I am using red tape shoes and closing since 2012 and I am very much satisfied. At this price u would not get better product than this…

I am a frequent visitor to the central mall in Bangalore . I have noticed from last 3-4 month,in leather shoes section where all the leather shoe brands are available, most of the customers are trying out the red tape shoe. Earlier they had very small space allocated for red tape shoe with less variety . In my last visit i saw a huge number of red tape shoe was available ,but i saw a few number of sports shoes was available.

Below are some picture i have taken

Like this they had 2 to 3 stall with full of red tape shoe .I have used red tape leather shoe and quality and durability wise its really good. Their leather loafer shoes are really attractive and most of my friend wear loafer shoe with formal dress as well as casual dress .Even i have asked few customer who have brought shoe from red tape and their comment was also good .I am not sure about the quality of sports shoe.

4 Likes

P.S. This post is long and winding and is not directly related to Mirza but to systems thinking and dealing with dynamic complexity as with my previous two posts. Please ignore if that’s not your thing. Also apologies for these sort-of off-topic posts

Woke up today with the crux of the idea for this post. Was reading “deep simplicity” by john gribbin before I slept and some ideas from it I think were processed in my sleep  The basic concept of the book is that extremely complex systems with lot of dynamic variables sometimes can be expressed with pretty simple rules - The book starts with a Feynman quote about how all the complexity of the universe may someday be explained with the simplicity of something like the rules of checkers. This sounds outlandish but consider how we don’t know individual positions and momentum of molecules of air in a can but can measure the pressure and temperature of it. This is sort of what it boils down to - The mental model is in finding macro properties without bothering about the myriad micro properties of the system which are seemingly and overwhelmingly chaotic.

The basic concept of the book is that extremely complex systems with lot of dynamic variables sometimes can be expressed with pretty simple rules - The book starts with a Feynman quote about how all the complexity of the universe may someday be explained with the simplicity of something like the rules of checkers. This sounds outlandish but consider how we don’t know individual positions and momentum of molecules of air in a can but can measure the pressure and temperature of it. This is sort of what it boils down to - The mental model is in finding macro properties without bothering about the myriad micro properties of the system which are seemingly and overwhelmingly chaotic.

So in a complex system like the Solar system which is a N-body problem where every body in it exerts some form of gravitational force on another depending on its size - a bulk of the freight is carried by the mass of the sun and the gas giants jupiter and saturn, though every small piece of rock in the asteroid belt has a say on earth’s orbit for eg., albeit negligible. I liked the concept of the lorenz attractor and stable states and phase space as explained in the book. The idea is simple - While newtonian mechanics would claim that based on initial states, it should be possible to know the states of a simple system at later points of time (or even back in time), small changes/errors in the initial states could skew outputs drastically (sorta like DCF). These simple systems, like frictionless planes, don’t exist in a dynamically complex world - at least not in the heavenly body scale when it comes to gravitational forces, though they might in the human scale (explaining the apple falling).

The book then explains how one might prove that the solar system is “stable” - based on orbits which are valleys in the phase space. The same is true for electrons in an atom to a dripping tap - for very small inputs, the period of dripping varies but settles into dripping with shorter periods - stable states, just like orbits of planets or that of electrons around the nucleus.

So what then are the stable states for a company like Mirza with seemingly complex number of variables? Inverting, how does something like this run to the ground? Debt and inventory pile-up of course since they are in brutal retail - the equivalent of the planets falling into the sun. However, in terms of stable states - it can move into higher and higher orbits if things go well - i.e the dynamic variables of sales, inventory, conversion cycles, profits, reinvestments, new stores and sales fall into place. I feel stable companies like page do just this - they have moved into a higher orbit year after year. How does this concept explain cyclicals? Imagine a planet whose orbit expands and contracts - however this doesn’t cause the planet to spiral out of control into falling into its sun but instead the changing orbits is in itself a stable system.

