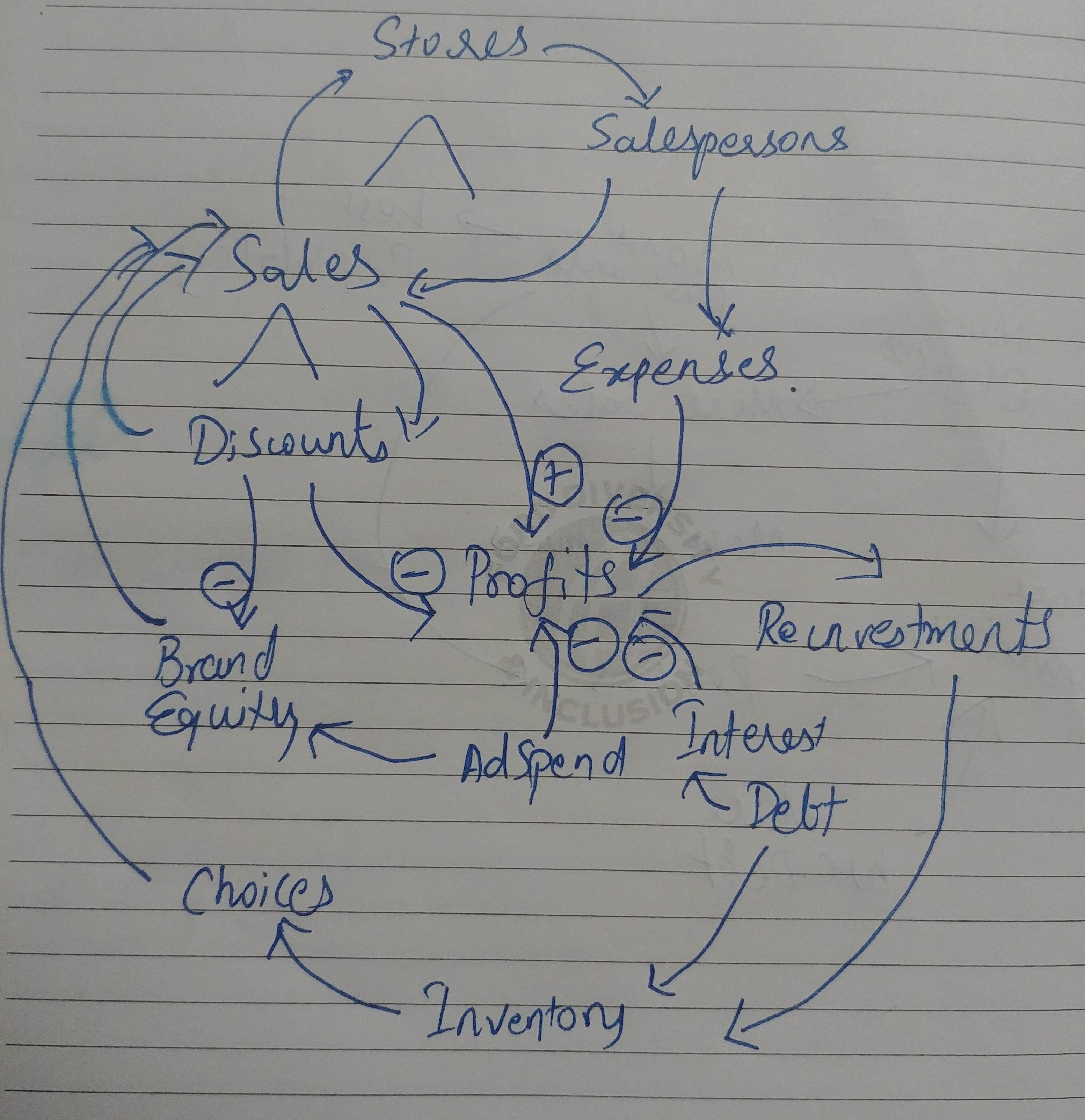

This reminds me of something I read in Peter Senge’s ‘The Fifth Discipline’.

In essence this system diagram represents the feedback loops representing a business for a company that was in the business of selling computers. The first loop on the left is a reinforcing loop - As in, as the size of sales force increases, orders increase and with it the revenues which means the sales force can be increased further thereby contributing to more orders - This is like a snowball effect - positive feedback loop in scientific terminology. Now as orders increase, delivery time increases if the capacity is not ramped which causes delays in delivery time - which means Customers are disgruntled but the company thinks that the customers are lining up for the products, so its OK to keep them waiting (short-term thinking).