Like an electron that absorbs a photon and moves into a higher-energy level, sometimes small changes in OPM or quality of product in a stable system can lead to the company moving to a higher orbit - think jubilant food after they changed the quality of pizzas early last year or bata india now. It is an exciting way to think. This is sort of what Buffett/Munger say as well in terms of complete idiots being able to run the company - At stable orbits, it takes a lot of energy to dethrone these companies from these stable states. So its no surprise that this book reco came from Munger. His concept of lollapalooza as well is derived from feedback loops of systems thinking. These books don’t directly add to investing knowledge but a strong systems thinking ability I think can help in investing.

18 Likes

Good for Mirza as this sneaker culture has huge scalability and longevity for a country like India esp when almost all those sneaker lovers aspiring to own a Nike or an Adidas but can’t afford one will settle for a budget sneaker. India will arguably have the biggest budget sneaker market in the world and Redtape’s positioning as a decent brand at an affordable price could serve them well if the growth shown in the last few quarters continues.

The concern on diluting brand power due to discount positioning is valid only if quality turns bad but so far the feedback has been quite good and if quality sustains so could the brand.

Rgds

RR

Disc: Token investment

Hi All,

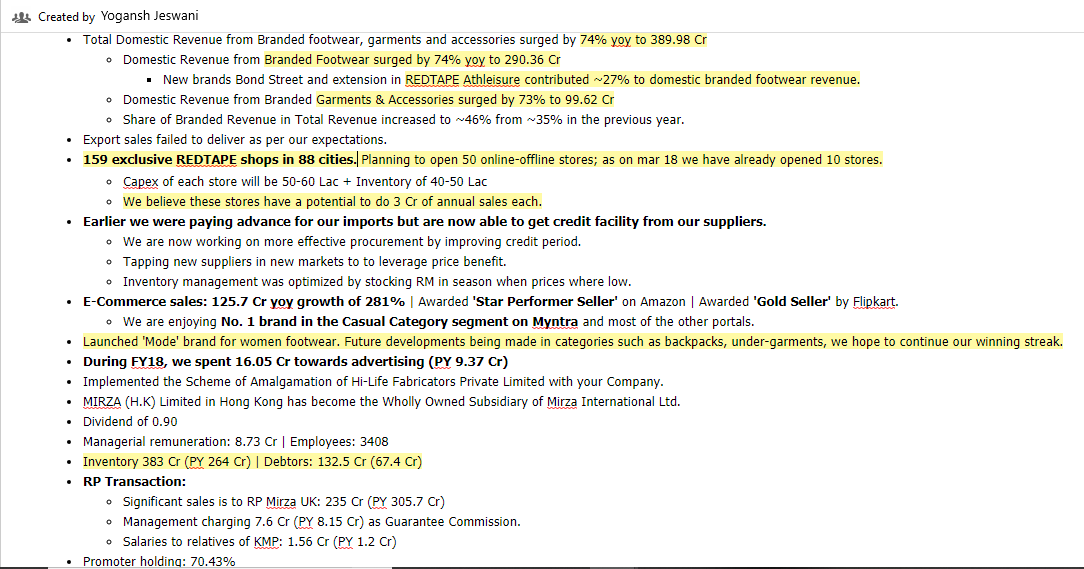

Sharing my notes from Mirza’s 2018 AR, please see below image.

Theme of the Annual report seems to be brand building. It talks a lot about consumer spending potential and company’s focus on growing branded business by reaching out to consumers through retail and online channels.

You can download the report from here.

Regards,

Yogansh Jeswani

Disclosure: Invested

6 Likes

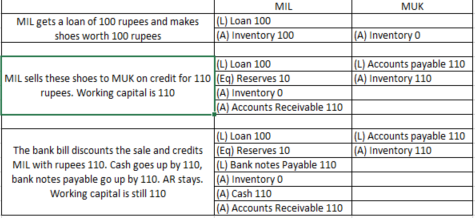

I learnt something new today on working capital management strategies analysing this company. Here is the deal.

Supposing we looked at the business in its totality, Mirza as a company will manufacture goods in India, export and sell them in the UK and recognise revenue when a sale is made. All unsold commodity is recognised in its books as inventory. Plain simple vanilla accounting.

However, in this case Mirza international limited (a listed company) exports to Mirza UK limited (privately held company, the directors of which are the promoters of MIL). Mirza UK limited has distribution rights of Red Tape in the UK and US. So in essence there is a supplier-customer relationship between MIL and Mirza UK limited. So when MIL makes a “sale” to Mirza UK, the transfer of goods is recognised as inventory on Mirza UK and as turnover on cash/credit basis on MIL.(this by itself is a bit difficult to get my heads around because this is only simply transfer of goods from one entity to another, there should be no revenue recognition. However, this is normal accounting.)

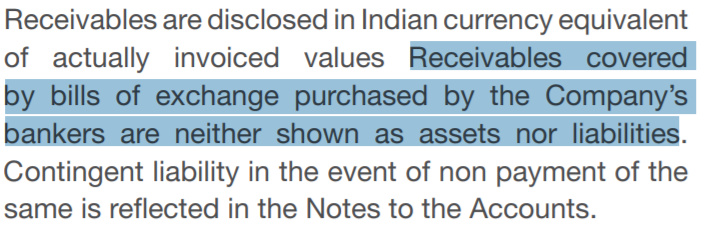

Now, here is where it gets interesting. MIL sells to Mirza UK on credit, takes the invoice along to the bank and asks the bank to “bill discount/invoice discount” it. Essentially stating, I have made a sale to a buyer and the buyer will pay me in some time. Can you, bank, loan me an amount slightly lesser than the invoice value and wait till the buyer repays you directly? The bank happily says yes(making it fully clear to MIL that should the buyer, Mirza UK, not pay up then the bank will come knocking on MIL’s door). So in essence, Mirza as a business has manufactured and sold to itself and gotten the bank to pay for it against the invoice.Why do this when they can get a simple working capital loan? Simply because Ind AS allows companies to account these bill discounts as contingent liabilities (off balance sheet).

Exhibit 1 - MIL’s trade receivables position for FY16, 17 and 18

That is 132 crores in FY18, 67 crores FY17 and 63 crores in FY16.

Exhibit 2 - Mirza UK’s trade payable position (March 2017)

That is £12.8M or about 120 crores in payables to MIL (against the 67 crores recognised above).

Exhibit 3 - This explains the difference and more.

This is entirely legal. However, every analysis on working capital/capital turns/inventory turns will be skewed (will be too optimistic).

P.S : Mirza UK’s filing history can be found here MIRZA (UK) LIMITED filing history - Find and update company information - GOV.UK

39 Likes

A very basic question (I have not analyzed Mirza International thoroughly so I may be missing out something).

Shouldn’t Mirza UK be a 100% subsidiary of Mirza International, the listed entity in India? Otherwise, it is very easy to skim and keep margins in a private entity like Mirza UK and deprive Mirza International of the additional profits.

1 Like

I have raised this as a red flag and this is a reason enough for me to stay away no matter how interesting the story is.

12 Likes

Generally banks do not fund receivables from related parties. These entities are in the restricted list for banks (as buyers and sellers) for financing working capital transactions. But if you are sure that PNB is doing it then I rest my case (somewhere above it was written that PNB is the only lender to the company). And if this is indeed what is happening, then it just goes to show the lax lending standards of pnb.

2 Likes

Of course one can ignore these red flags and some other issues like very high pay packets to the promoters and still make money in such stocks.

But I have generally seen that companies which don’t have very high governance standards will find ways to deprive the listed entity and enrich themselves personally when high profits do start coming into the listed company.