As delivery time increases though, disgruntled customers don’t come back the next time and orders drop off after a delay. The company may think that their current capacity is enough to serve their orders and doesn’t invest in capacity or in maintaining inventory which leads to a balancing loop - orders don’t grow further than what the company can service. There are delays in this system which makes short-term effects lead to short-term thinking while the solution involves long-term thinking of improving capacity to cut down delivery times leading to happier customers who come back or spread the word - This deals with the balancing feedback loop and fixes the problem whose effects will show up only in the long-term.

I think something of this sort happens with every retail business that is out to build a brand - its a catch 22 situation - without stores, a brand, inventory, working capital intensiveness - the business will never take off and the investments will show their outcome with a delay and there is no way of knowing that outcome. I believe things could change in the medium term but we need to follow this carefully.

Disc: Invested

P.S Apologies for the long-winded systems thinking perspective. I wanted to add a systems diagram for Mirza but couldn’t due to lack of time.

Q1 FY19 Concall Notes

Regards

Harshit

Disclosure: Invested

Hi,

Any update regarding significant fall in profit from Leather segment-Rs. 40 lac against last year Rs. 300.75 lac even when leather segment sales has increased.

Hi @cool_gaurav,

The Leather Segment mentioned in the results pertains to the tannery division which is operating at low capacity utilization (55%) and is hence at break-even level. Going forward the company expects utilization to inch up to 60-65%.

Cheers!

To continue with the systems thinking perspective I had started in the previous post, this is how the causal loops look for Mirza.

There are several loops here - both reinforcing as well as balancing and this is what makes it a dynamic complexity problem. This is by no means an exhaustive model but just the entities that should carry a bulk of the freight.

Sales is positively influenced by discounts, brand equity and choices for the customer and also by having more stores/salespersons.

Discounts is low-hanging fruit that can influence sales in the short-term but in the long-term can have detrimental consequences. Discounts negatively impact brand equity and profits. Psychologically as well, returning customers expect more discounts than the last time.

Brand equity is the magic-potion for sustaining sales in the long-term. It needs more ad spend which positively influences brand equity.

Choices and product quality are paramount for the customer to be interested in the product and this means maintaining an exhaustive SKU and inventory - Something that short-term investors will frown at - as it impacts the WC debt and until the optimum inventory turns and consequently the capital turns are achieved, this is walking on thin ice.

Maintaining optimum inventory means reinvesting the profits in WC and also probably taking in more WC debt but interest on debt will impact profits and can cripple future expansion or even sustenance if the churn of the causal loops isn’t respected.

Reinvestments is not just in WC but also in stores (I have missed drawing the link). In the case of Mirza, investment in a store is primarily investment in the inventory for the store.

Profits is obviously positively influenced by sales but negatively influenced by discounts, expenses per store, ad spend and interest.

A company that masters these causal loops should think both in terms of the short (discounts) and the long-term (brand equity) at varied proportions as it matures. Probably starting with more discounts and then reinvesting the profits in growth - until market saturation (optimal number of stores) is reached and then focusing solely on the brand equity for sales sustenance and same store sales growth.

I presume Mirza has set out on this path and I am curious to see how things turn out more than anything else.

The story looks very enticing - local leather based footwear company trying to become pan national sports/athletic wear company and then having ambition to become global player (heard Mr. Shuja Mirza saying it on con call today). Few concerns as highlighted by many boarders-

First 2 can be considered part of strategy and can go either way based on how they execute. Third one is absolutely abhorred by the market. Responding to investor emails, regular conference calls and uploading transcripts are the steps in showing their investor friendliness. But unless Mirza’s let go their old ways of compensating themselves by various methods, it would be struggle for the stock price to move up as all the growth and its benefits may never reach the shareholders!

Disclosure - tracking position initiated.

Mirza International Ltd

Highlights of Q1 FY19 results

Key Highlights

MIL reported revenue of Rs 2.6bn, a growth of 3.9% yoy led by 40% yoy growth in branded shoes revenue and 17.6% yoy decline in revenue from make to order exports. Red Tape brand exports recovered strongly on a low base of last year.

On domestic side, domestic brand sales grew by 27% yoy which was on the lower side as the company has guided for 50% yoy growth in domestic brand sale in FY19E.

EBITDA margin declined by 100 bps yoy to 16.5% and was below our estimates on account of lower margins in the branded shoes business on yoy. In the quarter, the company witnessed increase in working capital which took its debt to Rs 3.1 bn (Vs Rs 2.7 bn at the end of Q4FY18).