I prefer slightly quieter companies who don’t shout from the rooftops about being the next Nike or Adidas of the world. Instead, they quietly do their work and under promise and over achieve. A case in point being Page Industries which performs quietly (does not even conduct quarterly result con calls as they are more interested in running the company than wanting their share price to move up). The promoter of Page came of CNBC a few months back and mentioned that they should be able to achieve 20% growth every year and quietly went and grew profits by 30% in FY2018 and 45% in the 1st quarter of FY2019.

Will the promoters of Mirza International have the courage to say in their next quarterly con call that going forward, they will route sales through a new 100% sub of Mirza International and not Mirza UK which is owned by the promoters? And if not, they why not?

1 Like

Isn’t Mirza UK a subsidiary of MIL? If yes, then as pointed above PNB is leaving caution to winds!!

Few years ago, while working in a bank, I noticed similar discrepancy in Opto (setting up overseas subsidiaries in Singapore etc. Promoters and their relatives of Opto were directors of these entities). Sales were done to these entities and profits were booked(receivable position was ballooning yoy). Could not get fully comfortable with Opto at that time and we rejected the loan proposal.

Mirza may not be a same case and related party transactions are arm’s length . But it is always prudent to double check these things.

Disc: not invested in Mirza or Opto. Not a buy/sell reco. Kindly do your own due diligence.

If I understand this correctly, the net impact is that the loan taken (Bills discounted) will not show up as ‘Debt’ in the books of the company, but as Contingent Liabilities. Whatever inventory/receivables were used to acquire the loan should still show up in the books. Please help me understand how this will affect Working Capital (Receivables/Inventory) turns.

You can look up the net effect in Screener itself (By using the normal ‘D/E Ratio’ and comparing it with ‘debtplus’):

![]()

![]()

(Screener)

Going with the numbers (For 2017):

Mirza’s Equity: 504 Cr

Mirza’s ‘Borrowings’: 156 Cr

Mirza’s Contingent Liabilities (Bills Discounted): 178.09 Cr

So,

Normal D/E: 156/504 = 0.31

D/E w Contingent Liabilities = (178.09+156)/504 = 0.66 (Either my calculation or Screener’s is slightly off/using newer numbers)

Even if Mirza stops ‘selling’ to Mirza (UK), they can still avail loans off the inventory. Only this way, it will show up as ‘Debt’ in the books of the company. This is the net effect of this supposed ‘manipulation’. Correct me if I’m wrong.

In retrospect, I always consider Contingent Liabilities when calculating the D/E Ratio. It’s only logical do so. However, inquiry can be made about the nature of this debt, the repayment and so on in the next concall.

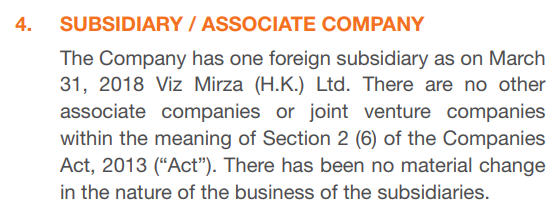

No, Mirza (UK) is a related party. A private entity with which MIL transacts (IIRC, Mirza UK’s sales are about 30% of MIL’s sales). Mirza (HK) is the only fully owned subsidiary.

5 Likes

Did some digging here and found some interesting reports which I feel, investors should definitely go through and may also check with company.

Mirza UK is held by a company called Tilbrook Enterprise Limited. Got their latest filings on the web

Tilbrook.pdf (1.2 MB)

Mirza uk.pdf (943.2 KB)

Now in Tilbrook accounts, they say there is no controlling party as in no majority shareholder (where as Mirza UK accounts say that Tilbrook is a controlling entity).

Interesting part here is Mr Rashid Ahmed Mirza (CEO/MD of Mirza India) has been named as person with significant control in Tilbrook

By this, as per accounting standards, Tilbrook may not qualify as related party to be mentioned in Mirza’s books. But, I feel Mr Rashid can still call the shots in both Mirza India and Tilbrook (and in turn Mirza UK).