MIL management has maintained guidance for 50% growth in revenue from domestic brand business based on strong response expected for Red Tape sports, Bond Street and other new brands. The company expects improvement in exports business (0-5% growth Vs 10% growth guided earlier), as it sees some sign of improvement in the segment.

Folks -

Last evening I visited a branch nearby ( or rather stumbled upon). Few interesting observations -

70% sale was on and the store was jam packed. Roughly 1000 Sq ft. in a good mall.

50% merchandise was apparels and most of the buyers were focused on those… Hardly any shoe buyer in half hour i spent

Quality to price equation seems good. I bought 2 shirts for 1100 INR - something that would cost me 5000 at Louise Phillipe

Good quality although packing and store front was poorly managed and high value customers won’t typically walk in

The store owner had franchise model with mirza and seems he had a good deal from them. As this store was earlier a Levi’s one… Now 50% branded for red tape.

Sales guy told me that business is good… Didn’t get numbers though.

The gentry of buyers seemed middle class, salaried type who would be drawn with a 70% discount tag.

In my assessment, what Mirza is trying is to give people a taste of their merchandise with hope that they would stick going forward given good quality at low prices. Key would therefore be to keep prices low while maintaining quality … Particularly in apparel, something that’s new to them.

Behind the Red Tape logo, the space was for Levi’s. The store owner said both brands are doing well although I felt he was evasive.

Thanks for sharing. Also try visiting their large format online stores…the apparels are available at a very good price and quality is good.

Need to see how these guys manage their inventory and if they can grow maintaining the current margins.

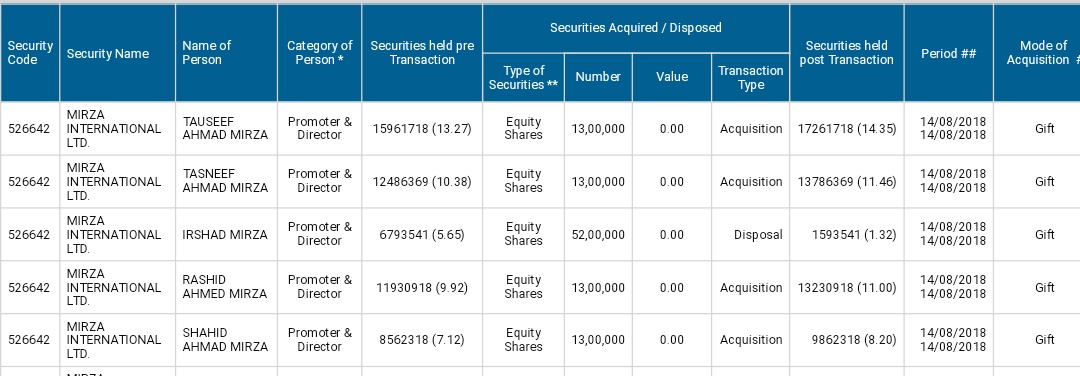

Mr Irshad Mirza one of the promotors has sold 52 lacs shares on 14 Aug 2018.

How many of the Mirza Stock buyers are using redtape and other brands of the company? Also, is the quality really better than others at same or lower price?

I visited the showroom of redtape in Inorbit mall, the sales rep of the shoes were talking more about the “Mirza” stock instead of the product quality and price.

I didnt buy the shoe and hence i wont buy the stock

Well I could tell you my case. I found the footwear and apparels and stocks worth the price, so bought all three in great quantity ![]() after I visited their newly opened store.

after I visited their newly opened store.

The products really have a good quality and comparable to some of the popular brands available 2-3-4 times their price.

But what I feel the real story is- solving mans purchasing problem. One hardly have stores where good quality branded shoes, chapals, t-shirts, jeans, semi-formals shirts/trousers available under one roof and available at good price. From where one can do bulk purchasing and still feel a winner in him.

Disc: Purchased stocks and products recently, hence my views could be biased.

Since this topic has come to discussion, I will narrate an incident that happened on last weekend.

I went to meet one of my cousin, who happened to show me his recent shoe purchase and was happy about the great deal that he got. We all absolutely loved the shoes. When I saw the pair of shoes, it was a Red Tape and I was amazed at the finish and quality of the shoes. I had never seen Red tape before. This was at par with Franco Leone, Louis Phillipe and Buckaroo shoes that I have used.

The use of material, stitching, smell of leather all were good. Yet it remains to be used and then look at the durability. Though there are others on the group who have used it for several years.

Also other details on the packaging (graphic sense) also made me feel that it was truly a world-class product.

Disclosure: Holding since last quarter.

{kind=link}