In my experience, such related party transactions/sales would definitely need a deeper investigation to gain full comfort by an investor.

Disc: Not invested. Kindly do your own due diligence.

4 Likes

Mirza definitely didn’t have good corporate governance so far.

A clear example is promoters getting money for loan guarantee.

However, shuza mirza in latest concall clearly indicated that this should be removed soon.

Also, regarding UK entity- going forward, the majority sales will be from domestic anyways. FY 20 objectives is to have 60-65% domestic sales.

So, the importance of UK entity also fades away.

The picture looks like this- the older promoters were primarily running this as a B2B business and taking money out of company by way of commissions etc. There was no vision of making it big and running it professionally.

But, now the vision has changed to make it a branded consumer story and to run it professionally. Past sins will not go away in a day. Will take an year or two.

Also, note that promoter anyway owns 70%+ of the company. So, if they forego some amount of commissions and stop taking money out… They lose only 30% of it… But make 10-30x in the form of market cap increase. Other footwear companies trade at 2-4x valuations multiples. Mirza trades at low multiples because of these issues. Removing these issues will be lot more beneficial to promoters overall.

1 Like

First of all, I did not call this manipulation. This is clever working capital management and clever accounting.

This really depends on how you interpret the below statements.

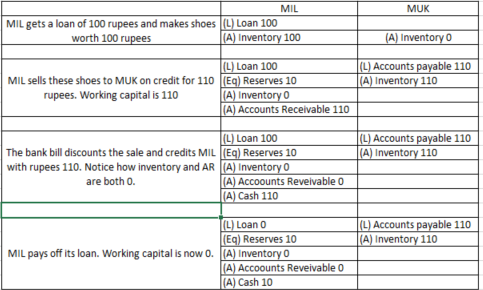

Here is my interpretation (I have tried to oversimplify this). This table below shows the current accounting practice. Again, this is entirely correct. Ind AS allows for this method of accounting (receivables covered by bills discounted are neither shown as assets nor liabilities).

And this table below shows how it should in effect be accounted ( I believe this is how it is done in the US GAAP, I could be wrong though).

You are right, from a D/E perspective including the contingent liabilities to derive ratios will give you the correct picture. Well, almost. The issue is, of the Rs.178 Crores bills discounted there might just be a portion of it which is a genuine sale to a distribution company elsewhere. But we would never know how much.

However, this method of accounting creates other issues.

- Notional profit - You’ll notice there is a notional profit of Rs.10 on the books now.

- Contingent liabilities are not part of the balance sheet. And this is a key issue, because it is skews the working capital calculation as shown on the table above.

- Inventory position isn’t accurate. Receivables position is also inaccurate.

- More importantly, and here is my biggest problem with all of this, if the going gets tough and Mirza UK defaults (they have no other sources for repayment), the listed business would take a hit. And this is very hard to see through as an individual investor.

There are other issues as well.

- Margin leakage,

![]()

- Inventory write off (at Mirza UK) and how this is accounted for in MIL

- Director’s salaries hidden on Mirza UK’s books

which will all need to be taken into consideration.

2 Likes

Page is just Indian distributor of International Jockey brand. Like Jubilant food works is Indian partner for International Dominoes. They didn’t build the brand. They just got lucky to partner with International brands and distribute their products.

To achieve a vision, you need to have it first. There is nothing wrong in seeing ones company in top league. If the top management will not have a vision, who will have it?

4 Likes

As you have shown, the Sales made to Mirza (UK) roughly matches the bills discounted. Whatever’s remaining, I’m sure, is too small to matter. You may question the activities of Mirza (India) choosing to sell to Mirza (UK) instead of some other distributor. But this is the very nature of related party transactions.

Isn’t this the case with any Account Receivable/Credit Sale? I fail to understand what’s wrong in a Credit Sale.

Once again, I fail to understand how this is a key issue. You have stated this is clever Working Capital management. If Mirza (India) is able to discount these bills, then it’s all the better anyway. From a calculation perspective, Mirza (India) follows the accounting practices allowed in India. The risk of these receivables are with the bank which discounted these receivables. Therefore, how prudent would it be for Mirza (India) to show this in their books?

Please do elaborate.

Nobody said Related Party Transactions are easily understandable. Going a bit with this, how many individual investors understand a BFSI firm’s activities completely? Yet the BFSI segment gets a very high inflow from retail investors. That’s why it’s prudent for a business to satisfy the investor’s queries through a concall or otherwise. If there’s no such outlet, only then it’s a genuine issue.

If I understand this, are you implying that by selling to Mirza (UK), Mirza (India) is hurting itself with poorer margins?

Mirza’s (India) margins has been fairly stable and even on a slight uptrend since the last many years. Mirza (India) largely sells to Mirza (UK). Whatever happens after this point only affects Mirza (UK). It is of no concern to Mirza (India) whether Mirza (UK) makes a higher margin than it does. Once again, this is the nature of Related Party Transactions.

Once again, re-valuation of inventors is a regular business activity. Let’s assume that these set of inventories never left Mirza (India). Would you find it any different if Mirza (India) itself re-valued the inventory? I personally wouldn’t. Since Mirza (UK) is a related, the disclosure requirements are being followed.

IIRC, 2 of Mirza (India) directors also sit at the board of Mirza (UK). So, they receive salaries in both the places. What is so wrong with that? I fail to understand how this salary is ‘hidden’.

3 Likes

You must have invested a lot of money in this company  I do appreciate the strong conviction.

I do appreciate the strong conviction.

We can both have an intellectual conversation all day long of what is and isn’t good practice. The truth of the matter is, our outlook on this is quite different. I’d personally not be able to sleep well investing in companies of this nature. I prefer simple businesses, with simpler balance sheets run professionally by an honest and transparent management team.

Now having said that, I have been wrong at least twice in the past. In the first instance the promoter was drawing a huge salary and there were significant related party transactions. In the second case, the promoter was controlling the overseas distributor and doing clever accounting to show negative working capital. In both cases, when the going was good, the stocks zoomed several times. (The businesses then slowed, receivables built up, margins cracked and the stocks have corrected 50% since, but that’s another story)

We need more data to analyse this further at least for academic purposes. But I hope, for your sake at least, that my concerns are unwarranted

Happy investing!

6 Likes

As someone has said, ‘Integrity is not a 90 percent thing, not a 95 percent thing; either you have it or you don’t.’

In case of Mirza International, the promoters clearly don’t seem to have it. The way they have been shortchanging the other 30% owners of the company all these years is shameful, to say the least. Skimming margins by having promoter owned overseas entities, paying themselves huge salaries, taking out funds by paying themselves guarantee commission, having high related parties transactions again to skim margins & maybe other ways to skim Mirza International that we may not be aware of.

Is Mr Suja Mirza waiting for a particular date after which Mirza International will become an ethical company?

And why is the leopard suddenly trying to change its spots? Is it just with an eye to get a higher market capitalization or is there a serious change of heart?

Right now, the overall markets seem to be on a good upward trend and the owners are suddenly realizing the benefits of coming clean. But a downtrend in the stock market & a recession in the economy will come sometime, though no one knows when. And that is when they will be go back to their old ways and again short change the 30% owners. Unfortunately for the promoters of Mirza, however hard they may try, the sad truth is that a leopard can never change its spots. The involvement of a large number of family members in the business will ensure that each looks after themselves well by skimming Mirza International.

6 Likes

That’s too bad. It doesn’t matter how much money I have on Mirza. Actually, I feel quite embarrassed that this is being made out to be about ownership bias. I was hoping to get to the bottom of your analysis, because it benefits everyone involved. Nothing’s better than a healthy discussion with two people with opposing view points.

Ciao.

5 Likes